UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or Section 15(d) of the

Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): October 15, 2024 (

October 15, 2024)

Mars Acquisition Corp.

(Exact name of registrant as specified in its charter)

| Cayman Islands |

|

001-41619 |

|

N/A |

|

(State or other jurisdiction

of incorporation) |

|

(Commission

File Number) |

|

(I.R.S. Employer

Identification No.) |

|

Americas Tower, 1177 Avenue of The

Americas, Suite 5100

New York, NY |

|

10036 |

| (Address of principal executive offices) |

|

(Zip Code) |

Registrant’s telephone number, including

area code: (888)-667-6277

Not Applicable

(Former name or former address, if changed since

last report)

Check the appropriate box below if the Form 8-K

filing is intended to simultaneously satisfy the filing obligation to the registrant under any of the following provisions:

| x |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ¨ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ¨ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b)

of the Act:

| Title of each class |

|

Trading

Symbol(s) |

|

Name of each exchange on which registered |

| Units, each consisting of one ordinary share, par value $0.000125, and one right entitling the holder to receive 2/10 of an ordinary share |

|

MARXU |

|

The Nasdaq Stock Market LLC |

| Ordinary Shares, $0.000125 par value |

|

MARX |

|

The Nasdaq Stock Market LLC |

| Rights to receive two-tenths (2/10) of one ordinary share |

|

MARXR |

|

The Nasdaq Stock Market LLC |

Indicate by check mark whether the registrant

is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the

Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company x

If an emerging growth company, indicate by check

mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting

standards provided pursuant to Section 13(a) of the Exchange Act. ¨

| Item 7.01. |

Regulation FD Disclosure. |

On September 5, 2023, Mars Acquisition Corp.

(“Mars”), a Cayman Island exempted company, entered into a Business Combination Agreement ( “Business Combination

Agreement”) with ScanTech AI Systems Inc., a Delaware corporation and a wholly owned subsidiary of Mars (“Pubco”),

Mars Merger Sub I Corp., a Cayman Islands exempted company and a wholly owned subsidiary of Mars (“Purchaser Merger Sub”),

Mars Merger Sub II LLC, a Delaware limited liability company and a wholly owned subsidiary of Pubco (“Company Merger Sub”),

ScanTech Identification Beam Systems, LLC, a Delaware limited liability company (“ScanTech”), and Dolan Falconer in

the capacity as the representative from and after the Effective Time for the Company Holder Participants as of immediately prior to the

Effective (the “Seller Representative”). The transactions contemplated by the Business Combination Agreement are hereinafter

referred to collectively as the “Business Combination.”

Filed herewith as Exhibit 99.1 hereto and

incorporated by reference herein is the investor presentation, dated October 2024 (the “Investor Presentation”),

that will be used by ScanTech and Mars with respect to the transactions contemplated by the Business Combination Agreement.

The information in this Item 7.01, including Exhibit 99.1,

is furnished and shall not be deemed “filed” for purposes of Section 18 of the Exchange Act, or otherwise subject to

liabilities under that section, and shall not be deemed to be incorporated by reference into the filings of Mars or Pubco under the Securities

Act or the Exchange Act, regardless of any general incorporation language in such filings. For the avoidance of doubt, Mars intends for

this Form 8-K, including Exhibit 99.1, to satisfy the requirements of Rule 165(a) and Rule 425(a) under

the Securities Act. This Current Report on Form 8-K will not be deemed an admission as to the materiality of any information of the

information in this Item 7.01, including Exhibit 99.1.

Important Additional Information About the Business Combination

and Where to Find It

In

connection with the proposed Business Combination, Pubco has filed a registration statement on Form S-4 with the SEC, which includes

a preliminary prospectus with respect to its securities to be issued in connection with the Business Combination and a preliminary proxy

statement with respect to the extraordinary general meeting at which Mars’ shareholders will be asked to vote on the proposed Business

Combination. Each of Mars, Pubco and ScanTech urge investors, shareholders or members, and other interested persons to read the Form S-4,

including the proxy statement/prospectus, any amendments thereto, and any other documents filed with the SEC, before making any voting

or investment decision because these documents will contain important information about the proposed Business Combination. After the

Form S-4 has been declared effective, Mars will mail the definitive proxy statement/prospectus to shareholders of Mars as of a record

date to be established for voting on the Business Combination. Mars’ shareholders will also be able to obtain a copy of such documents,

without charge, by directing a request to: Mars Acquisition Corp., Americas Tower, 1177 Avenue of The Americas, Suite 5100, New

York, New York, 10036. These documents, once available, can also be obtained, without charge, at the SEC’s website www.sec.gov.

INVESTMENT IN ANY SECURITIES DESCRIBED HEREIN HAS

NOT BEEN APPROVED OR DISAPPROVED BY THE SEC, THE ISRAELI SECURITIES AUTHORITY, OR ANY OTHER REGULATORY AUTHORITY, NOR HAS ANY SECURITIES

AUTHORITY PASSED UPON OR ENDORSED THE MERITS OF THE PROPOSED TRANSACTIONS PURSUANT TO WHICH ANY SECURITIES ARE TO BE OFFERED OR THE ACCURACY

OR ADEQUACY OF THE INFORMATION CONTAINED HEREIN. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

Participants in Solicitation

Mars and ScanTech and their respective directors,

executive officers and other persons may be deemed to be participants in the solicitation of proxies from Mars’ shareholders with

respect to the proposed transaction. Information about the directors and executive officers of Mars is set forth in its final prospectus,

dated as of February 13, 2023, and filed with the SEC on February 14, 2023, and is available free of charge at the SEC’s

website at www.sec.gov or by directing a request to: Mars Acquisition Corp., Americas Tower, 1177 Avenue of The Americas, Suite 5100,

New York, New York 10036. Information regarding the persons who may, under SEC rules, be deemed participants in the solicitation of Mars

shareholders in connection with the proposed transaction will be set forth in Mars’ and Pubco’s filings with the SEC, including

the proxy statement/prospectus and other relevant materials filed with the SEC in connection with the Business Combination when they become

available.

No Offer or Solicitation

This Current Report on Form 8-K is not a proxy

statement or solicitation of a proxy, consent or authorization with respect to any securities or in respect of the potential transaction

and does not constitute an offer to sell or a solicitation of an offer to buy any securities of Mars, ScanTech or Pubco, nor shall there

be any sale of any such securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration

or qualification under the securities laws of such state or jurisdiction. No offer of securities shall be made except by means of a prospectus

meeting the requirements of the Securities Act.

Forward-Looking Statements

Certain statements in this Current Report on Form 8-K

may be considered “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995

and are based on beliefs and assumptions and on information currently available to Mars and ScanTech. In some cases, you can identify

forward-looking statements by the following words: "may," "will," "could," "would," "should,"

"expect," "intend," "plan," "anticipate," "believe," "estimate," "predict,"

"project," "potential," "continue," "ongoing," "target," "seek" or the negative

or plural of these words, or other similar expressions that are predictions or indicate future events or prospects, although not all forward-looking

statements contain these words.

Any statements that refer to expectations, projections

or other characterizations of future events or circumstances, including, without limitation, projections of market opportunity and market

share; ScanTech’s or Pubco’s business plans, including any plans to expand; the sources and uses of cash from the proposed

transaction; the anticipated enterprise value of the combined company following the consummation of the proposed transaction; any benefits

of ScanTech’s partnerships, strategies or plans; anticipated benefits of the proposed transaction; and expectations related to the

terms and timing of the proposed transaction are also forward-looking statements. In addition, in order to be able to execute on its business

plan, ScanTech will be required to repay a significant amount of its current liabilities. These statements involve risks, uncertainties

and other factors that may cause actual results, levels of activity, performance or achievements to be materially different from those

expressed or implied by these forward-looking statements.

These statements are based on a combination of

facts and factors currently known and projections of the future, which are inherently uncertain. Neither Mars nor ScanTech can assure

you that the forward-looking statements in this communication will prove to be accurate. These forward-looking statements are subject

to a number of risks and uncertainties, including, among others: (i) the inability of the parties to complete the business combination

due to, among other things, (a) the failure to obtain required approvals from Mars’ shareholders, ScanTech’s members,

or any third parties whose approval is required; (b) the failure to timely obtain consent or approvals to the business combination

from any governmental agencies or entities whose consent or approval is required (including, without limitation, the Transportation Security

Administration (“TSA”), and any required consents or clearances by The Committee on Foreign Investment in the United States

(“CFIUS”); (c) ScanTech’s inability to complete its pre-closing recapitalization (including the conversion of approximately

$70 million of existing indebtedness into equity of ScanTech of which approximately $60 million is held by insiders, and other third parties,

who have indicated their intention to participate in the conversion); or (d) the inability or failure of Mars or ScanTech to satisfy

any of the other closing conditions in the Business Combination Agreement; (ii) the occurrence of any event that could give rise

to the termination of the Business Combination Agreement; (iii) the inability of the parties to recognize the anticipated benefits

of the Business Combination; (iv) the amount of redemption requests made by Mars’ public shareholders and the risk that all

or substantially all of Mars’ shareholders will elect to redeem their shares in connection with the transaction; (v) costs

and expenses related to the transaction, including the risk that the costs and expenses will exceed current estimates; (vi) the inability

of Pubco to continue as a going concern; (vii) the risk that the transaction disrupts current plans and operations of ScanTech as

a result of the announcement and consummation of the transaction; (viii) potential claims against ScanTech from vendors and other

third parties as a result of prior agreements or other obligations of ScanTech or its affiliates; (ix) the inability of Mars prior

to the transaction, and the Pubco following completion of the transaction, to satisfy and maintain (in the case of the Mars) and to obtain

and maintain (in the case of Pubco) the listing of their respective shares on Nasdaq; (x) the outcome of any existing or potential

litigation, government or regulatory proceedings; (xi) the inability of the parties to obtain a transaction financing; (xii) the

possibility that Mars, ScanTech, or Pubco may be adversely affected by other economic, business and/or competitive factors; (xiii) the

inability of ScanTech to manufacture, or arrange the manufacturing, of products that may be ordered by customers; (xiv) the inability

of ScanTech to retain and increase sales to existing customers, attract new customers and satisfy customers’ requirements; (xv) competition

from larger companies that have greater resources, technology, relationships and/or expertise; (xvi) the future financial performance

of the combined company following the transaction and its ability to achieve profitability in the future; (xvii) the inability of

ScanTech to satisfy past and future payroll and other obligations and liabilities; (xviii) ScanTech’s significant obligations

to the Internal Revenue Service in connection with unpaid federal payroll taxes; (xix) the fact that ScanTech is technically insolvent

and may not have sufficient funds to execute on its business plan or continue its operations, the inability of ScanTech or risk that the

combined company will become solvent and continue operations following completion of the transaction; (xx) the inability of ScanTech

and Pubco to complete successful testing of their products; (xxi) the inability of ScanTech’s products to be approved for placement

on the qualified products list of the CheckPoint Property Screening System (CPSS) program of the TSA (and, if approved, to be granted

funds from the CPSS program), and to obtain or maintain any required third-party certificates; (xxii) the risk that ScanTech’s

patents will expire or not be renewed; (xxiii) the fact that ScanTech’s assets, including its intellectual property, are subject

to security interests of creditors, and the loss of such assets, particularly intellectual property, would preclude ScanTech from conducting

its business; and (xxiii) those other risks and uncertainties set forth in documents of Mars or Pubco filed, or to be filed, with

the SEC.

These statements involve risks, uncertainties and

other factors that may cause actual results, levels of activity, performance or achievements to be materially different from those expressed

or implied by these forward-looking statements. These statements are based on a combination of facts and factors currently known and projections

of the future, which are inherently uncertain. Neither Mars, ScanTech nor Pubco can assure you that the forward-looking statements in

this Current Report on Form 8-K will prove to be accurate.

In light of the significant uncertainties in these

forward-looking statements, you should not regard these statements as a representation or warranty by Mars, ScanTech, or Pubco or their

respective directors, officers or employees or any other person that Mars, ScanTech or Pubco will achieve their objectives and plans in

any specified time frame, or at all. The forward-looking statements in this Current Report on Form 8-K represent the views of Mars

and ScanTech as of the date of this communication. Subsequent events and developments may cause those views to change. Neither Mars, ScanTech

nor Pubco undertakes any obligation to update or revise the forward-looking statements, whether as a result of new information, future

events or otherwise.

Nasdaq has determined to grant Mars an extension

to regain compliance with Listing Rule 5450(a)(2) (the “Rule”) under the following conditions: on or before October 30,

2024, Mars must file a definitive proxy statement for its business combination; on or before November 19, 2024, Mars must have its

business combination approved by its shareholders; and by November 30, 2024, Mars must file with Nasdaq documentation from its transfer

agent, or an independent source, confirming that Mars complies with the minimum total holders requirement under the Rule. If Mars does

not meet these conditions, Nasdaq will provide written notification that its securities will be delisted. At that time, Mars may appeal

the delisting determination to a Listing Qualifications Panel.

| Item 9.01. |

Financial Statements and Exhibits |

SIGNATURE

Pursuant to the requirements

of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto

duly authorized.

| Date: October 15, 2024 |

Mars Acquisition Corp. |

| |

|

| |

By: |

/s/

Karl Brenza |

| |

Name: |

Karl Brenza |

| |

Title: |

Chief Executive Officer |

Exhibit 99.1

| Investor

Presentation

October 2024 |

| About This Presentation :This presentation (“Presentation”) has been prepared in connection making an evaluation with respect to a proposed business combination (the

“Transaction”) between Mars Acquisition Corp. (“Mars”) and ScanTech Identification Beam Systems, LLC (“ScanTech”). This Presentation does not purport to contain all of

the information that may be required to evaluate the Transaction. This Presentation is not intended to form the basis of any investment decision by the recipient and

does not constitute investment, tax or legal advice. No representation or warranty, express or implied, is or will be given by Mars or ScanTech or Pubco or any of their

respective affiliates, directors, officers, employees or advisers or any other person as to the accuracy or completeness of the information in this Presentation or any other

written, oral or other communications transmitted or otherwise made available to any party in the course of its evaluation of the Transaction, and no responsibility or

liability whatsoever is accepted for the accuracy or sufficiency thereof or for any errors, omissions or misstatements, negligent or otherwise, relating thereto. Accordingly,

none of Mars or ScanTech or Pubco or any of their respective affiliates, directors, officers, employees or advisers or any other person shall be liable for any direct,

indirect or consequential loss or damages suffered by any person as a result of relying on any statement in or omission from this Presentation and any such liability is

expressly disclaimed.

Liquidity Disclosure: ScanTech is effectively insolvent and does not currently have sufficient funds to execute on its business plan or continue its operations. At June 30,

2024, ScanTech had approximately $0.7 million in current assets and approximately $77 million in current liabilities. These include significant obligations to the Internal

Revenue Service for unpaid payroll taxes (approximately $4.5 million) as well as to note holders (approximately $80.0 million including long-term notes, including

principal, default penalties and accrued interest), a judgment creditor for approximately $1.5 million and other third parties including trade payables. Although it is

contemplated that certain of ScanTech’s note holders may convert their notes into equity of ScanTech, there can be no assurance that, following the consummation of

the business combination, ScanTech will have sufficient working capital to conduct its operations. Among other things, the Business Combination Agreement does not

contain any minimum cash requirement as a closing condition, and there is no assurance that any funds will be available to ScanTech immediately following the closing.

Accordingly, ScanTech’s obligations to creditors and its other obligations (including, without limitation, the costs associated with ScanTech’s obligations as a public

company, including the costs of preparing required SEC filings, the compensation of its directors and executive management team, and the need to procure directors’

and officers’ liability insurance), may prevent ScanTech from being able to devote any funds to its operations following the business combination. There can therefore be

no assurance that ScanTech will be able to continue as a going concern.

page 2

Forward-Looking Statements: This Presentation contains forward-looking statements within the meaning of section 27A of the U.S. Securities Act of 1933, as amended

(the “Securities Act”), and Section 21E of the U.S. Securities Exchange Act of 1934 (the “Exchange Act”) that are based on beliefs and assumptions and on information

currently available to Mars and ScanTech. In some cases, you can identify forward-looking statements by the following words: “may,” “will,” “could,” “would,” “should,”

“expect,” “intend,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “project,” “potential,” “continue,” “ongoing,” “target,” “seek” or the negative or plural of these

words, or other similar expressions that are predictions or indicate future events or prospects, although not all forward-looking statements contain these words. Any

statements that refer to expectations, projections or other characterizations of future events or circumstances, including, without limitation, projections of market

opportunity and market share; ScanTech’s or Pubco’s business plans, including any plans to expand; the sources and uses of cash from the proposed transaction; the

anticipated enterprise value of the combined company following the consummation of the proposed transaction; any benefits of ScanTech’s partnerships, strategies or

plans; anticipated benefits of the proposed transaction; and expectations related to the terms and timing of the proposed transaction are also forward-looking

statements. In addition, in order to be able to execute on its business plan, ScanTech will be required to repay a significant amount of its current liabilities. These |

| page 3

statements involve risks, uncertainties and other factors that may cause actual results, levels of activity, performance or achievements to be materially different from

those expressed or implied by these forward-looking statements. These statements are based on a combination of facts and factors currently known and projections of

the future, which are inherently uncertain. Neither Mars nor ScanTech can assure you that the forward-looking statements in this communication will prove to be

accurate. These forward-looking statements are subject to a number of risks and uncertainties, including, among others: the inability of the parties to complete the

business combination due to, among other things, (i) the failure to obtain required approvals from Mars’ shareholders, ScanTech’s members, or any third parties whose

approval is required; (ii) the failure to timely obtain consent or approvals to the business combination from any governmental agencies or entities whose consent or

approval is required (including, without limitation, the Transportation Security Administration (“TSA”), and any required consents or clearances by the Committee on

Foreign Investment in the United States; (iii) ScanTech’s inability to complete its pre-closing recapitalization (including the conversion of approximately $70 million of

existing indebtedness into equity of ScanTech of which approximately $60 million is held by insiders, and other third parties, who have indicated their intention to

participate in the conversion); or (iv) the inability or failure of Mars or ScanTech to satisfy any of the other closing conditions in the Business Combination Agreement;

the occurrence of any event that could give rise to the termination of the Business Combination Agreement; the inability of the parties to recognize the anticipated

benefits of the Business Combination; the amount of redemption requests made by Mars’ public shareholders and the risk that all or substantially all of Mars’

shareholders will elect to redeem their shares in connection with the transaction; costs and expenses related to the transaction, including the risk that the costs and

expenses will exceed current estimates; the inability of Pubco to continue as a going concern; the risk that the transaction disrupts current plans and operations of

ScanTech as a result of the announcement and consummation of the transaction; potential claims against ScanTech from vendors and other third parties as a result of

prior agreements or other obligations of ScanTech or its affiliates; the inability of Mars prior to the transaction, and the Pubco following completion of the transaction, to

satisfy and maintain (in the case of the Mars) and to obtain and maintain (in the case of Pubco) the listing of their respective shares on Nasdaq; the outcome of any

existing or potential litigation, government or regulatory proceedings; the inability of the parties to obtain a transaction financing; the possibility that Mars, ScanTech, or

Pubco may be adversely affected by other economic, business and/or competitive factors; the inability of ScanTech to manufacture, or arrange the manufacturing, of

products that may be ordered by customers; the inability of ScanTech to retain and increase sales to existing customers, attract new customers and satisfy customers’

requirements; competition from larger companies that have greater resources, technology, relationships and/or expertise; the future financial performance of the

combined company following the transaction and its ability to achieve profitability in the future; the inability of ScanTech to satisfy past and future payroll and other

obligations and liabilities; ScanTech’s significant obligations to the Internal Revenue Service in connection with unpaid federal payroll taxes; the fact that ScanTech is

technically insolvent and may not have sufficient funds to execute on its business plan or continue its operations, the inability of ScanTech or risk that the combined

company will become solvent and continue operations following completion of the transaction; the inability of ScanTech and Pubco to complete successful testing of

their products; the inability of ScanTech’s products to be approved for placement on the qualified products list of the CheckPoint Property Screening System (“CPSS”)

program of the TSA (and, if approved, to be granted funds from the CPSS program), and to obtain or maintain any required third-party certificates; the risk that

ScanTech’s patents will expire or not be renewed; the fact that ScanTech’s assets, including its intellectual property, are subject to security interests of creditors, and the

loss of such assets, particularly intellectual property, would preclude ScanTech from conducting its business; and other risks and uncertainties set forth in documents of

Mars or Pubco filed, or to be filed, with the SEC.In light of the significant uncertainties in these forward-looking statements, you should not regard these statements as a

representation or warranty by Mars, ScanTech, or Pubco or their respective directors, officers or employees or any other person that Mars, ScanTech or Pubco will

achieve their objectives and plans in any specified time frame, or at all. The forward-looking statements in this Presentation represent the views of Mars and ScanTech as

of the date of this communication. Subsequent events and developments may cause those views to change. Neither Mars, ScanTech nor Pubco undertakes any

obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise. |

| Industry and Market Data: This Presentation contains estimates and other statistical data made by independent parties and by ScanTech relating to market size and

growth and other data about ScanTech’s industry. This data involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such

estimates. In addition, projections, assumptions, and estimates of the future performance of the markets in which ScanTech operates are necessarily subject to a high

degree of uncertainty and risk.

Trademarks and Trade Names: This Presentation contains trademarks, service marks, trade names and copyrights of other companies, which are the property of their

respective owners. The use thereof in this Presentation does not imply an affiliation with, or endorsement by, the owners of such trademarks, service marks, trade names

and copyrights. Solely for convenience, some of the trademarks, service marks, trade names and copyrights referred to in this Presentation may be listed without the TM,

SM or symbols, but such references are not intended to indicate, in any way, that Mars or ScanTech will not assert, to the fullest extent under applicable law, their rights

or the right of the applicable licensor to these trademarks, service marks, trade names and copyrights.

No Offer or Solicitation: This Presentation is not a proxy statement or solicitation of a proxy, consent or authorization with respect to any securities or in respect of the

potential transaction and does not constitute an offer to sell or a solicitation of an offer to buy any securities of Mars, ScanTech or Pubco, nor shall there be any sale of

any such securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of

such state or jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of the Securities Act.

Additional Information: In connection with the proposed Business Combination, which will include a preliminary prospectus with respect to its securities to be issued in

connection with the Business Combination and a preliminary proxy statement with respect to the extraordinary general meeting at which Mars’ shareholders will be

asked to vote on the proposed Business Combination. Each of Mars, Pubco and ScanTech urge investors, shareholders or members, and other interested persons to

read, the Form S-4, including the proxy statement/prospectus, any amendments thereto, and any other documents filed with the SEC, before making any voting or

investment decision because these documents will contain important information about the proposed Business Combination. After the Form S-4 has been filed and

declared effective, Mars will mail the definitive proxy statement/prospectus to shareholders of Mars as of a record date to be established for voting on the Business

Combination. Mars’ shareholders will also be able to obtain a copy of such documents, without charge, by directing a request to: Mars Acquisition Corp., Americas

Tower, 1177 Avenue of The Americas, Suite 5100, New York, New York, 10036. These documents, once available, can also be obtained, without charge, at the SEC’s

website www.sec.gov.

Participants in the Solicitation: Mars and ScanTech and their respective directors, executive officers and other persons may be deemed to be participants in the

solicitation of proxies from Mars’ shareholders with respect to the proposed transaction. Information about the directors and executive officers of Mars is set forth in its

final prospectus, dated as of February 13, 2023, and filed with the SEC on February 14, 2023 , and is available free of charge at the SEC’s website at www.sec.gov or by

directing a request to: Mars Acquisition Corp., Americas Tower, 1177 Avenue of The Americas, Suite 5100, New York, New York 10036. Information regarding the persons

who may, under SEC rules, be deemed participants in the solicitation of Mars shareholders in connection with the proposed transaction will be set forth in Mars’ and

Pubco’s filings with the SEC, including the proxy statement/prospectus and other relevant materials filed with the SEC in connection with the Business Combination when

they become available.

page 4 |

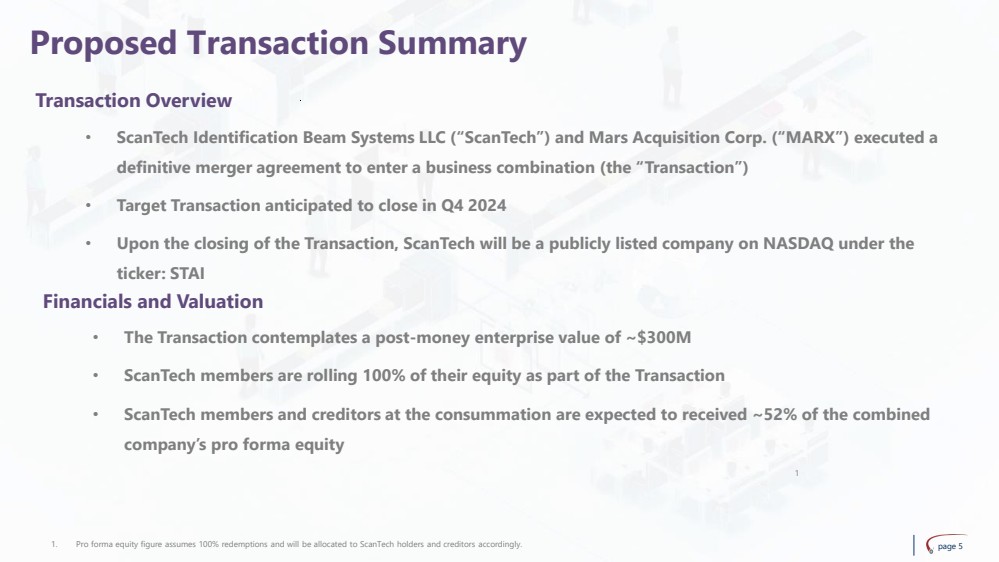

| Proposed Transaction Summary

page 5

Transaction Overview

• ScanTech Identification Beam Systems LLC (“ScanTech”) and Mars Acquisition Corp. (“MARX”) executed a

definitive merger agreement to enter a business combination (the “Transaction”)

• Target Transaction anticipated to close in Q4 2024

• Upon the closing of the Transaction, ScanTech will be a publicly listed company on NASDAQ under the

ticker: STAI

1. Pro forma equity figure assumes 100% redemptions and will be allocated to ScanTech holders and creditors accordingly.

Financials and Valuation

• The Transaction contemplates a post-money enterprise value of ~$300M

• ScanTech members are rolling 100% of their equity as part of the Transaction

• ScanTech members and creditors at the consummation are expected to received ~52% of the combined

company’s pro forma equity

1 |

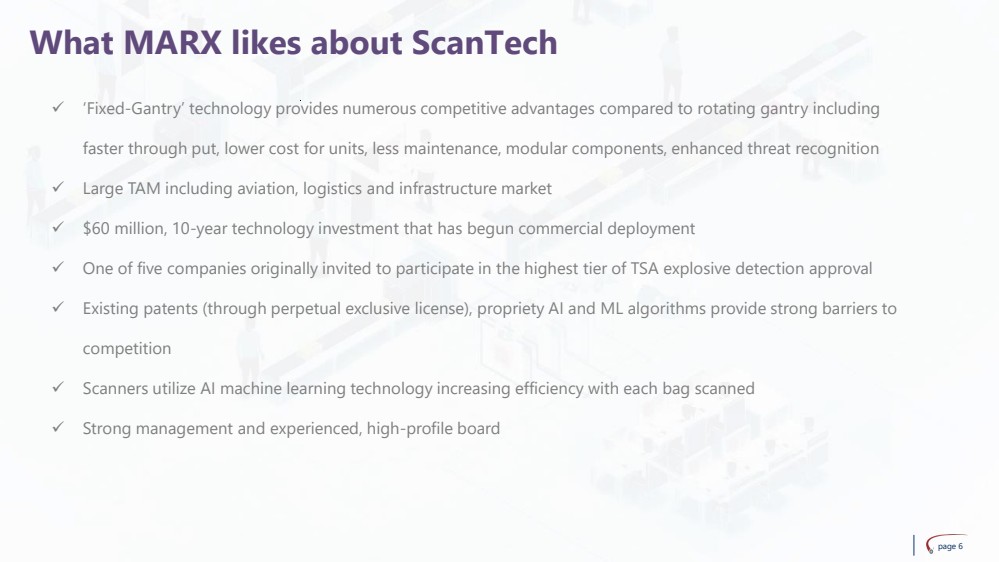

| page 6

What MARX likes about ScanTech

✓ ‘Fixed-Gantry’ technology provides numerous competitive advantages compared to rotating gantry including

faster through put, lower cost for units, less maintenance, modular components, enhanced threat recognition

✓ Large TAM including aviation, logistics and infrastructure market

✓ $60 million, 10-year technology investment that has begun commercial deployment

✓ One of five companies originally invited to participate in the highest tier of TSA explosive detection approval

✓ Existing patents (through perpetual exclusive license), propriety AI and ML algorithms provide strong barriers to

competition

✓ Scanners utilize AI machine learning technology increasing efficiency with each bag scanned

✓ Strong management and experienced, high-profile board |

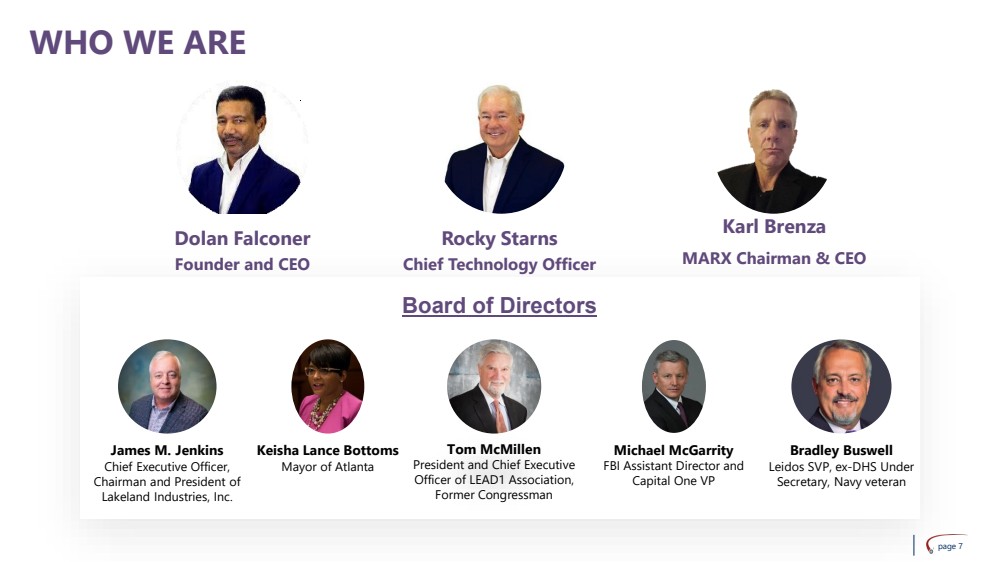

| page 7

WHO WE ARE

Dolan Falconer

Founder and CEO

Karl Brenza

MARX Chairman & CEO

Board of Directors

James M. Jenkins

Chief Executive Officer,

Chairman and President of

Lakeland Industries, Inc.

Keisha Lance Bottoms

Mayor of Atlanta

Bradley Buswell

Leidos SVP, ex-DHS Under

Secretary, Navy veteran

Michael McGarrity

FBI Assistant Director and

Capital One VP

Rocky Starns

Chief Technology Officer

Tom McMillen

President and Chief Executive

Officer of LEAD1 Association,

Former Congressman |

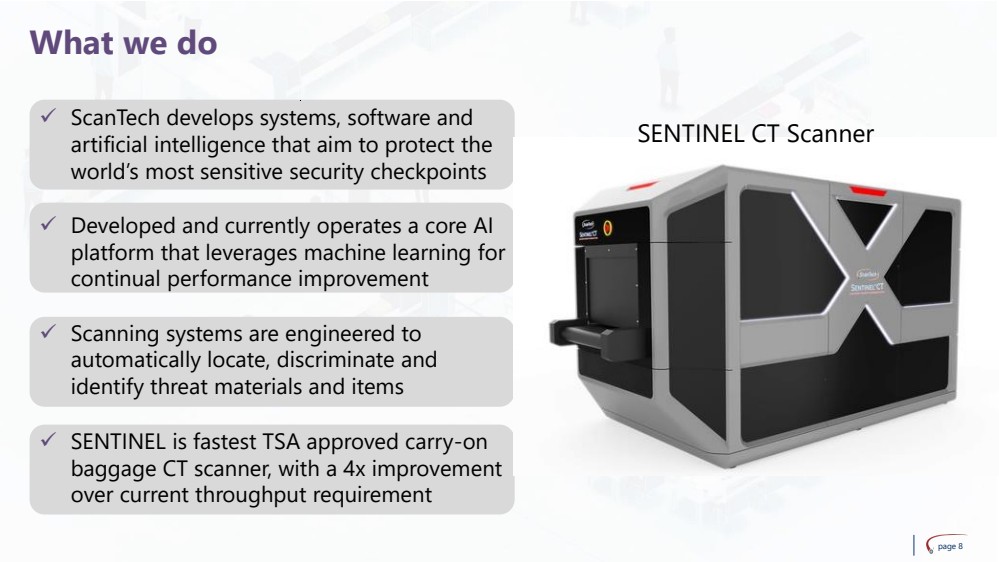

| ✓ ScanTech develops systems, software and

artificial intelligence that aim to protect the

world’s most sensitive security checkpoints

✓ Developed and currently operates a core AI

platform that leverages machine learning for

continual performance improvement

✓ Scanning systems are engineered to

automatically locate, discriminate and

identify threat materials and items

✓ SENTINEL is fastest TSA approved carry-on

baggage CT scanner, with a 4x improvement

over current throughput requirement

page 8

What we do

SENTINEL CT Scanner |

| page 9

Investment Highlights

Cutting-Edge Technology

Total Addressable

Market

High throughput and multiple plane design

allow for faster and safer screening

Rapidly growing market fueled by increasing

levels of Global threats

Differentiated algorithmic artificial intelligence combined

with ‘Fixed-Gantry’ CT will lead to significant

improvements in cost and operations

New private sector demand combined with

commercial infrastructure upgrades create multiple

avenues for growth

Leadership team brings together seasoned

professionals with extensive experience in security,

technology development and business management

Strong Competitive

Advantages

Multiple Strategies to

Fuel Growth

Experienced

Management Team |

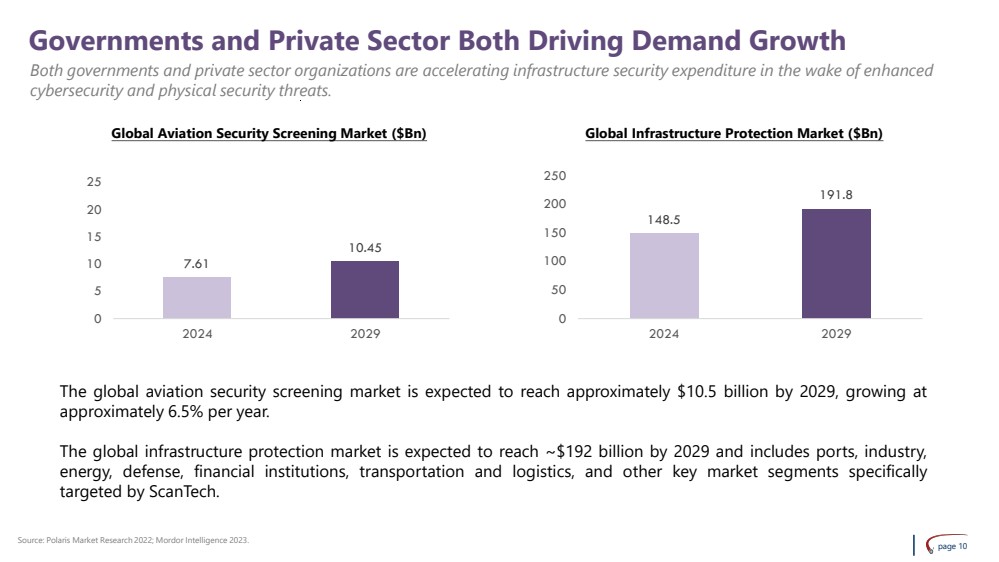

| Governments and Private Sector Both Driving Demand Growth

Source: Polaris Market Research 2022; Mordor Intelligence 2023.

Both governments and private sector organizations are accelerating infrastructure security expenditure in the wake of enhanced

cybersecurity and physical security threats.

Global Aviation Security Screening Market ($Bn) Global Infrastructure Protection Market ($Bn)

page 10

The global aviation security screening market is expected to reach approximately $10.5 billion by 2029, growing at

approximately 6.5% per year.

The global infrastructure protection market is expected to reach ~$192 billion by 2029 and includes ports, industry,

energy, defense, financial institutions, transportation and logistics, and other key market segments specifically

targeted by ScanTech.

148.5

191.8

0

50

100

150

200

250

2024 2029

7.61

10.45

0

5

10

15

20

25

2024 2029 |

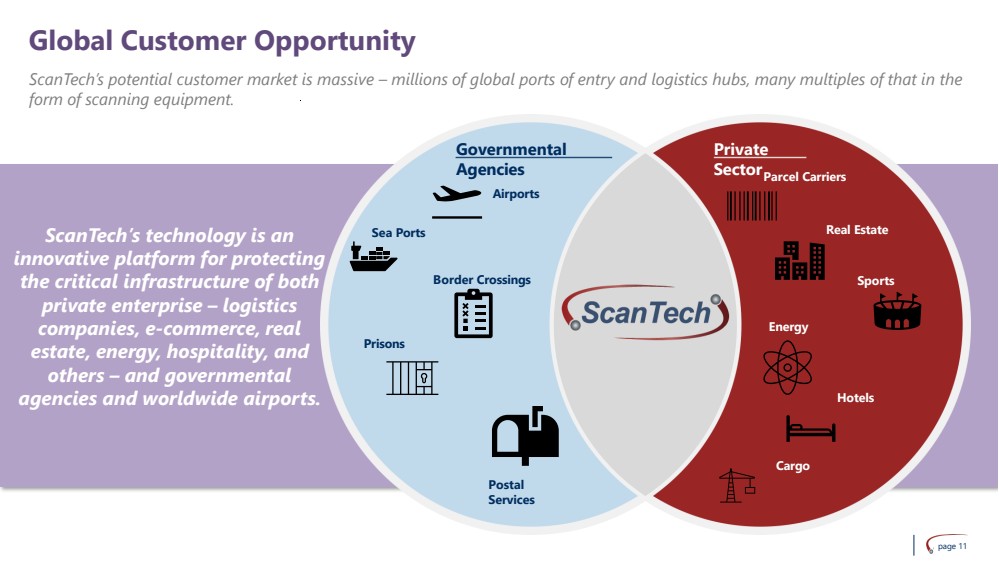

| ScanTech’s potential customer market is massive – millions of global ports of entry and logistics hubs, many multiples of that in the

form of scanning equipment.

Governmental

Agencies

Private

Sector

ScanTech’s technology is an

innovative platform for protecting

the critical infrastructure of both

private enterprise – logistics

companies, e-commerce, real

estate, energy, hospitality, and

others – and governmental

agencies and worldwide airports.

Airports

Sea Ports

Border Crossings

Prisons

Postal

Services

Parcel Carriers

Real Estate

Sports

Hotels

Cargo

page 11

Energy

Global Customer Opportunity |

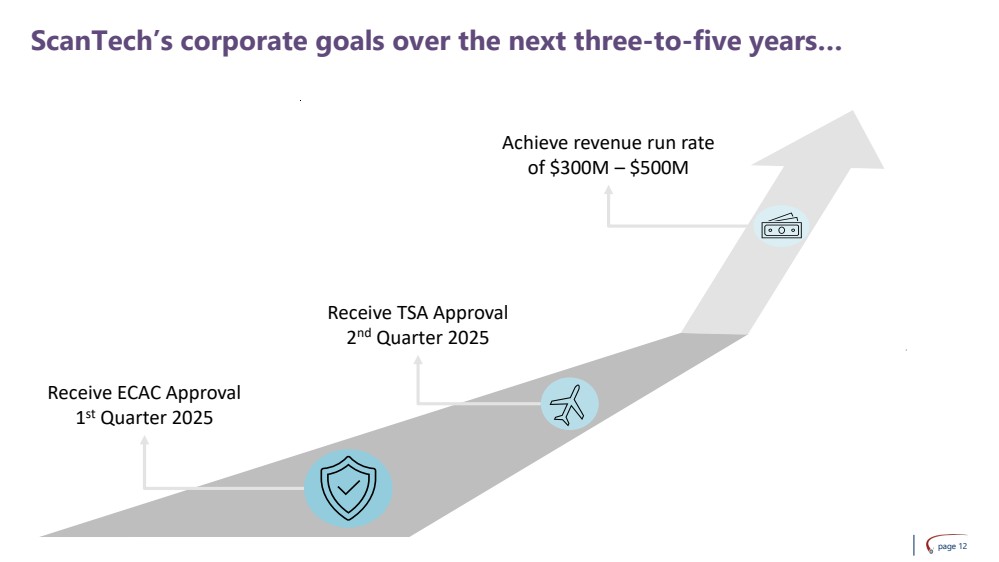

| page 12

ScanTech’s corporate goals over the next three-to-five years…

Receive ECAC Approval

1

st Quarter 2025

Receive TSA Approval

2

nd Quarter 2025

Achieve revenue run rate

of $300M – $500M |

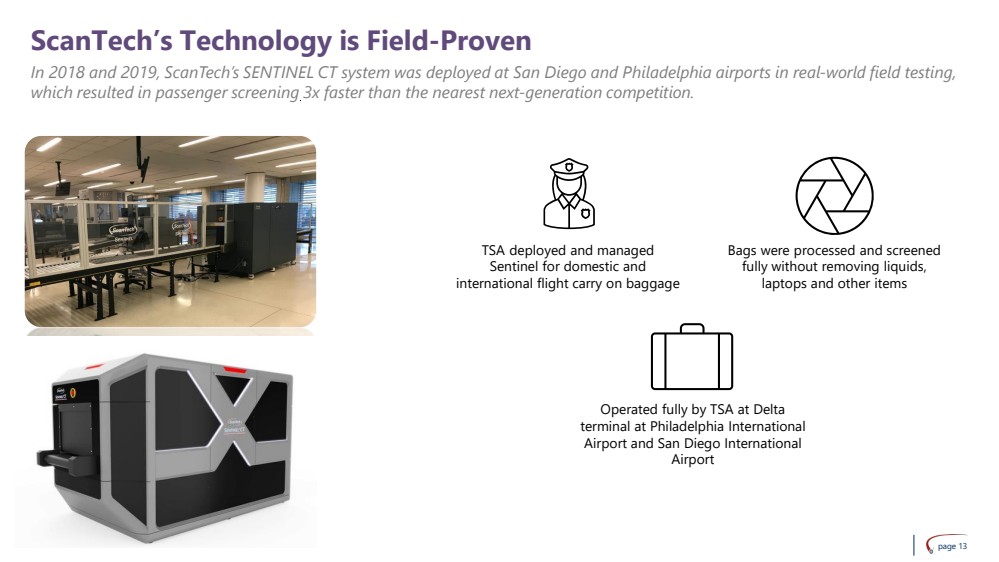

| ScanTech’s Technology is Field-Proven

In 2018 and 2019, ScanTech’s SENTINEL CT system was deployed at San Diego and Philadelphia airports in real-world field testing,

which resulted in passenger screening 3x faster than the nearest next-generation competition.

TSA deployed and managed

Sentinel for domestic and

international flight carry on baggage

Bags were processed and screened

fully without removing liquids,

laptops and other items

Operated fully by TSA at Delta

terminal at Philadelphia International

Airport and San Diego International

Airport

page 13 |

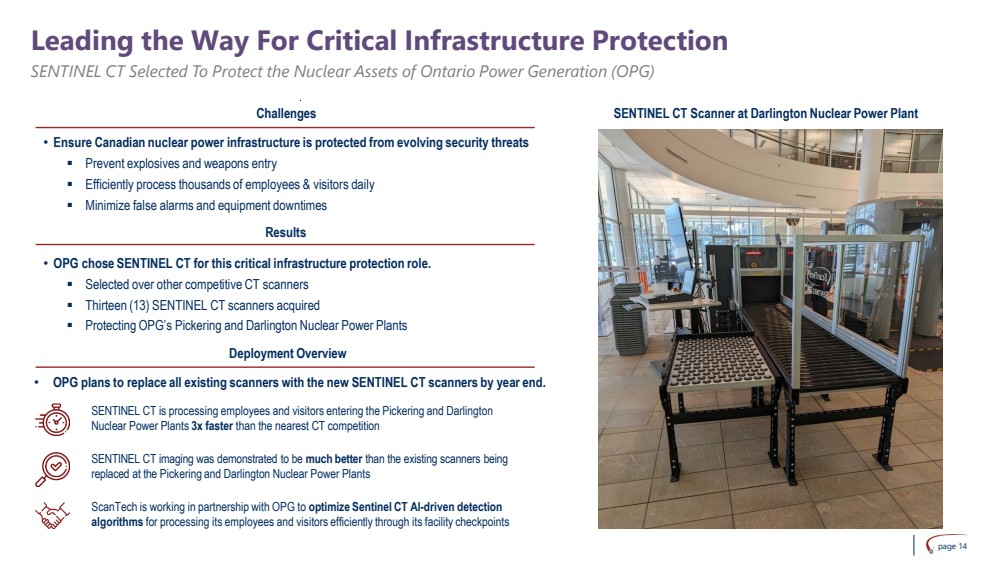

| Deployment Overview

SENTINEL CT is processing employees and visitors entering the Pickering and Darlington

Nuclear Power Plants 3x faster than the nearest CT competition

SENTINEL CT imaging was demonstrated to be much better than the existing scanners being

replaced at the Pickering and Darlington Nuclear Power Plants

ScanTech is working in partnership with OPG to optimize Sentinel CT AI-driven detection

algorithms for processing its employees and visitors efficiently through its facility checkpoints

SENTINEL CT Selected To Protect the Nuclear Assets of Ontario Power

Genera

• Ensure Canadian nuclear power infrastructure is protected from evolving security threats

▪ Prevent explosives and weapons entry

▪ Efficiently process thousands of employees & visitors daily

▪ Minimize false alarms and equipment downtimes

• OPG chose SENTINEL CT for this critical infrastructure protection role.

▪ Selected over other competitive CT scanners

▪ Thirteen (13) SENTINEL CT scanners acquired

▪ Protecting OPG’s Pickering and Darlington Nuclear Power Plants

CONFIDENTIAL

page 14

page 14

Leading the Way For Critical Infrastructure Protection

SENTINEL CT Selected To Protect the Nuclear Assets of Ontario Power Generation (OPG)

SENTINEL CT Scanner at Darlington Nuclear Power Plant

Results

Challenges

• OPG plans to replace all existing scanners with the new SENTINEL CT scanners by year end. |

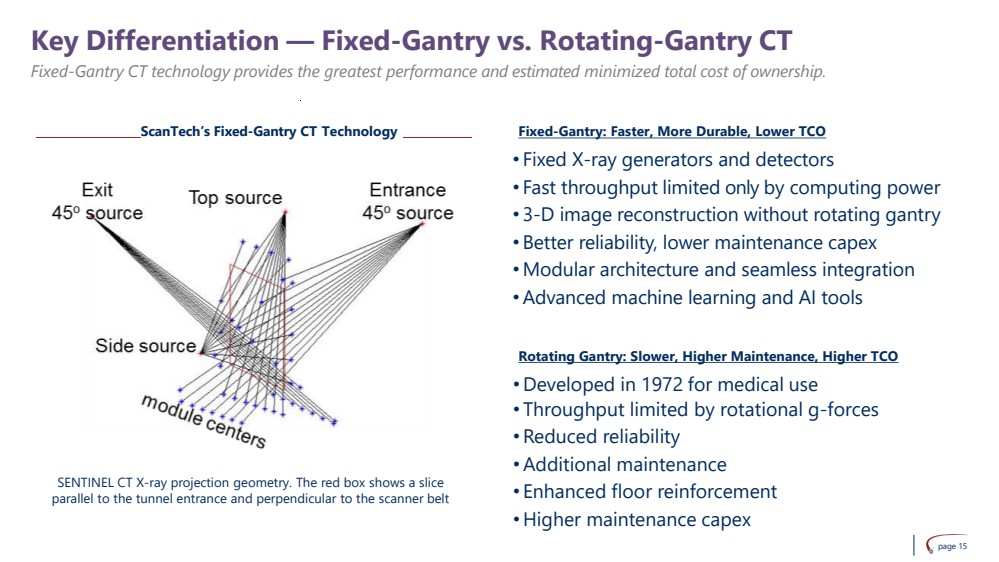

| Key Differentiation — Fixed-Gantry vs. Rotating-Gantry CT

ScanTech’s Fixed-Gantry CT Technology

page 15

• Fixed X-ray generators and detectors

• Fast throughput limited only by computing power

• 3-D image reconstruction without rotating gantry

• Better reliability, lower maintenance capex

• Modular architecture and seamless integration

• Advanced machine learning and AI tools

Fixed-Gantry: Faster, More Durable, Lower TCO

Rotating Gantry: Slower, Higher Maintenance, Higher TCO

• Developed in 1972 for medical use

• Throughput limited by rotational g-forces

• Reduced reliability

• Additional maintenance

• Enhanced floor reinforcement

• Higher maintenance capex

SENTINEL CT X-ray projection geometry. The red box shows a slice

parallel to the tunnel entrance and perpendicular to the scanner belt

Fixed-Gantry CT technology provides the greatest performance and estimated minimized total cost of ownership. |

| FIXED-GANTRY

DESIGN

MULTIPLE

PLANES

• Belt speed is not limited by rotating-gantry speed and Fixed-Gantry CT processes 400-800 bins per hour compared to competition’s limited

170 bins per hour1

HIGH

THROUGHPUT

• Compatible with most airport and commercial facilities because Fixed-Gantry CT utilizes standard 120-240VAC single

phase electrical service and doe not require infrastructure upgrades prior to installation

• Out-of-box, plug-and-play capability allows for same-day installation

UNIVERSAL

COMPATIBILITY

MODULAR

DESIGN

The Company has invested more than $60 million into the development of its proprietary technology which the Company believes

has distinct competitive advantages.

Significant Competitive Advantages

page 16

REDUCED

MAINTENANCE

EASE OF

INSTALLATION

• Modular scalable design enables seamless replacement of core components, facilitating efficient maintenance and system upgrades

to incorporate component advances and higher X-ray energy / flux ratings

• Fixed-Gantry CT design eliminates the traditional wear and tear associated with rotating-gantry scanners, reducing

operating & maintenance costs resulting in minimal downtime

• ‘Fixed-Gantry’ design has substantially lower component costs versus rotating-gantry scanners

• Four (4) integrated and interlaced projections provide four independent views of target contents and three (3) inspection axes for superior X-ray

interrogation and material discrimination vs conventional single-slice CT systems

1. OIG Report 21-69

September 23, 2021 |

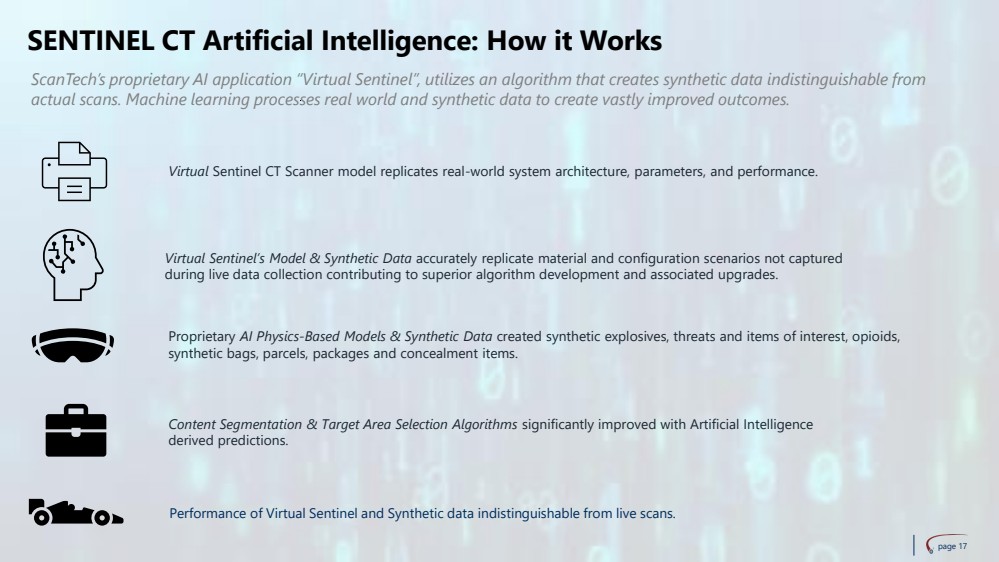

| SENTINEL CT Artificial Intelligence: How it Works

page 17

Performance of Virtual Sentinel and Synthetic data indistinguishable from live scans.

Virtual Sentinel CT Scanner model replicates real-world system architecture, parameters, and performance.

Virtual Sentinel’s Model & Synthetic Data accurately replicate material and configuration scenarios not captured

during live data collection contributing to superior algorithm development and associated upgrades.

Content Segmentation & Target Area Selection Algorithms significantly improved with Artificial Intelligence

derived predictions.

Proprietary AI Physics-Based Models & Synthetic Data created synthetic explosives, threats and items of interest, opioids,

synthetic bags, parcels, packages and concealment items.

ScanTech’s proprietary AI application “Virtual Sentinel”, utilizes an algorithm that creates synthetic data indistinguishable from

actual scans. Machine learning processes real world and synthetic data to create vastly improved outcomes. |

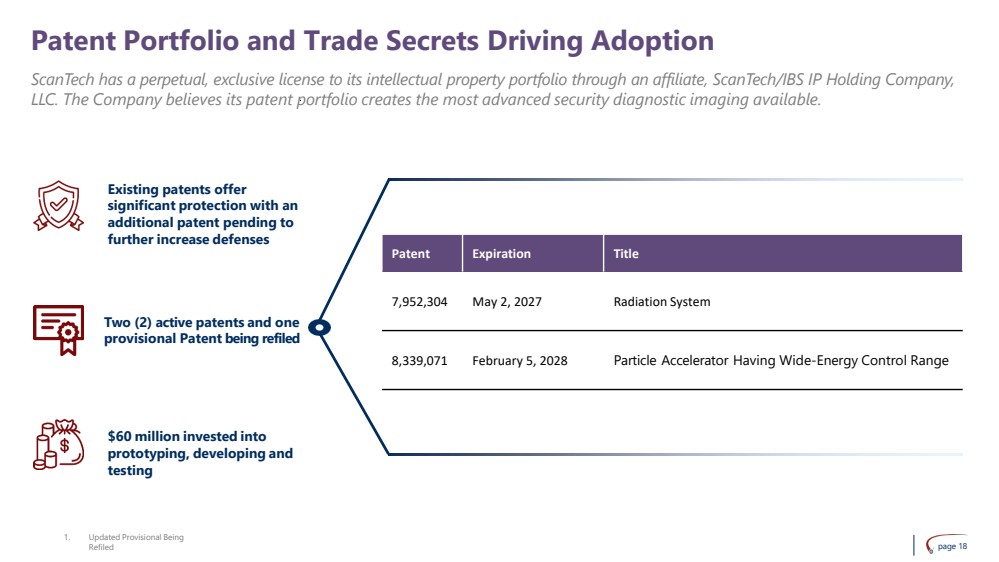

| Existing patents offer

significant protection with an

additional patent pending to

further increase defenses

Two (2) active patents and one

provisional Patent being refiled

$60 million invested into

prototyping, developing and

testing

Patent Portfolio and Trade Secrets Driving Adoption

1. Updated Provisional Being

Refiled

Patent Expiration Title

7,952,304 May 2, 2027 Radiation System

8,339,071 February 5, 2028 Particle Accelerator Having Wide-Energy Control Range

page 18

ScanTech has a perpetual, exclusive license to its intellectual property portfolio through an affiliate, ScanTech/IBS IP Holding Company,

LLC. The Company believes its patent portfolio creates the most advanced security diagnostic imaging available. |

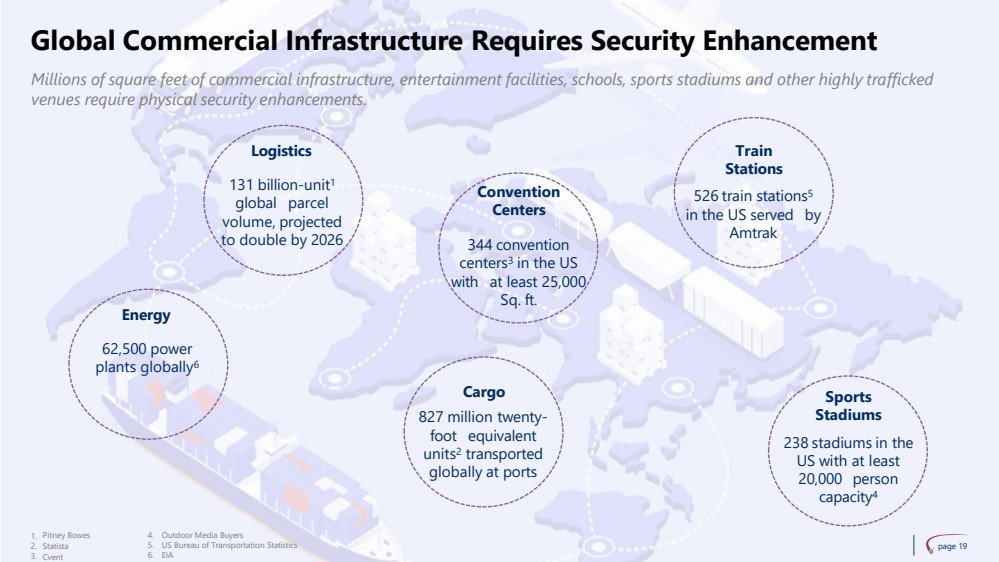

| Global Commercial Infrastructure Requires Security Enhancement

238 stadiums in the

US with at least

20,000 person

capacity4

Convention

Centers

344 convention

centers3

in the US

with at least 25,000

Sq. ft.

Train

Stations

526 train stations5

in the US served by

Amtrak

Cargo

827 million twenty-foot equivalent

units2

transported

globally at ports

Logistics

131 billion-unit1

global parcel

volume, projected

to double by 2026

Sports

Stadiums

page 19

Energy

62,500 power

plants globally6

1.

2.

3.

Pitney Bowes

Statista

Cvent

Outdoor Media Buyers

US Bureau of Transportation Statistics

EIA

4.

5.

6.

Millions of square feet of commercial infrastructure, entertainment facilities, schools, sports stadiums and other highly trafficked

venues require physical security enhancements. |

| Airport Security Market Growth Catalyst’s

• Growing passenger numbers and terrorism concerns drive

increased security investments

• Adoption of AI, robotics, and biometrics enhances security

efficiency amid regulatory demands

• According to Mordor the Airport Security Market size is

expected to grow at a CAGR of 9.5% during the forecast

period on the right

Global Aviation Security Market

page 20

$13.34

$20.99

2023 2024 2025 2026 2027 2028

Airport Security Market Size ($BN)

Source: Mordor Intelligence 2023.

The aviation security market is poised for substantial growth, driven by increasing investments in advanced checkpoint screening

systems and other security technologies |

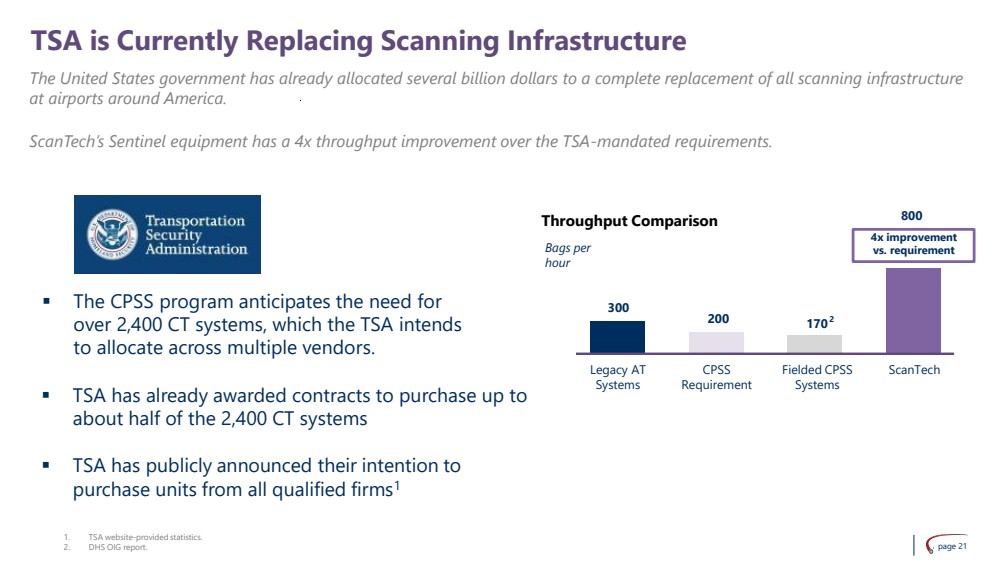

| ▪ The CPSS program anticipates the need for

over 2,400 CT systems, which the TSA intends

to allocate across multiple vendors.

▪ TSA has publicly announced their intention to

purchase units from all qualified firms1

TSA is Currently Replacing Scanning Infrastructure

1.

2.

TSA website-provided statistics.

DHS OIG report.

200

800

Bags per

hour

170

2

4x improvement

vs. requirement

300

page 21

Throughput Comparison

Legacy AT

Systems

CPSS

Requirement

Fielded CPSS

Systems

ScanTech

▪ TSA has already awarded contracts to purchase up to

about half of the 2,400 CT systems

The United States government has already allocated several billion dollars to a complete replacement of all scanning infrastructure

at airports around America.

ScanTech’s Sentinel equipment has a 4x throughput improvement over the TSA-mandated requirements. |

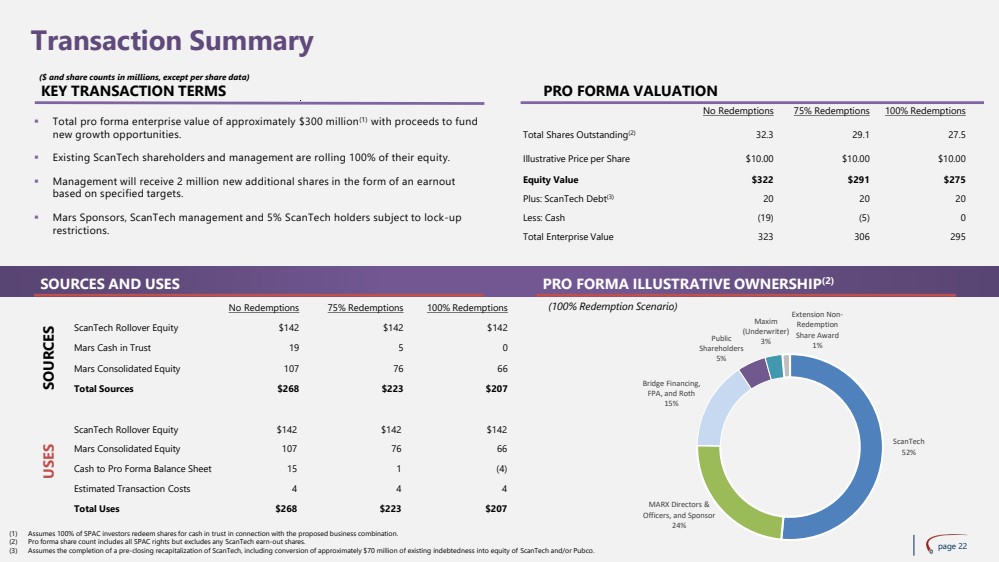

| PRO FORMA VALUATION

No Redemptions 75% Redemptions 100% Redemptions

Total Shares Outstanding(2) 32.3 29.1 27.5

Illustrative Price per Share $10.00 $10.00 $10.00

Equity Value $322 $291 $275

Plus: ScanTech Debt(3) 20 20 20

Less: Cash (19) (5) 0

Total Enterprise Value 323 306 295

($ and share counts in millions, except per share data)

(1) Assumes 100% of SPAC investors redeem shares for cash in trust in connection with the proposed business combination.

(2) Pro forma share count includes all SPAC rights but excludes any ScanTech earn-out shares.

(3) Assumes the completion of a pre-closing recapitalization of ScanTech, including conversion of approximately $70 million of existing indebtedness into equity of ScanTech and/or Pubco.

No Redemptions 75% Redemptions 100% Redemptions

ScanTech Rollover Equity $142 $142 $142

Mars Cash in Trust 19 5 0

Mars Consolidated Equity 107 76 66

SOURCES

Total Sources $268 $223 $207

ScanTech Rollover Equity $142 $142 $142

Mars Consolidated Equity 107 76 66

Cash to Pro Forma Balance Sheet 15 1 (4)

Estimated Transaction Costs 4 4 4

Total Uses $268 $223 $207

USES

SOURCES AND USES

KEY TRANSACTION TERMS

▪ Total pro forma enterprise value of approximately $300 million(1) with proceeds to fund

new growth opportunities.

▪ Existing ScanTech shareholders and management are rolling 100% of their equity.

▪ Management will receive 2 million new additional shares in the form of an earnout

based on specified targets.

▪ Mars Sponsors, ScanTech management and 5% ScanTech holders subject to lock-up

restrictions.

PRO FORMA ILLUSTRATIVE OWNERSHIP(2)

(100% Redemption Scenario)

Transaction Summary

page 22

ScanTech

52%

MARX Directors &

Officers, and Sponsor

24%

Bridge Financing,

FPA, and Roth

15%

Public

Shareholders

5%

Maxim

(Underwriter)

3%

Extension Non-Redemption

Share Award

1% |

| $ 16,294

$ 1,848 $ 1,411

$ 102

5.8x

3.9x

2.4x

1.7x

page 23

Benchmarking – Comparable Public Companies

2024 EV/Revenue

2024 Revenue

Source: CapIQ as of 10/7/2024.

($ in USD millions) |

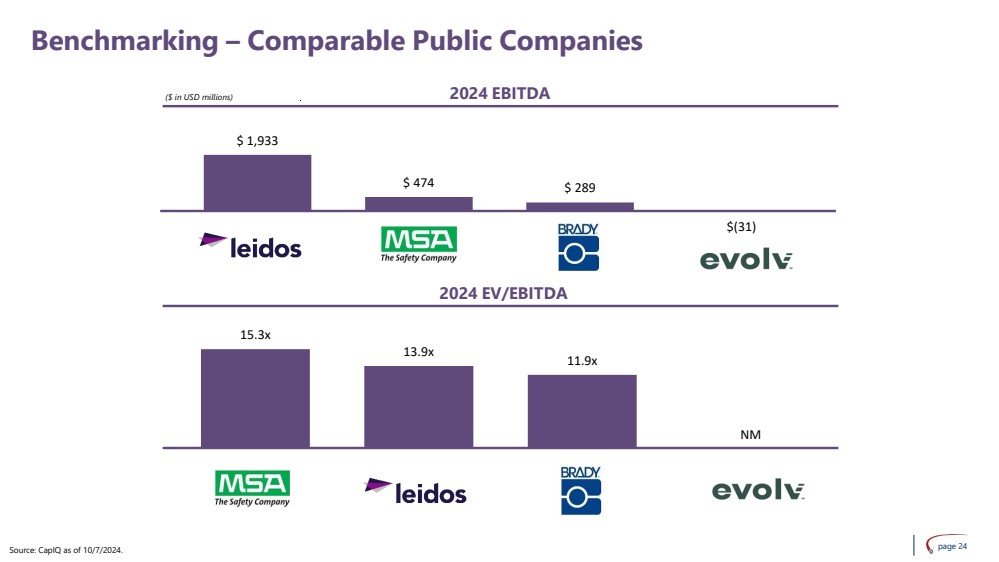

| 15.3x

13.9x 11.9x

NM

$ 1,933

$ 474 $ 289

$(31)

page 24

Benchmarking – Comparable Public Companies

2024 EV/EBITDA

2024 EBITDA

Source: CapIQ as of 10/7/2024.

($ in USD millions) |

Mars Acquisition (NASDAQ:MARXU)

Historical Stock Chart

From Nov 2024 to Dec 2024

Mars Acquisition (NASDAQ:MARXU)

Historical Stock Chart

From Dec 2023 to Dec 2024