false

2023

FY

0001949478

0001949478

2023-01-01

2023-12-31

0001949478

dei:BusinessContactMember

2023-01-01

2023-12-31

0001949478

2023-12-31

0001949478

2022-12-31

0001949478

2021-01-01

2021-12-31

0001949478

2022-01-01

2022-12-31

0001949478

us-gaap:CommonStockMember

2020-12-31

0001949478

us-gaap:AdditionalPaidInCapitalMember

2020-12-31

0001949478

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2020-12-31

0001949478

DTCK:MergerReserveMember

2020-12-31

0001949478

us-gaap:RetainedEarningsMember

2020-12-31

0001949478

2020-12-31

0001949478

us-gaap:CommonStockMember

2021-12-31

0001949478

us-gaap:AdditionalPaidInCapitalMember

2021-12-31

0001949478

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2021-12-31

0001949478

DTCK:MergerReserveMember

2021-12-31

0001949478

us-gaap:RetainedEarningsMember

2021-12-31

0001949478

2021-12-31

0001949478

us-gaap:CommonStockMember

2022-12-31

0001949478

us-gaap:AdditionalPaidInCapitalMember

2022-12-31

0001949478

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-12-31

0001949478

DTCK:MergerReserveMember

2022-12-31

0001949478

us-gaap:RetainedEarningsMember

2022-12-31

0001949478

us-gaap:CommonStockMember

2021-01-01

2021-12-31

0001949478

us-gaap:AdditionalPaidInCapitalMember

2021-01-01

2021-12-31

0001949478

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2021-01-01

2021-12-31

0001949478

DTCK:MergerReserveMember

2021-01-01

2021-12-31

0001949478

us-gaap:RetainedEarningsMember

2021-01-01

2021-12-31

0001949478

us-gaap:CommonStockMember

2022-01-01

2022-12-31

0001949478

us-gaap:AdditionalPaidInCapitalMember

2022-01-01

2022-12-31

0001949478

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-01-01

2022-12-31

0001949478

DTCK:MergerReserveMember

2022-01-01

2022-12-31

0001949478

us-gaap:RetainedEarningsMember

2022-01-01

2022-12-31

0001949478

us-gaap:CommonStockMember

2023-01-01

2023-12-31

0001949478

us-gaap:AdditionalPaidInCapitalMember

2023-01-01

2023-12-31

0001949478

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-01-01

2023-12-31

0001949478

DTCK:MergerReserveMember

2023-01-01

2023-12-31

0001949478

us-gaap:RetainedEarningsMember

2023-01-01

2023-12-31

0001949478

us-gaap:CommonStockMember

2023-12-31

0001949478

us-gaap:AdditionalPaidInCapitalMember

2023-12-31

0001949478

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-12-31

0001949478

DTCK:MergerReserveMember

2023-12-31

0001949478

us-gaap:RetainedEarningsMember

2023-12-31

0001949478

2022-09-30

0001949478

DTCK:MaxwillPteLtdMember

2023-01-01

2023-12-31

0001949478

DTCK:MaxwillPteLtdMember

2022-01-01

2022-12-31

0001949478

DTCK:MaxwillAsiaPteLtdMember

2023-01-01

2023-12-31

0001949478

DTCK:MaxwillAsiaPteLtdMember

2022-01-01

2022-12-31

0001949478

DTCK:LpGracePteLtdMember

2023-01-01

2023-12-31

0001949478

DTCK:LpGracePteLtdMember

2022-01-01

2022-12-31

0001949478

DTCK:MaxwillFoodlinkPteLtdMember

2023-01-01

2023-12-31

0001949478

DTCK:MaxwillFoodlinkPteLtdMember

2022-01-01

2022-12-31

0001949478

DTCK:DavisCommoditiesPteLtdMember

2023-01-01

2023-12-31

0001949478

DTCK:DavisCommoditiesPteLtdMember

2022-01-01

2022-12-31

0001949478

DTCK:YearEndMember

2023-12-31

0001949478

DTCK:YearEndMember

2022-12-31

0001949478

DTCK:AverageRateMember

2023-12-31

0001949478

DTCK:AverageRateMember

2022-12-31

0001949478

currency:SGD

2023-12-31

0001949478

currency:SGD

2022-12-31

0001949478

DTCK:InvestmentPropertyMember

2023-01-01

2023-12-31

0001949478

DTCK:RightOfUseAssetMember

2023-01-01

2023-12-31

0001949478

DTCK:FurnitureAndFittingsMember

2023-01-01

2023-12-31

0001949478

DTCK:MotorVehicleMember

2023-01-01

2023-12-31

0001949478

us-gaap:MaturityUpTo30DaysMember

2022-12-31

0001949478

us-gaap:MaturityUpTo30DaysMember

2023-12-31

0001949478

DTCK:Maturity31To60DaysMember

2022-12-31

0001949478

DTCK:Maturity31To60DaysMember

2023-12-31

0001949478

DTCK:Maturity61To90DaysMember

2022-12-31

0001949478

DTCK:Maturity61To90DaysMember

2023-12-31

0001949478

us-gaap:MaturityOver90DaysMember

2022-12-31

0001949478

us-gaap:MaturityOver90DaysMember

2023-12-31

0001949478

us-gaap:DepositsMember

2022-12-31

0001949478

us-gaap:DepositsMember

2023-12-31

0001949478

DTCK:GSTReceivableMember

2022-12-31

0001949478

DTCK:GSTReceivableMember

2023-12-31

0001949478

DTCK:MarginDepositsMember

2022-12-31

0001949478

DTCK:MarginDepositsMember

2023-12-31

0001949478

DTCK:OtherReceivablesThirdPartiesMember

2022-12-31

0001949478

DTCK:OtherReceivablesThirdPartiesMember

2023-12-31

0001949478

DTCK:OtherReceivablesRelatedPartyMember

2022-12-31

0001949478

DTCK:OtherReceivablesRelatedPartyMember

2023-12-31

0001949478

DTCK:PrepaymentToSuppliersThirdPartiesMember

2022-12-31

0001949478

DTCK:PrepaymentToSuppliersThirdPartiesMember

2023-12-31

0001949478

DTCK:LoanToARelatedPartyMember

2022-12-31

0001949478

DTCK:LoanToARelatedPartyMember

2023-12-31

0001949478

DTCK:InvestmentPropertyMember

2022-12-31

0001949478

DTCK:InvestmentPropertyMember

2023-12-31

0001949478

us-gaap:ComputerEquipmentMember

2022-12-31

0001949478

us-gaap:ComputerEquipmentMember

2023-12-31

0001949478

us-gaap:BuildingImprovementsMember

2022-12-31

0001949478

us-gaap:BuildingImprovementsMember

2023-12-31

0001949478

us-gaap:OfficeEquipmentMember

2022-12-31

0001949478

us-gaap:OfficeEquipmentMember

2023-12-31

0001949478

us-gaap:FurnitureAndFixturesMember

2022-12-31

0001949478

us-gaap:FurnitureAndFixturesMember

2023-12-31

0001949478

us-gaap:VehiclesMember

2022-12-31

0001949478

us-gaap:VehiclesMember

2023-12-31

0001949478

us-gaap:VehiclesMember

2023-07-16

2023-07-17

0001949478

us-gaap:VehiclesMember

2023-07-17

0001949478

DTCK:MotorVehicleMember

2022-12-31

0001949478

DTCK:MotorVehicleMember

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoanMember

2022-01-01

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoanMember

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoan1Member

2022-01-01

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoan1Member

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoan2Member

2022-01-01

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoan2Member

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoanMember

2023-01-01

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoanMember

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoan1Member

2023-01-01

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoan1Member

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoan2Member

2023-01-01

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoan2Member

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoanMember

DTCK:DebtInstrumentsPeriodWithInOneYearMember

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoanMember

DTCK:DebtInstrumentsPeriodTwoYearsMember

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoanMember

DTCK:DebtInstrumentsPeriodThreeYearsMember

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoanMember

DTCK:DebtInstrumentsPeriodFourYearsMember

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoanMember

DTCK:DebtInstrumentsPeriodFiveYearsMember

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoan1Member

DTCK:DebtInstrumentsPeriodWithInOneYearMember

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoan1Member

DTCK:DebtInstrumentsPeriodTwoYearsMember

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoan1Member

DTCK:DebtInstrumentsPeriodThreeYearsMember

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoan1Member

DTCK:DebtInstrumentsPeriodFourYearsMember

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoan1Member

DTCK:DebtInstrumentsPeriodFiveYearsMember

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoan2Member

DTCK:DebtInstrumentsPeriodWithInOneYearMember

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoan2Member

DTCK:DebtInstrumentsPeriodTwoYearsMember

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoan2Member

DTCK:DebtInstrumentsPeriodThreeYearsMember

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoan2Member

DTCK:DebtInstrumentsPeriodFourYearsMember

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoan2Member

DTCK:DebtInstrumentsPeriodFiveYearsMember

2022-12-31

0001949478

DTCK:DebtInstrumentsPeriodWithInOneYearMember

2022-12-31

0001949478

DTCK:DebtInstrumentsPeriodTwoYearsMember

2022-12-31

0001949478

DTCK:DebtInstrumentsPeriodThreeYearsMember

2022-12-31

0001949478

DTCK:DebtInstrumentsPeriodFourYearsMember

2022-12-31

0001949478

DTCK:DebtInstrumentsPeriodFiveYearsMember

2022-12-31

0001949478

DTCK:SecuredFixedRateBankLoanMember

DTCK:DebtInstrumentsPeriodWithInOneYearMember

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoanMember

DTCK:DebtInstrumentsPeriodTwoYearsMember

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoanMember

DTCK:DebtInstrumentsPeriodThreeYearsMember

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoanMember

DTCK:DebtInstrumentsPeriodFourYearsMember

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoanMember

DTCK:DebtInstrumentsPeriodFiveYearsMember

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoan1Member

DTCK:DebtInstrumentsPeriodWithInOneYearMember

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoan1Member

DTCK:DebtInstrumentsPeriodTwoYearsMember

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoan1Member

DTCK:DebtInstrumentsPeriodThreeYearsMember

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoan1Member

DTCK:DebtInstrumentsPeriodFourYearsMember

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoan1Member

DTCK:DebtInstrumentsPeriodFiveYearsMember

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoan2Member

DTCK:DebtInstrumentsPeriodWithInOneYearMember

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoan2Member

DTCK:DebtInstrumentsPeriodTwoYearsMember

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoan2Member

DTCK:DebtInstrumentsPeriodThreeYearsMember

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoan2Member

DTCK:DebtInstrumentsPeriodFourYearsMember

2023-12-31

0001949478

DTCK:SecuredFixedRateBankLoan2Member

DTCK:DebtInstrumentsPeriodFiveYearsMember

2023-12-31

0001949478

DTCK:DebtInstrumentsPeriodWithInOneYearMember

2023-12-31

0001949478

DTCK:DebtInstrumentsPeriodTwoYearsMember

2023-12-31

0001949478

DTCK:DebtInstrumentsPeriodThreeYearsMember

2023-12-31

0001949478

DTCK:DebtInstrumentsPeriodFourYearsMember

2023-12-31

0001949478

DTCK:DebtInstrumentsPeriodFiveYearsMember

2023-12-31

0001949478

DTCK:AccruedOperatingExpensesMember

2022-12-31

0001949478

DTCK:AccruedOperatingExpensesMember

2023-12-31

0001949478

DTCK:DeferredRevenueMember

2022-12-31

0001949478

DTCK:DeferredRevenueMember

2023-12-31

0001949478

DTCK:AdvancesFromCustomersMember

2022-12-31

0001949478

DTCK:AdvancesFromCustomersMember

2023-12-31

0001949478

DTCK:UnrealizedLossesOnCommodityFurtureContractsMember

2022-12-31

0001949478

DTCK:UnrealizedLossesOnCommodityFurtureContractsMember

2023-12-31

0001949478

DTCK:GSTPayablesMember

2022-12-31

0001949478

DTCK:GSTPayablesMember

2023-12-31

0001949478

DTCK:OtherPayablesThirdPartiesMember

2022-12-31

0001949478

DTCK:OtherPayablesThirdPartiesMember

2023-12-31

0001949478

DTCK:OtherPayablesRelatedPartyMember

2022-12-31

0001949478

DTCK:OtherPayablesRelatedPartyMember

2023-12-31

0001949478

DTCK:SpouseChairwomanMember

2023-12-31

0001949478

DTCK:ProvisionsMember

2020-12-31

0001949478

DTCK:TaxLossesMember

2020-12-31

0001949478

DTCK:ProvisionsMember

2021-01-01

2021-12-31

0001949478

DTCK:TaxLossesMember

2021-01-01

2021-12-31

0001949478

DTCK:ProvisionsMember

2021-12-31

0001949478

DTCK:TaxLossesMember

2021-12-31

0001949478

DTCK:ProvisionsMember

2022-01-01

2022-12-31

0001949478

DTCK:TaxLossesMember

2022-01-01

2022-12-31

0001949478

DTCK:ProvisionsMember

2022-12-31

0001949478

DTCK:TaxLossesMember

2022-12-31

0001949478

DTCK:ProvisionsMember

2023-01-01

2023-12-31

0001949478

DTCK:TaxLossesMember

2023-01-01

2023-12-31

0001949478

DTCK:ProvisionsMember

2023-12-31

0001949478

DTCK:TaxLossesMember

2023-12-31

0001949478

2023-09-20

2023-09-21

0001949478

DTCK:SaleOfSugarMember

2021-01-01

2021-12-31

0001949478

DTCK:SaleOfSugarMember

2022-01-01

2022-12-31

0001949478

DTCK:SaleOfSugarMember

2023-01-01

2023-12-31

0001949478

DTCK:SaleOfRiceMember

2021-01-01

2021-12-31

0001949478

DTCK:SaleOfRiceMember

2022-01-01

2022-12-31

0001949478

DTCK:SaleOfRiceMember

2023-01-01

2023-12-31

0001949478

DTCK:SaleOfOilsAndFatsMember

2021-01-01

2021-12-31

0001949478

DTCK:SaleOfOilsAndFatsMember

2022-01-01

2022-12-31

0001949478

DTCK:SaleOfOilsAndFatsMember

2023-01-01

2023-12-31

0001949478

DTCK:SaleOfOthersMember

2021-01-01

2021-12-31

0001949478

DTCK:SaleOfOthersMember

2022-01-01

2022-12-31

0001949478

DTCK:SaleOfOthersMember

2023-01-01

2023-12-31

0001949478

srt:AfricaMember

2021-01-01

2021-12-31

0001949478

srt:AfricaMember

2022-01-01

2022-12-31

0001949478

srt:AfricaMember

2023-01-01

2023-12-31

0001949478

country:CN

2021-01-01

2021-12-31

0001949478

country:CN

2022-01-01

2022-12-31

0001949478

country:CN

2023-01-01

2023-12-31

0001949478

country:ID

2021-01-01

2021-12-31

0001949478

country:ID

2022-01-01

2022-12-31

0001949478

country:ID

2023-01-01

2023-12-31

0001949478

country:VN

2021-01-01

2021-12-31

0001949478

country:VN

2022-01-01

2022-12-31

0001949478

country:VN

2023-01-01

2023-12-31

0001949478

country:PH

2021-01-01

2021-12-31

0001949478

country:PH

2022-01-01

2022-12-31

0001949478

country:PH

2023-01-01

2023-12-31

0001949478

country:TH

2021-01-01

2021-12-31

0001949478

country:TH

2022-01-01

2022-12-31

0001949478

country:TH

2023-01-01

2023-12-31

0001949478

country:SG

2021-01-01

2021-12-31

0001949478

country:SG

2022-01-01

2022-12-31

0001949478

country:SG

2023-01-01

2023-12-31

0001949478

DTCK:OtherCountriesMember

2021-01-01

2021-12-31

0001949478

DTCK:OtherCountriesMember

2022-01-01

2022-12-31

0001949478

DTCK:OtherCountriesMember

2023-01-01

2023-12-31

0001949478

us-gaap:TransferredAtPointInTimeMember

DTCK:SaleOfSugarMember

2023-01-01

2023-12-31

0001949478

us-gaap:TransferredAtPointInTimeMember

DTCK:SaleOfRiceMember

2023-01-01

2023-12-31

0001949478

us-gaap:TransferredAtPointInTimeMember

DTCK:SaleOfOilsAndFatsMember

2023-01-01

2023-12-31

0001949478

us-gaap:TransferredAtPointInTimeMember

DTCK:SaleOfOthersMember

2023-01-01

2023-12-31

0001949478

us-gaap:TransferredAtPointInTimeMember

DTCK:SaleOfSugarMember

2022-01-01

2022-12-31

0001949478

us-gaap:TransferredAtPointInTimeMember

DTCK:SaleOfRiceMember

2022-01-01

2022-12-31

0001949478

us-gaap:TransferredAtPointInTimeMember

DTCK:SaleOfOilsAndFatsMember

2022-01-01

2022-12-31

0001949478

us-gaap:TransferredAtPointInTimeMember

DTCK:SaleOfOthersMember

2022-01-01

2022-12-31

0001949478

us-gaap:TransferredAtPointInTimeMember

DTCK:SaleOfSugarMember

2021-01-01

2021-12-31

0001949478

us-gaap:TransferredAtPointInTimeMember

DTCK:SaleOfRiceMember

2021-01-01

2021-12-31

0001949478

us-gaap:TransferredAtPointInTimeMember

DTCK:SaleOfOilsAndFatsMember

2021-01-01

2021-12-31

0001949478

us-gaap:TransferredAtPointInTimeMember

DTCK:SaleOfOthersMember

2021-01-01

2021-12-31

0001949478

DTCK:CurrentAssetMember

2022-01-01

2022-12-31

0001949478

DTCK:CurrentAssetMember

2023-01-01

2023-12-31

0001949478

DTCK:CurrentLiabilityMember

2022-01-01

2022-12-31

0001949478

DTCK:CurrentLiabilityMember

2023-01-01

2023-12-31

0001949478

us-gaap:CostOfSalesMember

2021-01-01

2021-12-31

0001949478

us-gaap:CostOfSalesMember

2022-01-01

2022-12-31

0001949478

us-gaap:CostOfSalesMember

2023-01-01

2023-12-31

0001949478

DTCK:MaxwillPteLtdMember

2022-01-01

2022-12-31

0001949478

DTCK:LiPengLeckMember

2022-12-31

0001949478

DTCK:MaxwillPteLtdMember

2023-01-01

2023-12-31

0001949478

DTCK:CustomerAMember

2022-01-01

2022-12-31

0001949478

DTCK:CustomerAMember

2023-01-01

2023-12-31

0001949478

DTCK:CustomerBMember

2022-01-01

2022-12-31

0001949478

DTCK:CustomerCMember

2022-12-31

0001949478

DTCK:CustomerDMember

2023-12-31

0001949478

DTCK:CustomerEMember

2023-12-31

0001949478

DTCK:SupplierAMember

2021-01-01

2021-12-31

0001949478

DTCK:SupplierAMember

2023-01-01

2023-12-31

0001949478

DTCK:SupplierBMember

2022-01-01

2022-12-31

0001949478

DTCK:SupplierCMember

2022-01-01

2022-12-31

0001949478

DTCK:SupplierDMember

2023-01-01

2023-12-31

0001949478

DTCK:SupplierEMember

2023-01-01

2023-12-31

0001949478

DTCK:SupplierFMember

2021-01-01

2021-12-31

0001949478

DTCK:SupplierGMember

2021-01-01

2021-12-31

0001949478

DTCK:SupplierFMember

2022-12-31

0001949478

DTCK:SupplierHMember

2022-12-31

0001949478

DTCK:SupplierAMember

2022-12-31

0001949478

DTCK:SupplierIMember

2023-12-31

0001949478

DTCK:SupplierJMember

2023-12-31

0001949478

DTCK:SupplierDMember

2023-12-31

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

xbrli:pure

iso4217:SGD

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

☐

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☒

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2023

OR

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☐

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report

For the transition period from to

Commission file number: 001-41804

Davis Commodities Limited

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

Cayman Islands

(Jurisdiction of incorporation or organization)

10 Bukit Batok Crescent, #10-01, The Spire

Singapore 658079

(Address of principal executive offices)

Ai Imm Lim, Group Financial Controller

Telephone: +65 6896 5333

Email: imm@daviscl.com

At the address of the Company set forth above

(Name, Telephone, E-mail and/or Facsimile number

and Address of Company Contact Person)

Securities registered or to be registered pursuant

to Section 12(b) of the Act.

| Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

| Ordinary Shares |

|

DTCK |

|

The Nasdaq Stock Market LLC |

Securities registered or to be registered pursuant

to Section 12(g) of the Act.

None

(Title of Class)

Securities for which there is a reporting obligation

pursuant to Section 15(d) of the Act.

None

(Title of Class)

Indicate the number of outstanding shares of each

of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

An aggregate of 24,500,625 ordinary shares, par

value $0.000000430108 per share, as of December 31, 2023.

Indicate by check mark if the registrant is a

well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐

No ☒

If this report is an annual or transition report,

indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act

of 1934.

Yes ☐

No ☒

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months

(or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days.

Yes ☒

No ☐

Indicate by check mark whether the registrant

has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405

of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes ☒

No ☐

Indicate by check mark whether the registrant

is a large-accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large-accelerated

filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large-accelerated filer |

☐ |

Accelerated filer |

☐ |

| Non-accelerated filer |

☒ |

Emerging growth company |

☒ |

If an emerging growth company that prepares its

financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition

period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant

has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial

reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or

issued its audit report. ☐

If securities are registered pursuant to Section

12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction

of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error

corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s

executive officers during the relevant recovery period pursuant to §240.10D 1(b). ☐

Indicate by check mark which basis of accounting

the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ☒ |

International Financial Reporting Standards as issued by the International Accounting Standards Board ☐ |

Other ☐ |

| * |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ☐ Item 18 ☐ |

If this is an annual report, indicate by check

mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐

No ☒

TABLE OF CONTENTS

INTRODUCTION

In this annual report on Form 20-F, unless the

context otherwise requires, references to:

| |

· |

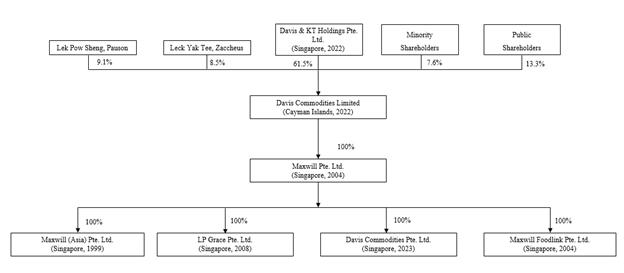

“Davis Commodities” are to Davis Commodities Limited, an exempted company with limited liability incorporated under the laws of the Cayman Islands; |

| |

|

|

| |

· |

“Davis Commodities (Singapore)” are to Davis Commodities Pte. Ltd., a private company limited by shares incorporated under the laws of Singapore, which is wholly owned by Maxwill (as defined below); |

| |

|

|

| |

· |

“LP Grace” are to LP Grace Pte. Ltd., a private company limited by shares incorporated under the laws of Singapore, which is a wholly owned subsidiary of Maxwill (as defined below); |

| |

|

|

| |

· |

“Maxwill” are to Maxwill Pte. Ltd., a private company limited by shares incorporated under the laws of Singapore, which is a wholly owned subsidiary of Davis Commodities Limited; |

| |

|

|

| |

· |

“Maxwill (Asia)” are to Maxwill (Asia) Pte. Ltd., a private company limited by shares incorporated under the laws of Singapore, which is a wholly owned subsidiary of Maxwill; |

| |

|

|

| |

· |

“Maxwill Foodlink” are to Maxwill Foodlink Pte. Ltd., a private company limited by shares incorporated under the laws of Singapore, which is a wholly owned subsidiary of Maxwill; |

| |

|

|

| |

· |

“Ordinary Shares” are to the ordinary shares of Davis Commodities, par value $0.000000430108 per share; |

| |

|

|

| |

· |

“Singapore dollars,” “SGD,” and “S$” are to the legal currency of Singapore; |

| |

|

|

| |

· |

“U.S. dollars,” “US$,” “$,” and “dollars” are to the legal currency of the United States; and |

| |

|

|

| |

· |

“we,” “us,” “our,” “our Company,” or the “Company” are to one or more of Davis Commodities Limited and its subsidiaries, as the case may be. |

This annual report on Form 20-F includes our audited

consolidated financial statements for the fiscal years ended December 31, 2023, 2022, and 2021. In this annual report, we refer to assets,

obligations, commitments, and liabilities in our consolidated financial statements in U.S. dollars. Certain dollar references are based

on the exchange rate of Singapore dollars to U.S. dollars, determined as of a specific date or for a specific period. Changes in the exchange

rate will affect the amount of our obligations and the value of our assets in terms of U.S. dollars which may result in an increase or

decrease in the amount of our obligations (expressed in dollars) and the value of our assets, including accounts receivable (expressed

in dollars).

This annual report contains translations of certain

Singapore dollars into U.S. dollars at specified rates. Unless otherwise stated, the following exchange rates are used in this annual

report:

| |

|

December 31, |

| US$ Exchange Rate |

|

2023 |

|

2022 |

|

2021 |

| At the end of the year – SGD |

|

SGD1.3465 to $1.00 |

|

SGD1.3900 to $1.00 |

|

SGD1.3680 to $1.00 |

| Average rate for the year – SGD |

|

SGD1.3578 to $1.00 |

|

SGD1.3853 to $1.00 |

|

SGD1.3448 to $1.00 |

Part I

Item 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT

AND ADVISERS

Not Applicable.

Item 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not Applicable.

Item 3. KEY INFORMATION

A. [Reserved]

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

Risks Related to Our Business and Industry

Our business is geographically concentrated,

which subjects us to greater risks from changes in local or regional conditions.

Our business operations are concentrated in Asia,

Africa and the Middle East regions. Due to this geographic concentration, our results of operations and financial conditions are subject

to greater risks from changes in general economic and other conditions in these regions, than the operations of more geographically diversified

competitors. These risks include:

| |

· |

changes in economic conditions and unemployment rates; |

| |

|

|

| |

· |

changes in laws and regulations; |

| |

|

|

| |

· |

changes in competitive environment; and |

| |

|

|

| |

· |

adverse weather conditions and natural disasters (including weather or road conditions that limit access to our stores). |

As a result of the geographic concentration of

our business, we face a greater risk of a negative impact on our business, financial condition, results of operations, and prospects

in the event that any of the regions to which we sell our products is more severely impacted by any such adverse condition, as compared

to other regions.

Import or export restrictions by other countries

on the commodity products may have a material adverse impact on our business, financial condition, results of operations, cash flows and

prospects.

Official and unofficial policies implemented by

other countries or international organizations to limit imports from certain countries and/or exports of sugar, rice, and oil and fat

products (such as the imposition of qualitative or quantitative restrictions, increased inspections and quarantines or additional requirements

for sales) may affect our ability to sell such products abroad. For example, we procure raw and white sugar products from India, because

in May 2022, the Indian government implemented an export quota for sugar to curb overseas sales and protect food supplies. Additionally,

in September 2022, the Indian government imposed a 20% levy on rice exports of key varieties, such as un-milled and husk brown rice, and

banned the export of broken rice. As of the date of this annual report, the aforementioned actions taken by the Indian government have

had no adverse impact on our business, financial condition, results of operations, cash flows or prospects, because we are not dependent

on suppliers from India, and we have alternative supply sources from Pakistan, Thailand and Vietnam. However, export restrictions by countries

from which we procure sugar and rice or any import restrictions implemented on the commodity products by other countries or international

organizations that we sell to may have a material adverse effect on our business, financial condition, results of operations, cash flows

and prospects. While import or export restrictions implemented by countries have not affected our ability to procure and export commodity

products into the markets where our customers are based in the past, we cannot assure you that we will not encounter such disruptions

in the future, which may have a material adverse effect on our business, financial condition, results of operations, cash flows and prospects.

Our operations are dependent on the availability

and price of raw materials such as sugar, rice, palm oil, palm olein, and coconut oil. Unfavorable global weather conditions, the lack

of long-term contracts at fixed prices with our suppliers, and the seasonal nature of crops, may have an adverse effect on the price and

availability of such raw materials. Any increase in the cost of or shortfall in the availability of such raw materials could have an adverse

effect on our business, financial condition, results of operations, cash flows and prospects. Seasonable variations could also result

in fluctuations in our results of operations.

We source our finished packaged commodity products

from global suppliers, which are predominantly sugar products from Brazil, India, Malaysia, Thailand and Indonesia, rice products from

Thailand, India, Vietnam and Pakistan, and oil and fat products from Indonesia and Malaysia. We are not involved in the milling, processing

and/or refining of raw materials used to produce the finished package commodity products that we sell to our customers. We purchase finished

packaged commodities from our suppliers, after which we engage with third-party freight and/or shipping companies for the transportation

of these products, and then distribute these products to our customers. Nevertheless, our business is highly dependent on the price reasonability

and availability of high quality raw agricultural commodity materials which serve as inputs that our suppliers use to manufacture the

commodity products that we distribute to our customers.

The price and availability of such raw materials

depend on several factors beyond our control, including overall economic conditions, production levels, market demand and competition

for such raw materials, production and transportation costs, duties and taxes and trade restrictions. Negative developments pertaining

to such factors may have an adverse impact on the availability and prices of raw materials used in our suppliers’ manufacturing

operations, which may consequently increase the costs of our operations as well as negatively affect our business, financial condition,

results of operations, cash flows and prospects.

Additionally, we do not have long-term supply

contracts with any of our suppliers. We typically place orders with them in advance of our anticipated requirements for some of our products.

For example, we typically pre-order sugar products from certain suppliers for the upcoming calendar year based on the annual forecasted

demand. We will place additional orders with the relevant suppliers when inventory levels run low. The absence of long-term contracts

at fixed prices exposes us to volatility in the prices of raw materials that are used to manufacture the sugar, rice, and oil and fat

products and we cannot assure you that we will always be able to pass on any consequent cost increases from our suppliers to our customers,

nor that volumes purchased by our customers can be maintained should selling prices to our customers increase.

Furthermore, the supply of raw materials used

by our suppliers to manufacture our commodity products is subject to seasonal variations. For example, the supply of raw materials is

generally dependent on the harvesting season of various crops such as sugar cane, rice and palm. As a result of such seasonal fluctuations,

and given that we do not have access to storage infrastructure such as warehouses for off-season sales, our sales and results of operations

may vary by financial quarter, and the sales and results of operations of any given financial quarter may not be relied upon as indicators

of the sales or results of operations of other financial quarters or of our future performance. Such seasonal fluctuations may also result

in a shortfall in the availability of the raw materials required by our suppliers to manufacture the commodity products during certain

periods, which could lead to a shortage in production of the finished commodity products we distribute to our customers, and, consequently,

have an adverse effect on our business, financial condition, results of operations, cash flows and prospects.

Risks relating to climate change and episodes

of extreme weather events could have an adverse effect on the price and availability of raw materials on which our operations are dependent.

Our business is highly dependent on the price

reasonability and availability of high quality raw agricultural commodity materials such as sugar, rice, palm oil, palm olein, and coconut

oil, which serve as inputs that our suppliers use to manufacture the finished commodity products that we distribute to our customers.

The physical effects of climate change, which

may include extreme weather events, resource shortages, changes in rainfall and storm patterns, water shortages, changing sea levels and

temperatures, including higher temperatures, may have an adverse effect on our business and operations. Unfavorable global weather conditions,

including extreme weather, such as drought, floods and natural disasters, may have an adverse effect on the price reasonability and availability

of raw materials. Additionally, such events or conditions could also have other adverse effects on the operations, workforce and/or the

local communities surrounding our suppliers or customers, including an increased risk of food insecurity, water scarcity, civil unrest

and the prevalence of disease. There is growing concern that carbon dioxide and other greenhouse gases in the atmosphere may have an adverse

impact on global temperatures, weather patterns and the frequency and severity of extreme weather and natural disasters. The availability

of raw materials used to manufacture the finished commodity products for our business, which include, amongst others, sugar, rice, palm

oil, palm olein, and coconut oil, may be adversely affected by longer than usual periods of heavy rainfall in certain regions or a drought

caused by weather conditions such as El Niño. For example, excessive rainfall may lead to poor pollination of palms, decrease the

effectiveness of fertilizers and affect harvesting. Adverse weather conditions may also result in decreased availability of water, which

could impact the processing and refining of the raw materials.

Our business depends on consistent supplies of

finished commodity products from our suppliers to operate efficiently. In the event that the effects of climate change, including extreme

weather events, cause prolonged disruptions to the delivery of raw materials, essential commodities and/or other essential inputs used

in our suppliers’ manufacturing operations, or affect the prices or availability thereof, it may in turn increase the costs of our

operations or the availability of finished commodity products that we sell to our customers, which will consequently negatively affect

our business, financial condition, results of operations, cash flows and prospects.

We depend significantly on the procurement

of finished products, and various factors may result in an inadequate supply or result in an increase in our costs in order to secure

sufficient products to meet our deliverable requirements to customers.

Although all the finished commodity products are

imported from global suppliers which are typically reliable, it is nevertheless possible for there to be an inadequate supply of finished

commodity products due to a breach in performance obligation(s) by a certain supplier, by export restrictions imposed by governments of

foreign countries from which we export the finished commodity products, or for any other reason, which could hamper our business and operations.

Additionally, we estimate the transportation time for the export of the finished commodities several months in advance of the actual time

that they are required by our customers, and any error in our estimate or any change in market conditions by the time the products are

delivered may lead to a shortfall in the relevant sugar, rice, and oil and fat products to fulfill the orders placed by our customers.

Even in situations where it is possible to meet our customers’ requirements or demands, our inability to predict the transportation

lead time may result in an increase in our costs if we are required to secure sufficient products from alternative sources or suppliers.

Although we may seek to pass on some or all of any such additional costs to customers, we cannot assure you that we will be successful

in doing so. This may adversely affect our business, financial condition, results of operations, cash flows and prospects.

It is also possible that from time to time, one

or more of our existing suppliers may discontinue their supply of finished commodity products to us, and any inability on our part to

procure the commodity products from alternative suppliers in a timely fashion, or on commercially acceptable terms, may adversely affect

our operations. If, for any reason, primary suppliers curtail or discontinue their delivery of the commodity products to us in the quantities

we need, or on commercially acceptable terms, our delivery schedules could be disrupted, and our business, financial condition, results

of operations, cash flows and prospects could be adversely affected.

We have a diverse range of products in three

main categories of agricultural commodities and our inability to manage our diversified operations may have an adverse effect on our business,

financial condition, results of operations, cash flows and prospects.

We offer a diverse range of products across three

main categories of agricultural commodities: sugar, rice, and oil and fat products. Accordingly, our management requires considerable

expertise and skill to manage and allocate an appropriate amount of time and attention to each category of commodity products. Merchandizing

a diverse range of products also makes forecasting future revenue and operating results difficult, which may impair our operations and

your ability to assess our financial prospects. In addition, our cost controls, internal controls, and accounting and reporting systems

must be integrated and upgraded on a continual basis to support our operations. In order to manage and integrate our products and operations,

we are required to, among other things, stay abreast with key developments in each geography in which we operate, implement and continue

to improve our operational, financial and management systems, develop the management skills of our managers and continue to train, motivate

and manage our employees. If we are unable to manage our business and operations, our business, financial condition, results of operations,

cash flows and prospects may be adversely affected.

The COVID-19 pandemic has affected, and

could continue to affect, the global economy as a whole and the markets in which we operate.

The COVID-19 pandemic has caused volatility in

the global economy. Government measures taken in response to the pandemic, including quarantine orders, as well as other indirect effects

that the COVID-19 pandemic is having on global economic activity have also resulted in operating and logistics risks for us, and industrial

operations by our suppliers were impacted by changed protocols or working practices. Preventative measures put in place to tackle the

COVID-19 pandemic in any jurisdiction with which our supply chain is involved could negatively impact our operations. For instance, a

lockdown may impact our supply chain which may result in a delay in the supply of the finished commodity products to our customers. However,

as a whole, our business and operations have not been affected by the pandemic-related lockdowns in China. As sugar is a key staple commodity,

demand for our products, including sugar, rice and oil and fat products, remain strong in China, and we have not experienced a decline

in consumer demand for our products in China.

The impact of the COVID-19 pandemic on our business

going forward will depend on a range of factors which we are not able to accurately predict, including the duration and scope of the pandemic,

a repeat of the spike in the number of COVID-19 cases, the geographies impacted, the impact of the pandemic on economic activity and the

nature and severity of measures adopted by governments, including restrictions on travel, mandates to avoid large gatherings and orders

to self-quarantine or shelter in place. Further, COVID-19 pandemic restrictions had disrupted supply chains, resulting in delayed shipments

for some of our products.

The COVID-19 pandemic has also led to sharp reductions

in global growth rates and the ultimate impact on the global economy remains uncertain. Accordingly, the COVID-19 pandemic may have significant

negative impacts in the medium and long term, including on our business, financial condition, results of operations, cash flows and prospects.

We derive a significant portion of our revenue

from sugar products and any reduction in demand or in the production of sugar products could have an adverse effect on our business, financial

condition, results of operations, cash flows and prospects.

We derive a significant portion of our revenue

from the sale and distribution of sugar products. For the fiscal years ended December 31, 2023, 2022 and 2021, our revenue from the sale

of sugar products amounted to approximately US$116.4 million, US$154.8 million and US$135.1 million, or approximately 61.0%, 74.9% and

69.6% of our revenue, respectively. For details on the sugar products distributed by our Company, please see the section entitled “Item

4. Information on the Company – B. Business Overview – Our Main Business Activities – Sugar”. Consequently, any

reduction in demand or a temporary or permanent discontinuation of manufacturing of the sugar products by any of our suppliers could have

an adverse effect on our business, financial condition, results of operations, cash flows and prospects.

Our products are commodities in nature,

and their prices are subject to fluctuations that may affect our profitability.

Our earnings are, to a large extent, dependent

on the prices of the sugar, rice, and oil and fat products that we sell, which are commodities in nature. These prices fluctuate due to

factors beyond our control, including, among other things, world supply and demand, supply of raw materials, weather, crop yields, trade

disputes between governments of key producing and consuming countries and governmental regulation. Global demand for agricultural commodities

may be adversely affected in periods of sustained economic downturn, while supply may be affected due to weather conditions or long-term

technological developments, all of which are factors are beyond our control.

We strive to minimize our commodity price risks

by either selling the sugar, rice, and oil and fat products on a cost-plus basis (a pricing method whereby a fixed percentage is added

to the cost it takes to produce one unit of a product), or by hedging prices of the sugar products through futures contracts on the commodity

exchanges. The rice and oil and fat products and others, specifically tomato puree, together accounted for approximately 39.0% of our

revenue for the fiscal year ended December 31, 2023, and we sell all of the rice products and oil and fat products to our customers on

a cost-plus basis. The sugar products accounted for approximately 61.0% of our revenue for the fiscal year ended December 31, 2023, and

we typically pre-order sugar products from certain suppliers for the upcoming calendar year based on the annual forecasted sugar product

demand. While we sell most of our sugar product volume on a cost-plus basis, we have had open positions on sugar product prices for approximately

20% of our annual sugar product volume, historically. These open positions on sugar product prices are a result of the sugar product pricing

at the point of purchase from the relevant supplier possibly varying with the sugar product prices at the point of sales to our customers,

and may lead to uncertainty in our sugar product margins. We mitigate against this risk by hedging the sugar products which are exposed

to open positions by trading sugar futures over the futures exchanges, including the ICE Futures Europe and ICE Futures U.S. Our hedging

positions enable us to fix the price of the sell future contracts at the point of purchase for the total purchase amount of the sugar

products purchased from certain suppliers against adverse fluctuations in the sugar product prices and, upon maturity of such sell future

contract. In addition, a buy future contract is simultaneously executed at sugar product’s spot price in order to close such sell

future contract.

Although we have thus far been able to pass on

any increased costs to our customers by increasing prices for our products, and may be adequately hedged against adverse fluctuations

in commodity product prices through our practice of hedging our purchases, we cannot assure you that we will always be successful in doing

so. It is difficult to predict the specific price fluctuations that may occur and the exact impact which they may have on our earnings,

and such price fluctuations may adversely affect our business, financial condition, results of operations, cash flows and prospects.

Fluctuation in the exchange rate between

the US$ and foreign currencies may have an adverse effect on our business.

Although some of our clients and producers are

located in jurisdictions that use currencies other than US$, S$ or Euros€, the majority of our trades are conducted using US$ and

we have minimal trades which are conducted using € and S$. While we follow established risk management practices, we are nevertheless

exposed to risks from foreign exchange rate fluctuations, since our business is dependent on imports and exports entailing large foreign

exchange transactions, in currencies including the US$, S$ and €. Exchange rates between some of these currencies and the US$ in

recent years have fluctuated significantly and may do so in the future, thereby impacting our results of operations and cash flows in

US$ terms. However, we do not hedge our exposure to foreign exchange fluctuations through derivatives or any other means. For the fiscal

years ended December 31, 2021, 2022 and 2023, we recognized a foreign exchange loss of US$30,729, US$22,379 and US$1,778, respectively.

Further, given that we rely on the importation of commodity products, any adverse movement in currency exchange rates may result in an

increase in the costs of the commodity products that we procure, which could have an adverse effect on our business, financial condition,

results of operations, cash flows and prospects.

Our inability to effectively manage our

growth could have an adverse effect on our business, financial condition, results of operations, cash flows and prospects.

For the fiscal years ended December 31, 2023,

2022 and 2021, our total revenue was approximately US$190.7 million, US$206.7 million and US$194.2 million, respectively, representing

a decrease by approximately 7.7% from fiscal year 2022 to 2023, and an increase by approximately 6.4% from fiscal year 2021 to 2022; our

net profit was approximately US$1.1 million, US$4.6 million and US$4.7 million, respectively, representing a decrease by approximately

76.5% from fiscal year 2022 to fiscal year 2023, and a decrease by approximately 1.8% from fiscal year 2021 to 2022. Our inability

to manage our expansion effectively and execute our growth strategy in a timely manner, or within budget estimates, or our inability to

meet the expectations of our customers and other stakeholders, could have an adverse effect on our business, financial condition, results

of operations, cash flows and prospects. We intend to continue expanding our business. Our future prospects will depend on our ability

to grow our business and operations, which could be affected by many factors, including our ability to introduce new products and maintain

the quality of the products, general political and economic conditions, government policies or strategies in respect of specific industries,

prevailing interest rates, price of commodity products we procure, energy supply and currency exchange rates.

In order to manage our growth effectively, we

must implement, upgrade and improve our operational systems, procedures and internal controls on a timely basis. If we fail to implement

these systems, procedures and controls on a timely basis, or if there are weaknesses in our internal controls that would result in inconsistent

internal standard operating procedures, we may not be able to meet our customers’ needs, hire and retain new employees or operate

our business effectively. Moreover, our ability to sustain our rate of growth depends significantly upon our ability to select and retain

key managerial personnel, maintain effective risk management practices and train managerial personnel to address emerging challenges.

We cannot assure you that our existing or future

management, operational and financial systems, procedures and controls will be adequate to support future operations or establish or develop

business relationships beneficial to future operations. Failure to manage growth effectively could have an adverse effect on our business,

financial condition, results of operations, cash flows and prospects.

The improper handling or storage of commodity

products, spoilage of and damage to such commodity products, or any real or perceived contamination in the commodity products, could subject

us to regulatory and legal action, damage our reputation and have an adverse effect on our business, financial condition, results of operations,

cash flows and prospects.

The commodity products that we procure and distribute

are subject to risks of contamination, adulteration and product tampering during their processing, transport or storage. In the event

that our products fail to meet quality standards, including as prescribed by the Singapore Food Agency, or are alleged to result in harm

to our customers, we may be exposed to the risks of product liability or recall claims. For example, any occurrence of negligence and/or

oversight in the process of refining by our suppliers, may result in us selling impure oil to our customers which may cause harm to their

health. Although we only purchase finished commodity products from our suppliers and have no involvement in the processing, refining or

milling of commodities, such incidents may nonetheless expose us to liabilities and claims by our customers, which could adversely affect

our reputation, growth and profitability. Additionally, storage of our products entails risks associated with the storage environment,

including the risk of moisture, adverse temperature and humidity levels and pests. Excessively high or low levels of moisture, temperature

or humidity may result in damage to our stored products, which may have a material adverse effect on our business, financial condition,

results of operations, cash flows and prospects.

While such risks may be controlled, albeit not

eliminated, by adherence to good manufacturing practices and finished product testing, we have little control over the manufacturing processes

of our suppliers or their third-party manufacturers. We cannot assure you that there will not be incidents of contaminated products or

ingredients in the future which may result in product liability claims, product recalls and negative publicity. Such product liability

claims may also result legal proceedings brought against us by our consumers, distributors and government agencies. If we are made a party

to product liability proceedings, we may incur considerable expenses in defending such claims which would also require the diversion of

management’s attention and the diversion of significant resources away from our core profitable business areas. For the fiscal years

ended December 31, 2021, 2022 and 2023, we did not incur any costs associated with product liability claims. We do not maintain product

liability insurance coverage for our domestic and international markets. We are, accordingly, not able to claim any losses and/or receive

compensation from insurers in connection with any product liability claims. Any product recalls, product liability claims or adverse regulatory

action may adversely affect our reputation and brand image, as well as entail significant costs, which could adversely affect our reputation,

business, financial condition, results of operations, cash flows and prospects.

We rely heavily on our existing brands,

the dilution of which could adversely affect our business.

Our product portfolio spans various brands which

are owned by our Company, including two main brands: Maxwill and Taffy. We distribute sugar products and oil and fat products

under these brands to customers both in Singapore and in overseas markets. Additionally, we distributed the Lin brand sugar products

in Singapore through our exclusive distributorship with the Thai Roong Ruang Sugar Group from February 1, 2021 to December 31, 2023. On

December 31, 2023, the distribution agreement between us and the Thai Roong Ruang Sugar Group was terminated. The amount of revenues that

were generated through our exclusive distributorship with Thai Roong Ruang Sugar Group was less than 1.0% of our total revenues in each

of the fiscal years ended December 31, 2021, 2022 and 2023. We have appointed Tong Seng Produce Pte. Ltd., an established distributor

of rice, oil, sugar, flour and fiber products in Singapore, for the exclusive distribution of certain sugar products under our Taffy

brand. The amount of revenues that were generated through our exclusive distributorship with Tong Seng Produce Pte. Ltd. was also

less than 1.0% of our revenues in each of the fiscal years ended December 31, 2021, 2022 and 2023. We have no commitment from any customer

to purchase a certain amount of our products, even under these exclusive or established distributorships. Our brands and reputation are

among our most important assets and serve in attracting customers to our products in preference over those of our competitors. We believe

that continuing to develop awareness of these brands, through focused and consistent branding and marketing initiatives, among retail

consumers and institutional customers, is important for our ability to increase our sales volumes and our revenues, grow our existing

market share and expand into new markets. Any decrease in product quality due to reasons beyond our control or allegations of product

defects, even when false or unfounded, could tarnish the image of the established brands and may cause consumers to choose other products.

Our brands and reputation could also be affected by social, health and cultural organizations and any negative publicity campaigns (such

as the introduction of low-sugar or low-fat campaigns), which could lead to a decline in our sales volume. Further, the considerable expansion

in the use of social media over recent years has compounded the impact of those groups’ negative publicity. Consequently, any adverse

publicity involving these brands, our Company or our products may impair our reputation, dilute the impact of our branding and marketing

initiatives and adversely affect our business and our prospects. Any adverse publicity involving our brands may result in a substantial

impairment to our reputation and negatively affect our business, financial condition, results of operations, cash flows and prospects.

We procure commodity products from our suppliers

and utilize the services of certain third-party service providers for our operations. Any deficiency or interruption in their services

could adversely affect our business, financial condition, results of operations, cash flows and prospects.

We rely on global suppliers for the supply of

finished sugar, rice, and oil and fat products which we purchase. We also utilize and depend on the services of certain third-party service

providers for our operations. For instance, we depend on third-party transport providers, such as international haulers, shipping lines

and transport companies, for freight forwarding and shipping services. The agreements entered into with such third parties include provisions

which may allow the third-party to terminate the agreement with limited prior notice. In the event that any of such third parties determine

to terminate or breach their respective agreements, we cannot assure you that we will be able to obtain a replacement in a timely manner,

or at all, which may reduce our sales volumes and adversely affect our business, financial condition, results of operations, cash flows

and prospects.

We cannot assure you that we will be successful

in continuing to receive uninterrupted, high quality service from various third parties on whom we rely for materially all of our current

and future products and related services. Any termination or breach of contract, disruption or inefficiencies in the operations of these

third parties may adversely affect our business, financial condition, results of operations, cash flows and prospects.

Our inability to expand or effectively manage

our distribution network may have an adverse effect on our business, financial condition, results of operations, cash flows and prospects.

Our customers in Asia, Africa and the Middle East

are located in over 20 countries. In addition to traditional distribution channels, we have utilized third-party e-commerce platforms

to market and distribute the sugar, rice, and oil and fat products. Our ability to expand and grow our product reach significantly depends

on the reach and effective management of our distribution network. We continuously seek to increase the market penetration of our products

by appointing new distributors targeted at different customer groups and geographies. We cannot assure you that we will be able to successfully

identify or appoint new distributors or effectively manage our existing distribution network. If the terms offered to such distributors

by our competitors are more favorable than those offered by us, distributors may decline to distribute our products and terminate their

arrangements with us. We may be unable to appoint replacement distributors in a timely fashion, or at all, which may reduce our sales

volumes and adversely affect our business, financial condition, results of operations, cash flows and prospects.

Further, our competitors may have exclusive arrangements

with certain distributors who may be unable to stock and distribute our products, which may limit our ability to expand our distribution

network. Similarly, our competitors may adopt innovative distribution models, which could be more effective than traditional distribution

models resulting in a reduction in the sales of our products. We may also face disruptions in the distribution and delivery of the products

for various reasons beyond our control, including poor handling by distributors of our products, transportation bottlenecks, natural disasters

and labor issues which could lead to delayed or lost deliveries, and any failure to provide distributors with sufficient inventories of

our products may result in a reduction in the sales. If our distributors fail to distribute our products in a timely manner, or adhere

to the terms of the distribution arrangement, or if our distribution arrangements are terminated, our business, financial condition, results

of operations, cash flows and prospects may be adversely affected.

If we pursue strategic acquisitions or joint

ventures, we may not be able to successfully consummate favorable transactions or successfully integrate acquired businesses.

As of the date of this annual report, we have

not identified any such strategic acquisitions. We may evaluate potential acquisitions or joint ventures that would further our strategic

objectives, from time to time. However, we may not be able to identify suitable target assets or companies, consummate a transaction on

terms that are favorable to us, or achieve the anticipated synergies, expected returns and other benefits as a result of integration challenges

or anti-monopoly regulations. Companies or operations acquired, or joint ventures created by us may not be profitable or may not achieve

sales levels and profitability that justify the investments made. Our corporate development activities may entail financial and operational

risks, including diversion of management attention from its existing core businesses, difficulty in integrating or separating personnel,

financial, information technology and other systems, difficulty in retaining key employees, and negative impacts on existing business

relationships with suppliers and customers. The potential for future acquisitions could also result in potentially dilutive issuances

of equity securities, the incurrence of debt and such issuances or incurrences, or the perception that such issuances or incurrences may

occur, could depress the market price of our equity securities. Potential future acquisitions may also increase our contingent liabilities

and operating expenses, all of which could adversely affect our business, financial condition, results of operations, cash flows and prospects.

Our existing loan agreements contain certain

covenants and restrictions that may limit the flexibility of our Company in the way in which we organize our subsidiaries and/or operate

our business.

Certain of our Company’s financing agreements

contain covenants that limit its ability to undertake or permit, among other things, any re-organization or change of shareholders, without

the prior written consent of the relevant lender. Such limitations could hinder strategic initiatives, restructuring efforts, or capital

allocation decisions, potentially impacting the Company's growth prospects, financial flexibility, and ability to adapt to changing market

conditions. Failure to comply with these covenants could result in breaches of contractual obligations, triggering default provisions

and leading to adverse consequences, including acceleration of debt repayment or other enforcement actions by lenders.

Notwithstanding the above, the total outstanding

debt facilities our Company had with these lenders amounted to approximately US$464,514 as of April 30, 2024. Our cash and cash balances

position as of December 31, 2023 amounted to US$1,330,355. In the event that all our borrowings require immediate repayment, our directors

and management believe that the total amounts can be repaid without severely affecting our cash flows and/or operations.

If we are unable to introduce new products

and respond to changing consumer preferences in a timely and effective manner, the demand for our products may decline, which may have

an adverse effect on our business, financial condition, results of operations, cash flows and prospects. There is no guarantee that we

will be successful in the new business segments or products that we plan to expand into.

The success of our business depends upon our ability

to anticipate and identify changes in consumer preferences and offer commodity products that consumers require. For example, according

to Frost & Sullivan Limited ("Frost & Sullivan”), whom we commissioned in June 2022 to produce the “The Agricultural

Commodity Market Independent Market Research Report” (the “Frost & Sullivan Report”), health awareness of Asian

consumers is increasing and is being driven by the rising standard of living in Asia. Consumer inclination towards purchasing healthier

food varieties has increased. Consumers are now seeking healthier, less processed, raw sugar varieties such as brown and organic sugar

to reduce its negative impact on the body following its consumption. Many sugar manufacturers are developing innovative varieties to keep

up with market demand. The growing concerns with regards to lifestyle related health conditions such as obesity and diabetes is expected

to further drive demand for healthier sugar varieties. Additionally, such consumer preferences are influenced by a number of factors beyond

our control, such as the prices of alternative products and economic conditions. Although we seek to identify such trends and introduce

new products, we recognize that customer tastes cannot be predicted with certainty and can change rapidly, and that there is no certainty

that these will be commercially viable or effective or accepted by our customers, or that we will be able to successfully compete in such

new product segments. Our failure to successfully predict such consumer preferences and trends as they relate to our selection of products

in a cost effective and/or timely manner could increase our costs and lead to us being less competitive in terms of our prices or variety

of products we sell, which could adversely affect our business, financial condition, results of operations, cash flows and prospects.

Before we can introduce a new product, we must

successfully execute a number of steps, including obtaining required approvals and registrations, effective branding and marketing strategies

for target customers, while engaging with the relevant third-party suppliers to increase or change the nature and quantities of the finished

commodity products supplied. We also depend on the successful introduction of new production and manufacturing processes by our suppliers

such as manufacturing facilities and processing plants to create innovative products, achieve operational efficiencies and adapt to advances

in, or obsolescence of technology. We cannot assure you that our suppliers will be able to successfully keep up with technological improvements

in order to meet our customers’ needs or that the technology developed by others will not render our products less competitive or

attractive. Our failure to successfully adopt such technologies in our selection of third-party suppliers and/or service providers in

a cost effective and/or timely manner could increase our costs and lead to us being less competitive in terms of our prices or quality

of products we sell, which may adversely affect our business, financial condition, results of operations, cash flows and prospects.

The commercialization process of a new product

would require us to spend considerable time and capital. Delays in any part of the process, our inability to obtain necessary regulatory

approvals for the products or failure of a product to be successful at any stage could adversely affect our business. Consequently, any

failure on our part to successfully introduce new products may have an adverse effect on our business, financial condition, results of

operations, cash flows and prospects.

Our inability to accurately forecast demand

for our products may have an adverse effect on our business, financial condition, results of operations, cash flows and prospects.

Our business depends on our estimate of the demand

for the sugar products from our customers. We typically pre-order the sugar products from certain suppliers for the upcoming calendar

year based on the annual forecasted demand. We constantly monitor our inventory levels and will place additional orders with the relevant

suppliers when inventory levels run low. If we underestimate demand or have inadequate capacity due to conditions for which we are unable

to meet the demand for the sugar products, we may place orders for fewer quantities of products than required, which could result in the

loss of business. While we forecast the demand for the sugar products and accordingly plan our purchase volumes, any error in our forecast

could result in a reduction in our profit margins and/or surplus or insufficient stock, which may result in additional storage cost and

any surplus stock may not be sold in a timely manner, or at all. In the event we overestimate demand, we may incur additional costs to

secure capacity from suppliers or purchase more products than required. Additionally, our inability to accurately forecast demand for

our products may have an adverse effect on our business, financial condition, results of operations, cash flows and prospects.

Our suppliers and customers may be subject

to extensive government regulations and if they fail to obtain, maintain or renew required statutory and regulatory licenses, permits

and approvals required for the import and/or export of the commodity products, our business, financial condition, results of operations,

cash flows and prospects may be adversely affected.

Our suppliers and customers may be subject to

extensive government regulations and may be required to obtain and maintain a number of statutory and regulatory licenses, permits, certificates

and approvals. Customers may also be required to comply with international rules and regulations in respect of the delivery and importation

of the commodity products. To ensure that our operations are not disrupted by such regulatory requirements, we seek customers that have

the relevant licenses, permits, certificates and approvals required to import the commodity products into their markets and to receive

deliveries of such commodity products.

While we have not encountered any incident in

the past involving non-compliance by any of our suppliers or customers, we cannot assure you that all our suppliers and/or customers would

have obtained or renewed the relevant permits, certificates and approvals prior to entering into any transaction with us. If our suppliers

and customers do not receive such approvals or are not able to renew the approvals in a timely manner, our business and operations may

be adversely affected. Further, the relevant authorities may initiate penal action against them, restrain their operations, impose fines

or penalties, or initiate legal proceedings for their inability to renew/obtain approvals in a timely manner or at all, which will consequently

have an adverse impact on our business, financial condition, results of operations, cash flows and prospects.

The approvals required by our suppliers and customers