UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16 UNDER

THE SECURITIES EXCHANGE ACT OF 1934

For the month of October 2023

GRUPO AEROPORTUARIO DEL CENTRO NORTE, S.A.B.

DE C.V.

(CENTRAL NORTH AIRPORT GROUP)

(Translation of Registrant’s Name Into

English)

México

(Jurisdiction of incorporation or organization)

Torre Latitud, L501, Piso 5

Av. Lázaro Cárdenas 2225

Col. Valle Oriente, San Pedro Garza García

Nuevo León, México

(Address of principal executive offices)

(Indicate by check mark whether the registrant

files or will file annual reports under cover of Form 20-F or Form 40-F.)

(Indicate by check mark whether the registrant

by furnishing the information contained in this form is also thereby furnishing the information to the Commission pursuant to Rule

12g3-2(b) under the Securities Exchange Act of 1934.)

(If “Yes” is marked, indicate below

the file number assigned to the registrant in connection with Rule 12g3-2(b): 82- .)

|

OMA Announces Updates on the

Tariff Regulation Bases

|

Mexico City, Mexico, October 19, 2023—Mexican airport

operator Grupo Aeroportuario del Centro Norte, S.A.B. de C.V., known as OMA (NASDAQ: OMAB; BMV: OMA), informs that on October 19, 2023,

we received new tariff regulation bases from the Federal Civil Aviation Agency (Agencia Federal de Aviación Civil, “AFAC”),

a deconcentrated entity of the Ministry of Infrastructure, Communications and Transportation (“SICT”), which replace the bases

received on October 4, 2023.

The tariff regulation bases refer to those set forth in Annex

7 of the concession titles issued by the SICT on June 29, 1998, as amended, applicable to OMA’s 13 airport concessions.

According to the notification from AFAC, the new tariff regulation

bases will come into effect the day after their reception. The full text of the amended document received on October 19, 2023 can be

found on the following website: http://avisos.oma.aero/11.%20Comunicados2023/Otros/OMA_Anexo7_2023_ENG_vf.pdf.

Additionally, in compliance with the Mexican Stock Exchange (“BMV”)

requirement, pursuant to Article 106 of the Mexican Securities Market Law, Article 50 of the of the General Provisions Applicable to Securities

Issuers and Other Market Participants, and sections 4.046.00 and 4.047.00 of BMV’s Internal Regulation, OMA informs that with the

latest information that we own, we are not aware of any activity by members of our Board of Directors or any of our relevant executive

officers that may have been related to the unusual trading volumes today; additionally, the repurchase program did not operate during

this period.

This report may contain forward-looking information and statements.

Forward-looking statements are statements that are not historical facts. These statements are only predictions based on our current information

and expectations and projections about future events. Forward-looking statements may be identified by the words “believe,”

“expect,” “anticipate,” “target,” “estimate,” or similar expressions. While OMA's management

believes that the expectations reflected in such forward-looking statements are reasonable, investors are cautioned that forward-looking

information and statements are subject to various risks and uncertainties, many of which are difficult to predict and are generally beyond

the control of OMA, that could cause actual results and developments to differ materially from those expressed in, or implied or projected

by, the forward-looking information and statements. These risks and uncertainties include, but are not limited to, those discussed in

our most recent annual report filed on Form 20-F under the caption “Risk Factors.” OMA undertakes no obligation to update

publicly its forward-looking statements, whether as a result of new information, future events, or otherwise.

About OMA

Grupo Aeroportuario del Centro Norte, S.A.B. de C.V., known

as OMA, operates 13 international airports in nine states of central and northern Mexico. OMA’s airports serve Monterrey, Mexico’s

third largest metropolitan area, the tourist destinations of Acapulco, Mazatlán, and Zihuatanejo, and nine other regional centers

and border cities. OMA also operates the NH Collection Hotel inside Terminal 2 of the Mexico City airport and the Hilton Garden Inn at

the Monterrey airport. OMA employs over 1,200 persons in order to offer passengers and clients airport and commercial services in facilities.

OMA is listed on the Mexican Stock Exchange (OMA) and on the NASDAQ Global Select Market (OMAB). For more information, visit:

• Webpage http://ir.oma.aero

• Twitter http://twitter.com/OMAeropuertos

• Facebook https://www.facebook.com/OMAeropuertos

2

Pursuant to the requirements of the Securities

Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly

authorized.

| |

Grupo Aeroportuario del Centro Norte, S.A.B. de C.V. |

| |

|

| By: |

/s/ Ruffo Pérez Pliego |

|

| |

Ruffo Pérez Pliego |

| |

Chief Financial Officer |

Dated October 19, 2023

GRUPO AEROPORTUARIO DEL CENTRO NORTE, S.A.B. DE C.V. 6-K

EXHIBIT 99.1

Letterhead: Ministry of Infrastructure, Communications and Transport

Letterhead: Federal Civil Aviation Agency

[NOTE:

PLEASE NOTE THAT THE ENGLISH VERSION OF THE NOTICE IS A TRANSLATION FROM THE ORIGINAL DOCUMENT IN SPANISH. IN THE EVENT OF ANY DISCREPANCY

BETWEEN THE TRANSLATION AND THE ORIGINAL SPANISH LANGUAGE VERSIONS, THE LATTER SHALL PREVAIL.]

RULES

FOR TARIFF REGULATION

| 1.1. | These

rules governing Tariff Regulation and the appendices hereto (hereafter, “Rules”)

are applicable to the airport concessions in which the Federal Economic Competition Commission

(hereafter, “COFECE”) has opined that reasonable conditions do not exist to guarantee

competition in the rendering of Regulated Services. |

| 1.2. | The

concessions referred to in the immediately preceding paragraph shall be subject to these

Rules for as long as, in the opinion of the COFECE, there are no reasonable competitive conditions

to render airport services, nor in connection with leases and fees under the contracts that

the concession holders enter into with complementary service providers, in accordance with

the provisions of article 70 of the Airport Law. |

| 1.3. | The

Federal Civil Aviation Agency (hereafter, “AFAC”), an autonomous administrative

body within the Department of Infrastructure, Communications and Transport, shall be the

government agency in charge of the application of, interpretation of, and verification of

compliance with these Rules. |

| 1.4. | The

Rules establish a maximum revenue per traffic unit (hereafter, “Joint Maximum Tariff”),

which the concession holder may charge in exchange for the services specified in point 2

of these Rules (hereafter, “Regulated Services”). |

| 1.5. | During

one calendar year, total revenues accrued from the provision of Regulated Services at the

airport, divided by the total number of traffic units handled, must not exceed the Joint

Maximum Tariff in accordance with these Rules. |

| 1.6. | For

reporting purposes, all monetary calculations must be expressed in pesos as of December 31

of the immediately preceding year, in accordance with a similar methodology as that set forth

in Financial Reporting Standard (NIF) B-10 “Inflationary Effects”. |

| 1.7. | One

traffic unit is defined as one passenger or 100 kilograms of cargo transported. The total

traffic units handled by a given airport shall be calculated as the sum of passengers arriving

and departing by air, including those in transit and transfer, who use the airport’s

infrastructure, plus the airport’s amount of cargo (measured in hundreds of kilograms)

arriving and departing, in transit and in transfer. |

| 1.8. | In

the event that a concession holder accrues revenues in excess of the established Joint Maximum

Tariff in a given calendar year, after a hearing with the concession holder the AFAC will

stipulate an adjustment to specific registered tariffs. The AFAC will permit the concession

holder to re-register its tariffs with the aim of reducing its revenues from Regulated Services. |

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

| 2.1. | As

per these Rules, Regulated Services are defined as: airport services, leases, and fees relating

to the contracts that the concession holder enters into with the providers of complementary

services. |

| 2.2. | The

following are expressly excluded from the Regulated Services: |

| 2.2.1. | Public

car parking services. |

| 2.2.2. | Leases

and fees relating to administrative offices or facilities that, in the opinion of the AFAC,

are not indispensable for the rendering of services to passengers or aircraft. |

| 3.1. | The

concession holder shall establish and register with the AFAC specific tariffs applicable

to each of the Regulated Services, in accordance with the provisions of articles 69 of the

Airport Law and 133, section I, 134, 135 and 136 of the Airport Law Regulations. Such specific

tariffs may only be modified once every six months ordinarily, or extraordinarily when adjustments

are made to the Joint Maximum Tariff or when the AFAC detects revenues accrued in excess

of the Joint Maximum Tariff in a given calendar year. |

| 3.2. | The

concession holder shall be at liberty to determine different tariff levels for different

times, operations volumes, regulated service packages, and other conditions in general, provided

that said tariffs do not exceed those registered with the AFAC and are applied to all users

that meet the corresponding conditions. The concession holder shall notify the AFAC of any

incentives, promotions, or discounts applicable to the tariffs. |

| 4. | Determination

of Joint Maximum Tariff |

| 4.1. | The

Joint Maximum Tariff will be determined ordinarily in the last six months of each five-year

period, that is, once every five years. However, during each five-year period the Joint Maximum

Tariff may be adjusted or updated as required, as set forth in points 5 and 7 of these Rules. |

| 4.2. | The

numeric values of the variables used to calculate the Joint Maximum Tariff will be proposed

by the concession holder during the final year of the preceding five-year period. They will

be subject to review and, if applicable, authorization by the AFAC, in accordance with the

provisions of Appendices A and B of these Rules. Economic and financial variables must be

stated in real terms from the immediately preceding year. |

| 4.3. | The

discount rate or rate of return applicable to the calculation of the Joint Maximum Tariff

will be established by the AFAC, in accordance with the provisions of point 9 of these Rules. |

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

| 4.4. | It

is hereby understood that the discount rate constitutes a parameter for the determination

of the Joint Maximum Tariff and under no circumstances will it be construed that the discount

rate on investments constitutes a guarantee or commitment on the part of the Federal Government

with regard to yield objectives or similar future returns. Furthermore, achievement of such

returns shall not constitute a condition for the concession holder’s compliance with

its obligations as set forth in the Concession Agreement. |

| 4.5. | The

Joint Maximum Tariff will be determined using the discounted cash flows method. The Joint

Maximum Tariff will be calculated and established on the basis of the following formula: |

| VPN |

Net

Present Value |

Refers

to reference value as of year n. |

| TMC |

Joint

Maximum Tariff |

Refers

to Joint Maximum Tariff per traffic unit for regulated services. |

| UT |

Traffic

Unit |

Refers

to the number of traffic units forecast for each year in the first five-year period of the proposed Master Development Program. |

| I |

Investments |

Sum

of committed investments to be made in each year of the first five-year period of the proposed Master Development Program, in relation

to the rendering of regulated services. |

| C |

Costs

and operating expenses |

All

forecasted costs and operating expenses (not including depreciation and amortization) for each year of the first five-year period

of the proposed Master Development Program, in relation to the rendering of regulated services. |

| r |

Discount

rate |

Refers

to the rate of return on investments. |

| n |

Year |

Refers

to each of the calendar years of the five-year period. |

| VT |

Terminal

Value |

Refers

to the residual value at the close of year 5, which will be estimated as set forth in point 10. |

| 4.6. | The

value of capital investments (I) to be included in the formula will only consider the sum

of estimated amounts for investments for the rendering of Regulated Services. |

| 4.7. | The

value of costs and operating expenses (C) to be included in the formula will only consider

the sums of estimated expenditures for the provision of Regulated Services, which shall be

broken down in accordance with the categories defined in Appendix A of the Rules. |

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

| 4.8. | During

an ordinary or extraordinary Joint Maximum Tariff review, the AFAC will request that the

concession holder provide any and all relevant information and documentation that substantiates

or helps to substantiate the proposed values for the sums of investments (I) and costs and

operating expenses (C), in order for the AFAC to authorize the proposed sums. If the AFAC

determines that such information contains errors and/or inconsistencies, a hearing will be

held with the concession holder and the AFAC may make modifications to the sums presented

by the concession holder for (I) and (C). |

| 4.9. | The

Joint Maximum Tariff determined in accordance with the aforementioned procedure shall be

binding for the applicable five-year period. In the process of reviewing and determining

the Joint Maximum Tariff, the AFAC will seek to reduce abrupt variations in each five-year

period. |

| 5. | Updates

and Adjustments to Joint Maximum Tariff |

| 5.1. | The

Joint Maximum Tariff, once determined for the corresponding five-year period, will be adjusted

annually for efficiency and will be updated for inflation, as provided in these Rules. |

| 5.2. | The

Joint Maximum Tariff will be adjusted on the first day of each year during the five-year

period in question according to the efficiency factor, which will be previously determined

in the ordinary five-yearly review. This efficiency factor must be published together with

the Joint Maximum Tariff at the start of the five-year period for each year. |

| 5.3. | The

efficiency factor will be determined by the AFAC and will be less than 1, expressed in decimals. |

| 5.4. | Adjustments

for efficiency will be determined according to the following formula: |

Where:

| TMCt |

New

Joint Maximum Tariff |

Refers

to current Joint Maximum Tariff, after adjustment for efficiency. |

| TMCt-1 |

Previous

Joint Maximum Tariff |

Refers

to Joint Maximum Tariff applicable up to adjustment for efficiency. |

| X |

Efficiency

factor adjustment |

Refers

to efficiency factor, expressed in decimals, that will be used to adjust the Joint Maximum Tariff. |

| 5.5. | Following

adjustment for efficiency, the Joint Maximum Tariff will be updated for accumulated inflation

according to the National Producer Price Index (hereafter, “INPP”), excluding

oil, published by the National Institute of Statistics and Geography (hereafter, “INEGI”).

Said updates shall be carried out every six months or in the event of an accumulated increase

greater than five per cent (5.0%), whichever occurs first following the date of the most

recent update for inflation. |

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

| 6. | Regular

Reviews of Joint Maximum Tariff |

| 6.1. | The

Joint Maximum Tariff will be revised regularly every five calendar years, within the final

six months of the current five-year period, when the Master Development Program for the subsequent

period is submitted for review. |

| 6.2. | On

the basis of the forecasts in the Master Development Program approved for the subsequent

period and these Rules, the AFAC will revise and determine the new parameters applicable

during the next five years, including new projections for traffic units, reference values,

discount rate, estimated operating costs and expenses, and investment commitments. |

| 6.3. | For

the purposes of the above, the Master Development Program must be prepared in accordance

with the procedures set forth in Appendix B of these Rules. |

| 6.4. | The

AFAC may at any time require the concession holder to provide any clarifications or additional

information it considers pertinent, and may request the opinions of airport users, air carriers,

and passengers. |

| 7. | Extraordinary

Adjustments to Joint Maximum Tariff |

| 7.1. | The

AFAC may carry out an extraordinary review and, if applicable, adjustment of the Joint Maximum

Tariff whether or not the relevant five-year period has elapsed, under the circumstances

set forth in this point. |

| 7.2. | At

the request of the concession holder, when operating costs or capital investments are required

in relation to the rendering of Regulated Services, which are not included in the Master

Development Program, as a result of: |

| 7.2.1. | Modifications

to the applicable legislation or regulations with regard to the quality standards that the

concession holder is required to meet prior to the next periodical review; |

| 7.2.2. | Modifications

to the applicable legislation or regulations that require the implementation of new security

measures or environmental protection measures that the concession holder must comply with

immediately; or |

| 7.2.3. | Natural

disasters that result in the modification of the Master Development Program, in terms of

both forecast demand and the investments and works required. For the purposes thereof, any

compensation deriving from respective insurance policies shall be taken into consideration,

at nominal value and as an operating expense, in the year immediately following payment of

said compensation, in order to adjust the Joint Maximum Tariff for subsequent years. If the

inclusion of compensation results in an abrupt rise in the Joint Maximum Tariff, the sum

may be spread over several years, with the respective price adjustment. |

| 7.3. | When

the AFAC authorizes the concession holder to reduce the capital investments established in

the approved Master Development Program, as a result of a significant decrease in air traffic

in a given year compared to the traffic forecast as used as an assumption in said Program

for the year in question, due to a contraction in economic activity in Mexico in excess of

five per cent (5.0%), measured in terms of the Gross Domestic Product reported by the INEGI

for the previous 12 consecutive months. |

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

| 7.4. | The

AFAC will adjust the Joint Maximum Tariff when as a result of the annual review it is determined

that in the immediately preceding year: |

| 7.4.1. | The

investments established in the current Master Development Program were not made in whole

or in part, and as a result works were not carried out or were carried out to a lesser standard. |

| 7.4.2. | Total

revenues accrued from the rendering of Regulated Services divided by the total number of

traffic units in the calendar year exceeded the updated, authorized Joint Maximum Tariff. |

| 7.5. | In

the circumstances set forth in points 7.4.1 and 7.4.2, and notwithstanding any applicable

penalties, the AFAC will reduce the Joint Maximum Tariff in such a way that, in accordance

with present value and based on the application of the discount rate in force, users are

compensated for the excess charges. In the case of the circumstance mentioned in point 7.4.2,

the AFAC may stipulate adjustments to specific tariffs. |

| 7.6. | When

extraordinary reviews are carried out: |

| 7.6.1. | The

concession holder must present any and all information and documentation that is requested

of it, as well as any other supporting documentation that justifies the request. |

| 7.6.2. | In

extraordinary reviews of the Joint Maximum Tariff, the reference values for the year in question

will be used, updated for inflation on the basis of the INPP excluding oil, and the formula

described in point 4.5 will be applied. |

| 7.6.3. | The

adjusted Joint Maximum Tariff, as per this point, will be applied for the remainder of the

period until the next regular review, on the understanding that it may be adjusted and updated

in accordance with the provisions of point 5 and this point. |

| 8. | Determination

of Reference Values |

| 8.1. | Reference

values represent the net present value of cash flows (before tax) projected and generated

by the rendering of Regulated Services. Their calculation method is described in Appendix

E of this document. They are the sum of revenues arising from the rendering of Regulated

Services, less costs and operating expenses (excluding depreciation and amortization) and

projected capital investments. |

| 8.2. | Reference

values constitute an indicative parameter only for the estimation, and where applicable the

determination, of the Joint Maximum Tariff. Consequently, they do not constitute a guarantee

of any nature on the part of the Federal Government with regard to financial returns or the

value of the airport business. |

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

| 8.3. | Reference

values will be calculated on the basis of the cash flow in the projections presented by the

concession holder as part of the most recent approved Master Development Program, which is

applicable to the period in question, and discounted at the applicable discount rate determined

by the AFAC as per point 9 below. |

| 8.4. | As

from the seventh ordinary period of determination of the Joint Maximum Tariff, a comparison

will first be made of forecast traffic units in the immediately preceding five-year period

against the actual traffic results over the same time. In the event that there is an accumulated

difference greater than 3% in the airport group, an adjustment will be made to the reference

value (year 6 according to the authorization document) to be used for the new calculation.

The economic value resulting from the excess traffic units above 3% will be deducted from

the reference value for year 6 of the five-year period immediately preceding the regular

review. Economic value shall be understood to mean regulated revenue less concession fees

on the excess income. |

| 8.5. | During

the procedure to determine the Joint Maximum Tariff for the following ordinary period, the

first reference value for the following five-year period will be re-estimated as the sum

of the approved reference values for the sixth year of the previous ordinary or extraordinary

review, as applicable, for each concession holder in the group, which will be distributed

to each concession holder on the basis of the actual average traffic units recorded during

the last five years. For the purposes thereof, the AFAC will calculate an annualized figure

for the remainder of the final year of the current five-year period on the basis of the traffic

units recorded during said year, in order to establish a five-year total for traffic units. |

| 8.6. | The

present value of payments disbursed to the government, in excess of those included in the

most recent ordinary review as per point 3 of Appendix A, shall be added to the reference

value for year 6 to be used in the following ordinary review. |

| 8.7. | For

the adjustments set forth in this section, the value determined in point 8.3 will first be

adjusted according to point 8.4, followed by 8.6 and finally 8.5. |

| 9. | Determination

of Discount Rate |

| 9.1. | The

Discount Rate or objective for return on investments is a measure of the capital cost (real,

before taxes) of companies in the airport industry, and constitutes just one parameter for

the determination of the Joint Maximum Tariff. The Discount Rate will be determined on the

basis of average rates in the airport sector in the United Mexican States. |

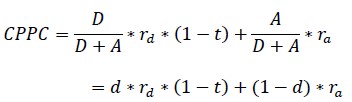

| 9.2. | For

the calculation of the Discount Rate, the Average Weighted Cost of Capital (hereafter, “CPPC”)

will first be determined according to internationally accepted methodology. This is defined

by the following formula: |

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

Where:

rd

is the cost of debt

ra

is the cost of equity

D

is the value of debt

A

is the value if equity

is

the level of leverage

is

the level of leverage

t

is the corporate income tax rate according to the Income Tax Law [Ley del Impuesto Sobre la Renta]

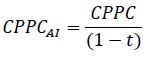

| 9.3. | Subsequently,

CPPC “before tax” will be calculated, according to the following formula: |

Where:

CCPC

AI is CPPC before tax

| 9.4. | Finally,

the Discount Rate is determined on the basis of CPPC “before tax-real”, according

to the following formula: |

Where:

is the five-year average of the expected inflation rate at period-end in the United States of America published

in the most recent World Economic Outlook publication by the International Monetary Fund.

is the five-year average of the expected inflation rate at period-end in the United States of America published

in the most recent World Economic Outlook publication by the International Monetary Fund.

| 9.5. | The

parameters used to calculate CPPC and Discount Rate will be estimated in accordance with

the procedures described below: |

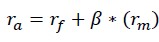

| 9.5.1. | Determination

of Cost of Equity (ra) |

The

cost of equity is determined using the Capital Asset Pricing Model (“CAPM”) methodology, based on the following formula:

Where:

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

r

a is the cost of equity

r

f is the risk-free rate of return

r

m is the market-risk premium

β

is the volatility of return of companies in the airport sector in Mexico in comparison to the stock market as a whole

Risk-Free

Rate of Return (r f )

The

risk-free rate of return will be determined on the basis of an average over the last five years of the rate of return on dollar-denominated

UMS (United Mexican States) Bonds issued on the global markets by the Government of the United Mexican States. For the purposes thereof,

UMS Bonds with maturity periods of between 5 and 30 years will be used for reference.

In

the event that the Government of the United Mexican States suspends UMS Bond issuances, the calculation will be based on the average

over the last five years of the rate of return on United States of America Treasury Bonds with maturity periods of between 5 and 30 years,

plus a country-risk premium provided by internationally recognized sources.

Market-Risk

Premium (r m)

The

market-risk premium represents the premium paid by the market for investment in assets on the stock market. Market risk must be quantified

as a measure of the relative volatility of the markets, in particular in relation to the market risk in the United States of America,

as indicated below:

Where:

r

m is the market-risk premium (%)

r

m,EEUU is the market-risk premium in the United States of America (%)

is the standard deviation of the stock market in Mexico (per Índice de Precios y Cotizaciones) (%)

is the standard deviation of the stock market in Mexico (per Índice de Precios y Cotizaciones) (%)

is the standard deviation of the stock market in the United States of America (per S&P 500) (%)

is the standard deviation of the stock market in the United States of America (per S&P 500) (%)

To

ensure objectivity, transparency, and consistency with other parameters, average values over the last five years as estimated by Aswath

Damodaran will be used for  and

.

and

.

In

the event that Aswath Damodaran suspends or cancels the publication of these parameters, the AFAC will determine them in accordance with

internationally accepted methodologies, using a weekly frequency for the last five years.

Beta

for Companies in the Airport Sector (β)

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

β

measures the sensitivity of returns on the shares of a company in relation to the yield of the stock market as a whole.

To

determine the value of β, the AFAC will follow the sequential steps outlined below:

| i). | Determine

the leveraged β value for each company in the airport sector that is traded on the stock

market in Mexico. To ensure objectivity, transparency, and consistency with other parameters,

the β value published by Reuters on its official website will be used, which is calculated

with a monthly frequency over the past five years. |

In

the event that Reuters suspends or cancels the publication of the required leveraged β values, the AFAC will determine leveraged

β values in accordance with internationally accepted methodologies, using a monthly frequency for the last five years.

| ii). | Deleverage

each leveraged β value obtained in step i), according to the following formula: |

For

the purposes of this calculation, the arithmetic average of the capital structure of all of the concession holders subject to these Rules

will be used, to calculate the mean D/A quotient reported in annual financial statements during the last five years.

| iii). | Re-leverage

each deleveraged β obtained in step ii), using the arithmetic average of the capital

structure of the airport group in particular, as a function of the D/A quotient reported

in annual financial statements during the last five years, for each concession holder that

makes up the airport group. |

| iv). | Obtain

the arithmetic average of the re-leveraged β values obtained in step iii). |

The

average β value obtained from this step will be the β value used as a parameter in the formula to determine the cost of equity

(r a).

During

each regular review, to estimate the level of leverage (d)

the  ratio will be calculated for the sum of the Mexican airport concession holders

that form part of the airport group in particular, in relation to their operations in Mexico, and the arithmetic averages of these levels

will then be determined. For the purposes thereof, average values observed during the last five years will be taken into account.

ratio will be calculated for the sum of the Mexican airport concession holders

that form part of the airport group in particular, in relation to their operations in Mexico, and the arithmetic averages of these levels

will then be determined. For the purposes thereof, average values observed during the last five years will be taken into account.

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

During

each regular review, to determine the cost of debt (rd)

the total cost of debt will be calculated for each airport group in particular, made up of the concessions holders subject to determination

of the Joint Maximum Tariff, including all short- and long-term debt in the form of credits, loans, bond issuances, and other financial

instruments (derivatives, options, etc.) with an implicit financial cost.

For

the purposes thereof, the concession holder must provide the cost of debt established in current loan agreements or similar documents,

which specify the general terms and conditions relating to interest rates, debt amounts, capital amortizations, and so on, and shall

explain the methodology used to determine the cost of debt presented for the last five years for the airport group, in relation to the

airport concession holders in Mexico and their operations in Mexico.

| 9.5.4. | Proposed

Capital Structure |

In

the event that the concessionaire decides to present a future capital structure and/or cost of debt that differs from that calculated

by the AFAC, with verifiable documentary supporting evidence, the AFAC shall consider the capital structure submitted by the concession

holders for the purposes of calculating the CPPC.

| 10. | Determination

of Terminal Value |

| 10.1. | Terminal

value represents the present value of cash flows to be generated during the remaining period

of validity of the concession. |

| 10.2. | Terminal

value will be calculated on the basis of the following formula: |

Where:

VT

is Terminal Value

FEN

is the cash flow corresponding to the final year of the five-year projection, calculated in accordance with Appendix E, excluding non-recurring

investments made during such year. Such investments shall be understood to refer to those relating to capacity increases, which shall

include but shall not be limited to new runways, new taxiways, new terminal buildings or the acquisition of land.

Subject

to the AFAC’s discretion, other recurring or non-recurring investments that are properly justified shall also be included.

r

is the discount rate calculated according to point 9 of these Rules.

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

n

is the number of years between the final calendar year of the five-year projection and the final calendar year of the concession period.

g

is calculated as the annual compound average growth rate (CAGR) of traffic units during the previous 10 years of the explicit forecast.

If this growth rate is inconsistent with historical traffic performance in the airport during the concession period that has already

elapsed, the AFAC may adjust the rate in accordance industry trends and specific growth rates in the airport.

| 11. | Supervision

of Compliance |

| 11.1. | Ordinarily

at the beginning of each year, or extraordinarily, the AFAC will verify the concession holder’s

degree of compliance with the application of the Joint Maximum Tariff and with the implementation

of the required investments during the immediately preceding calendar year. For the purposes

thereof, within the first three months of each calendar year, the concession holder will

provide the AFAC with a detailed annual report, covering all points mentioned in Appendix

C of these Rules. |

| 11.2. | In

order to verify compliance with investment commitments, physical and documentary inspections

will be carried out. For the purposes thereof, the AFAC will schedule compliance-verification

site visits at the airports under concession, with the aim of corroborating that the investments

have been carried out in accordance with the authorized program, and according to the standards

and specifications required by the applicable regulations. |

| 11.3. | In

the event that the concession holder requires an amendment to its Master Development Program

to adjust investment commitments in the current year or subsequent years, as a result of

an extraordinary situation that has been confirmed by the AFAC, it shall present an application

for authorization to the AFAC by the 31st of December of the year in question

at the latest. Under such circumstances, the AFAC will respond to the application within

a period of no more than 60 calendar days, in order for the relevant supervision activities

for compliance with investment obligations from the previous year to be carried out within

the first six months of the subsequent year. |

| 11.4. | Authorized

amendments to the Master Development Programs may not entail the alteration of annual investments

sums committed in the ordinary review, nor the total sums for the current five-year period,

unless the AFAC issues an authorization for which an analysis and valuations are previously

carried out. |

| 11.5. | Verification

of compliance with investment obligations shall be based on the version of the Master Development

Program in force at the moment that site visits are conducted. Any subsequent modifications

to the Master Development Program shall be applicable to the following ordinary or extraordinary

verification visit. |

| 11.6. | To

assess compliance with annual investment commitments, the AFAC will verify both physical

compliance with each investment project, as well as financial compliance as determined by

the investment sums disbursed. Therefore the concession holder may not evidence compliance

with investment projects without a physical inspection of the project by the AFAC, except

in the case of advance payments for multiannual projects or with the prior authorization

of the AFAC. |

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

| 11.7. | The

concession holder may reassign savings made in investment projects as a result of changes

in unit prices for construction or exchange-rate fluctuations, and invest these sums in other

projects, provided that the agreed scope of investment projects and the annual investment

sums authorized in the Master Development Program are not affected. |

| 11.8. | Once

the physical and documentary inspections have been carried out to verify compliance with

these Rules, and in the event of a modification to the Joint Maximum Tariff, the AFAC will

provide notification of the adjusted Joint Maximum Tariff for the airport within the first

six months of the year in question. The concession holder must therefore make the necessary

adjustments to its specific tariffs to comply with the maximum revenues determined by the

AFAC. |

| 11.9. | Notwithstanding

the foregoing, the AFAC may verify compliance with these Rules at any time. In relation thereto: |

| 11.9.1. | The

concession holder shall be obliged to provide periodic information as listed in Appendix

C, as well as any other document, information or clarification required by the AFAC, and |

| 11.9.2. | The

AFAC may conduct surveys and consultation processes, whether directly or through third parties,

with the participation of airport users, in order to verify information submitted by the

concession holder, compliance with quality standards, and compliance with the Master Development

Program. |

| 11.10. | The

AFAC may set forth specific requirements regarding the content and format of the information

and documentation that the concession holder must present in accordance with this point,

as well as forms and formulae that must be submitted. |

| 12.1. | These

Rules for Tariff Regulation shall enter into force as from the date of their notification

to the concession holder. |

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

APPENDIX

A

CRITERIA

TO ASSIGN COSTS AND EXPENSES CORRESPONDING TO THE PROVISION OF SERVICES INCLUDED AS REGULATED SERVICES

| 1. | Costs

and expenses directly attributable to the operation of airport services: |

| 1.1.1 | In

general, total costs are included for staff dedicated to airport activities, such as operations

staff, maintenance and upkeep staff, security staff, and airport firefighters. |

| 1.1.2 | Costs

relating to staff in shared areas, such as administrative, accounting and maintenance personnel,

among other categories, shall be included on the basis of their contribution to revenues

from Regulated Services during the last five years. |

| 1.1.3 | The

AFAC shall assess and validate the sums relating to total staff costs and their relation

to the rendering of Regulated Services. |

| 1.2.1 | In

general, expenses are included for electricity consumption in infrastructure and equipment,

as well as those areas of terminal buildings that are directly connected to the rendering

of airport services. In terminal buildings, the cost will be distributed according to the

square meters dedicated to the provision of Regulated Services as a proportion of total surface

area. |

| 1.2.2 | In

the event that this is not possible, all expenses that cannot be directly assigned to airport

services shall be included on the basis of their contribution to revenues from Regulated

Services during the last five fiscal years. |

| 1.2.3 | The

AFAC shall assess and validate the sums relating to electricity costs and their relation

to the rendering of Regulated Services. |

| 1.3 | Materials

and supplies: |

| 1.3.1 | In

general, expenses are included for materials and supplies used in infrastructure, equipment,

and the areas of terminal buildings directly involved in the provision of Regulated Services.

In the terminal building, the cost will be distributed in proportion to the use of the area

in the provision of Regulated Services. |

| 1.3.2 | In

the event that this is not possible, all expenses for materials and supplies that cannot

be directly assigned to airport services shall be included on the basis of their contribution

to revenues from Regulated Services. |

| 1.3.3 | The

AFAC shall assess and validate the sums relating to material and supply costs and their relation

to the rendering of Regulated Services. |

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

| 1.4 | Maintenance

and upkeep: |

| 1.4.1 | In

general, expenses are included for maintenance of infrastructure and equipment, and the areas

of terminal buildings directly involved in the provision of Regulated Services. In the terminal

building, the cost will be distributed in proportion to the number of square meters used

in the provision of Regulated Services. |

| 1.4.2 | In

the event that this is not possible, all expenses for maintenance that cannot be directly

assigned to Regulated Services shall be included on the basis of their contribution to revenues

from Regulated Services during the last five fiscal years. |

| 1.4.3 | The

AFAC shall assess and validate the sums relating to maintenance and upkeep costs and their

relation to the rendering of Regulated Services. |

| 1.5 | Insurance

and security: Included directly in Regulated Services, unless insurance or security services

are contract specifically for commercial services, which shall be excluded. |

| 1.6 | Taxes

and contributions: Included on the basis of their contribution to revenues from Regulated

Services during the last five years. |

| 1.7 | Other:

Sundry expenses not attributable exclusively to Regulated Services shall be included on the

basis of their contribution to revenues from Regulated Services during the last five years. |

| 1.8 | Any

other item that the AFAC considers necessary for determination of the Joint Maximum Tariff. |

| 2. | Costs

and expenses at the corporate level: |

| 2.1 | Airport

costs are assigned to each individual airport, in proportion to the number of traffic units

handled, as registered at each airport according to the average of the last five years. |

| 2.2 | The

following are distributed between airport costs and other costs: |

| 2.2.1 | Staff:

As set forth in point 1.1.1. above. |

| 2.2.2 | Office

rental and other general expenses: Included on the basis of their contribution to revenues

from Regulated Services during the last five years. |

| 3. | Concession

fees and duties: |

| 3.1 | The

amount of fees will correspond to the percentage established in the Federal Fees Law, applied

to the revenues derived from the rendering of services classed as Regulated Services. |

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

| 4. | Strategic

partner consultancy fees: |

Strategic

partner consultancy fees are assigned to each individual airport, in proportion to the number of passengers or cargo units handled, as

registered at each airport according to the average of the last five years. The sum assigned to Regulated Services will be the lower

of 30% or the contribution of revenues from Regulated Services to total revenues during the last five business years.

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

APPENDIX

B

PROCEDURE

TO PREPARE THE MASTER DEVELOPMENT PROGRAM

The

Master Development Program will be updated every five years, as provided in the Airport Law and the Airport Law Regulations, and in accordance

with the following procedure:

| 1. | Twenty-four

months prior to the date of the regular review, the concession holder will hire an independent

company with proven experience in the relevant activities to conduct and process user surveys

with regard to (a) existing quality standards, and those expected in the future, (b) traffic

forecasts for the coming fifteen years, and (c) investment needs during the time horizon

of the forecast. |

| 2. | Eighteen

months prior to the date of the regular review, the concession holder will prepare a draft

Master Development Program for the airport, based on the results of the aforementioned surveys

and in accordance with the provisions of the Airport Law and the Airport Law Regulations.

Among other requirements, this draft document must indicate the following: |

| 2.1 | Annual

forecasts for each of the fifteen subsequent years in real terms, unless otherwise determined

by the AFAC; |

| 2.2 | For

each year, operating and financial data must be included that includes as a minimum the forecasts

for passengers, cargo workload units, and aircraft movements, with detailed breakdowns and

in-depth explanations of the methodologies used to produce them. The AFAC may also require

additional data. |

| 2.3 | An

explanation must be provided of the quality standards applied, as well as the security measures

and environmental protection measures taken into consideration. Any proposed alterations

must be justified, and comparisons with other nationally and internationally used quality

standards shall be included. |

| 2.4 | Estimated

capital investments for each of the years covered, with a specification of whether they are

related or not to Regulated Services, including an explanation of the main assumptions and

methodologies used for estimation purposes, a detailed breakdown of the works to be carried

out, cost (including items), program with the greatest level of detail possible regarding

implementation and scope, and effects on the quality and capacity of the infrastructure; |

| 2.5 | A

detailed estimate of operating costs and expenses per year relating to Regulated Services,

with an explanation of the main assumptions used and following the criteria established in

Appendix A. |

| 2.6 | A

proposal for the discount rate to be used in the calculation of the Joint Maximum Tariff. |

| 2.7 | An

estimation of the implications for the Joint Maximum Tariff and specific tariffs. |

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

| 2.8 | Any

other information required by the AFAC. |

| 3. | Twelve

months prior to the date of the periodic review, and for a period of three months, the concession

holder will make the draft Master Development Program and the estimated projections for the

variables included in the equation for the Joint Maximum Tariff available for consultation

by users, by means of the Operation and Slots Committee. This information shall include (a)

quality standards, (b) traffic forecasts for the subsequent fifteen years, (c) investment

needs and an estimated unit cost of works during the same time horizon, and (d) implications

for the level of the Joint Maximum Tariff. |

| 4. | Nine

months prior to the date of the regular review, the concession holder will incorporate all

pertinent comments and observations from users into the draft Master Development Program. |

| 5. | Six

months prior to the date of the regular review, the concession holder will submit the draft

Master Development Program to the AFAC, together with the recommendation of the Operation

and Slots Committee. |

| 6. | For

purposes thereof, the concession holder shall provide all information required by the AFAC

relating to the Master Development Program. |

| 7. | During

the subsequent period, the AFAC will review the proposed Master Development Program and any

other information submitted by the concession holder. The AFAC may require the concession

holder to provide any additional clarification or information deemed necessary, and may request

additional opinions from airport users and the Operations and Slots Committee. |

| 8. | The

AFAC will issue its resolution in accordance with the provisions of articles 36, 37, 38,

39, 40, 41, 46, 48, 61, 62, 71, 72, 73 TERDECIES, 74 and 76 of the Airport Law, and 23, 24,

26, 29, 30, 31, 32, 33, 34, 35, 37, 38, 39, 40, 41, 42, 43, 44, 45, 47, 48, 49, 50, 52, 53,

54, 55, 56, 57, 58, 62, 65, 90, 94, 95, 112, 113, 114, 116, 117, 119, 120, 122, 129, 130,

131, 132, 146, 149, 151, 152, 154, 155 y 160 of the Airport Law Regulations. |

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

APPENDIX

C

ANNUAL

INFORMATION FROM CONCESSION HOLDER

Within

the first three months of each calendar year, the concession holder must submit the following information and documentation to the AFAC.

The information presented will correspond to the immediately preceding calendar year, and this obligation shall be applicable one year

after these Rules enter into force.

| 1. | Financial

statements prepared in accordance with Financial Reporting Standards, audited by an independent

accounting firm of recognized prestige, that clearly describe revenue and expense accounts

relating to Regulated Services and non-regulated services, and the details of accounts that

allow the identification thereof. |

| 2. | Total

monthly passenger statistics, with detailed analysis of arriving passengers, departing passengers,

transit passengers, transfer passengers, fee-paying passengers and those exempt from fees,

as well as the corresponding cargo statistics. The preceding data must be presented with

a breakdown by type of air transport service: scheduled, non-scheduled charter, non-scheduled

air taxi, and commercial and non-commercial private aviation. |

| 3. | Total

monthly operations statistics, identifying aircraft type and client. In the case of commercial

and non-commercial private air transport services, the concession holder must report an aggregate

number by type of air transport. |

| 4. | The

distribution of passengers and operations at different times throughout the day. |

| 5. | Indicators

regarding the level of use of infrastructure. |

| 6. | Level

of and compliance with the quality standards set forth in the Concession Agreement. |

| 7. | Details

of investments made and under way, as well as reports on compliance with investment commitments. |

| 8. | Current

debt rate corresponding to each short- and long-term credit. |

| 9. | Delay

and accident statistics. |

| 10. | Productivity,

operating and financial efficiency indicators for the airport. |

| 11. | Number

of persons employed, and total staff cost per operational or functional area, in accordance

with the criteria defined in Appendix A. |

| 12. | List

of airport and complementary service providers, describing the services they render and the

sums of the fees and rents paid by the service providers to the airport. |

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

In

the case of rents, the concession holder must include details of the rate per square meter, the number of square meters rented to each

airport and complementary service provider, as well as specific attributes of the lease area and its location.

| 13. | List

of air transport concession holders, assignees or permit holders that have been served at

the airport, with the monthly details of revenues received from each user for each airport

service and, if applicable, for each complementary service. |

| 14. | Copy

of all current insurance policies. |

| 15. | List

of insurance claims. |

| 16. | Sums

paid out as fees and duties to the Federal Government. |

| 17. | List

of operating costs attributable to the rendering of Regulated Services. |

| 18. | Any

other information that the AFAC deems necessary. |

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

APPENDIX

D

JOINT

MAXIMUM TARIFF DETERMINATION FORM

The

Federal Civil Aviation Agency, an autonomous administrative body within the Ministry of Infrastructure, Communications and Transport,

based on the provisions of articles 67, 69 and 70 of the Airport Law and of these Rules for Tariff Regulation, hereby determines:

| 1. | The

Joint Maximum Tariff of the airport, the reference values and the discount rate applicable

for the following five-year period shall be as follows: |

| Period |

Year |

Reference

Value |

Discount

Rate |

Joint

Maximum Tariff |

| 1 |

|

|

|

|

| 1 |

|

|

|

|

| 1 |

|

|

|

|

| 1 |

|

|

|

|

| 1 |

|

|

|

|

| 2 |

|

|

|

|

| 2. | The

discount rate is calculated in real terms and applies to cash flows expressed in Mexican

pesos, before taxes, as set forth in point 9 of the Rules. |

| 3. | The

Joint Maximum Tariff established in the table above shall be adjusted in accordance with

the provisions of the Rules for Tariff Regulation and the National Producer Price Index excluding

oil published by the National Institute of Statistics and Geography. |

| 4. | With

the prior approval of the AFAC, the concession holder may make investments ahead of time,

which shall be included in the Master Development Program for the following five-year period.

For the purposes thereof, the concession holders must submit the requisite technical, operating

and financial information that justifies bringing the investment forward. |

Letterhead: Ministry of Infrastructure, Communications and Transport Letterhead: Federal Civil Aviation Agency |

APPENDIX

E

PROCEDURE

FOR CASH FLOWS CALCULATION TO DETERMINE REFERENCE VALUES

Cash

flows shall be calculated as the sum of the following items:

Revenues

not including value added tax generated from the provision of Regulated Services (aeronautical revenues)

(less)

fees paid to the Federal Government, calculated according to the percentage applicable to total Airport Revenues

(less)

operating costs and expenses, and costs for the maintenance and upkeep of infrastructure, facilities and equipment, not including depreciations

and amortizations, incurred in the provision of Regulated Services

(less)

corporate costs assigned to the airport, costs incurred in the provision of Regulated Services, and Strategic Partner consultancy fees

assigned, (less) other extraordinary costs and expenses approved by the AFAC, incurred in the provision of Regulated Services.

(less)

capital investments in infrastructure and equipment linked exclusively to the provision of Regulated Services and approved in the airport’s

Master Development

Grupo Aeroportuario del ... (NASDAQ:OMAB)

Historical Stock Chart

From Oct 2024 to Nov 2024

Grupo Aeroportuario del ... (NASDAQ:OMAB)

Historical Stock Chart

From Nov 2023 to Nov 2024