Filed by Golub Capital BDC, Inc.

pursuant to Rule 425 under the Securities Act

of 1933

and deemed filed under Rule 14a-6(b) of the Securities

Exchange Act of 1934

Subject Company: Golub Capital BDC 3, Inc.

Commission File No. 814-01244

File No. of Related Registration Statement: 333-277325

Attached hereto as Exhibit 1 is a GBDC Merger Investor Presentation

GOLUB CAPITAL BDC, INC. (“GBDC”) OVERVIEW OF PROPOSED MERGER WITH GOLUB CAPITAL BDC 3, INC. (“GBDC 3”) MAY 2024 CONFIDENTIAL | © 2024 GOLUB CAPITAL LLC

Disclaimer 2 company and to monitor and administer its investments ; (xvii) the ability of GC Advisors or its affiliates to attract and retain highly talented professionals ; (xviii) the business prospects of GBDC, GBDC 3 or, following the closing of one or both of the Mergers, the combined company and the prospects of their portfolio companies ; (xix) the impact of the investments that GBDC, GBDC 3 or, following the closing of one or both of the Mergers, the combined company expect to make ; (xx) the expected financings and investments and additional leverage that GBDC, GBDC 3 or, following the closing of one or both of the Mergers, the combined company may seek to incur in the future ; and (xxi) other considerations that may be disclosed from time to time in GBDC’s and GBDC 3 ’s publicly disseminated documents and filings . GBDC and GBDC 3 have based the forward - looking statements included in this press release on information available to them on the date of this communication, and they assume no obligation to update any such forward - looking statements . Although GBDC and GBDC 3 undertake no obligation to revise or update any forward - looking statements, whether as a result of new information, future events or otherwise, you are advised to consult any additional disclosures that they may make directly to you or through reports that GBDC and GBDC 3 in the future may file with the SEC, including the Joint Proxy Statement (each as defined below), annual reports on Form 10 - K, quarterly reports on Form 10 - Q and current reports on Form 8 - K . Additional Information and Where to Find It This communication relates to a proposed business combination involving GBDC and GBDC 3 , along with the related Proposals for which stockholder approval will be sought . In connection with the Proposals, each of GBDC and GBDC 3 intend to file relevant materials with the SEC, including a registration statement on Form N - 14 , which will include a joint proxy statement of GBDC and GBDC 3 and a prospectus of GBDC (the “Joint Proxy Statement”) . This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval . No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act . STOCKHOLDERS OF EACH OF GBDC AND GBDC 3 ARE URGED TO READ ALL RELEVANT DOCUMENTS FILED WITH THE SEC, INCLUDING THE JOINT PROXY STATEMENT OF GBDC AND GBDC 3 REGARDING THE PROPOSALS WHEN IT BECOMES AVAILABLE, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS THERETO, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT GBDC, GBDC 3 , THE MERGERS AND THE PROPOSALS . Investors and security holders will be able to obtain the documents filed with the SEC free of charge at the SEC’s web site, http : //www . sec . gov or, for documents filed by GBDC, from GBDC’s website at http : //www . golubcapitalbdc . com . Participants in the Solicitation GBDC and GBDC 3 and their respective directors, executive officers and certain other members of management and employees of GC Advisors and its affiliates, may be deemed to be participants in the solicitation of proxies from the stockholders of GBDC and GBDC 3 in connection with the Proposals . Information regarding the persons who may, under the rules of the SEC, be considered participants in the solicitation of the GBDC and GBDC 3 stockholders in connection with the Proposals will be contained in the Proxy Statement when such document becomes available . This document may be obtained free of charge from the sources indicated above . Forward - Looking Statements This communication may contain “forward - looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 . Statements other than statements of historical facts included in this communication may constitute forward - looking statements and are not guarantees of future performance or results and involve a number of risks and uncertainties . Actual results may differ materially from those expressed or implied in the forward - looking statements as a result of a number of factors, including those described from time to time in filings with the Securities and Exchange Commission . GBDC undertakes no duty to update any forward - looking statement made herein . All forward - looking statements speak only as of the date of this communication . Some of the statements in this communication constitute forward - looking statements because they relate to future events, future performance or financial condition or the two - step merger of GBDC 3 with and into GBDC (collectively, the “Mergers”), along with the related proposals for which stockholder approval will be sought (collectively, the “Proposals”) . The forward - looking statements may include statements as to : future operating results of GBDC and GBDC 3 and distribution projections ; business prospects of GBDC and GBDC 3 and the prospects of their portfolio companies ; and the impact of the investments that GBDC and GBDC 3 expect to make . In addition, words such as “may,” “might,” “will,” “intend,” “should,” “could,” “can,” “would,” “expect,” “believe,” “estimate,” “anticipate,” “predict,” “potential,” “plan” or similar words indicate forward - looking statements, although not all forward - looking statements include these words . The forward - looking statements contained in this communication involve risks and uncertainties . Certain factors could cause actual results and conditions to differ materially from those projected, including the uncertainties associated with (i) the timing or likelihood of the Mergers closing ; (ii) the expected synergies and savings associated with the Mergers ; (iii) the ability to realize the anticipated benefits of the Mergers, including the expected elimination of certain expenses and costs due to the Mergers ; (iv) the percentage of GBDC and GBDC 3 stockholders voting in favor of the proposals submitted for their approval ; (v) the possibility that competing offers or acquisition proposals will be made ; (vi) the possibility that any or all of the various conditions to the consummation of the Mergers may not be satisfied or waived ; (vii) risks related to diverting management’s attention from ongoing business operations ; (viii) the risk that stockholder litigation in connection with the Mergers may result in significant costs of defense and liability ; (ix) changes in the economy, financial markets and political environment, including the impacts of inflation and rising interest rates ; (x) risks associated with possible disruption in the operations of GBDC and GBDC 3 or the economy generally due to terrorism, war or other geopolitical conflict (including the current conflict between Russia and Ukraine), natural disasters or global health pandemics, such as the COVID - 19 pandemic ; (xi) future changes in laws or regulations (including the interpretation of these laws and regulations by regulatory authorities) ; (xii) changes in political, economic or industry conditions, the interest rate environment or conditions affecting the financial and capital markets that could result in changes to the value of GBDC’s or GBDC 3 ’s assets ; (xiii) elevating levels of inflation, and its impact on GBDC and GBDC 3 , on their portfolio companies and on the industries in which they invest ; (xiv) combined company’s plans, expectations, objectives and intentions, as a result of the Mergers ; (xv) the future operating results and net investment income projections of GBDC, GBDC 3 , or, following the closing of one or both of the Mergers, the combined company ; (xvi) the ability of GC Advisors to locate suitable investments for the combined

Process for Evaluating Potential Merger with GBDC 3 Good for existing stockholders Good for new stockholders Good for GBDC 3 GBDC’s Board of Directors — along with the independent directors’ financial advisor and legal counsel — has gone through a careful, methodical process to evaluate a potential merger with GBDC 3 and believes that it is:

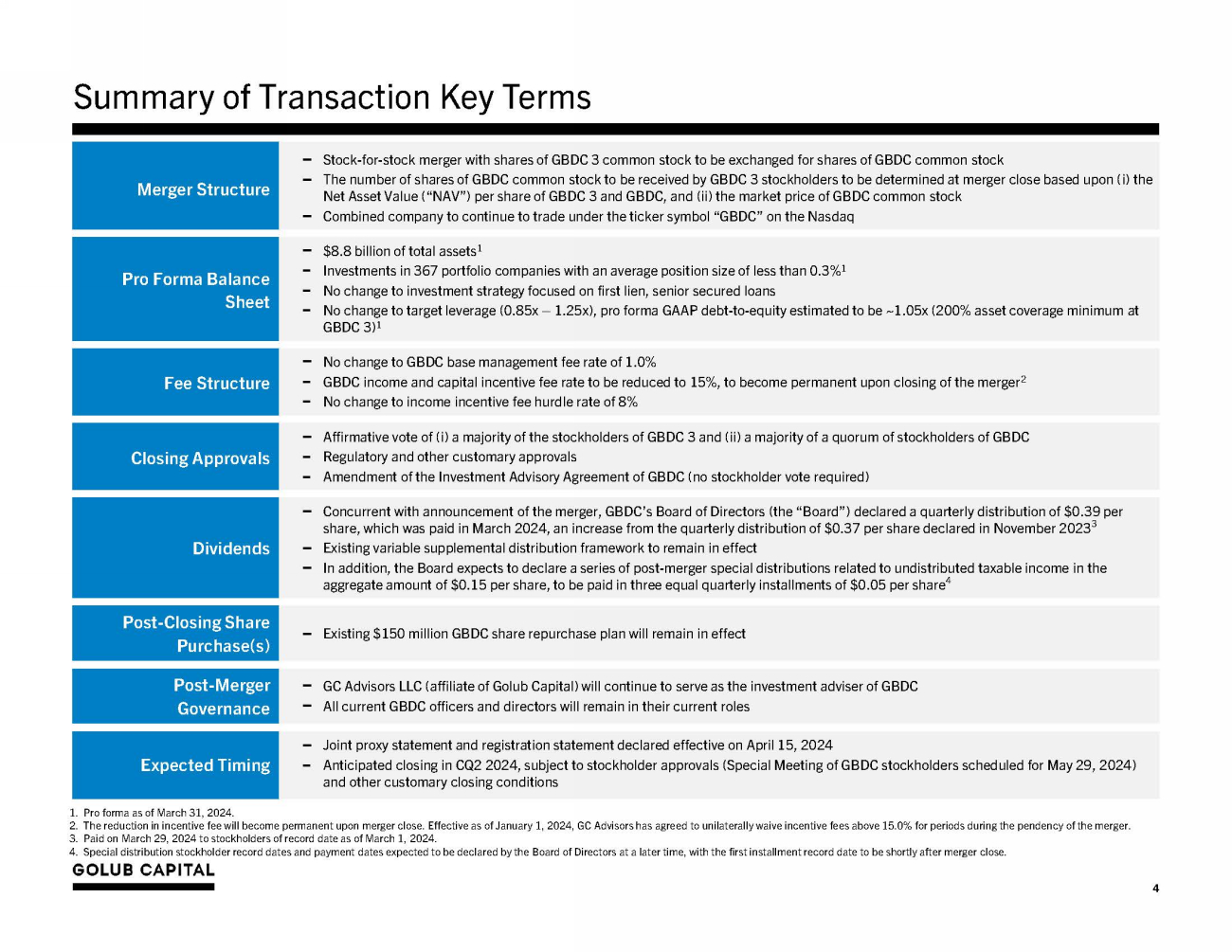

Merger Structure − Stock - for - stock merger with shares of GBDC 3 common stock to be exchanged for shares of GBDC common stock − The number of shares of GBDC common stock to be received by GBDC 3 stockholders to be determined at merger close based upon (i) the Net Asset Value (“NAV”) per share of GBDC 3 and GBDC, and (ii) the market price of GBDC common stock − Combined company to continue to trade under the ticker symbol “GBDC” on the Nasdaq Pro Forma Balance S h ee t − $8.8 billion of total assets 1 − Investments in 367 portfolio companies with an average position size of less than 0.3% 1 − No change to investment strategy focused on first lien, senior secured loans − No change to target leverage (0.85x – 1.25x), pro forma GAAP debt - to - equity estimated to be ~1.05x (200% asset coverage minimum at GBDC 3) 1 Fee Structure − No change to GBDC base management fee rate of 1.0% − GBDC income and capital incentive fee rate to be reduced to 15%, to become permanent upon closing of the merger 2 − No change to income incentive fee hurdle rate of 8% Closing Approvals − Affirmative vote of (i) a majority of the stockholders of GBDC 3 and (ii) a majority of a quorum of stockholders of GBDC − Regulatory and other customary approvals − Amendment of the Investment Advisory Agreement of GBDC (no stockholder vote required) D i v id e nd s − Concurrent with announcement of the merger, GBDC’s Board of Directors (the “Board”) declared a quarterly distribution of $0.39 per share, which was paid in March 2024, an increase from the quarterly distribution of $0.37 per share declared in November 2023 3 − Existing variable supplemental distribution framework to remain in effect − In addition, the Board expects to declare a series of post - merger special distributions related to undistributed taxable income in the aggregate amount of $0.15 per share, to be paid in three equal quarterly installments of $0.05 per share 4 Post - Closing Share P u r chas e ( s ) − Existing $150 million GBDC share repurchase plan will remain in effect Po s t - M e r g e r G o ve r nan c e − GC Advisors LLC (affiliate of Golub Capital) will continue to serve as the investment adviser of GBDC − All current GBDC officers and directors will remain in their current roles Expected Timing − Joint proxy statement and registration statement declared effective on April 15, 2024 − Anticipated closing in CQ2 2024, subject to stockholder approvals (Special Meeting of GBDC stockholders scheduled for May 29, 2024) and other customary closing conditions 4 Summary of Transaction Key Terms 1. Pro forma as of March 31, 2024. 2. The reduction in incentive fee will become permanent upon merger close. Effective as of January 1, 2024, GC Advisors has agreed to unilaterally waive incentive fees above 15.0% for periods during the pendency of the merger. 3. Paid on March 29, 2024 to stockholders of record date as of March 1, 2024. 4. Special distribution stockholder record dates and payment dates expected to be declared by the Board of Directors at a later time, with the first installment record date to be shortly after merger close.

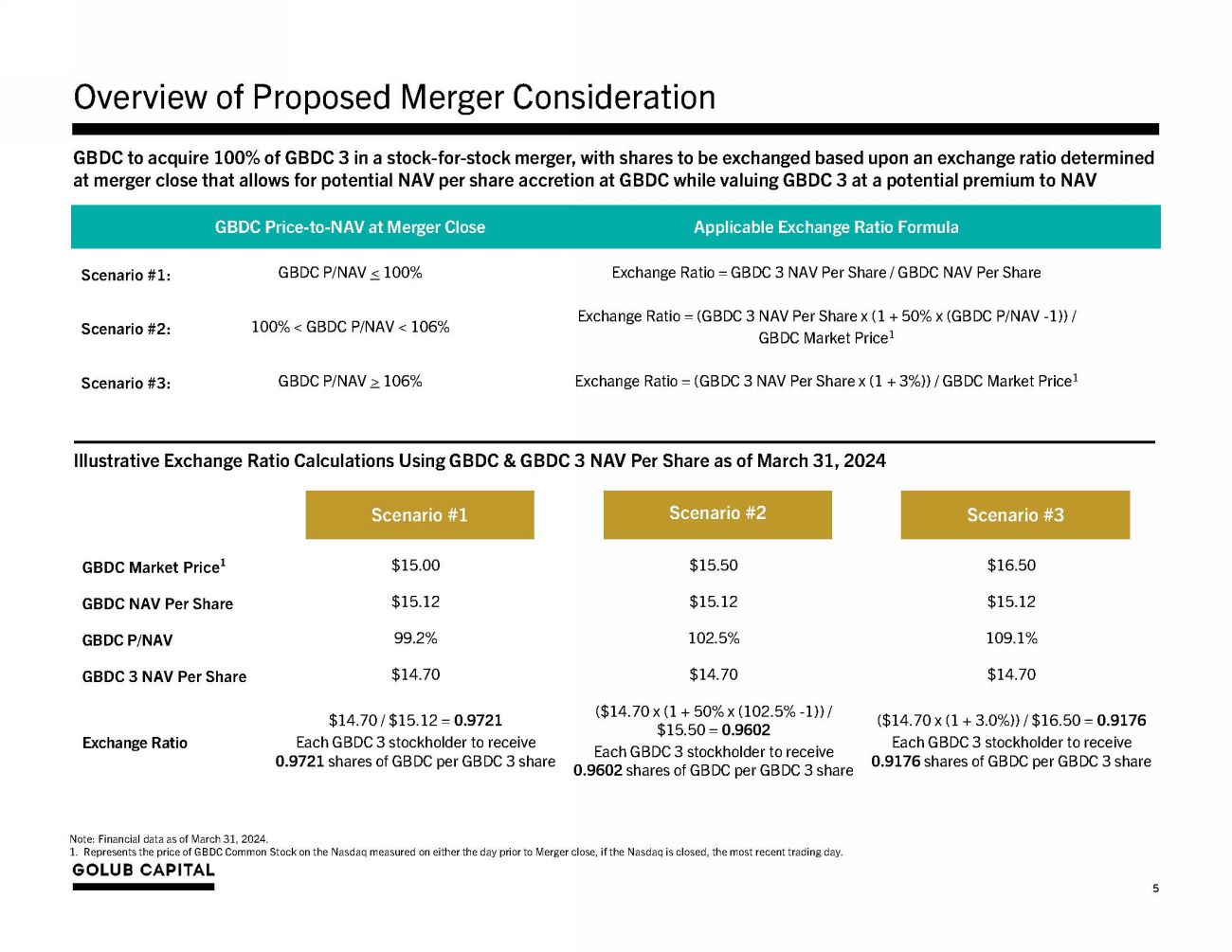

GBDC to acquire 100% of GBDC 3 in a stock - for - stock merger, with shares to be exchanged based upon an exchange ratio determined at merger close that allows for potential NAV per share accretion at GBDC while valuing GBDC 3 at a potential premium to NAV Overview of Proposed Merger Consideration Illustrative Exchange Ratio Calculations Using GBDC & GBDC 3 NAV Per Share as of March 31, 2024 1. Represents the price of GBDC Common Stock on the Nasdaq measured on either the day prior to Merger close, if the Nasdaq is closed, the most recent trading day. 5 GBDC Price - to - NAV at Merger Close Applicable Exchange Ratio Formula Scenario #1: GBDC P/NAV < 100% Exchange Ratio = GBDC 3 NAV Per Share / GBDC NAV Per Share Scenario #2: 100% < GBDC P/NAV < 106% Exchange Ratio = (GBDC 3 NAV Per Share x (1 + 50% x (GBDC P/NAV - 1)) / GBDC Market Price 1 Scenario #3: GBDC P/NAV > 106% Exchange Ratio = (GBDC 3 NAV Per Share x (1 + 3%)) / GBDC Market Price 1 Scenario #1 Scenario #2 GBDC Market Price 1 $15.00 $15.50 $16.50 GBDC NAV Per Share $15.12 $15.12 $15.12 GBDC P/NAV 99.2% 102.5% 109.1% GBDC 3 NAV Per Share $14.70 $14.70 $14.70 Exchange Ratio $14.70 / $15.12 = 0.9721 Each GBDC 3 stockholder to receive 0.9721 shares of GBDC per GBDC 3 share ($14.70 x (1 + 50% x (102.5% - 1)) / $15.50 = 0.9602 Each GBDC 3 stockholder to receive 0.9602 shares of GBDC per GBDC 3 share ($14.70 x (1 + 3.0%)) / $16.50 = 0.9176 Each GBDC 3 stockholder to receive 0.9176 shares of GBDC per GBDC 3 share Note: Financial data as of March 31, 2024. Scenario #3

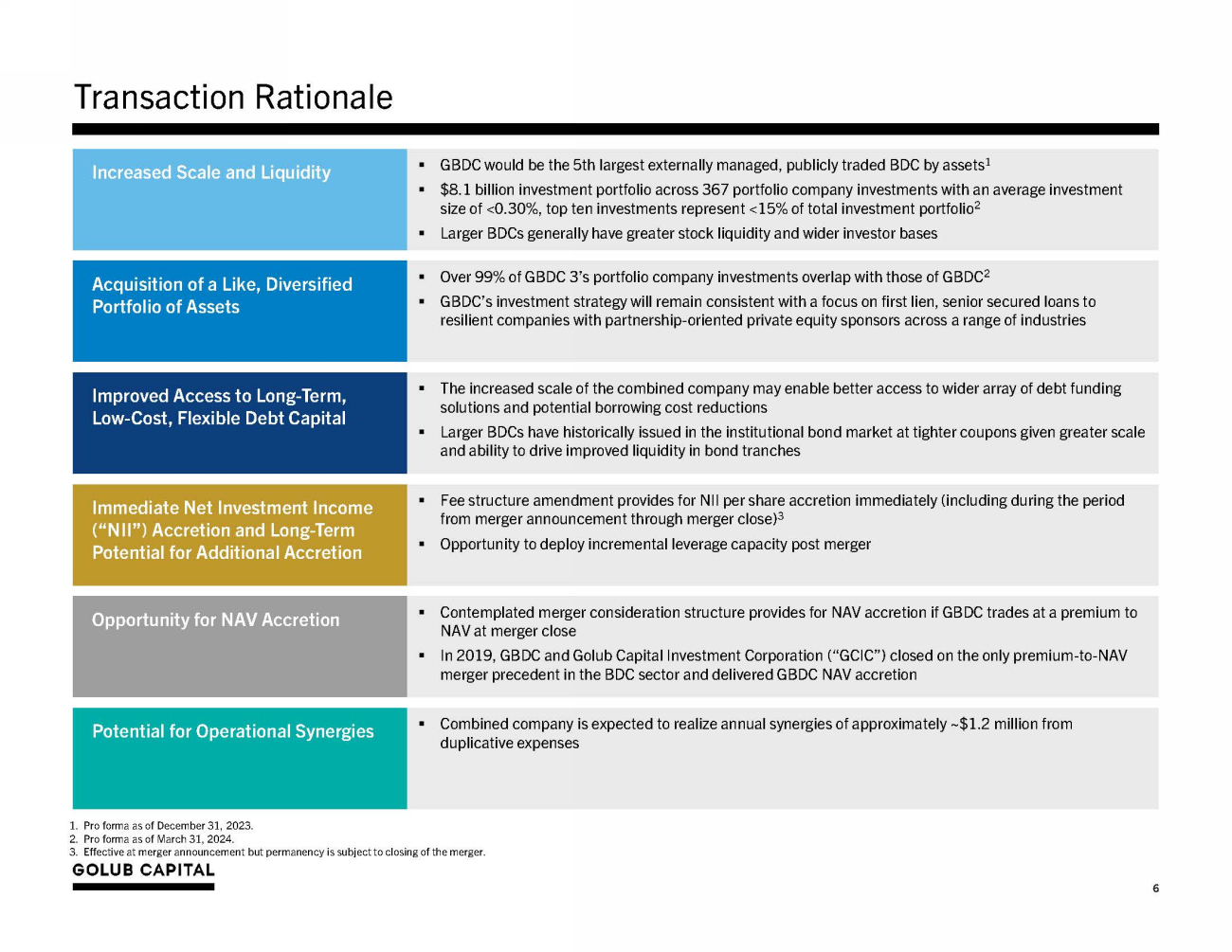

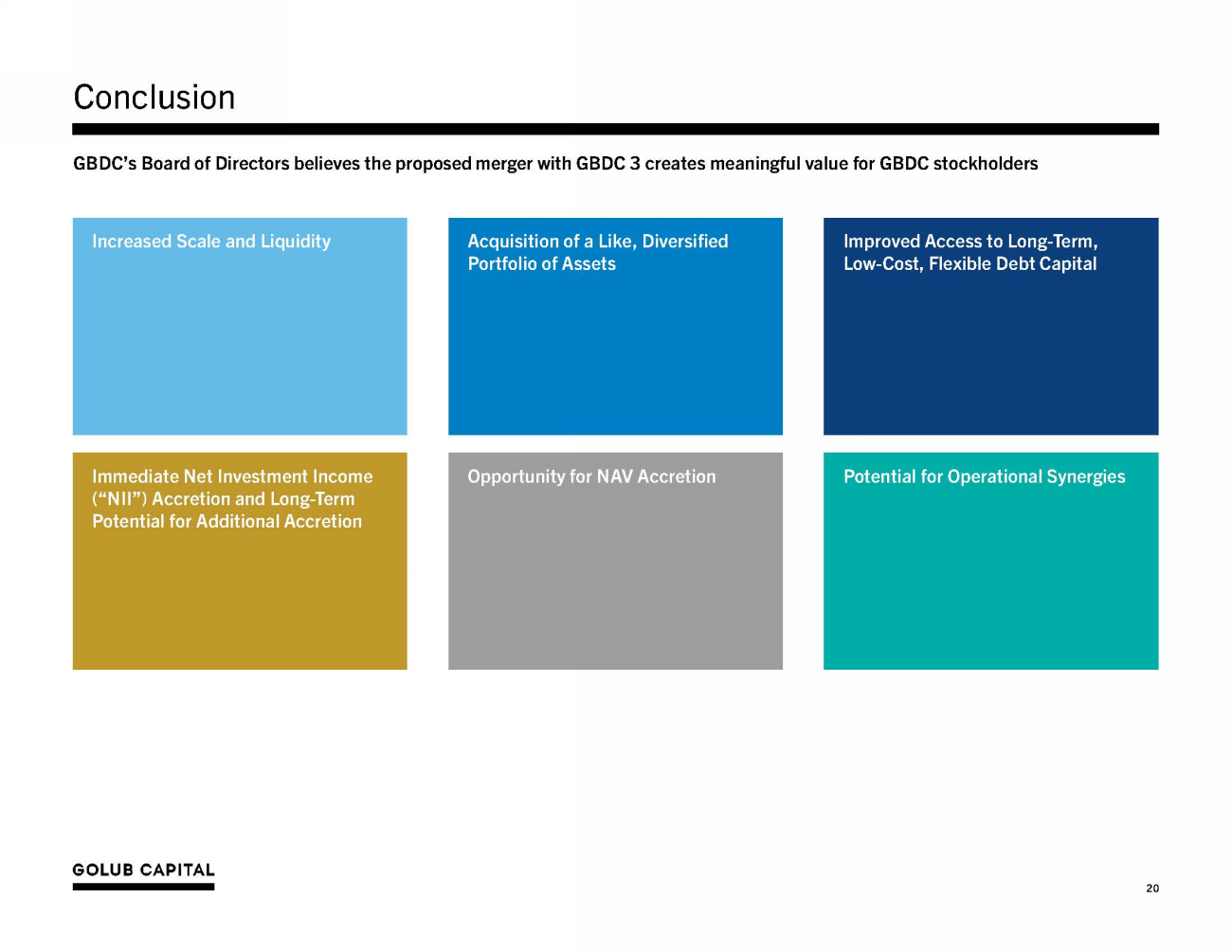

Transaction Rationale 3. Effective at merger announcement but permanency is subject to closing of the merger. 6 ▪ GBDC would be the 5th largest externally managed, publicly traded BDC by assets 1 ▪ $8.1 billion investment portfolio across 367 portfolio company investments with an average investment size of <0.30%, top ten investments represent <15% of total investment portfolio 2 ▪ Larger BDCs generally have greater stock liquidity and wider investor bases Increased Scale and Liquidity ▪ Over 99% of GBDC 3’s portfolio company investments overlap with those of GBDC 2 ▪ GBDC’s investment strategy will remain consistent with a focus on first lien, senior secured loans to resilient companies with partnership - oriented private equity sponsors across a range of industries Acquisition of a Like, Diversified Portfolio of Assets ▪ The increased scale of the combined company may enable better access to wider array of debt funding solutions and potential borrowing cost reductions ▪ Larger BDCs have historically issued in the institutional bond market at tighter coupons given greater scale and ability to drive improved liquidity in bond tranches Improved Access to Long - Term, Low - Cost, Flexible Debt Capital ▪ Combined company is expected to realize annual synergies of approximately ~$1.2 million from duplicative expenses Potential for Operational Synergies ▪ Contemplated merger consideration structure provides for NAV accretion if GBDC trades at a premium to NAV at merger close ▪ In 2019, GBDC and Golub Capital Investment Corporation (“GCIC”) closed on the only premium - to - NAV merger precedent in the BDC sector and delivered GBDC NAV accretion Opportunity for NAV Accretion ▪ Fee structure amendment provides for NII per share accretion immediately (including during the period from merger announcement through merger close) 3 ▪ Opportunity to deploy incremental leverage capacity post merger Immediate Net Investment Income (“NII”) Accretion and Long - Term Potential for Additional Accretion 1. Pro forma as of December 31, 2023. 2. Pro forma as of March 31, 2024.

GBDC 3 Overview Note: Past performance does not guarantee future results. Investments are subject to risk of loss. 1. As of March 31, 2024. 2. Represents annualized average quarterly return on equity since inception. Return on equity calculations are based on the daily weighted average of total net assets during the individual quarters. 3. The 9.3% Internal rate of return (“IRR”) on NAV is calculated at the fund level using beginning of period NAV, capital share issuances during the period, distributions paid or payable during the period, and ending period NAV. Period beginning August 1, 2017 and ending March 31, 2024. The first investment in GBDC 3 took place on August 1, 2017. These returns do not represent an actual return to any investor in GBDC 3. 4. Refers to investments with GC Advisors’ internal performance ratings of 4 or 5. Our internal performance ratings do not constitute any rating of investments by a nationally recognized statistical rating organization or represent or ▪ Commenced operations October 2, 2017 ▪ Managed by GC Advisors, an affiliate of Golub Capital ▪ $1.4 billion in investor capital subscriptions 1 , primarily from institutional investors including marquee pension funds, insurance companies, endowments and foundations ▪ Intent from inception to seek a liquidity event and to use commercially reasonable efforts to wind down if no liquidity event occurred within six years of the initial closing (to the extent consistent with its fiduciary duties) ▪ Stockholders approved an extension of the investment period in October 2023 by two years to October 2025 ▪ Approximately $2.7 billion investment portfolio focused on floating rate, first lien senior secured loans to middle market companies controlled by private equity sponsors; well diversified with 319 portfolio company investments and an average position size of 0.3% 1 ▪ Solid performance to date with an average quarterly return on equity of 9.2% 2 and an investor internal rate of return since inception of 9.3% 3 ▪ Strong credit results. Net realized and unrealized gains on investments for 20 out of 26 quarters since inception. Over 90% of portfolio is performing at or above expectations and only four portfolio company investments are on non - accrual as of March 31, 2024 1,4 Golub Capital BDC 3, Inc. Quarterly Returns on Equity While Private (Net of Management Fees, Incentive Fees and all other Expenses) 8.3% Avg. 2.3% 1.8% 3.1% 3.1% 2.7% 2.3% 2.1% 2.5% 3.0% 2.4% reflect any third - party assessment of any of our investments. 7 (8.7%) Dec - Mar - Jun - Sep - Dec - Mar - Jun - Sep - Dec - Mar - Jun - 17 18 18 18 18 19 19 19 19 20 20 3.5% 3.1% 3.5% 2.5% 2.2% 2.6% 2.5% 0.4% 0.7% 1.0% 2.5% 2.8% 3.0% 3.6% 3.6% Sep - Dec - Mar - Jun - Sep - Dec - Mar - 20 20 21 21 21 21 22 Jun - Sep - Dec - Mar - Jun - Sep - Dec - Mar - 22 22 22 23 23 23 23 24

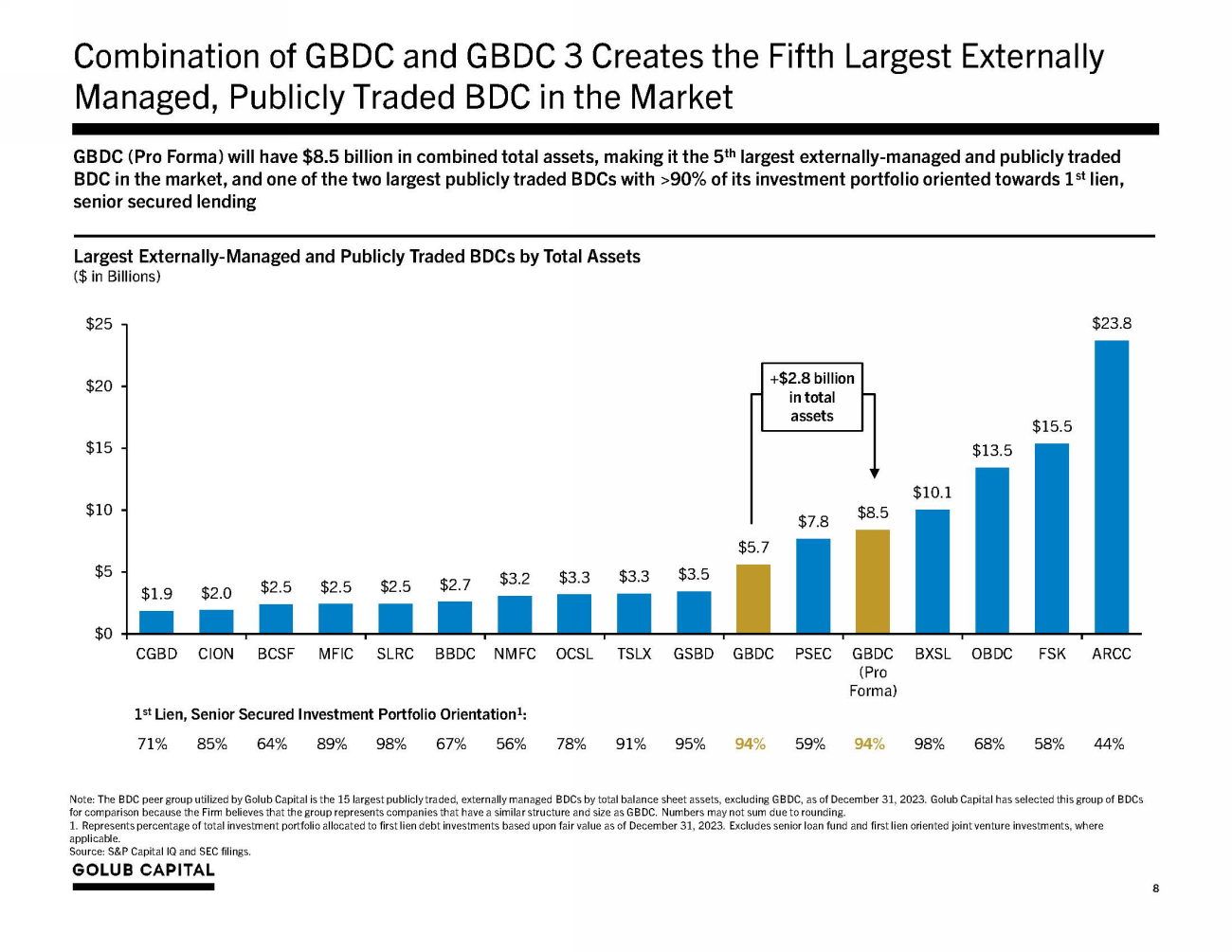

Combination of GBDC and GBDC 3 Creates the Fifth Largest Externally Managed, Publicly Traded BDC in the Market $1 . 9 $2 . 0 $2 . 5 $2 . 5 $ 2 . 5 $2 . 7 $3 . 2 $3 . 3 $3 . 3 $3 . 5 $ 5 . 7 $ 7 . 8 $8 . 5 $10 . 1 $13 . 5 $15 . 5 $23 . 8 $0 $5 $10 $15 $20 $25 C G BD C I O N B C S F M F IC S LR C B B DC N M F C O CSL T S LX G S B D G BD C PS E C G BD C B X S L (Pro F o r m a) O BD C F S K AR CC GBDC (Pro Forma) will have $ 8 . 5 billion in combined total assets, making it the 5 th largest externally - managed and publicly traded BDC in the market, and one of the two largest publicly traded BDCs with > 90 % of its investment portfolio oriented towards 1 st lien, senior secured lending Largest Externally - Managed and Publicly Traded BDCs by Total Assets ( $ in Billions) Note: The BDC peer group utilized by Golub Capital is the 15 largest publicly traded, externally managed BDCs by total balance sheet assets, excluding GBDC, as of December 31, 2023. Golub Capital has selected this group of BDCs for comparison because the Firm believes that the group represents companies that have a similar structure and size as GBDC. Numbers may not sum due to rounding. 1. Represents percentage of total investment portfolio allocated to first lien debt investments based upon fair value as of December 31, 2023. Excludes senior loan fund and first lien oriented joint venture investments, where applicable. +$2.8 billion in total assets Source: S&P Capital IQ and SEC filings. 8 1 st Lien, Senior Secured Investment Portfolio Orientation 1 : 71% 85% 64% 89% 98% 67% 56% 78% 91% 95% 94% 59% 94% 98% 68% 58% 44%

Larger BDCs Generally Have Improved Trading Liquidity Market Capitalization and Average Daily Trading Volume of Largest Externally - Managed and Publicly Traded BDCs ($ in Millions) Note: The BDC peer group utilized by Golub Capital is the 15 largest publicly traded, externally managed BDCs by total balance sheet assets, excluding GBDC, as of September 30, 2023. Golub Capital has selected this group of BDCs for comparison because the Firm believes that the group represents companies that have a similar structure and size as GBDC. Note: Market data as of January 16, 2024. FSK BXSL GBDC GBDC (Pro Forma) 1 Market C apit alization 30 - Day Average Daily Trading Volume $0.0 1. GBDC (Pro Forma) market capitalization assumes application of GBDC’s P/NAV premium (as of January 16, 2024) to GBDC 3’s NAV as of September 30, 2023; does not reflect merger adjustments. Source: S&P Capital IQ. 9 $10.0 $20.0 $30.0 $40.0 $50.0 $60.0 $70.0 $80.0 $0 $2 , 000 $4 , 000 $6,000 $8 , 000 $10,000 $12,000 ARCC O BD C PS E C TS L X OCS L G S B D N M F C BCS F B B D C M F IC S LR C CGB D CION

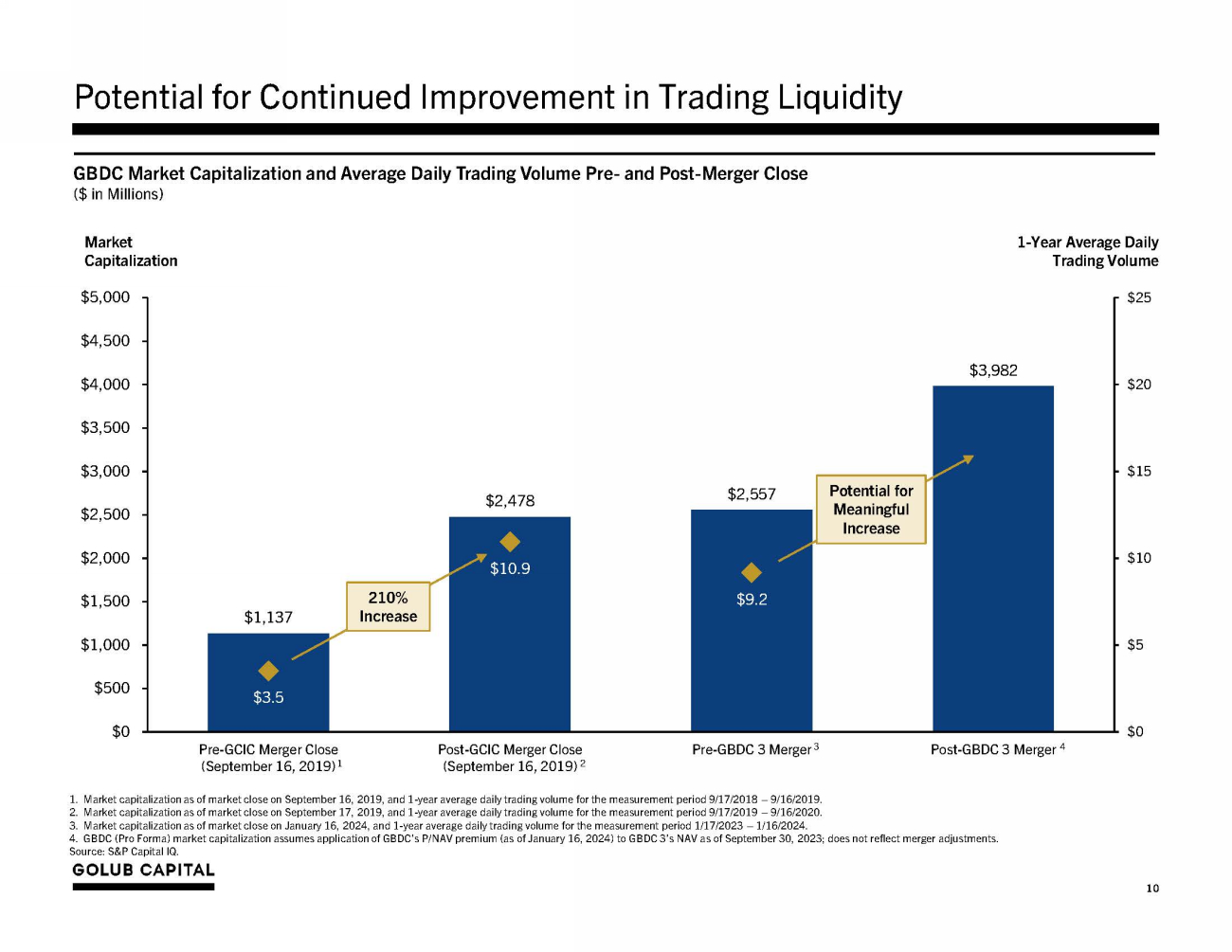

$1 , 137 $2 , 478 $2 , 557 $3 , 982 $3 . 5 $10 . 9 $9 . 2 $0 $5 $10 $15 $20 $25 $0 $500 $1 , 000 $1 , 500 $2 , 000 $2 , 500 $3 , 000 $3,500 $4 , 000 $4 , 500 $5 , 000 Pre - GCIC Merger Close (September 16, 2019) 1 Post - GCIC Merger Close (September 16, 2019) 2 Pre - GBDC 3 Merger 3 Post - GBDC 3 Merger 4 Potential for Continued Improvement in Trading Liquidity GBDC Market Capitalization and Average Daily Trading Volume Pre - and Post - Merger Close ($ in Millions) Market C apit alization 1 - Year Average Daily Trading Volume 210% Increase 1. Market capitalization as of market close on September 16, 2019, and 1 - year average daily trading volume for the measurement period 9/17/2018 – 9/16/2019. 2. Market capitalization as of market close on September 17, 2019, and 1 - year average daily trading volume for the measurement period 9/17/2019 – 9/16/2020. 3. Market capitalization as of market close on January 16, 2024, and 1 - year average daily trading volume for the measurement period 1/17/2023 – 1/16/2024. Potential for Meaningful Increase 4. GBDC (Pro Forma) market capitalization assumes application of GBDC’s P/NAV premium (as of January 16, 2024) to GBDC 3’s NAV as of September 30, 2023; does not reflect merger adjustments. Source: S&P Capital IQ. 10

Substantial Overlap in Highly Diversified Investment Portfolios Pro Forma GBDC Diversity by Portfolio Company (% of Total Investment Portfolio at Fair Value) Avg. Size 0.3% Top 10 Portfolio Companies 16% Top 25 Portfolio Companies 31% Remaining 341 Portfolio Companies 69% Note: Financial data as of March 31, 2024. G B D C GBDC 3 Avg. Size 0.3% Top 10 Portfolio Companies 16% Top 25 Portfolio Companies 34% Remaining 294 Portfolio Companies 66% Avg. Size 0.3% Pro Forma GBDC Top 10 Portfolio C o mpan ies 15% Top 25 Portfolio Companies 30% Remaining 332 Portfolio Companies 70% 366 Investments 1 319 Investments 1 Overl a p p i n g 88.0% GBDC & GBDC 3 Overlapping Portfolio Company Investments (% of Total Investment Portfolio at Fair Value) GBDC Non - Overl a p p i n g 12.0% Overl a p p i n g 99.6% 1. Denotes the total number of portfolio company investments. 11 GBDC 3 Non - Overlapping 0.4%

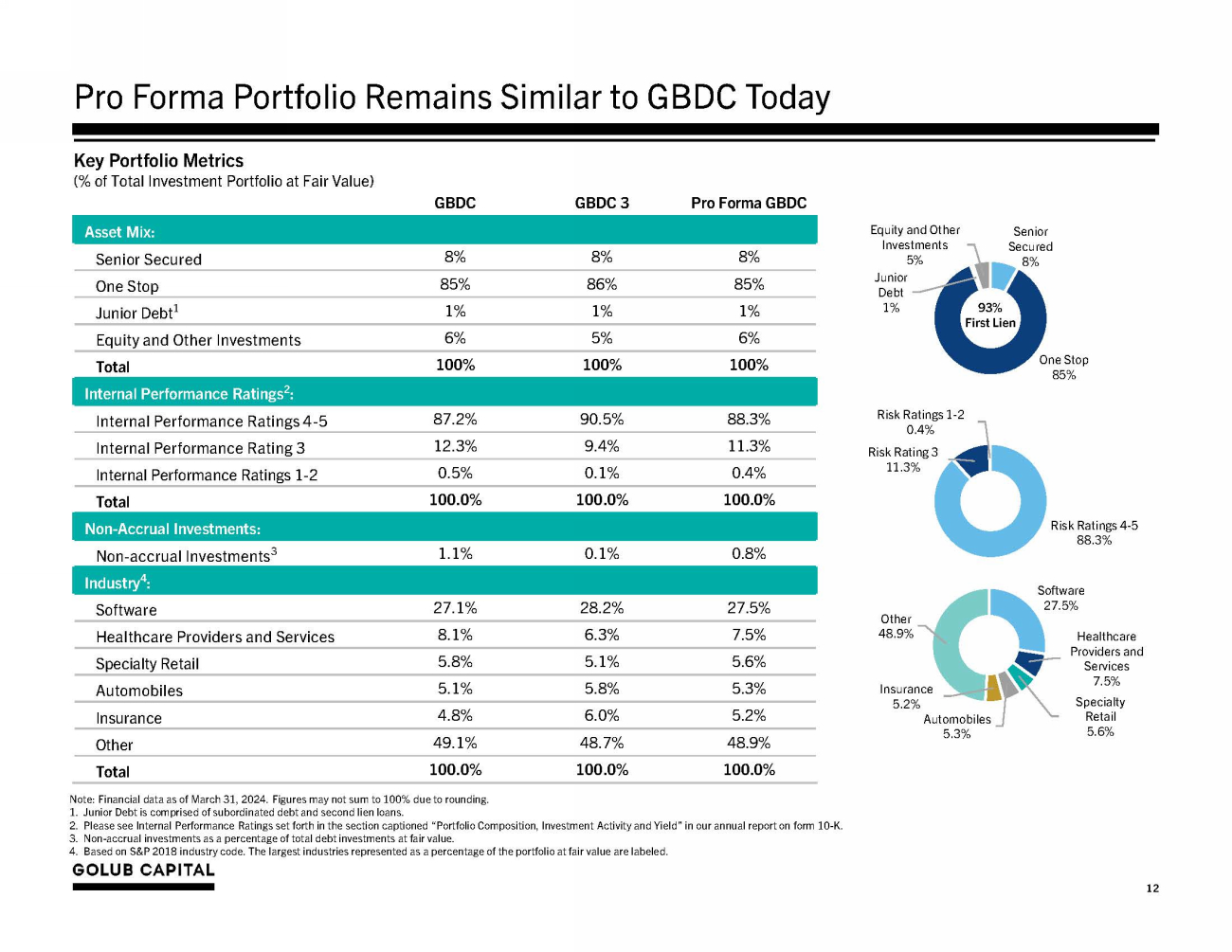

Healthcare Providers and Services 7.5% S p e c ia lty Retail 5.6% Insuran c e 5.2% Automob ile s 5.3% Other 48 . 9 % Risk Ratings 4 - 5 88.3% Software 27.5% Senior S e c ure d 8% One Stop 85% Risk Ratings 1 - 2 0.4% Risk Rating 3 11.3% Equity and Other Investments 5% Junior Debt 1 % Pro Forma Portfolio Remains Similar to GBDC Today GBDC GBDC 3 Pro Forma GBDC Asset Mix: Senior Secured 8% 8% 8% One Stop 85% 86% 85% Junior Debt 1 1% 1% 1% Equity and Other Investments 6% 5% 6% Total 100% 100% 100% Internal Performance Ratings 2 : Internal Performance Ratings 4 - 5 87.2% 90.5% 88.3% Internal Performance Rating 3 12.3% 9.4% 11.3% Internal Performance Ratings 1 - 2 0.5% 0.1% 0.4% Total 100.0% 100 . 0 % 100.0% Non - Accrual Investments: Non - accrual Investments 3 1.1% 0.1% 0.8% Industry 4 : Software 27.1% 28.2% 27.5% Healthcare Providers and Services 8.1% 6.3% 7.5% Specialty Retail 5.8% 5.1% 5.6% Automobiles 5.1% 5.8% 5.3% Insurance 4.8% 6.0% 5.2% Other 49.1% 48.7% 48.9% Total 100.0% 100 . 0 % 100.0% Note: Financial data as of March 31, 2024. Figures may not sum to 100% due to rounding. 1. Junior Debt is comprised of subordinated debt and second lien loans. 2. Please see Internal Performance Ratings set forth in the section captioned “Portfolio Composition, Investment Activity and Yield” in our annual report on form 10 - K. 3. Non - accrual investments as a percentage of total debt investments at fair value. Key Portfolio Metrics (% of Total Investment Portfolio at Fair Value) 4. Based on S&P 2018 industry code. The largest industries represented as a percentage of the portfolio at fair value are labeled. 12 93% First Lien

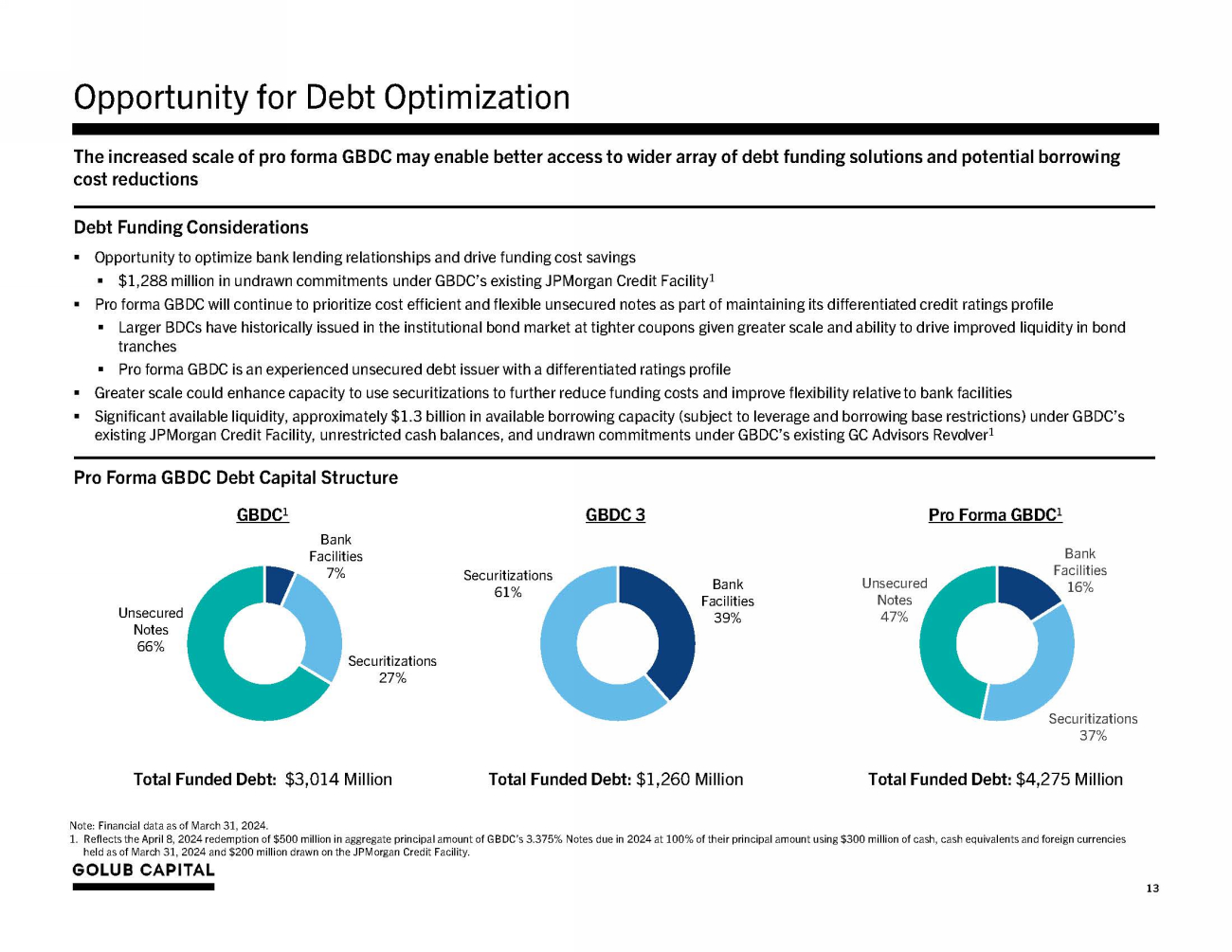

Bank Fa c ilit ie s 16% U n s ecu red Notes 47% Bank Fa c ilit ie s 39% S e curi t iz a t ions 61% Bank Fa c ilit ie s 7% Securitizations 27% U n s ecu red Notes 66% Sec u rit iz at i o n s 37% Total Funded Debt: $3,014 Million Total Funded Debt: $1,260 Million Total Funded Debt: $4,275 Million Note: Financial data as of March 31, 2024. 1. Reflects the April 8, 2024 redemption of $500 million in aggregate principal amount of GBDC’s 3.375% Notes due in 2024 at 100% of their principal amount using $300 million of cash, cash equivalents and foreign currencies Opportunity for Debt Optimization Pro Forma GBDC Debt Capital Structure GBDC 1 GBDC 3 Pro Forma GBDC 1 The increased scale of pro forma GBDC may enable better access to wider array of debt funding solutions and potential borrowing cost reductions Debt Funding Considerations ▪ Opportunity to optimize bank lending relationships and drive funding cost savings ▪ $1,288 million in undrawn commitments under GBDC’s existing JPMorgan Credit Facility 1 ▪ Pro forma GBDC will continue to prioritize cost efficient and flexible unsecured notes as part of maintaining its differentiated credit ratings profile ▪ Larger BDCs have historically issued in the institutional bond market at tighter coupons given greater scale and ability to drive improved liquidity in bond tranches ▪ Pro forma GBDC is an experienced unsecured debt issuer with a differentiated ratings profile ▪ Greater scale could enhance capacity to use securitizations to further reduce funding costs and improve flexibility relative to bank facilities ▪ Significant available liquidity, approximately $1.3 billion in available borrowing capacity (subject to leverage and borrowing base restrictions) under GBDC’s existing JPMorgan Credit Facility, unrestricted cash balances, and undrawn commitments under GBDC’s existing GC Advisors Revolver 1 held as of March 31, 2024 and $200 million drawn on the JPMorgan Credit Facility. 13

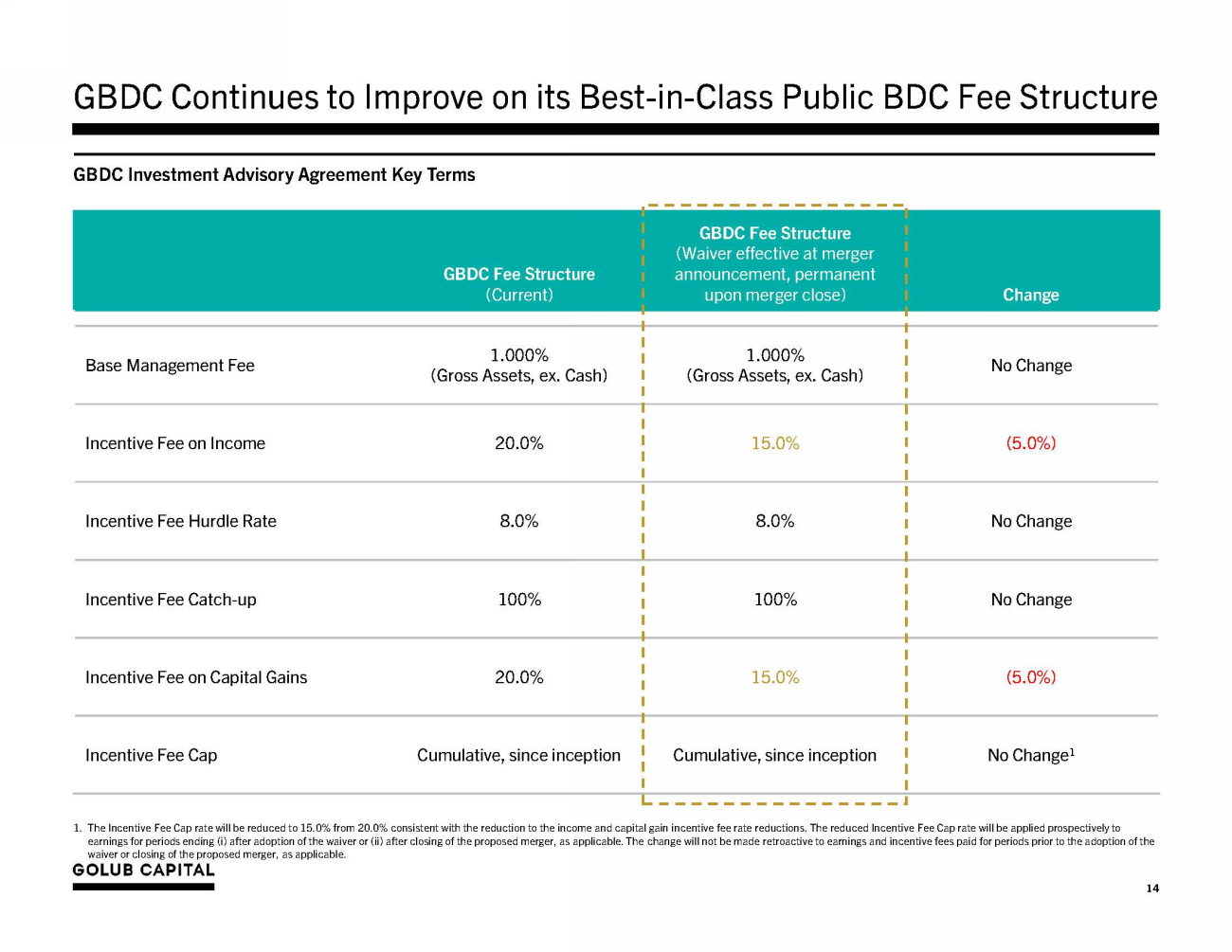

GBDC Continues to Improve on its Best - in - Class Public BDC Fee Structure GBDC Investment Advisory Agreement Key Terms GBDC Fee Structure (Current) GBDC Fee Structure (Waiver effective at merger announcement, permanent upon merger close) Change Base Management Fee 1.000% (Gross Assets, ex. Cash) 1.000% (Gross Assets, ex. Cash) No Change Incentive Fee on Income 20.0% 15.0% (5.0%) Incentive Fee Hurdle Rate 8.0% 8.0% No Change Incentive Fee Catch - up 100% 100% No Change Incentive Fee on Capital Gains 20.0% 15.0% (5.0%) Incentive Fee Cap Cumulative, since inception Cumulative, since inception No Change 1 waiver or closing of the proposed merger, as applicable. 14 1. The Incentive Fee Cap rate will be reduced to 15.0% from 20.0% consistent with the reduction to the income and capital gain incentive fee rate reductions. The reduced Incentive Fee Cap rate will be applied prospectively to earnings for periods ending (i) after adoption of the waiver or (ii) after closing of the proposed merger, as applicable. The change will not be made retroactive to earnings and incentive fees paid for periods prior to the adoption of the

Income Incentive Fee Hurdle Rate 8.0% GBDC 8.0% NMFC 7.0% AR C C FSK GSBD P SEC 6.0% - 6.5% BCSF BXSL O BD C OCSL TSLX Base Management Fee Charged on Cash? No GBDC AR C C BC SF FSK No GSBD NM FC O BD C OCSL B X SL Yes P SEC TSL X (% of Gross Ass ets) B ase Mana geme nt F ee A 1.00% GBDC 1.00% B X SL GSB D 1.50% AR C C BC SF FSK N M F C 1 O BD C O C SL TSL X 1.75% - 2.00% PSEC ( % of Pre - Incentive Fee NII) Income Incentive Fee 15.0% GBDC 17.5% BC SF BXSL FSK O BD C O CSL TSLX 20.0% ARCC GSBD N M FC PSEC The Gold Standard in Public BDC Fee Structures GREATEST DEGREE OF SHAREHOLDER ALIGNMENT GOLD STANDARD Note: The BDC peer group utilized by Golub Capital is the 10 largest publicly traded, externally managed BDCs by market capitalization, excluding GBDC, as of January 16, 2024. 1. Base management fee is calculated at an annual rate of 1.4% of NMFC’s gross assets. Pro forma fee structure positions GBDC to provide market - leading risk - adjusted returns across different economic and interest rate environments while keeping its investment strategy focused at the top of the capital structure (first lien, first out senior secured sponsor backed floating rate loan investment strategy) Incentive Fee Cap Measurement Period S ince G B D C Inception Trailing BCSF 3 Years BXSL GSBD AR C C FSK N M FC None O BD C OCSL PSEC TSLX Source: SEC Filings. 15

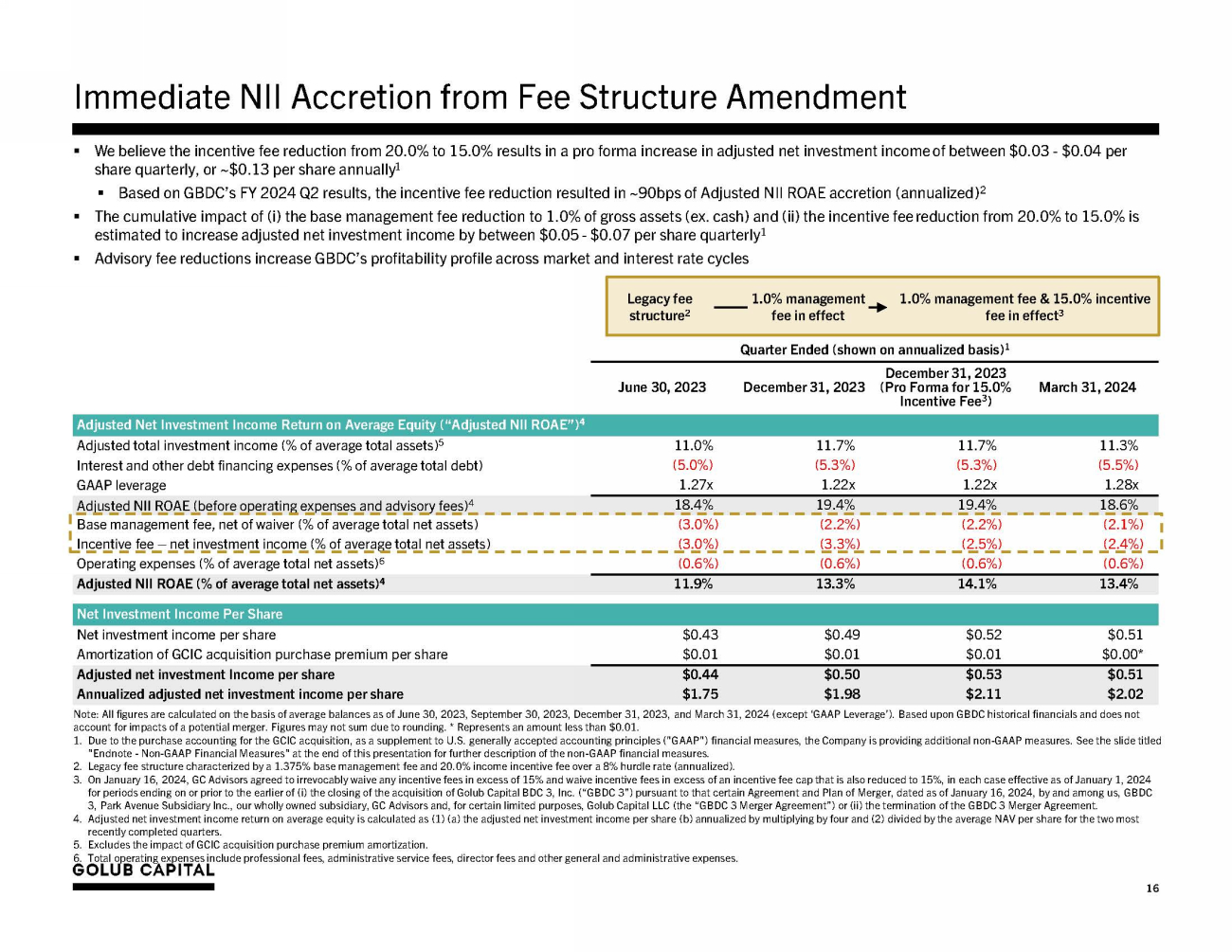

Immediate NII Accretion from Fee Structure Amendment Note : All figures are calculated on the basis of average balances as of June 30 , 2023 , September 30 , 2023 , December 31 , 2023 , and March 31 , 2024 (except ‘GAAP Leverage’) . Based upon GBDC historical financials and does not account for impacts of a potential merger . Figures may not sum due to rounding . * Represents an amount less than $ 0 . 01 . 1. Due to the purchase accounting for the GCIC acquisition, as a supplement to U . S . generally accepted accounting principles ("GAAP") financial measures, the Company is providing additional non - GAAP measures . See the slide titled "Endnote - Non - GAAP Financial Measures" at the end of this presentation for further description of the non - GAAP financial measures . 2. Legacy fee structure characterized by a 1 . 375 % base management fee and 20 . 0 % income incentive fee over a 8 % hurdle rate (annualized) . 3. On January 16 , 2024 , GC Advisors agreed to irrevocably waive any incentive fees in excess of 15 % and waive incentive fees in excess of an incentive fee cap that is also reduced to 15 % , in each case effective as of January 1 , 2024 for periods ending on or prior to the earlier of (i) the closing of the acquisition of Golub Capital BDC 3 , Inc . (“GBDC 3 ”) pursuant to that certain Agreement and Plan of Merger, dated as of January 16 , 2024 , by and among us, GBDC 3 , Park Avenue Subsidiary Inc . , our wholly owned subsidiary, GC Advisors and, for certain limited purposes, Golub Capital LLC (the “GBDC 3 Merger Agreement”) or (ii) the termination of the GBDC 3 Merger Agreement . 4. Adjusted net investment income return on average equity is calculated as ( 1 ) (a) the adjusted net investment income per share (b) annualized by multiplying by four and ( 2 ) divided by the average NAV per share for the two most recently completed quarters . 5. Excludes the impact of GCIC acquisition purchase premium amortization . ▪ We believe the incentive fee reduction from 20.0% to 15.0% results in a pro forma increase in adjusted net investment income of between $0.03 - $0.04 per share quarterly, or ~$0.13 per share annually 1 ▪ Based on GBDC’s FY 2024 Q2 results, the incentive fee reduction resulted in ~90bps of Adjusted NII ROAE accretion (annualized) 2 ▪ The cumulative impact of (i) the base management fee reduction to 1.0% of gross assets (ex. cash) and (ii) the incentive fee reduction from 20.0% to 15.0% is estimated to increase adjusted net investment income by between $0.05 - $0.07 per share quarterly 1 ▪ Advisory fee reductions increase GBDC’s profitability profile across market and interest rate cycles Legacy fee 1.0% management 1.0% management fee & 15.0% incentive structure 2 fee in effect fee in effect 3 Quarter Ended (shown on annualized basis) 1 June 30, 2023 December 31, 2023 December 31, 2023 (Pro Forma for 15.0% Incentive Fee 3 ) March 31, 2024 Adjusted Net Investment Income Return on Average Equity (“Adjusted NII ROAE”) 4 Adjusted total investment income (% of average total assets) 5 11.0% 11.7% 1 1.7% 11.3% Interest and other debt financing expenses (% of average total debt) (5.0%) (5.3%) (5.3%) (5.5%) GAAP leverage 1.27x 1.22x 1.22x 1.28x Adjusted NII ROAE (before operating expenses and advisory fees) 4 18.4% 19.4% 1 9.4% 18.6% Base management fee, net of waiver (% of average total net assets) (3.0%) (2.2%) (2.2%) (2.1%) Incentive fee – net investment income (% of average total net assets) (3.0%) (3.3%) (2.5%) (2.4%) Operating expenses (% of average total net assets) 6 (0.6%) (0.6%) (0.6%) (0.6%) Adjusted NII ROAE (% of average total net assets) 4 11.9% 13.3% 1 4.1% 13.4% Net Investment Income Per Share Net investment income per share $0.43 $0.49 $0.52 $0.51 Amortization of GCIC acquisition purchase premium per share $0.01 $0.01 $0.01 $0.00* Adjusted net investment Income per share $0.44 $0.50 $0.53 $0.51 Annualized adjusted net investment income per share $1.75 $1.98 $2.11 $2.02 6. Total operating expenses include professional fees, administrative service fees, director fees and other general and administrative expenses. 16

The Bottom Line for BDC Investors: Higher Returns, Lower Portfolio Risk, and Credit Outperformance Pro forma for the fee structure amendment, GBDC will be amongst the highest returning BDCs in the public BDC sector with a more meaningful 1 st lien senior secured focus and better underlying credit performance Net Investment Income Return on Average Equity Benchmarking for BDC Peers 1 (CQ4 2023, annualized) Note: Financial data as of December 31, 2023. The BDC peer group utilized by Golub Capital is the 15 largest publicly traded, externally managed BDCs by total balance sheet assets, excluding GBDC, as of December 31, 2023. Golub Capital has selected this group of BDCs for comparison because the Firm believes that the group represents companies that have a similar structure and size as GBDC. 1. Net investment income return on average equity is calculated as (1) (a) the net investment income per share excluding per share impact of capital gains incentive fees, where applicable, (b) annualized by multiplying by four, and (2) divided by the average NAV per share for the two most recently completed quarters. 2. GBDC (Pro Forma) is based on GBDC’s Adjusted Net Investment Income Return on Average Equity for the quarter ended December 31, 2023, pro forma for the incentive fee reduction from 20.0% to 15.0%. See Slide 16 for details. 3. GBDC and GBDC (Pro Forma) displays net investment income return on average equity based on adjusted net investment income; due to the purchase accounting for the GCIC acquisition, as a supplement to U.S. generally accepted accounting principles ("GAAP") financial measures, the Company is providing additional non - GAAP measures. See the slide titled "Endnote - Non - GAAP Financial Measures" at the end of this presentation for further description of the non - GAAP financial measures. 4. Represents percentage of total investment portfolio allocated to first lien debt investments based upon fair value as of December 31, 2023. Excludes senior loan fund and first lien oriented joint venture investments, where applicable. Source: S&P Capital IQ and SEC Filings. 1 st Lien, Senior Secured Investment Portfolio Orientation 4 : 95% 91% 98% 94% 94% 71% 68% 44% 56% 64% 58% 89% 78% 67% 59% 85% 98% Non - Accrual Investments as a % of Total Portfolio Investments at Fair Value: 2.3% 0.6% <0.1% 0.7% 1.0% 2.1% 0.9% 0.6% 1.7% 1.2% 5.5% 0.2% 4.0% 1.5% 0.2% 0.9% 0.4% GBDC (Pro Forma) 2,3 3 GB D C CGB D O BD C ARCC N M F C BCSF 15.1% 17 14.6% 14.4% 14.1% 13.3% 13.2% 13.2% 13.2% 12.3% 12.3% 12.2% 12.0% 11.8% 1 1 .0 % 10.6% 10.0% 9.7% GSBD TS L X B X S L FSK M F IC OCSL B B D C PS E C CION SL R C

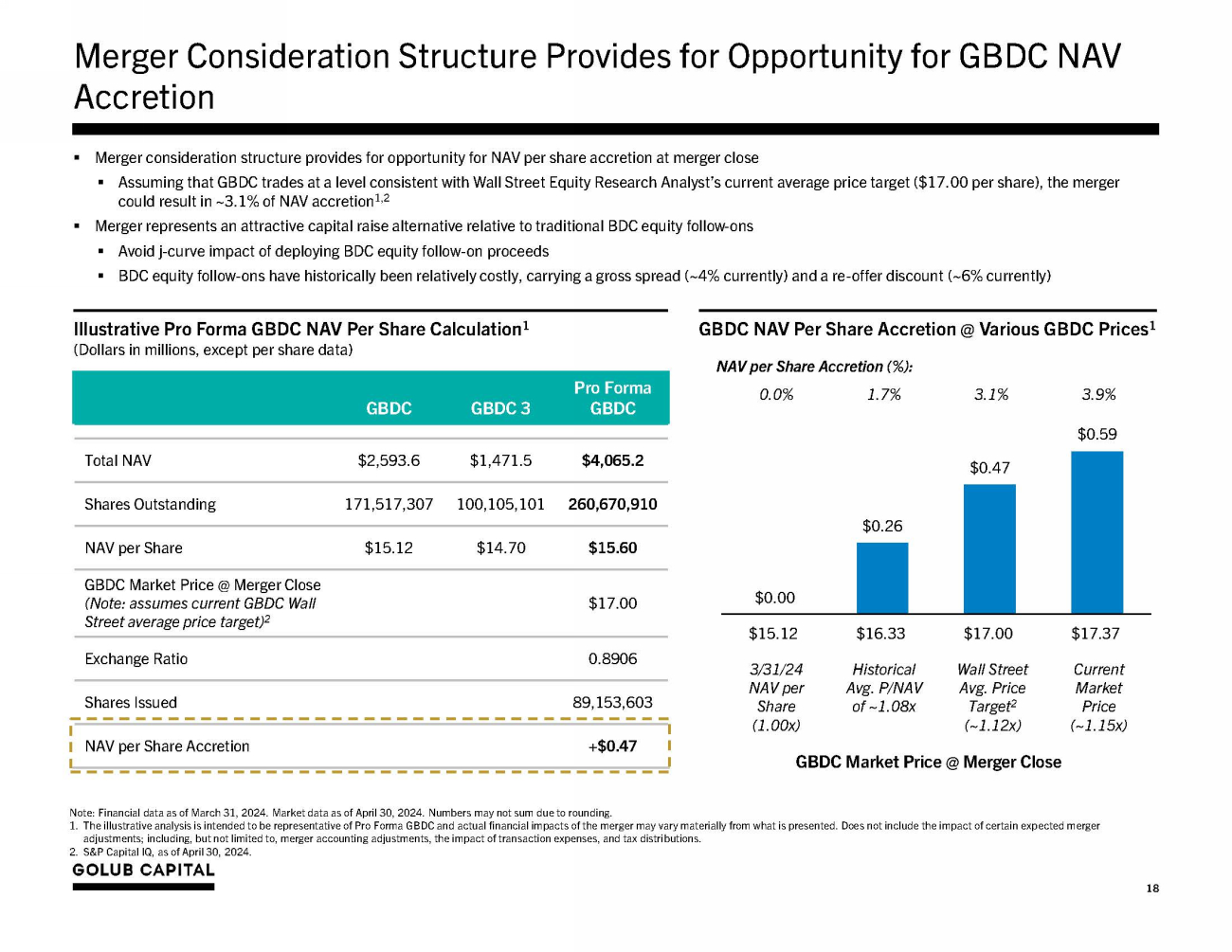

Merger Consideration Structure Provides for Opportunity for GBDC NAV Accretion Illustrative Pro Forma GBDC NAV Per Share Calculation 1 (Dollars in millions, except per share data) GBDC NAV Per Share Accretion @ Various GBDC Prices 1 NAV per Share Accretion (%): GBDC GBDC 3 Pro Forma GBDC Total NAV $2,593.6 $1,471.5 $4,065.2 Shares Outstanding 171,517,307 100,105,101 260,670,910 NAV per Share $15.12 $14.70 $15.60 GBDC Market Price @ Merger Close (Note: assumes current GBDC Wall Street average price target) 2 $17.00 Exchange Ratio 0.8906 Shares Issued 89,153,603 NAV per Share Accretion +$0.47 Note: Financial data as of March 31, 2024. Market data as of April 30, 2024. Numbers may not sum due to rounding. 1. The illustrative analysis is intended to be representative of Pro Forma GBDC and actual financial impacts of the merger may vary materially from what is presented. Does not include the impact of certain expected merger adjustments; including, but not limited to, merger accounting adjustments, the impact of transaction expenses, and tax distributions. 2. S&P Capital IQ, as of April 30, 2024. 0.0% 1.7% 3.1% 3.9% $0 . 59 $0.47 $0.26 $0.00 $15.12 $16.33 $17.00 $17 . 37 3/31/24 Historical Wall Street C u rr ent NAV per Avg. P/NAV Avg. Price Ma r k et Share (1.00x) of ~1.08x Target 2 (~1.12x) Price ( ~1 . 15 x ) 18 GBDC Market Price @ Merger Close ▪ Merger consideration structure provides for opportunity for NAV per share accretion at merger close ▪ Assuming that GBDC trades at a level consistent with Wall Street Equity Research Analyst’s current average price target ($17.00 per share), the merger could result in ~3.1% of NAV accretion 1,2 ▪ Merger represents an attractive capital raise alternative relative to traditional BDC equity follow - ons ▪ Avoid j - curve impact of deploying BDC equity follow - on proceeds ▪ BDC equity follow - ons have historically been relatively costly, carrying a gross spread (~4% currently) and a re - offer discount (~6% currently)

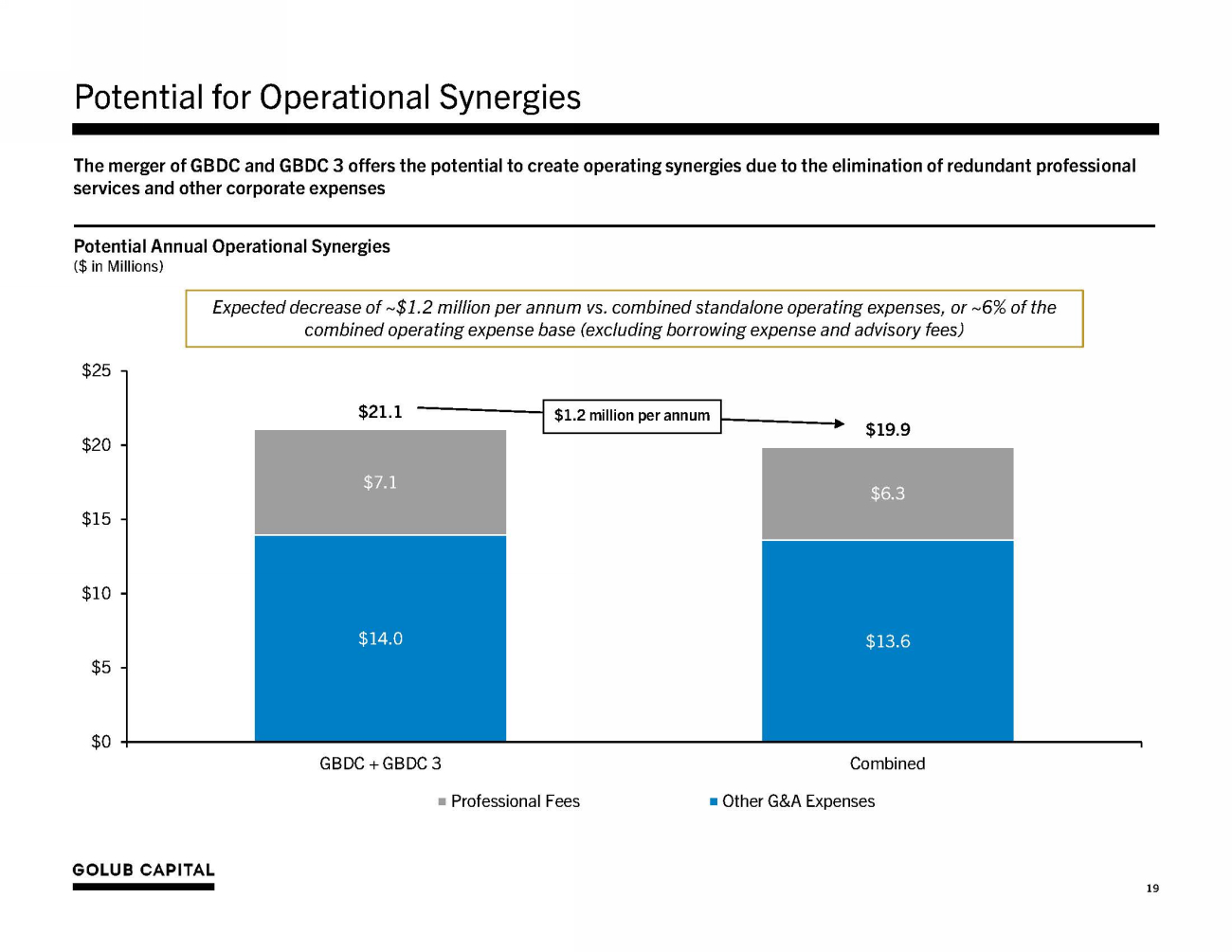

Potential for Operational Synergies $14.0 $13.6 $7.1 $6.3 $21.1 $19.9 $0 $5 $ 1 0 $ 1 5 $ 2 0 $ 2 5 GBDC + GBDC 3 Combined Other G&A Expenses Tot a l Professional Fees The merger of GBDC and GBDC 3 offers the potential to create operating synergies due to the elimination of redundant professional services and other corporate expenses Potential Annual Operational Synergies ($ in Millions) Expected decrease of ~$1.2 million per annum vs. combined standalone operating expenses, or ~6% of the combined operating expense base (excluding borrowing expense and advisory fees) 19 $1.2 million per annum

Conclusion 20 GBDC’s Board of Directors believes the proposed merger with GBDC 3 creates meaningful value for GBDC stockholders Increased Scale and Liquidity Acquisition of a Like, Diversified Portfolio of Assets Improved Access to Long - Term, Low - Cost, Flexible Debt Capital Potential for Operational Synergies Opportunity for NAV Accretion Immediate Net Investment Income (“NII”) Accretion and Long - Term Potential for Additional Accretion

Appendix 21 01

Appendix: Proposed Merger Consideration Structure GBDC to acquire 100% of GBDC 3 in a stock - for - stock transaction, with shares to be exchanged based on the following: iii. i. If the ratio of GBDC’s market price to GBDC’s NAV per share is less than or equal to 1 . 00 x then the exchange ratio is determined by the ratio of (a) GBDC 3 ’s NAV per share and (b) GBDC’s NAV per share at transaction close, or ii. If the ratio of GBDC’s market price to GBDC’s NAV per share is greater than 1 . 00 x but less than 1 . 06 x then the exchange ratio is determined by the ratio of (a) the product of ( 1 ) GBDC 3 ’s NAV per share and ( 2 ) 1 + 50 % of GBDC’s trading premium to GBDC’s NAV, and (b) GBDC’s market price at transaction close, or If the ratio of GBDC’s market price to GBDC’s NAV per share is greater than or equal to 1 . 06 x then the exchange ratio is determined by the ratio of (a) the product of ( 1 ) GBDC 3 ’s NAV per share and ( 2 ) 1 . 03 , and (b) GBDC’s market price at transaction close . Merger Consideration Description i. If the ratio of GBDC’s market price to GBDC’s NAV per share is less than or equal to 1.00x : ii. If the ratio of GBDC’s market price to GBDC’s NAV per share is greater than 1.00x but less than 1.06x: iii. If the ratio of GBDC’s market price to GBDC’s NAV per share is greater than or equal to 1.06x: Merger Consideration Formulaic Representation GBDC 3 NAV PER SHARE EX CH A NGE RATIO GBDC NAV PER SHARE GBDC 3 NAV PER SHARE x ( 1 + 50.0% x (GBDC MARKET PRICE / GBDC NAV PER SHARE - 1)) EX CH A NGE RATIO GBDC MARKET PRICE GBDC 3 NAV PER SHARE x 1.03 EX CH A NGE RATIO GBDC MARKET PRICE 22

Endnotes – Non - GAAP Financial Measures 23 1. On September 16 , 2019 , the Company completed its acquisition of GCIC . The merger was accounted for under the asset acquisition method of accounting in accordance with Accounting Standards Codification (“ASC”) 805 - 50 , Business Combinations — Related Issues . Under asset acquisition accounting, where the consideration paid to GCIC’s stockholders exceeded the relative fair values of the assets acquired, the premium paid by GBDC was allocated to the cost of the GCIC assets acquired by GBDC pro - rata based on their relative fair value . Immediately following the acquisition of GCIC, GBDC recorded its assets at their respective fair values and, as a result, the purchase premium allocated to the cost basis of the GCIC assets acquired was immediately recognized as unrealized depreciation on the Company's Consolidated Statement of Operations . The purchase premium allocated to investments in loan securities will amortize over the life of the loans through interest income with a corresponding reversal of the unrealized depreciation on the GCIC loans acquired through their ultimate disposition . The purchase premium allocated to investments in equity securities will not amortize over the life of the equity securities through interest income and, assuming no subsequent change to the fair value of the GCIC equity securities acquired and disposition of such equity securities at fair value, the Company will recognize a realized loss with a corresponding reversal of the unrealized depreciation upon disposition of the GCIC equity securities acquired . As a supplement to U . S . generally accepted accounting principles (“GAAP”) financial measures, the Company has provided the following non - GAAP financial measures : • “Adjusted Net Investment Income” and “Adjusted Net Investment Income Per Share” - excludes the amortization of the purchase premium from net investment income calculated in accordance with GAAP . • “Adjusted Net Realized and Unrealized Gain/(Loss)” and “Adjusted Net Realized and Unrealized Gain/(Loss) Per Share” - excludes the unrealized loss resulting from the purchase premium write - down and the corresponding reversal of the unrealized loss resulting from the amortization of the premium on loans or from the sale of equity investments from the determination of realized and unrealized gain/(loss) in accordance with GAAP . • “Adjusted Net Income” and “Adjusted Earnings/(Loss) Per Share” – calculates net income and earnings per share based on Adjusted Net Investment Income and Adjusted Net Realized and Unrealized Gain/(Loss) . The Company believes that excluding the financial impact of the purchase premium in the above non - GAAP financial measures is useful for investors as this is a non - cash expense/loss and is one method the Company uses to measure its financial condition and results of operations . In addition to the non - GAAP financial measures above, the Company has provided the non - GAAP financial measure “Adjusted Net Investment Income Before Accrual for Capital Gain Incentive Fee” and “Adjusted Net Investment Income Before Accrual for Capital Gain Incentive Fee Per Share” , which excludes the accrual for the capital gain incentive fee required under GAAP (including the portion of such accrual that is not payable under GBDC’s investment advisory agreement) from Adjusted Net Investment Income . The Company believes excluding the accrual of the capital gain incentive fee as a non - GAAP financial measure is useful as a portion of such accrual is not contractually payable under the terms of either the Company’s current investment advisory agreement with GC Advisors, which was effective September 16 , 2019 , or its prior investment advisory agreement with GC Advisors, (each an, “Investment Advisory Agreement”) . In accordance with GAAP, the Company is required to include aggregate unrealized appreciation on investments in the calculation and accrue a capital gain incentive fee on a quarterly basis as if such unrealized capital appreciation were realized, even though such unrealized capital appreciation is not permitted to be considered in calculating the fee actually payable under either Investment Advisory Agreement . As of September 30 , 2023 , there was no cumulative capital gain incentive fee accrued by the Company in accordance with GAAP, and none was payable as a capital gain incentive fee pursuant to the current Investment Advisory Agreement as of September 30 , 2023 . Any payment due under the terms of the current Investment Advisory Agreement is based on the calculation at the end of each calendar year or upon termination of the Investment Advisory Agreement . The Company paid capital gain incentive fees in the amounts of $ 1 . 2 million and $ 1 . 6 million calculated in accordance with its prior Investment Advisory Agreement as of December 31 , 2017 and 2018 , respectively . The Company did not pay any capital gain incentive fee under the Investment Advisory Agreement for any period ended prior to December 31 , 2017 . Although these non - GAAP financial measures are intended to enhance investors’ understanding of the Company’s business and performance, these non - GAAP financial measures should not be considered an alternative to GAAP. Refer to slide ‘Summary of Quarterly Results’ for a reconciliation to the nearest GAAP measures. 2. Purchase premium refers to the premium paid by GBDC to acquire GCIC in excess of the fair value of the assets acquired.

Golub Capital BDC (NASDAQ:GBDC)

Historical Stock Chart

From Oct 2024 to Nov 2024

Golub Capital BDC (NASDAQ:GBDC)

Historical Stock Chart

From Nov 2023 to Nov 2024