Filed Pursuant to Rule

424(b)(3)

Registration No. 333-282803

PROSPECTUS

EON Resources Inc.

Up to 1,847,963 Shares of Class A Common Stock

This prospectus relates to

the offering from time to time by the selling securityholders named in this prospectus (the “Selling Securityholders”) of

up to an aggregate of 1,847,963 shares of our Class A Common Stock, par value $0.0001 per share (“Class A Common Stock”),

consisting of (i) 260,000 shares of Class A Common Stock issued to certain Selling Securityholders in exchange for forgiveness of accounts

payable (the “Exchange Shares”), (ii) 27,963 shares of Class A Common Stock (the “Pledge Shares”) issued to certain

Selling Securityholders in connection with their agreement to pledge equity in favor of First International Bank & Trust (“FIBT”),

(iii) 75,000 shares issued to a Selling Securityholder in connection with fees owed for consulting services (the “Consultant Shares”),

(iv) up to 75,000 shares of Class A Common Stock (the “Private Warrant Shares”) issuable upon exercise of certain private

warrants issued in connection with working capital loans (the “Private Warrants”) having an exercise price of $11.50 per share,

(v) 60,000 shares of Class A Common Stock issued to a Selling Securityholder in connection with a separation and release agreement (the

“2023 Settlement Agreement) effective December 17, 2023, and 150,000 shares of Class A Common Stock (together with the 60,000 shares,

the “Settlement Shares”) issued to a Selling Securityholder in connection with a settlement and mutual release agreement (the

“2024 Settlement Agreement” and together with the 2023 Settlement Agreement, the “Settlement Agreements”) effective

May 6, 2024, and (vi) up to 1,200,000 shares of Class A Common Stock (the “A/P Warrant Shares” and together with the Private

Warrant Shares, the “Warrant Shares”) issuable upon exercise of certain private warrants issued in connection with the forgiveness

of certain accounts payable (the “A/P Warrants”) having an exercise price of $0.75 per share.

The shares of Class A Common

Stock being registered for resale were issued to, purchased by or will be purchased by the Selling Securityholders for the following consideration:

(i) a purchase of price of $1.00 per share of Class A Common Stock for the Exchange Shares; (ii) the Pledge Shares were issued in consideration

for the agreement of those Selling Securityholders to place certain shares of Class A Common Stock into escrow and to agree to certain

obligations under the Loan Agreement (as defined herein), with an effective price of $2.01 per share of Class A Common Stock; (iii) the

Consultant Shares were issued in consideration for services rendered with an effective price of $2.06 per share of Class A Common Stock;

and (iv) the Settlement Shares were issued as a settlement of obligations with an effective price of $1.80 per share of Class A Common

Stock. The shares of Class A Common Stock underlying the Private Warrants will be purchased, if at all, by such holders at the $11.50

exercise price of the Private Warrants, and the Class A Common Stock underlying the A/P Warrants will be purchased, if at all, by such

holders at the exercise price of $0.75 of the A/P Warrants.

On November 15, 2023, we

completed the purchase of equity interests and transactions contemplated thereby (the “Purchase”) as set forth in that certain

Amended and Restated Membership Interest Purchase Agreement, dated August 28, 2023, as amended (the “MIPA”), by and among

us, HNRA Upstream, LLC, a newly formed Delaware limited liability company which is managed by us, and is a subsidiary of ours (“OpCo”),

and HNRA Partner, Inc., a newly formed Delaware corporation and wholly owned subsidiary of ours (“SPAC Subsidiary”, and together

with us and OpCo, “Buyer” and each a “Buyer”), CIC Pogo LP, a Delaware limited partnership (“CIC”),

DenCo Resources, LLC, a Texas limited liability company (“DenCo”), Pogo Resources Management, LLC, a Texas limited liability

company (“Pogo Management”), 4400 Holdings, LLC, a Texas limited liability company (“4400” and, together with

CIC, DenCo and Pogo Management, collectively, “Seller” and each a “Seller”), and, solely with respect to Section 6.20

of the MIPA, HNRAC Sponsors, LLC (the “Sponsor”).

We are registering the offer

and sale of the securities listed herein to satisfy certain registration rights we have granted. All of the securities being registered

for resale, when sold, will be sold by the Selling Securityholders. We are not selling any Class A Common Stock under this prospectus

and will not receive any of the proceeds from the sale or other disposition of shares by the Selling Securityholders except we will receive

the cash proceeds from any exercise of the Warrants, as we are registering for resale the shares underlying the Warrants.

The Selling Securityholders

may sell or otherwise dispose of the securities covered by this prospectus in a number of different ways. We provide more information

about how the Selling Securityholders may sell or otherwise dispose of their securities in the section entitled “Plan of Distribution”

on page 136. Discounts, concessions, commissions and similar selling expenses attributable to the sale of securities covered by this

prospectus will be borne by the Selling Securityholders. We will pay the expenses incurred in registering the shares of Class A Common

Stock covered by this prospectus, including legal and accounting fees. We will not be paying any underwriting discounts or commissions

in this offering to any person.

Our Class A Common Stock is listed

on NYSE American under the symbol “EONR” and our Public Warrants are listed on NYSE American under the symbol “EONR

WS”. On October 22, 2024, the last reported sale price for our Class A Common Stock was $1.29. Because, in the near term,

the exercise price of the Private Warrants are greater than the current market price of our Class A Common Stock, such Private Warrant

are unlikely to be exercised and therefore we do not expect to receive any proceeds from such exercise of the Private Warrants in the

near term. Any cash proceeds associated with the exercise of the Private Warrants are dependent on the stock price. Whether any holders

of Private Warrants determine to exercise such warrants, which would result in cash proceeds to us, will likely depend upon the market

price of our Class A Common Stock at the time of any such holder’s determination.

As of October 17, 2024, there were 9,104,972 shares of Class A Common

Stock outstanding. If all shares being registered hereby were sold, it would comprise approximately 17.8% of our total shares of Class

A Common Stock outstanding. Given the current market price of our Class A Common Stock, certain of the Selling Securityholders who paid

less for their shares than such current market price will receive a higher rate of return on any such sales than the public securityholders

who purchased Class A Common Stock in our initial public offering or any Selling Securityholder who paid more for their shares than the

current market price.

Investing in our Class

A Common Stock involves risks. See “Risk Factors” beginning on page 11.

We have not registered the

sale of the shares under the securities laws of any state. Brokers or dealers effecting transactions in the shares of Class A Common

Stock offered hereby should confirm that the shares have been registered under the securities laws of the state or states in which sales

of the shares occur as of the time of such sales, or that there is an available exemption from the registration requirements of the securities

laws of such states.

We have not authorized anyone,

including any salesperson or broker, to give oral or written information about this offering, EON Resources Inc., or the shares of Class

A Common Stock offered hereby that is different from the information included in this prospectus. You should not assume that the information

in this prospectus, or any supplement to this prospectus, is accurate at any date other than the date indicated on the cover page of

this prospectus or any supplement to it.

We are an “emerging

growth company,” as defined under the federal securities laws, and, as such, may elect to comply with certain reduced public company

reporting requirements for future filings.

Neither the SEC nor any

state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete.

Any representation to the contrary is a criminal offense.

The date of this prospectus is November 8, 2024.

TABLE OF CONTENTS

ABOUT THIS PROSPECTUS

This prospectus is part of

a registration statement on Form S-1 that we filed with the U.S. Securities Exchange Commission (the “SEC”), under which

the Selling Securityholders may, from time to time, sell the securities listed herein offered by them described in this prospectus. We

will not receive any proceeds from the sale by such Selling Securityholders of the securities offered by them described in this prospectus.

This prospectus also relates to the issuance by us of shares of Class A Common Stock issuable upon the exercise of the Private Warrants

and the A/P Warrants. We will receive proceeds to the extent there are any cash exercises of the Private Warrants and/or the A/P Warrants.

Neither we nor the Selling

Securityholders have authorized anyone to provide you with any information or to make any representations other than those contained

in this prospectus, any applicable prospectus supplement, or any free writing prospectuses prepared by or on behalf of us or to which

we have referred you. Neither we nor the Selling Securityholders take responsibility for, and can provide no assurance as to the reliability

of, any other information that others may give you. Neither we nor the Selling Securityholders will make an offer to sell these securities

in any jurisdiction where such offer or sale is not permitted. No dealer, salesperson, or other person is authorized to give any information

or to represent anything not contained in this prospectus, any applicable prospectus supplement or any related free writing prospectus.

You should assume that the information appearing in this prospectus or any prospectus supplement is accurate as of the date on the front

of those documents only, regardless of the time of delivery of this prospectus or any applicable prospectus supplement, or any sale of

a security. Our business, financial condition, results of operations, and prospects may have changed since those dates.

The Selling Securityholders

and their permitted transferees may use this registration statement to sell securities from time to time through any means described

in the section entitled “Plan of Distribution.” More specific terms of any securities that the Selling Securityholders

and their permitted transferees offer and sell may be provided in a prospectus supplement that describes, among other things, the specific

amounts and prices of the securities being offered and the terms of the offering.

We may also provide a prospectus

supplement or post-effective amendment to the registration statement to add information to, or update or change information contained

in, this prospectus. Any statement contained in this prospectus will be deemed to be modified or superseded for purposes of this prospectus

to the extent that a statement contained in such prospectus supplement or post-effective amendment modifies or supersedes such statement.

Any statement so modified will be deemed to constitute a part of this prospectus only as so modified, and any statement so superseded

will be deemed not to constitute a part of this prospectus. You should read both this prospectus and any applicable prospectus supplement

or post-effective amendment to the registration statement together with the additional information to which we refer you in the section

of this prospectus entitled “Where You Can Find More Information.”

This prospectus contains

summaries of certain provisions contained in some of the documents described herein, but reference is made to the actual documents for

complete information. All of the summaries are qualified in their entirety by the actual documents. Copies of some of the documents referred

to herein have been filed, will be filed, or will be incorporated by reference as exhibits to the registration statement of which this

prospectus is a part, and you may obtain copies of those documents as described below under “Where You Can Find More Information.”

CERTAIN TERMS

Unless otherwise stated in this prospectus,

or the context otherwise requires, references to:

| |

● |

“Class A Common Stock”

is to our Class A Common Stock, par value $0.0001 per share; |

| |

● |

“Class B Common Stock”

is to our Class B Common Stock, par value $0.0001 per share; |

| |

● |

“founder shares”

are to shares of our Class A Common Stock initially purchased by our sponsor in a private placement prior to our Initial Public Offering; |

| |

● |

“initial business

combination” or “Purchase” refers to the completion of our initial business combination on November 15, 2023, pursuant

to the closing of the transactions contemplated by the MIPA whereby we acquired (through our subsidiaries) 100% of the outstanding

membership interests of Pogo Resources, LLC, a Texas limited liability company (“Pogo” or the “Target”);

|

| |

|

|

| |

● |

“Initial Public Offering”

refers to the Initial Public Offering closed on February 15, 2022; |

| |

● |

“initial stockholders”

are to our holders of our founder shares prior to our Initial Public Offering (or their permitted transferees); |

| |

● |

“management”

or our “management team” are to our officers and directors; |

| |

● |

“MIPA” means

that that certain Amended and Restated Membership Interest Purchase Agreement, dated August 28, 2023, as amended (the “MIPA”),

by and among us, HNRA Upstream, LLC, a newly formed Delaware limited liability company which is managed by us, and is a subsidiary

of ours (“OpCo”), and HNRA Partner, Inc., a newly formed Delaware corporation and wholly owned subsidiary of ours (“SPAC

Subsidiary”, and together with us and OpCo, “Buyer” and each a “Buyer”), CIC Pogo LP, a Delaware limited

partnership (“CIC”), DenCo Resources, LLC, a Texas limited liability company (“DenCo”), Pogo Resources Management,

LLC, a Texas limited liability company (“Pogo Management”), 4400 Holdings, LLC, a Texas limited liability company (“4400”

and, together with CIC, DenCo and Pogo Management, collectively, “Seller” and each a “Seller”), and, solely

with respect to Section 6.20 of the MIPA, Sponsor. |

| |

|

|

| |

● |

“Predecessor”

refers to the historical business of Pogo prior to the Purchase on November 15, 2023. |

| |

|

|

| |

● |

“private placement

units” are to the units issued to our sponsor in a private placement simultaneously with the closing of our Initial Public

Offering; |

| |

● |

“private placement

warrants” are to the warrants sold as part of the private placement units, and to any private placement warrants or warrants

issued in connection with working capital loans that were sold to third parties, our executive officers, or our directors (or permitted

transferees). |

| |

● |

“public shares”

are to shares of our Class A Common Stock sold as part of the units in our Initial Public Offering (whether they were purchased in

our Initial Public Offering or thereafter in the open market); |

| |

● |

“public stockholders”

are to the holders of our public shares, including our initial stockholders and management team to the extent our initial stockholders

and/or members of our management team purchase public shares, provided that each initial stockholder’s and member of our management

team’s status as a “public stockholder” shall only exist with respect to such public shares; |

| |

● |

“public warrants”

are to our redeemable warrants sold as part of the units in our Initial Public Offering (whether they were purchased in our Initial

Public Offering or thereafter in the open market); |

| |

● |

“Sponsor” refers

to HNRAC Sponsors, LLC, a Delaware limited liability company; |

| |

● |

“warrants”

are to our redeemable warrants, which includes the public warrants as well as the private placement warrants to the extent they are

no longer held by the initial purchasers of the private placement units or their permitted transferees; |

| |

● |

“EON,” “EONR,”

“registrant,” “we,” “us,” “company” or “our company” “Successor”

are to EON Resources, Inc. (and the business of Pogo which became the business of the Company after giving effect to the Purchase). |

PROSPECTUS SUMMARY

This summary highlights

information contained elsewhere in this prospectus and may not contain all of the information that you should consider before investing

in the shares. You are urged to read this prospectus in its entirety, including the information under “Risk Factors” and

our financial statements and related notes included elsewhere in this Prospectus. Unless otherwise indicated, the estimates of our proved,

probable and possible reserves as of December 31, 2022 and 2023 were prepared by the third-party independent petroleum engineering firm

of William M. Cobb & Associates, Inc.

Overview

EON Resources, Inc. (f/k/a

HNR Acquisition Corp), was incorporated in Delaware as a blank check company formed for the purpose of effecting a merger, capital stock

exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more businesses or entities.

Prior to closing the Purchase, our efforts were limited to organizational activities, completion of an initial public offering and the

evaluation of possible business combinations. On February 15, 2022, we consummated the Initial Public Offering of 7,500,000 units (the

“Units”), at $10.00 per Unit, generating proceeds of $75,000,000. Additionally, the underwriter fully exercised its option

to purchase 1,125,000 additional Units, for which we received cash proceeds of $11,250,000. Simultaneously with the closing of the Initial

Public Offering, we consummated the sale of 505,000 private placement units at a price of $10.00 per unit generating proceeds of $5,050,000

in a private placement to our Sponsor and EF Hutton (formerly Kingswood Capital Markets) (“EF Hutton”). On April 4, 2022,

the Units separated into Class A Common Stock and warrants, and ceased trading. On April 4, 2022, the Class A Common Stock and Public

Warrants commenced trading on the NYSE American.

We identified Pogo as the

initial target for our initial business combination, and on November 15, 2023, we closed on the acquisition of Pogo. While we were permitted

to pursue an acquisition opportunity in any industry or sector, we focused on assets used in exploring, developing, producing, transporting,

storing, gathering, processing, fractionating, refining, distributing or marketing of natural gas, natural gas liquids, crude oil or

refined products in North America.

On September 16, 2024, we

filed a Certificate of Amendment to our Amended and Restated Certificate of Incorporation with the Secretary of State of the State of

Delaware to change our name from “HNR Acquisition Corp” to “EON Resources Inc.”, effective at 11:59PM on September

17, 2024. Following the change of our name from HNR Acquisition Corp to EON Resources Inc., effective at the beginning of trading on

September 18, 2024, our Class A Common Stock began trading on the NYSE American under the symbol “EONR” and our Public Warrants

began trading on the NYSE American under the symbol “EONR WS”. The CUSIP numbers for the Company’s Class A Common Stock

and Public Warrants did not change.

Purchase

On December 27, 2022,

we, entered into a Membership Interest Purchase Agreement (the “Original MIPA”) with CIC Pogo LP, a Delaware limited partnership

(“CIC”), DenCo Resources, LLC, a Texas limited liability company (“DenCo”), Pogo Resources Management, LLC, a

Texas limited liability company (“Pogo Management”), 4400 Holdings, LLC, a Texas limited liability company (“4400”

and, together with CIC, DenCo and Pogo Management, collectively, “Seller” and each a “Seller”), and, solely with

respect to Section 7.20 of the Original MIPA, HNRAC Sponsors LLC, a Delaware limited liability company (“Sponsor”).

On August 28, 2023, we, HNRA Upstream, LLC, a newly formed Delaware limited liability company which is managed by us, and is a subsidiary

of ours (“OpCo”), and HNRA Partner, Inc., a newly formed Delaware corporation and wholly owned subsidiary of ours (“SPAC

Subsidiary”, and together with us and OpCo, “Buyer” and each a “Buyer”), entered into an Amended and Restated

Membership Interest Purchase Agreement (the “A&R MIPA”) with Seller, and, solely with respect to Section 6.20 of

the A&R MIPA, the Sponsor, which amended and restated the Original MIPA in its entirety (as amended and restated, the “MIPA”).

Our stockholders approved the transactions contemplated by the MIPA at a special meeting of stockholders that was originally convened

October 30, 2023, adjourned, and then reconvened on November 13, 2023 (the “Special Meeting”).

On November 15, 2023 (the

“Closing Date”), as contemplated by the MIPA:

| |

● |

We filed a Second Amended

and Restated Certificate of Incorporation (the “Second A&R Charter”) with the Secretary of State of the State of

Delaware, pursuant to which the number of authorized shares of our capital stock, par value $0.0001 per share, was increased to 121,000,000

shares, consisting of (i) 100,000,000 shares of Class A Common Stock, (ii) 20,000,000 shares of Class B Common Stock, and (iii) 1,000,000

shares of preferred stock, par value $0.0001 per share; |

| |

● |

Our shares of common stock

were reclassified as Class A Common Stock; the Class B Common Stock has no economic rights but entitles its holder to one vote on

all matters to be voted on by stockholders generally; holders of shares of Class A Common Stock and shares of Class B Common Stock

will vote together as a single class on all matters presented to our stockholders for their vote or approval, except as otherwise

required by applicable law or by the Second A&R Charter; |

| |

● |

(A) We contributed to OpCo

(i) all of our assets (excluding our interests in OpCo and the aggregate amount of cash required to satisfy any exercise by our stockholders

of their Redemption Rights (as defined below)) and (ii) 2,000,000 newly issued shares of Class B Common Stock (such shares, the “Seller

Class B Shares”) and (B) in exchange therefor, OpCo issued to us a number of Class A common units of OpCo (the “OpCo

Class A Units”) equal to the number of total shares of Class A Common Stock issued and outstanding immediately after the closing

(the “Closing”) of the transactions contemplated by the MIPA (following the exercise by our stockholders of their Redemption

Rights) (such transactions, the “SPAC Contribution”); and |

| |

● |

Immediately following the

SPAC Contribution, OpCo contributed $900,000 to SPAC Subsidiary in exchange for 100% of the outstanding common stock of SPAC Subsidiary

(the “SPAC Subsidiary Contribution”); |

| |

● |

Immediately following the

SPAC Subsidiary Contribution, Seller sold, contributed, assigned, and conveyed to (A) OpCo, and OpCo acquired and accepted from Seller,

ninety-nine percent (99.0%) of the outstanding membership interests of Pogo Resources, LLC, a Texas limited liability company

(“Pogo” or the “Target”), and (B) SPAC Subsidiary, and SPAC Subsidiary purchased and accepted from Seller,

one percent (1.0%) of the outstanding membership interest of Target (together with the ninety-nine percent (99.0%) interest, the

“Target Interests”), in each case, in exchange for (x) $900,000 of the Cash Consideration (as defined below) in the case

of SPAC Subsidiary and (y) the remainder of the Aggregate Consideration (as defined below) in the case of OpCo (such transactions,

together with the SPAC Contribution and SPAC Subsidiary Contribution and the other transactions contemplated by the MIPA, the “Purchase”). |

The “Aggregate Consideration”

for the Target Interests was: (a) cash in the amount of $31,074,127 in immediately available funds (the “Cash Consideration”),

(b) 2,000,000 Class B common units of OpCo (“OpCo Class B Units”) valued at $10.00 per unit (the “Common Unit Consideration”),

which will be equal to and exchangeable into 2,000,000 shares of Class A Common Stock issuable upon exercise of the OpCo Exchange Right

(as defined below), as reflected in the amended and restated limited liability company agreement of OpCo that became effective at Closing

(the “A&R OpCo LLC Agreement”), (c) the Seller Class B Shares, (d) $15,000,000 payable through a promissory note to Seller

(the “Seller Promissory Note”), (e) 1,500,000 preferred units (the “OpCo Preferred Units” and together with the

Opco Class A Units and the OpCo Class B Units, the “OpCo Units”) of OpCo (the “Preferred Unit Consideration”,

and, together with the Common Unit Consideration, the “Unit Consideration”), and (f) an agreement for Buyer, on or before

November 21, 2023, to settle and pay to Seller $1,925,873 from sales proceeds received from oil and gas production attributable to Pogo,

including pursuant to its third party contract with affiliates of Chevron. At Closing, 500,000 Seller Class B Shares (the “Escrowed

Share Consideration”) were placed in escrow for the benefit of Buyer pursuant to an escrow agreement and the indemnity provisions

in the MIPA. The Aggregate Consideration is subject to adjustment in accordance with the MIPA.

In connection with the Purchase,

holders of 3,323,707 shares of common stock sold in our initial public offering (the “public shares”) properly exercised

their right to have their public shares redeemed (the “Redemption Rights”) for a pro rata portion of the trust account (the

“Trust Account”) which held the proceeds from our initial public offering, funds from our payments to extend the time to

consummate a business combination and interest earned, calculated as of two business days prior to the Closing, which was approximately

$10.95 per share, or $49,362,479 in the aggregate. The remaining balance in the Trust Account (after giving effect to the Redemption

Rights) was $12,979,300.

Immediately upon the Closing,

Pogo Royalty exercised the OpCo Exchange Right as it relates to 200,000 OpCo Class B units (and 200,000 shares of Class B Common Stock).

After giving effect to the Purchase, the redemption of public shares as described above and the exchange mentioned in the preceding sentence,

were (i) 5,097,009 shares of Class A Common Stock issued and outstanding, (ii) 1,800,000 shares of Class B Common Stock issued and outstanding

and (iii) no shares of preferred stock issued and outstanding.

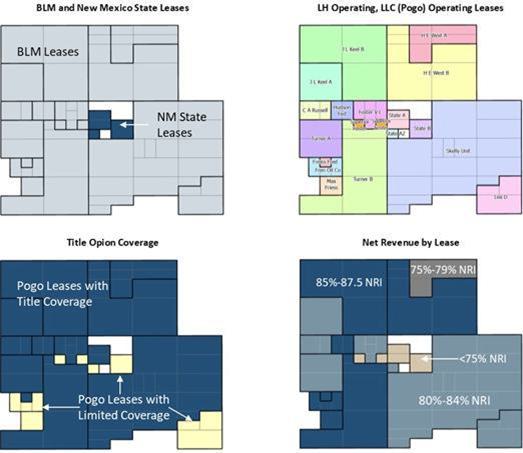

Pogo Overview

Pogo is an exploration and

production company that began operations in February 2017. Pogo is based in Dallas, Texas, and a field office in Loco Hills, New

Mexico. As of December 31, 2023, Pogo’s operating focus is the Northwest Shelf of the Permian Basin, with a specific emphasis

on oil and gas producing properties located in the Grayburg-Jackson Field in Eddy County, New Mexico. Pogo is the Operator of Record

of its oil and gas properties, operating its properties through its wholly owned subsidiary, LH Operating LLC. Pogo completed multiple

acquisitions in 2018 and 2019. These acquisitions included multiple producing properties in Lea and Eddy counties, New Mexico. In

2020, after identifying its core development property, Pogo successfully completed a series of divestures of its non-core properties.

Then, with one key asset, its Grayburg-Jackson Field in Eddy County, New Mexico, Pogo focused all of its efforts on developing this

asset. This has been Pogo’s focus for 2022 and 2023. Currently, Pogo and EON combined have 14 employees (5 executive officers where

4 are in Houston and 1 in Lubbock; 9 field staff in Loco Hills). From time to time, on an as needed basis, contract workers handle additional

necessary responsibilities.

Pogo owns, manages, and operates,

through its wholly owned subsidiary, LH Operating, LLC, 100% working interest in a gross 13,700 acres located on the Northwest Shelf

of the prolific oil and gas producing Permian Basin. Pogo benefits from cash flow growth through continued development of its working

interest’s ownership, with relatively low capital cost and lease operating expenses. As of December 31, 2023, average net

daily production associated with Pogo’s working interests was 1,022 barrel of oil equivalent (“BOE”) per day consisting

of 94% oil and 6% natural gas. Pogo expects to continue to grow its cash flow by production enhancements in its operations on its gross

13,700-acre leasehold. Furthermore, Pogo intends to make additional acquisitions within the Permian Basin, as well as other oil

and gas producing regions in the USA, that meet its investment criteria for minimum risk, geologic quality, operator capability, remaining

growth potential, cash flow generation and, most importantly, rate of return.

As of December 31, 2023,

100% of Pogo’s gross 13,700 leasehold acres were located in Eddy County, New Mexico, where there 100% of the leasehold working

interests owned by Pogo consist of state and federal lands. Pogo believes the Permian Basin offers some of the most compelling rates

of return for Pogo and significant potential for cash flow growth. As a result of compelling rates of return, development activity in

the Permian Basin has outpaced all other onshore U.S. oil and gas basins since the end of 2016. This development activity has driven

basin-level production to grow faster than production in the rest of the United States.

Pogo’s working interests

entitle it to receive an average of 97% of the net revenue from crude oil and natural gas produced from the oil and gas reservoirs underlying

its acreage. Pogo is not under any mandatory obligation to fund drilling and completion costs associated with oil and gas development

because 100% of its lease holdings are held by production. As a working interest owner with significant net earnings, Pogo seeks to fully

capture all remaining oil and gas reserves underlying its leasehold acres by systematically developing its low risk, predictable, proven

reserves by means of adding perforations in previously drilled and completed wells, were applicable, and drilling new wells in a predetermined

drilling pattern. Accordingly, Pogo’s development model generates strong margins greater than 60%, at low risk, predictable, production

outcomes that requires low overhead and is highly scalable. For the year ended December 31, 2023, Pogo’s lifting cost was

about $27.21 per barrel of oil equivalent at a realized price of $72.69 per BOE, excluding the impact of settled commodity derivatives.

Pogo is led by a management team with extensive oil and gas engineering, geologic and land expertise, long-standing industry relationships

and a history of successfully managing a portfolio of working and leasehold interests, producing crude oil and natural gas assets. Pogo

intends to capitalize on its management team’s expertise and relationships to increase production and cash flow in the field.

Pogo Business Strategies

Pogo’s primary business

objective is to generate discretionary cash flow by maintaining its strong cash flow from the PDP reserves and increasing cash flow by

developing predictable, low cost PDNP reserves in its Permian Basin asset. Pogo intends to accomplish this objective by executing the

following strategies:

Generate strong cash

flow supported by means of disciplined development of its PDNP Reserves. As the sole working interest owner, Pogo benefits from

the continued organic development of its acreage in the Permian Basin. As of December 31, 2023, Pogo, in conjunction with William

M. Cobb & Associates, Inc. (“Cobb & Associates”), a third-party engineering consulting firm, has confirmed that

Pogo has 115, low cost, well patterns to be developed during 2024 to 2027. The total costs to complete these 115 well patterns have been

predetermined by historical analysis. The estimated cost to complete each PDNP pattern is $345,652 and the estimated cost to complete

each PUD pattern is $1,187,698. A single well pattern consists of one each producing well with its corresponding or dedicated water injection

wells, with each injection well situated on four sides of the producing well. Water injection wells are necessary to maintain reservoir

pressure in its original state and to move the oil in place toward the producing well. Pressure maintenance helps ensure maximum oil

and gas recovery. Without pressure maintenance, oil recoveries from a producing oil reservoir generally do not exceed 10% of the original

oil in place (“OOIP”). With pressure maintenance by re-injecting produced water into the oil reservoir, then Pogo expects

to see ultimate oil recoveries 25% or greater of the OOIP. Offsetting oil wells on its leasehold also take advantage of the water

injected into the oil reservoir, and is able to convert a high percentage of its revenue to discretionary cash flow. Because Pogo owns

100% working interests it incurs 100% of the monthly leasehold operating costs for the production of crude oil and natural gas or capital

costs for the drilling and completion of wells on its acreage. Because these wells are shallow oil producers, with vertical depths between

1500 ft and 4000 ft, the monthly operating expenses are relatively low.

Focus primarily on

the Permian Basin. All of Pogo’s working interests are currently located in the Permian Basin, one of the most prolific

oil and gas basins in the United States. Pogo believes the Permian Basin provides an attractive combination of highly-economic and

oil-weighted geologic and reservoir properties, opportunities for development with significant inventory of drilling locations and

zones to be delineated our top-tier management team.

| |

● |

Business Relations.

Leverage expertise and relationships to continue acquiring Permian Basin targets with high working interests in actively producing

oil fields from top-tier E&P operators, with predictable, stable cash flow, and with significant growth potential. Pogo

has a history of evaluating, pursuing and consummating acquisitions of crude oil and natural gas targets in the Permian Basin and

other oil producing basins. Pogo’s management team intends to continue to apply this experience in a disciplined manner when

identifying and acquiring working interests. Pogo believes that the current market environment is favorable for oil and gas acquisitions

in the Permian Basin and other oil generating basins. Numerous asset packages from sellers presents attractive opportunities for

assets that meet Pogo’s target investment criteria. With sellers seeking to monetize their investments, Pogo intends to continue

to acquire working interests that have substantial resource potential in the Permian Basin. Pogo expects to focus on acquisitions

that complement its current footprint in the Permian Basin while targeting working interests underlying large scale, contiguous acreage

positions that have a history of predictable, stable oil and gas production rates, and with attractive growth potential. Furthermore,

Pogo seeks to maximize its return on capital by targeting acquisitions that meet the following criteria: |

| |

● |

sufficient visibility to

production growth; |

| |

● |

de-risked geology

supported by stable production; |

| |

● |

targets from top-tier E&P

operators; and |

| |

● |

a geographic footprint

that Pogo believes is complementary to its current Permian Basin asset and maximizes its potential for upside reserve and production

growth. |

Maintain conservative

and flexible capital structure to support Pogo’s business and facilitate long-term operations. Pogo is committed

to maintaining a conservative capital structure that will afford it the financial flexibility to execute its business strategies on an

ongoing basis. Pogo believes that internally generated cash flows from its working interests and operations, available borrowing capacity

under its revolving credit facility, and access to capital markets will provide it with sufficient liquidity and financial flexibility

to continue to acquire attractive targets with high working interests that will position it to grow its cash flows in order to distributed

to its shareholders as dividends and/or reinvested to further expand its base of cash flow generating assets. Pogo intends to maintain

a conservative leverage profile and utilize a mix of cash flows from operations and issuance of debt and equity securities to finance

future acquisitions.

SUMMARY RISK FACTORS

You should carefully read

this prospectus, including the section entitled “Risk Factors.” Certain of the key risks are summarized below.

| |

● |

Pogo’s producing

properties are located in the Permian Basin, making it vulnerable to risks associated with operating in a single geographic area. |

| |

● |

Title to the properties

in which Pogo is acquiring an interest may be impaired by title defects. |

| |

● |

Pogo depends on various

services for the development and production activities on the properties it operates. Substantially all Pogo’s revenue is derived

from these producing properties. A reduction in the expected number of wells to be developed on Pogo’s acreage by or the failure

of Pogo to develop and operate the wells on its acreage could have an adverse effect on its results of operations and cash flows

adequately and efficiently. |

| |

● |

Pogo’s identified

development activities are susceptible to uncertainties that could materially alter the occurrence or timing of their development

activities. |

| |

● |

Acquisitions and Pogo’s

development of Pogo’s leases will require substantial capital, and our company may be unable to obtain needed capital or financing

on satisfactory terms or at all. |

| |

● |

Pogo currently plans to

enter hedging arrangements with respect to the production of crude oil, and possibly natural gas which is a smaller portion of the

reserves. Pogo will mitigate the exposure to the impact of decreases in the prices by establishing a hedging plan and structure that

protects the earnings to a reasonable level, and the debt service requirements. |

| |

● |

Pogo’s estimated

reserves are based on many assumptions that may turn out to be inaccurate. Any material inaccuracies in these reserve estimates or

underlying assumptions will materially affect the quantities and present value of its reserves. |

| |

● |

We believe Pogo currently

has ineffective internal control over its financial reporting. |

| |

● |

A substantial majority

of Pogo’s revenues from crude oil and gas producing activities are derived from its operating properties that are based on

the price at which crude oil and natural gas produced from the acreage underlying its interests are sold. Prices of crude oil and

natural gas are volatile due to factors beyond Pogo’s control. A substantial or extended decline in commodity prices may adversely

affect Pogo’s business, financial condition, results of operations and cash flows. |

| |

● |

If commodity prices decrease

to a level such that Pogo’s future undiscounted cash flows from its properties are less than their carrying value, Pogo may

be required to take write-downs of the carrying values of its properties. |

| |

● |

The unavailability, high

cost or shortages of rigs, equipment, raw materials, supplies or personnel may restrict or result in increased costs to develop and

operate Pogo’s properties. |

| |

● |

The marketability of crude

oil and natural gas production is dependent upon transportation and processing and refining facilities, which Pogo cannot control.

Any limitation in the availability of those facilities could interfere with Pogo’s ability to market its production and

could harm Pogo’s business. |

| |

● |

Drilling for and producing

crude oil and natural gas are high-risk activities with many uncertainties that may materially adversely affect Pogo’s business,

financial condition, results of operations and cash flows. |

| |

● |

Crude oil and natural gas

operations are subject to various governmental laws and regulations. Compliance with these laws and regulations can be burdensome

and expensive for Pogo, and failure to comply could result in Pogo incurring significant liabilities, either of which may impact

its willingness to develop Pogo’s interests. |

| |

● |

Federal and state legislative

and regulatory initiatives relating to hydraulic fracturing could cause Pogo to incur increased costs, additional operating restrictions

or delays and have fewer potential development locations. |

| |

● |

The historical financial

results of EON included in this prospectus may not be indicative of what EON’s actual financial position or results of operations

would have been if it were a public company. |

| |

● |

Purchases made pursuant

to the Common Stock Purchase Agreement will be made at a discount to the volume weighted average price of Class A Common Stock, which

may result in negative pressure on the stock price. |

| |

|

|

| |

● |

It is not possible to predict

the actual number of shares of Class A Common Stock, if any, we will sell under the Common Stock Purchase Agreement to White Lion

or the actual gross proceeds resulting from those sales. |

| |

|

|

| |

● |

The sale and issuance of

Class A Common Stock to White Lion will cause dilution to our existing securityholders, and the resale of the Class A Common Stock

acquired by White Lion, or the perception that such resales may occur, could cause the price of our Class A Common Stock to decrease. |

ABOUT THIS OFFERING

This prospectus relates to

the offering of up to 1,847,963 shares of Class A Common Stock.

Resale Offering of Class A Common Stock |

| Shares

of Class A Common Stock Offered by the Selling Securityholders |

|

An aggregate of 1,847,963 shares of our Class A Common Stock, consisting

of (i) 260,000 shares of Class A Common Stock issued to certain Selling Securityholders in exchange for forgiveness of accounts payable

(the “Exchange Shares”), (ii) 27,963 shares of Class A Common Stock (the “Pledge Shares”) issued to certain Selling

Securityholders in connection with their agreement to pledge equity in favor of First International Bank & Trust (“FIBT”),

(iii) 75,000 shares issued to a Selling Securityholder in connection with fees owed for consulting services (the “Consultant Shares”),

(iv) up to 75,000 shares of Class A Common Stock issuable upon exercise of certain private warrants issued in connection with working

capital loans (the “Private Warrants”) having an exercise price of $11.50 per share, (v) 60,000 shares of Class A Common Stock

issued to a Selling Securityholder in connection with a separation and release agreement (the “2023 Settlement Agreement) effective

December 17, 2023, and 150,000 shares of Class A Common Stock (together with the 60,000 shares, the “Settlement Shares”) issued

to a Selling Securityholder in connection with a settlement and mutual release agreement (the “2024 Settlement Agreement”

and together with the 2023 Settlement Agreement, the “Settlement Agreements”) effective May 6, 2024, and (vi) up to 1,200,000

shares of Class A Common Stock (the “A/P Warrant Shares” and together with the Private Warrant Shares, the “Warrant

Shares”) issuable upon exercise of certain private warrants issued in connection with the forgiveness of certain accounts payable

(the “A/P Warrants”) having an exercise price of $0.75 per share. |

| |

|

|

| Terms

of the Offering |

|

The Selling Securityholders

will determine when and how they will dispose of the shares of Class A Common Stock registered under this prospectus for resale. |

| |

|

|

| Shares

of Common Stock Outstanding as of the Date of this Prospectus |

|

9,104,972 shares of Class

A Common Stock issued and outstanding and 500,000 shares of Class B Common Stock issued and outstanding. |

| |

|

|

| Exercise

Price of Warrants |

|

$11.50 per share for the Private Warrants, subject

to adjustments as described herein, and $0.75 per share for the A/P Warrants, subject to adjustments described herein.

On October 22, 2024, the last quoted sale

price for our Class A Common Stock as reported on NYSE American was $1.29 per share. Because, in the near term, the exercise price

of the Private Warrants is greater than the current market price of our Class A Common Stock, such warrants are unlikely to be

exercised and therefore we do not expect to receive any proceeds from such exercise of the Private Warrants in the near term.

Whether any holders of Private Warrants determine to exercise such warrants, which would result in cash proceeds to us, will likely

depend upon the market price of our Class A Common Stock at the time of any such holder’s determination. |

| Purchase

Price of Securities offered for Resale |

|

The shares of Class A Common Stock being registered

for resale were issued to, purchased by or will be purchased by the Selling Securityholders for the following consideration: (i) a purchase

of price of $1.00 per share of Class A Common Stock for the Exchange Shares; (ii) the Pledge Shares were issued in consideration for the

agreement of those Selling Securityholders to place certain shares of Class A Common Stock into escrow and to agree to certain obligations

under the Loan Agreement (as defined herein), with an effective price of $2.01 per share of Class A Common Stock; (iii) the Consultant

Shares were issued in consideration for services rendered with an effective price of $2.06 per share of Class A Common Stock; and (iv)

the Settlement Shares were issued as a settlement of obligations with an effective price of $1.80 per share of Class A Common Stock. The

shares of Class A Common Stock underlying the Private Warrants will be purchased, if at all, by such holders at the $11.50 exercise price

of the Private Warrants, and the shares of Class A Common Stock underlying the A/P Warrants will be purchased, if at all, by such holders

at the $0.75 exercise price of the A/P Warrants.

|

| Use

of Proceeds |

|

We will not receive any of the proceeds from

the resale of the shares offered by the Selling Securityholders. In the event any Warrants are exercised for cash, we would receive

the proceeds from any such cash exercise, provided, however, we will not receive any proceeds from the sale of the shares of Class

A Common Stock issuable upon such exercise. The exercise of the Warrants, and any proceeds we may receive from their exercise, are

highly dependent on the price of our shares of our Class A Common Stock and the spread between the exercise price of such securities

and the market price of our Class A Common Stock at the time of exercise. It is possible that we may never generate any cash proceeds

from the exercise of such Warrants.

|

| Market

for Class A Common Stock |

|

Our Class A Common Stock is currently listed

on NYSE American under the symbol “EONR” and our Public Warrants are currently listed on NYSE American under the symbol

“EONR WS”.

|

| Risk

Factors |

|

See the section titled “Risk Factors”

beginning on page 11 of this prospectus and other information included in this prospectus for a discussion of factors that you

should consider carefully before deciding to invest in our Class A Common Stock.

|

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL INFORMATION

OF EON RESOURCES INC.

The following table presents

selected historical consolidated financial data for the periods indicated. The summary historical consolidated financial data as of June

30, 2024 and for the six months ended June 30, 2024 (Successor) are derived from the Company’s unaudited consolidated financial

statements and related notes thereto. The summary historical consolidated financial data as of December 31, 2023 and for the period from

November 15, 2023 to December 31, 2023 (Successor) are derived from the Company’s audited consolidated financial statements and

related notes thereto. The summary historical consolidated financial data as of and for the three months ended March 31, 2024 are derived

from Pogo’s unaudited consolidated financial statements and related notes thereto. The summary historical consolidated financial

data as of and for the years ended December 31, 2022, 2021 and 2020 and for the period from January 1, 2023 to November 14,

2023 for the Predecessor are derived from Pogo’s audited consolidated financial statements and related notes thereto. The unaudited

and audited consolidated financial statements and related notes thereto for the are included elsewhere in this prospectus.

The Company’s historical

results are not necessarily indicative of the results that may be expected for any other period in the future. For a detailed discussion

of the summary historical financial data contained in the following table, please read “Management’s Discussion and Analysis

of Financial Condition and Results of Operations of Pogo.” The following table should also be read in conjunction with the historical

financial statements of Pogo included elsewhere in this prospectus. Among other things, the historical financial statements include more

detailed information regarding the basis of presentation for the information in the following table.

| | |

Successor | | |

Predecessor | |

| | |

Six

Months Ended

June 30, | | |

November 15,

2023 to

December 31, | | |

January 1,

2023 to

November 14, | | |

Year Ended

December 31, | |

| | |

2024 | | |

2023 | | |

2023 | | |

2022 | | |

2021 | | |

2020 | |

| Statement of Operations Data: | |

| | |

| | |

| | |

| | |

| | |

| |

| Revenues | |

| | |

| | |

| | |

| | |

| | |

| |

| Oil and gas revenues | |

$ | 10,163,801 | | |

$ | 2,584,115 | | |

$ | 23,666,074 | | |

$ | 39,941,778 | | |

$ | 23,966,375 | | |

$ | 8,202,200 | |

| Commodity derivative gain (loss) | |

| (2,080,725 | ) | |

| 340,808 | | |

| 51,957 | | |

| (4,793,790 | ) | |

| (5,704,113 | ) | |

| 1,239,436 | |

| Other revenue | |

| 260,818 | | |

| 50,738 | | |

| 520,451 | | |

| 255,952 | | |

| — | | |

| — | |

| Net revenues | |

| 8,343,894 | | |

| 2,975,661 | | |

| 24,238,482 | | |

| 35,403,940 | | |

| 18,262,262 | | |

| 9,441,636 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Expenses | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Production taxes, transportation and processing | |

| 837,265 | | |

| 226,062 | | |

| 2,117,800 | | |

| 3,484,477 | | |

| 2,082,371 | | |

| 825,525 | |

| Lease operating | |

| 4,393,699 | | |

| 1,453,367 | | |

| 8,692,752 | | |

| 8,418,739 | | |

| 5,310,139 | | |

| 4,148,592 | |

| Depreciation, depletion and amortization | |

| 998,616 | | |

| 352,127 | | |

| 1,497,749 | | |

| 1,613,402 | | |

| 4,783,832 | | |

| 2,207,963 | |

| Accretion of asset retirement obligations | |

| 73,531 | | |

| 11,062 | | |

| 848,040 | | |

| 1,575,296 | | |

| 368,741 | | |

| 117,562 | |

| General and administrative | |

| 4,633,486 | | |

| 3,553,117 | | |

| 3,700,267 | | |

| 2,953,202 | | |

| 1,862,969 | | |

| 1,468,615 | |

| Acquisition costs | |

| — | | |

| 9,999,860 | | |

| — | | |

| — | | |

| — | | |

| — | |

| Total operating expenses | |

| 10,936,597 | | |

| 15,595,595 | | |

| 16,856,608 | | |

| 18,045,116 | | |

| 14,408,052 | | |

| 8,768,257 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Operating income (loss) | |

| (2,592,703 | ) | |

| (12,619,934 | ) | |

| 7,381,874 | | |

| 17,358,824 | | |

| 3,854,210 | | |

| 673,379 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Other income (expenses) | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Change in fair value of warrant liability | |

| (346,888 | ) | |

| 187,704 | | |

| — | | |

| — | | |

| — | | |

| — | |

| Change in fair value of forward purchase agreement liability | |

| (325,472 | ) | |

| 3,268,581 | | |

| — | | |

| — | | |

| — | | |

| — | |

| Amortization of debt discount | |

| (1,475,257 | ) | |

| (1,191,553 | ) | |

| — | | |

| — | | |

| — | | |

| — | |

| Interest expense | |

| (3,890,899 | ) | |

| (1,043,312 | ) | |

| (1,834,208 | ) | |

| (1,076,060 | ) | |

| (498,916 | ) | |

| (176,853 | ) |

| Interest income | |

| 29,362 | | |

| 6,736 | | |

| 313,401 | | |

| — | | |

| — | | |

| — | |

| Gain on extinguishment of liabilities | |

| 1,720,000 | | |

| — | | |

| — | | |

| — | | |

| — | | |

| — | |

| Insurance policy recovery | |

| — | | |

| — | | |

| — | | |

| 2,000,000 | | |

| — | | |

| — | |

| Net gain (loss) on asset sales | |

| — | | |

| — | | |

| (816,011 | ) | |

| — | | |

| 69,486 | | |

| (2,706,642 | ) |

| Other income (expense) | |

| 1,506 | | |

| 2,937 | | |

| (74,193 | ) | |

| 13,238 | | |

| (22,294 | ) | |

| (94,643 | ) |

| Total other income (expenses) | |

| (4,287,648 | ) | |

| 1,231,093 | | |

| 2,411,011 | | |

| 937,178 | | |

| (451,724 | ) | |

| (2,978,138 | ) |

| Income (loss) before income taxes | |

| (6,880,351 | ) | |

| (11,388,841 | ) | |

| 4,970,863 | | |

| 18,296,002 | | |

| 3,402,486 | | |

| (2,304,759 | ) |

| Income tax provision | |

| 1,549,054 | | |

| 2,387,639 | | |

| — | | |

| — | | |

| — | | |

| — | |

| Net income (loss) | |

| (5,331,297 | ) | |

| (9,001,202 | ) | |

| 4,970,863 | | |

| 18,296,002 | | |

| 3,402,486 | | |

| (2,304,759 | ) |

| Net income (loss) attributable to noncontrolling

interests | |

| — | | |

| — | | |

| — | | |

| — | | |

| — | | |

| — | |

| Net income (loss) attributable to

EON Resources Inc. | |

$ | (5,331,297 | ) | |

$ | (9,001,202 | ) | |

$ | 4,970,863 | | |

$ | 18,296,002 | | |

$ | 3,402,486 | | |

$ | (2,304,759 | ) |

| | |

Successor | | |

Predecessor | |

| | |

Six

Months Ended

June 30, | | |

November 15,

2023 to

December 31, | | |

January 1,

2023 to

November 14, | | |

Year Ended

December 31, | |

| | |

2024 | | |

2023 | | |

2022 | | |

2022 | | |

2021 | | |

2020 | |

| Statement of Cash Flows Data: | |

| | |

| | |

| | |

| | |

| | |

| |

| Operating activities | |

$ | 2,250,267 | | |

$ | 484,474 | | |

$ | 8,190,563 | | |

$ | 18,651,132 | | |

$ | 9,719,795 | | |

$ | 3,186,518 | |

| Investing activities | |

| (1,212,769 | ) | |

| 18,296,176 | | |

| (6,960,555 | ) | |

| (20,700,859 | ) | |

| (24,260,882 | ) | |

| (8,104,490 | ) |

| Financing activities | |

| (1,479,204 | ) | |

| (17,866,128 | ) | |

| (3,000,000 | ) | |

| 3,000,000 | | |

| 15,500,000 | | |

| 4,029,508 | |

| Net cash provided (used) | |

$ | (441,706 | ) | |

$ | 914,522 | | |

$ | (1,769,992 | ) | |

$ | 950,273 | | |

$ | 958,913 | | |

$ | (888,464 | ) |

| | |

Successor | | |

Predecessor | |

| | |

As of

June 30, | | |

As of

December 31, | | |

As of December 31, | |

| | |

2024 | | |

2023 | | |

2022 | | |

2021 | | |

2020 | |

| Selected Balance Sheet Data: | |

| | |

| | |

| | |

| | |

| |

| Current assets | |

$ | 5,918,313 | | |

$ | 6,812,448 | | |

$ | 5,476,133 | | |

$ | 4,149,111 | | |

$ | 1,634,108 | |

| Crude oil and natural gas properties, successful efforts

method | |

| 95,981,206 | | |

| 93,837,245 | | |

| 55,206,917 | | |

| 41,847,223 | | |

| 21,023,568 | |

| Other assets | |

| 20,000 | | |

| 76,199 | | |

| 4,025,353 | | |

| 193,099 | | |

| 131,596 | |

| Current liabilities | |

| 38,470,967 | | |

| 20,113,049 | | |

| 4,225,474 | | |

| 8,601,758 | | |

| 4,228,246 | |

| Long-term liabilities | |

| 36,983,652 | | |

| 50,006,614 | | |

| 31,978,682 | | |

| 25,385,824 | | |

| 9,822,692 | |

| Total stockholders’ (deficit) equity attributable

to EON Resources Inc. (Successor) or Pogo (Predecessor) | |

| (6,941,514 | ) | |

| (2,800,185 | ) | |

| 28,504,247 | | |

| 12,201,851 | | |

| 8,738,334 | |

| Noncontrolling interest | |

| 33,406,414 | | |

| 33,406,414 | | |

| — | | |

| — | | |

| — | |

RISK FACTORS

An investment in our in

our Class A Common Stock involves a high degree of risk. The risks described below include all material risks to our company or to investors

in this offering that are known to our company. You should carefully consider such risks before participating in this offering. If any

of the following risks actually occur, our business, financial condition and results of operations could be materially harmed. As a result,

the trading price of our Class A Common Stock could decline, and you might lose all or part of your investment. When determining whether

to buy our Class A Common Stock, you should also refer to the other information in this prospectus, including our financial statements

and the related notes included elsewhere in this prospectus.

In addition to the other

information in this prospectus, you should carefully consider the following factors in evaluating us and our business. This prospectus

contains, in addition to historical information, forward-looking statements that involve risks and uncertainties, some of which are beyond

our control. Should one or more of these risks and uncertainties materialize or should underlying assumptions prove incorrect, our actual

results could differ materially. Factors that could cause or contribute to such differences include, but are not limited to, those discussed

below, as well as those discussed elsewhere in this prospectus, including the documents incorporated by reference.

There are risks associated

with investing in companies such as ours who are primarily engaged in research and development. In addition to risks which could apply

to any company or business, you should also consider the business we are in and the following:

Risks Related to Our Business

Pogo’s producing properties are located

in the Permian Basin, making it vulnerable to risks associated with operating in a single geographic area.

All of Pogo’s producing

properties are currently geographically concentrated in the Permian Basin. As a result of this concentration, Pogo may be disproportionately

exposed to the impact of regional supply and demand factors, delays or interruptions of production from wells in this area caused by

governmental regulation, processing or transportation capacity constraints, availability of equipment, facilities, personnel or services

market limitations, natural disasters, adverse weather conditions, plant closures for scheduled maintenance or interruption of the processing

or transportation of crude oil and natural gas. In addition, the effect of fluctuations on supply and demand may become more pronounced

within specific geographic crude oil and natural gas producing areas such as the Permian Basin, which may cause these conditions to occur

with greater frequency or magnify the effects of these conditions. Due to the concentrated nature of Pogo’s portfolio of properties,

a number of its properties could experience any of the same conditions at the same time, resulting in a relatively greater impact on

its results of operations than they might have on other companies that have a more diversified portfolio of properties. Such delays or

interruptions could have a material adverse effect on Pogo’s financial condition and results of operations.

As a result of Pogo’s

exclusive focus on the Permian Basin, it may be less competitive than other companies in bidding to acquire assets that include properties

both within and outside of that basin. Although Pogo is currently focused on the Permian Basin, it may from time to time evaluate and

consummate the acquisition of asset packages that include ancillary properties outside of that basin, which may result in the dilution

of its geographic focus.

Title to the properties in which Pogo is

acquiring an interest may be impaired by title defects.

Pogo is not required to,

and under certain circumstances it may elect not to, incur the expense of retaining lawyers to examine the title to its operating interests.

In such cases, Pogo would rely upon the judgment of oil and gas lease brokers or landmen who perform the fieldwork in examining records

in the appropriate governmental office before acquiring an operating interest. The existence of a material title deficiency can render

an interest worthless and can materially adversely affect Pogo’s results of operations, financial condition and cash flows. No

assurance can be given that Pogo will not suffer a monetary loss from title defects or title failure. Additionally, undeveloped acreage

has a greater risk of title defects than developed acreage. If there are any title defects in properties in which Pogo holds an interest,

it may suffer a financial loss.

Pogo depends on various services for the

development and production activities on the properties it operates. Substantially all Pogo’s revenue is derived from these producing

properties. A reduction in the expected number of wells to be developed on Pogo’s acreage by or the failure of Pogo to develop

and operate the wells on its acreage could have an adverse effect on its results of operations and cash flows adequately and efficiently.

Pogo’s assets consists

of operating interests. The failure of Pogo to perform operations adequately or efficiently or to act in ways that are not in Pogo’s

best interests could reduce production and revenues. Additionally, certain investors have requested that operators adopt initiatives

to return capital to investors, which could also reduce the capital available to Pogo for investment in development and production activities.

Moreover, should a low commodity price environment incur, Pogo may also opt to reduce development activity that could further reduce

production and revenues.

If production on Pogo acreage

decreases due to decreased development activities, because of a low commodity price environment, limited availability of development

capital, production-related difficulties or otherwise, Pogo’s results of operations may be adversely affected. Pogo is not

obligated to undertake any development activities other than those required to maintain their leases on Pogo’s acreage. In the

absence of a specific contractual obligation, any development and production activities will be subject to their reasonable discretion

(subject to certain implied obligations to develop imposed by the laws of some states). Pogo could determine to develop wells on Pogo’s

acreage than is currently expected. The success and timing of development activities on Pogo’s properties, depends on a number

of factors that are largely outside of Pogo’s control, including:

| |

● |

the capital

costs required for development activities on Pogo’s acreage, which could be significantly more than anticipated; |

| |

● |

the ability of Pogo to

access capital; |

| |

● |

prevailing commodity prices; |

| |

● |

the availability of suitable

equipment, production and transportation infrastructure and qualified operating personnel; |

| |

● |

the availability of storage

for hydrocarbons, Pogo’s expertise, operating efficiency and financial resources; |

| |

● |

Pogo’s expected return

on investment in wells developed on Pogo’s acreage as compared to opportunities in other areas; |

| |

● |

the selection of technology; |

| |

● |

the selection of counterparties

for the marketing and sale of production; |

| |

● |

and the rate of production

of the reserves. |

Pogo may elect not to undertake

development activities, or may undertake these activities in an unanticipated fashion, which may result in significant fluctuations in

Pogo’s results of operations and cash flows. Sustained reductions in production by Pogo on Pogo’s properties may also adversely

affect Pogo’s results of operations and cash flows. Additionally, if Pogo were to experience financial difficulty, Pogo might not

be able to pay invoices to continue its operations, which could have a material adverse impact on Pogo’s cash flows.

Pogo’s future success depends on

replacing reserves through acquisitions and the exploration and development activities.

Producing crude oil and natural

gas wells are characterized by declining production rates that vary depending upon reservoir characteristics and other factors. Pogo’s

future crude oil and natural gas reserves and Pogo’s production thereof and Pogo’s cash flows are highly dependent on the

successful development and exploitation of Pogo’s current reserves and its ability to successfully acquire additional reserves

that are economically recoverable. Moreover, the production decline rates of Pogo’s properties may be significantly higher than

currently estimated if the wells on its properties do not produce as expected. Pogo may also not be able to find, acquire or develop

additional reserves to replace the current and future production of its properties at economically acceptable terms. If Pogo is not able

to replace or grow its oil and natural gas reserves, its business, financial condition and results of operations would be adversely affected.

Pogo’s failure to successfully identify,

complete and integrate acquisitions of properties or businesses could materially and adversely affect its growth, results of operations

and cash flows.

Pogo depends, in part, on

acquisitions to grow its reserves, production and cash flows. Pogo’s decision to acquire a property will depend in part on the

evaluation of data obtained from production reports and engineering studies, geophysical and geological analyses and seismic data, and

other information, the results of which are often inconclusive and subject to various interpretations. The successful acquisition of

properties requires an assessment of several factors, including:

| |

● |

future crude oil and natural

gas prices and their applicable differentials; |

| |

● |

operating costs Pogo’s

E&P operators would incur to develop and operate the properties; |

| |

● |

and potential environmental

and other liabilities that E&P operators may incur. |

The accuracy of these assessments

is inherently uncertain and Pogo may not be able to identify attractive acquisition opportunities. In connection with these assessments,

Pogo performs a review of the subject properties that it believes to be generally consistent with industry practices, given the nature

of its interests. Pogo’s review will not reveal all existing or potential problems, nor will it permit it to become sufficiently

familiar with the properties to assess fully their deficiencies and capabilities. Inspections are often not performed on every well,

and environmental problems, such as groundwater contamination, are not necessarily observable even when an inspection is undertaken.

Even when problems are identified, the seller may be unwilling or unable to provide effective contractual protection against all or part

of the problems. Even if Pogo does identify attractive acquisition opportunities, it may not be able to complete the acquisition or do

so on commercially acceptable terms. Unless Pogo further develops its existing properties, it will depend on acquisitions to grow its

reserves, production and cash flow.

There is intense competition

for acquisition opportunities in Pogo’s industry. Competition for acquisitions may increase the cost of, or cause Pogo to refrain

from, completing acquisitions. Additionally, acquisition opportunities vary over time. Pogo’s ability to complete acquisitions

is dependent upon, among other things, its ability to obtain debt and equity financing and, in some cases, regulatory approvals. Further,

these acquisitions may be in geographic regions in which Pogo does not currently hold assets, which could result in unforeseen operating

difficulties. In addition, if Pogo acquires interests in new states, it may be subject to additional and unfamiliar legal and regulatory

requirements. Compliance with regulatory requirements may impose substantial additional obligations on Pogo and its management, cause

it to expend additional time and resources in compliance activities and increase its exposure to penalties or fines for non-compliance with

such additional legal requirements. Further, the success of any completed acquisition will depend on Pogo’s ability to effectively

integrate the acquired business into its existing business. The process of integrating acquired businesses may involve unforeseen difficulties

and may require a disproportionate amount of Pogo’s managerial and financial resources. In addition, potential future acquisitions

may be larger and for purchase prices significantly higher than those paid for earlier acquisitions.

No assurance can be given

that Pogo will be able to identify suitable acquisition opportunities, negotiate acceptable terms, obtain financing for acquisitions

on acceptable terms or successfully acquire identified targets. Pogo’s failure to achieve consolidation savings, to integrate the

acquired assets into its existing operations successfully or to minimize any unforeseen difficulties could materially and adversely affect

its financial condition, results of operations and cash flows. The inability to effectively manage these acquisitions could reduce Pogo’s

focus on subsequent acquisitions and current operations, which, in turn, could negatively impact its growth, results of operations and

cash flows.

Pogo may acquire properties that do not

produce as projected, and it may be unable to determine reserve potential, identify liabilities associated with such properties or obtain

protection from sellers against such liabilities.

Acquiring crude oil and natural

gas properties requires Pogo to assess reservoir and infrastructure characteristics, including recoverable reserves, development and

operating costs and potential environmental and other liabilities. Such assessments are inexact and inherently uncertain. In connection

with the assessments, Pogo performs a review of the subject properties, but such a review will not necessarily reveal all existing or

potential problems. In the course of Pogo’s due diligence, it may not inspect every well or pipeline. Pogo cannot necessarily observe

structural and environmental problems, such as pipe corrosion, when an inspection is made. Pogo may not be able to obtain contractual

indemnities from the seller for liabilities created prior to its purchase of the property. Pogo may be required to assume the risk of

the physical condition of the properties in addition to the risk that the properties may not perform in accordance with its expectations.

Any acquisitions that Pogo completes will

be subject to substantial risks.

Even if Pogo makes acquisitions

that it believes will increase its cash generated from operations, these acquisitions may nevertheless result in a decrease in its cash

flows. Any acquisition involves potential risks, including, among other things:

| |

● |

the validity of Pogo’s

assumptions about estimated proved reserves, future production, prices, revenues, capital expenditures, the operating expenses and

costs to develop the reserves; |

| |

● |

a decrease in Pogo’s

liquidity by using a significant portion of its cash generated from operations or borrowing capacity to finance acquisitions; |

| |

● |

a significant increase

in Pogo’s interest expense or financial leverage if it incurs debt to finance acquisitions; |

| |

● |

the assumption of unknown

liabilities, losses or costs for which Pogo is not indemnified or for which any indemnity it receives is inadequate; |

| |

● |

mistaken assumptions about

the overall cost of equity or debt; |

| |

● |

Pogo’s ability to

obtain satisfactory title to the assets it acquires; |

| |

● |

an inability to hire, train

or retain qualified personnel to manage and operate Pogo’s growing business and assets; |

| |

● |

and the occurrence of other

significant changes, such as impairment of crude oil and natural gas properties, goodwill or other intangible assets, asset devaluation

or restructuring charges. |

Pogo’s identified development activities

are susceptible to uncertainties that could materially alter the occurrence or timing of their development activities.

The ability of Pogo to perform

development activities depends on a number of uncertainties, including the availability of capital, construction of and limitations on

access to infrastructure, inclement weather, regulatory changes and approvals, crude oil and natural gas prices, costs, development activity

results and the availability of water. Further, Pogo’s identified potential development activities are in various stages of evaluation,

ranging from wells that are ready to be developed to wells that require substantial additional interpretation. The use of technologies