As

filed with the Securities and Exchange Commission on February 8, 2024

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

WASHINGTON,

D.C. 20549

FORM

N-CSR

CERTIFIED

SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT

COMPANIES

Investment

Company Act file number 811-21650

ASA

GOLD AND PRECIOUS METALS LIMITED

Three

Canal Plaza, Suite 600

Portland,

ME 04101

Karen

Shaw, Principal Financial Officer

Three

Canal Plaza, Suite 600

Portland,

Maine 04101

207-347-2000

Date

of fiscal year end: November 30

Date

of reporting period: December 1 – November 30

ITEM

1. REPORT TO STOCKHOLDERS.

Annual

Report and Financial Statements

November 30, 2023

A

Closed-End Fund

Specializing

in Gold and Other

Precious

Metals Investments

ASA

Gold and Precious Metals Limited

Annual

Report and Financial Statements

November

30, 2023

Table

of Contents

Dear

Shareholder,

To

protect the interests of ASA and all its shareholders, ASA’s Board of Directors unanimously adopted a limited-duration shareholder

rights plan on December 31, 2023. Please read the message from ASA’s Board of Directors (the “Board”) below,

expanding on Saba Capital Management L.P.’s attempt to obtain creeping control of your fund, which the Board believes would

undermine ASA’s strategic focus on long-term capital appreciation in the global gold mining industry.

Portfolio

Performance and Attribution

The

closing share price of ASA Gold and Precious Metals Limited (“ASA”, “the Fund” or “the Company”)

on November 30, 2023, was $15.31, reflecting a total return of +7.5% for the previous 12 months versus a total return of +10.6%

for the NYSE Arca Gold Miners Index (GDMNTR) (the “Index”).

ASA

reported a net asset value (“NAV”) of $17.36 per share on November 30, 2023, with a total return increase of 3.0%

over the year. At the end of the fiscal year 2023, ASA shares were trading at a market price that was 11.8% less than its Net

Asset Value per share (NAV). This was an improvement from the start of the fiscal year when the shares were trading at a 15.5%

discount to the NAV. During this period, the average discount between the share price and the NAV was 14.6%, with the discount

varying between 11.0% and 17.3%.

At

fiscal year end, ASA's total net assets had increased to $334.9 million, a $9.5 million rise compared to the end of fiscal year

2022.

In

the past twelve months, ASA distributed $0.02 per share to its shareholders.

Large:

annual production > 1,000,000 ounces

Medium:

annual production 500,000 – 1,000,000 ounces

Small:

annual production < 500,000 ounces

Attribution:

a measure of the relative contribution to the performance

The

Fund's portfolio includes a range of companies involved in various phases of the mining process. Investments in production companies

are sorted based on their market capitalization. These investments have had an overall positive impact on the Fund's performance,

particularly the mid-cap mining companies, which were the most significant contributors. However, the Fund's investment in preproduction

companies, which cover both development and exploration stage companies, had a mixed effect. While exploration investments have

faced challenges, reflecting general industry trends, investments in development companies have had a modestly positive influence

on returns. The Fund's impressive gains in the small and mid-cap companies were partially offset by its exposure to underperforming

exploration companies, which are not part of the benchmark index. This exposure has resulted in the Fund's performance lagging

behind that of the index.

Management

Discussion

As

we concluded the fiscal year on November 30, 2023, we observed an impressive 15.1% increase in the price of gold. In contrast,

gold stocks, as measured by the NYSE Arca Gold Miners Index (GDMNTR), experienced a less dramatic

increase, rising by 10.6%. ASA’s

significant exposure to small cap companies has caused it to underperform the Index this year. However, since Peter Maletis first

initiated a repositioning of ASA’s portfolio in April 2019, the Fund's share price has surpassed that of the leading precious

metal ETFs, GDX and GDXJ, as well as the NYSE Arca Gold Miners Index. Taking advantage of the closed-end fund structure, Merk

has adopted a distinctive approach, concentrating on smaller cap companies, including select private investments, warrants and

convertible securities. This strategy sets the Fund apart from other public investment fund offerings.

The

fiscal year was marked by the absence of the anticipated US recession, with robust consumer spending and rising credit card debt.

Dominating the financial landscape were the Federal Reserve's substantial rate hikes, including four 25 basis point increases

and one 50 basis point hike. These monetary policy adjustments exerted pressure on both risk assets and gold, which is typically

sensitive to interest rate changes. Yet after the last rate hike in July, the equity market rallied, with expectations shifting

towards potential rate cuts in 2024. This optimism bolstered the market and rate-sensitive assets like gold. The year also saw

ongoing geopolitical tensions, notably the protracted conflict in Ukraine and the escalation of hostilities involving Hamas and

Israel following the October 7 terrorist attack on Israel. These developments heightened global geopolitical risk, potentially

influencing the gold market positively.

This

year, the gold market's robust performance significantly benefitted large gold mining companies with a high correlation to gold

prices, as well as many mid-cap gold mining and development companies. Consistent with this, ASA's largest contributors to returns

stemmed the Fund’s small cap holding focused on the Fund’s core strategy: backing management teams we know well to

develop potentially high-margin assets. The Fund’s largest holding, and top performing holdings, were Emerald Resources

(+148% return during the fiscal year) and G-Mining Ventures (+107%) exemplify the power of this approach, leveraging our network

and expertise to identify high-conviction early-stage opportunities. We remain committed to backing exceptional founders starting

new projects, confident that identifying and backing the best talent within the sector has the potential to generate strong returns.

In

our annual review, we observed a diverse range of performance outcomes among midcap and small-cap companies within the sector.

The market response was notably critical of firms that struggled to achieve production goals or effectively manage the lingering

cost implications from the Covid-19 pandemic. This dynamic was a significant influence on the underperformance of certain assets

within our portfolio. Particularly, Orla Mining and SSR Mining experienced challenges related to expanding their production capacities.

These challenges, while impactful, are anticipated to diminish over time. However, the shift in market expectations did adversely

affect the stock prices of these companies, reflecting a recalibration of investor confidence and market valuation.

While

producing companies gained from the increased gold prices, the Federal Reserve's “higher for longer” messaging created

a challenging financial landscape for exploration and development firms. This was evident in their share prices, as these companies

depend on market financing for their operations. The tough financial climate put pressure on their shares, as investor anticipated

that these companies would struggle to raise the capital necessary to run their companies. ASA's holdings in pre-production companies

experienced similar struggles alongside their industry counterparts. Nevertheless, a late-year surge in precious metals prices

sparked a recovery in these investments, showcasing their potential for strong returns in favorable conditions.

Looking

ahead, if the Federal Reserve has put “higher for longer” in the rear view mirror as we anticipate, it's worth recalling

how the ASA portfolio performed in 2020, especially as exploration and development companies significantly outshined others. In

our opinion, the current market situation and the emergence of unique investment opportunities closely mirror the period from

2019 to 2021. During that time, ASA's stock demonstrated exceptional performance, paving the way for what we believe is a promising

outlook for the Fund in the current market.

With

industry consolidation accelerating recently, quality exploration and resource projects could see increasing investor attention

looking ahead. As we review our positioning, we believe targeted exposure to top-tier resource companies with significant mineral

endowments in a good jurisdiction should provide optionality over the market cycle. We view it as a positive development that

larger mining entities intensified their M&A activities, and exploration and development companies proactively reduced costs

through efficiency measures and strategic mergers, aiming to lower overhead expenses.

The

year's most significant transaction was Newmont Mining's acquisition of Newcrest Mining, reflecting the industry's shift towards

a portfolio rich in copper and long-life assets. This acquisition is expected to trigger further M&A activity in 2024, particularly

with Newmont Mining's likely divestiture of non-core assets. Additionally, the year saw acquisitions in the small and mid-cap

segments, exemplified by Caliber Mining's takeover of Marathon Mining, which faced funding challenges in the final stages of mine

development.

At

ASA, our outlook for the precious metal mining sector in the upcoming year is positive. The sector appears well-positioned, with

large miners boasting what we consider clean balance sheets and generating substantial free cash

flow. The overall debt burden

in the sector is minimal, and we're observing a shift from companies merely focusing on stabilizing their operations to pursuing

more aggressive growth strategies. We anticipate that this trend, coupled with the current elevated gold prices, could be particularly

advantageous for ASA’s portfolio. ASA holds substantial positions in small and mid-cap miners, poised to significantly benefit

from the potential surge in merger and acquisition activities. We believe these companies stand to gain not only from potential

acquisitions but also from strategic mergers that could lead to them becoming larger entities. Post-merger, these merged companies

could potentially trade at higher multiples of their net asset value or cash flow, thereby offering enhanced returns. We remain

committed to providing exposure to the industry's top teams, focusing on significant projects, investing in companies at attractive

prices. Our continuous effort in this direction is aimed at sustaining strong performance to benefit our shareholders.

Please

reach out to us with questions at any time at asaltd.com/contact.

| Peter Maletis |

James Holman |

Axel Merk |

| Portfolio Manager |

Portfolio Manager |

Chief Investment Officer |

Message

from the ASA Board of Directors (Unaudited)

Saba

Capital Attempt to Control ASA

Saba

Capital Management, LP (“Saba”) has disclosed that it and its affiliates have acquired a position in ASA representing

16.87% of ASA’s outstanding common shares and has nominated a slate of directors for election to the Board at ASA’s

2024 annual meeting of shareholders. In response, on December 31, 2023, the Board of Directors of the Company unanimously adopted

a 120 day shareholder rights plan (“Rights Plan”) to protect the interests of the Company and all its shareholders.

The Rights Plan is intended to prevent Saba’s unilateral attempt to obtain creeping control of the Company, which the Board

believes would undermine ASA’s strategic focus on long-term capital appreciation in the global gold mining industry.

The

Rights Plan is designed to guard against tactics to gain control of ASA without the potential acquirer paying all shareholders

what the Board considers to be an appropriate control premium. The Board retains flexibility to take actions, such as entertaining

proposals from Saba or others, that it believes is in the best interest of the Company and its shareholders.

The

notes to the financial statements provide more details about the Rights Plan. The upcoming Proxy Statement will include additional

information.

We

welcome interaction with all shareholders, please reach out at asaltd.com/contact with any questions you may have.

ASA

Board of Directors

January

29, 2024

Forward-Looking

Statements

This

shareholder letter includes forward-looking statements, which involve known and unknown risks, uncertainties and other factors

that may cause the actual results, levels of activity, performance or achievements of the Company, or industry results, to be

materially different from any future results, levels of activity, performance or achievements expressed or implied by such forward-looking

statements. The Company’s actual performance or results may differ from its beliefs, expectations, estimates, goals and

projections, and consequently, investors should not rely on these forward-looking statements as predictions of future events.

Forward-looking statements are not historical in nature and generally can be identified by words such as “believe,”

“anticipate,” “estimate,” “expect,” “intend,” “should,” “may,”

“will,” “seek,” or similar expressions or their negative forms, or by references to strategy, plans, goals

or intentions. The absence of these words or references does not mean that the statements are not forward-looking. The Company’s

performance or results can fluctuate from month to month depending on a variety of factors, a number of which are beyond the Company’s

control and/or are difficult to predict, including without limitation: the Company’s investment decisions, the performance

of the securities in its investment portfolio, economic, political, market and financial factors, and the prices of gold, platinum

and other precious minerals that may fluctuate substantially over short periods of time. The Company may or may not revise, correct

or update the forward-looking statements as a result of new information, future events or otherwise.

The

Company concentrates its investments in the gold and precious minerals sector. This sector may be more volatile than other industries

and may be affected by movements in commodity prices triggered by international monetary and political developments. The Company

is a non-diversified fund and, as such, may invest in fewer investments than that of a diversified portfolio. The Company may

invest in smaller-sized companies that may be more volatile and less liquid than larger more established companies. Investments

in foreign securities, especially those in the emerging markets, may involve increased risk as well as exposure to currency fluctuations.

Shares of closed-end funds frequently trade at a discount to net asset value. All performance information reflects past performance

and is presented on a total return basis. Past performance is no guarantee of future results. Current performance may differ from

the performance shown.

This

shareholder letter does not constitute an offer to sell or solicitation of an offer to buy any securities.

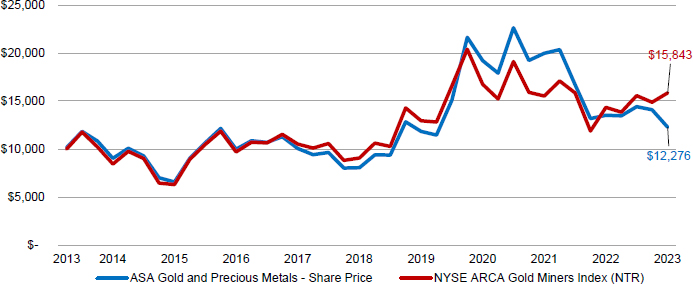

10-Year

Performance Returns (Unaudited)

Comparison

of Change in Value of a $10,000 Investment

ASA

Gold and Precious Metals – Share Price and NYSE ARCA Gold Miners Index (NTR)(1)

The

following chart reflects the change in the value of a hypothetical $10,000 investment, including reinvested dividends and distributions,

in ASA Gold and Precious Metals, Ltd. (the “Company”) compared with the performance of the benchmark, NYSE ARCA Gold

Miners Index (NTR), over the past ten fiscal years. The total return of the index includes the reinvestment of dividends and income.

The total return of the Company includes operating expenses that reduce returns, while the total return of the indices do not

include expenses. The Company is professionally managed, while the index is unmanaged and is not available for investment.

Fiscal

Year Total Returns

| Best Quarter (NAV): |

Q2 2020 |

80.11% |

| Worst Quarter (NAV): |

Q2 2022 |

-34.86% |

| Average Annual Total Returns |

|

|

|

|

| For

the years ended November 30, 2023 |

1

Year |

3

Year |

5

Year |

10

Year |

| ASA Gold

and Precious Metals - NAV |

2.98% |

-10.19% |

11.59% |

3.20% |

| ASA Gold

and Precious Metals - Share Price |

7.51% |

-8.28% |

12.22% |

2.07% |

| NYSE

ARCA Gold Miners Index NTR(1) |

10.56% |

-1.81% |

11.81% |

4.71% |

The

performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher

than the performance data quoted. For more current performance data, please visit http://www.asaltd.com/investor-information/factsheets.

The

results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The

results do not reflect the effect of taxes a shareholder would pay on Company distributions or on the sale of the Company’s

common shares.

The

investment return and market price will fluctuate and the Company’s common shares may trade at prices above or below NAV.

The Company’s common shares, when sold, may be worth more or less than their original cost.

| (1) | The

NYSE Arca Gold Miners Index (NTR) (the “Index”) is a net total return modified

capitalization weighted index comprised of publicly traded companies primarily involved

in the mining of gold and silver in locations around the world. The Company does not

attempt to replicate the Index. The Index does not necessarily reflect investments in

other precious metals companies (e.g., silver, platinum, and diamonds) in which the Company

may invest. Data about the performance of the Index is prepared or obtained by Management

and include reinvestment of all income dividends and other distributions, if any. The

Company may invest in securities not included in the Index and does not invest in all

securities included in Index. |

For

more complete information about the Company, please call us directly at 1-800-432-3378, or visit the Company’s website at

www.asaltd.com.

Certain

Investment Policies and Restrictions (Unaudited)

The

following is a summary of certain of the Company’s investment policies and restrictions and is subject to the more complete

statements contained in documents filed with the Securities and Exchange Commission.

The

concentration of investments in a particular industry or group of industries. It is a fundamental policy (i.e., a policy that

may be changed only by shareholder vote) of the Company that at least 80% of its total assets be (i) invested in common shares

or securities convertible into common shares of companies engaged, directly or indirectly, in the exploration, mining or processing

of gold, silver, platinum, diamonds or other precious minerals, (ii) held as bullion or other direct forms of gold, silver, platinum

or other precious minerals, (iii) invested in instruments representing interests in gold, silver, platinum or other precious minerals

such as certificates of deposit therefor, and/or (iv) invested in securities of investment companies, including exchange traded

funds, or other securities that seek to replicate the price movement of gold, silver or platinum bullion. Compliance with the

percentage limitation relating to the concentration of the Company’s investments will be measured at the time of investment.

If investment opportunities deemed by the Company to be attractive are not available in the types of securities referred to above,

the Company may deviate from the investment policy outlined in that paragraph and make temporary investments of unlimited amounts

in securities issued by the U.S. Government, its agencies or instrumentalities or other high quality money market instruments.

The

percentage of voting securities of any one issuer that the company may acquire. It is a non-fundamental policy (i.e., a policy

that may be changed by the Board of Directors) of the Company that the Company shall not purchase a security if, at the time of

purchase, more than 20% of the value of its total assets would be invested in securities of the issuer of such security.

Report

of Independent Registered Public Accounting Firm

To

the Board of Directors and Shareholders of ASA Gold and Precious Metals Limited

Opinion on the Financial Statements

We

have audited the accompanying statement of assets and liabilities of ASA Gold and Precious Metals Limited (the “Company”),

including the schedule of investments, as of November 30, 2023, the related statement of operations for the year then ended, statements

of changes in net assets for each of the two years in the period then ended, and financial highlights for each of the five years

in the period then ended, and the related notes (collectively referred to as the “financial statements”). In our opinion,

the financial statements present fairly, in all material respects, the financial position of the Company as of November 30, 2023,

the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then

ended, and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles

generally accepted in the United States of America..

Basis

for Opinion

These

financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on

the Company’s financial statements based on our audit. We are a public accounting firm registered with the Public Company

Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in

accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission

and the PCAOB. We have served as the Company’s auditor since 2012.

We

conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audits

to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error

or fraud. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial

reporting. As part of our audits we are required to obtain an understanding of internal control over financial reporting, but

not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting.

Accordingly, we express no such opinion.

Our

audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to

error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence

regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles

used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements.

Our procedures included confirmation of securities owned as of November 30, 2023 by correspondence with the custodian and private

companies. We believe that our audits provide a reasonable basis for our opinion.

TAIT,

WELLER & BAKER LLP

Philadelphia,

Pennsylvania

January

29, 2024

Schedule

of Investments

November

30, 2023

| Name of Company | |

Principal Amount

| | |

Value | | |

%

of Net

Assets

|

| Corporate Convertible

Bond | |

| | |

| | |

| |

| Gold mining, exploration,

development and royalty companies | |

| | | |

| | | |

| | |

| Canada | |

| | | |

| | | |

| | |

| i-80

Gold Corp., 8.00%, 2/22/27 (1) | |

$ | 3,000,000 | | |

$ | 2,889,300 | | |

| 0.9 | % |

| Total

corporate convertible bond (Cost $2,948,813) | |

| | | |

| 2,889,300 | | |

| 0.9 | |

| Name of Company | |

Shares | | |

Value | | |

%

of Net

Assets

|

| Common Shares | |

| | |

| | |

| |

| Gold mining, exploration,

development and royalty companies | |

| | | |

| | | |

| | |

| Australia | |

| | | |

| | | |

| | |

| Alicanto Minerals, Ltd. (2) | |

| 50,958,971 | | |

| 1,447,859 | | |

| 0.4 | |

| Barton Gold Holdings, Ltd. (2) | |

| 9,500,000 | | |

| 1,569,281 | | |

| 0.5 | |

| Bellevue Gold, Ltd. (2) | |

| 2,500,000 | | |

| 2,824,706 | | |

| 0.8 | |

| Cygnus Metals, Ltd. (2) | |

| 19,300,000 | | |

| 1,721,584 | | |

| 0.5 | |

| Emerald Resources NL (2) | |

| 15,000,000 | | |

| 28,247,057 | | |

| 8.4 | |

| LCL Resources, Ltd. (2) | |

| 36,750,000 | | |

| 509,934 | | |

| 0.1 | |

| Perseus Mining, Ltd. | |

| 5,500,000 | | |

| 7,013,860 | | |

| 2.1 | |

| Predictive Discovery, Ltd. (2) | |

| 94,183,334 | | |

| 14,624,432 | | |

| 4.4 | |

| Prodigy Gold NL (2) | |

| 116,250,000 | | |

| 537,685 | | |

| 0.2 | |

| | |

| | | |

| 58,496,398 | | |

| 17.4 | |

| Canada | |

| | | |

| | | |

| | |

| Agnico Eagle Mines, Ltd. | |

| 165,000 | | |

| 8,860,500 | | |

| 2.6 | |

| Alamos Gold, Inc. | |

| 1,000,000 | | |

| 14,810,000 | | |

| 4.4 | |

| American Pacific Mining Corp. 144A (2)(3) | |

| 3,000,000 | | |

| 431,114 | | |

| 0.1 | |

| Angel Wing Metals, Inc. (2) | |

| 4,650,000 | | |

| 445,484 | | |

| 0.1 | |

| Atex Resources, Inc. (2) | |

| 3,600,000 | | |

| 2,440,768 | | |

| 0.7 | |

| B2Gold Corp. | |

| 2,000,000 | | |

| 6,760,000 | | |

| 2.0 | |

| Barrick Gold Corp. | |

| 650,000 | | |

| 11,433,500 | | |

| 3.4 | |

| Calibre Mining Corp. (2) | |

| 10,000,000 | | |

| 9,580,309 | | |

| 2.9 | |

| Desert Gold Ventures, Inc. (2) | |

| 14,588,264 | | |

| 537,539 | | |

| 0.2 | |

| G Mining Ventures Corp. (2) | |

| 23,265,947 | | |

| 23,489,699 | | |

| 7.0 | |

| G2 Goldfields, Inc. (2) | |

| 3,000,000 | | |

| 1,746,564 | | |

| 0.5 | |

| GoGold Resources, Inc. (2) | |

| 2,857,140 | | |

| 3,032,007 | | |

| 0.9 | |

| HighGold Mining, Inc. (2) | |

| 3,000,000 | | |

| 784,848 | | |

| 0.2 | |

| Karora Resources, Inc. (2) | |

| 2,500,000 | | |

| 8,861,786 | | |

| 2.6 | |

| Lahontan Gold Corp. (2) | |

| 14,500,000 | | |

| 641,144 | | |

| 0.2 | |

| Liberty Gold Corp. (2) | |

| 12,482,000 | | |

| 3,127,514 | | |

| 0.9 | |

| Lotus Gold Corp. (1)(2) | |

| 5,912,500 | | |

| 2,178,599 | | |

| 0.7 | |

| Marathon Gold Corp. (2) | |

| 6,389,200 | | |

| 3,672,630 | | |

| 1.1 | |

| Mawson Gold, Ltd. (2) | |

| 10,600,000 | | |

| 2,734,073 | | |

| 0.8 | |

| Monarch Mining Corp. (1)(2) | |

| 7,300,000 | | |

| 26,899 | | |

| 0.0 | |

| Newcore Gold, Ltd. (2) | |

| 5,750,000 | | |

| 593,242 | | |

| 0.2 | |

| Nighthawk Gold Corp. (2) | |

| 6,148,000 | | |

| 1,585,762 | | |

| 0.5 | |

| O3 Mining, Inc. (2) | |

| 2,223,000 | | |

| 2,621,172 | | |

| 0.8 | |

| Onyx Gold Corp. (2) | |

| 750,000 | | |

| 107,778 | | |

| 0.0 | |

| Orla Mining, Ltd. (2) | |

| 6,200,000 | | |

| 18,596,116 | | |

| 5.6 | |

| Osino Resources Corp. (2) | |

| 5,000,000 | | |

| 4,532,223 | | |

| 1.4 | |

| Prime Mining Corp. (2) | |

| 7,600,000 | | |

| 8,793,250 | | |

| 2.6 | |

| Probe Gold, Inc. (2) | |

| 7,087,500 | | |

| 7,155,662 | | |

| 2.1 | |

| Roscan Gold Corp. (2) | |

| 10,886,900 | | |

| 1,002,883 | | |

| 0.3 | |

| Skeena Resources, Ltd. (2) | |

| 700,000 | | |

| 3,150,000 | | |

| 0.9 | |

| Talisker Resources, Ltd. (2) | |

| 2,500,000 | | |

| 654,040 | | |

| 0.2 | |

| TDG Gold Corp. (2) | |

| 9,227,925 | | |

| 1,258,091 | | |

| 0.4 | |

| Thesis Gold, Inc. (2) | |

| 13,198,758 | | |

| 5,252,463 | | |

| 1.6 | |

| 10 | The

notes to financial statements form an integral part of these statements. |

Schedule

of Investments (continued)

November

30, 2023

| Name of Company | |

Shares | | |

Value | | |

%

of Net

Assets

|

| Common

Shares (continued) | |

| | |

| |

| Gold mining, exploration,

development and royalty companies (continued) | |

| | | |

| | | |

| | |

| Canada (continued) | |

| | | |

| | | |

| | |

| Westhaven Gold

Corp. (2) | |

| 5,500,000 | | |

$ | 1,094,366 | | |

| 0.3 | % |

| | |

| | | |

| 161,992,025 | | |

| 48.2 | |

| Cayman Islands | |

| | | |

| | | |

| | |

| Endeavour Mining PLC | |

| 700,000 | | |

| 16,419,912 | | |

| 4.9 | |

| South Africa | |

| | | |

| | | |

| | |

| Gold Fields, Ltd. ADR | |

| 600,000 | | |

| 9,174,000 | | |

| 2.7 | |

| United Kingdom | |

| | | |

| | | |

| | |

| Anglogold Ashanti PLC | |

| 275,000 | | |

| 5,293,750 | | |

| 1.6 | |

| United States | |

| | | |

| | | |

| | |

| SSR

Mining, Inc. | |

| 800,000 | | |

| 9,439,038 | | |

| 2.8 | |

| Total gold mining, exploration, development and royalty companies (Cost $187,636,909) | | |

| 260,815,123 | | |

| 77.6 | |

| | |

| | | |

| | | |

| | |

| Diversified metals mining,

exploration, development and royalty companies | |

| | | |

| | | |

| | |

| Australia | |

| | | |

| | | |

| | |

| Auteco Minerals, Ltd. (2) | |

| 5,946,717 | | |

| 2,043,232 | | |

| 0.6 | |

| Bellavista Resources ltd (2) | |

| 3,772,832 | | |

| 209,403 | | |

| 0.1 | |

| Castile Resources, Ltd. (2) | |

| 15,143,255 | | |

| 590,348 | | |

| 0.2 | |

| Delta Lithium, Ltd. (2) | |

| 14,578,200 | | |

| 4,575,458 | | |

| 1.4 | |

| Genesis Minerals, Ltd. (2) | |

| 1,166,934 | | |

| 1,422,590 | | |

| 0.4 | |

| Geopacific Resources, Ltd.

(2) | |

| 28,135,714 | | |

| 334,632 | | |

| 0.1 | |

| | |

| | | |

| 9,175,663 | | |

| 2.8 | |

| Canada | |

| | | |

| | | |

| | |

| Adventus Mining Corp. (2) | |

| 5,310,000 | | |

| 1,408,748 | | |

| 0.4 | |

| Americas Gold & Silver Corp. (2) | |

| 2,701,028 | | |

| 665,817 | | |

| 0.2 | |

| Arizona Metals Corp. (2) | |

| 2,500,000 | | |

| 4,108,479 | | |

| 1.2 | |

| Aya Gold & Silver, Inc. (2) | |

| 2,900,000 | | |

| 21,307,344 | | |

| 6.4 | |

| Bunker Hill Mining Corp. (2) | |

| 19,214,957 | | |

| 1,699,248 | | |

| 0.5 | |

| Emerita Resources Corp. (2) | |

| 2,750,000 | | |

| 881,573 | | |

| 0.3 | |

| Huntsman Exploration, Inc. (2) | |

| 617,500 | | |

| 13,652 | | |

| 0.0 | |

| Integra Resources Corp. (2) | |

| 3,937,473 | | |

| 3,365,462 | | |

| 1.0 | |

| Max Resource Corp. (2) | |

| 8,200,000 | | |

| 694,941 | | |

| 0.2 | |

| Pan Global Resources, Inc. (2) | |

| 6,667,000 | | |

| 884,380 | | |

| 0.3 | |

| Red Pine Exploration, Inc. (2) | |

| 16,700,000 | | |

| 2,584,473 | | |

| 0.8 | |

| Sable Resources, Ltd. (2) | |

| 26,160,000 | | |

| 963,926 | | |

| 0.3 | |

| San Cristobal Mining, Inc.

(1)(2) | |

| 2,583,332 | | |

| 6,200,002 | | |

| 1.9 | |

| | |

| | | |

| 44,778,045 | | |

| 13.5 | |

| United States | |

| | | |

| | | |

| | |

| Bendito

Resources, Inc. 144A (1)(2)(3) | |

| 4,288,000 | | |

| 1,072,000 | | |

| 0.3 | |

| Total diversified metals mining, exploration, development and royalty companies (Cost $82,121,044) | 55,025,708 | | |

| 16.6 | |

| | |

| | | |

| | | |

| | |

| Silver mining, exploration,

development and royalty companies | |

| | | |

| | | |

| | |

| Canada | |

| | | |

| | | |

| | |

| Andean Precious Metals Corp. (2) | |

| 2,000,000 | | |

| 854,858 | | |

| 0.3 | |

| Discovery Silver Corp. (2) | |

| 7,154,545 | | |

| 4,692,542 | | |

| 1.4 | |

| Silver Mountain Resources, Inc. (2) | |

| 10,000,000 | | |

| 958,031 | | |

| 0.3 | |

| Silver Tiger Metals, Inc.

(2) | |

| 14,795,333 | | |

| 1,962,607 | | |

| 0.6 | |

| | |

| | | |

| 8,468,038 | | |

| 2.6 | |

| South Africa | |

| | | |

| | | |

| | |

| Sibanye

Stillwater, Ltd. ADR | |

| 273,043 | | |

| 1,217,772 | | |

| 0.4 | |

| Total silver mining, exploration, development and royalty companies (Cost $13,652,662) | 9,685,810 | | |

| 3.0 | |

| Total

common shares (Cost $283,410,615 ) | |

| | | |

| 325,526,641 | | |

| 97.2 | |

| The notes to financial statements

form an integral part of these statements. |

11 |

Schedule

of Investments (continued)

November

30, 2023

| Name of Company | |

Shares | | |

Value | | |

%

of Net

Assets

|

| Rights (1)(2) |

| Silver mining, exploration, development

and royalty companies |

| Canada |

| Pan

American Silver Corp. (Exp. Date 2/22/29) | |

| 393,200 | | |

$ | 91,808 | | |

| 0.0 | % |

| Total

rights (Cost $136,720) | |

| | | |

| 91,808 | | |

| 0.0 | |

| Warrants (1)(2) |

| Diversified metals mining, exploration,

development and royalty companies |

| Australia |

| Red Dirt Metals, Ltd. (Exercise

Price $0.25, Exp. Date 11/18/24) | |

| 2,834,650 | | |

| 449,519 | | |

| 0.1 | |

| Canada |

| Bunker Hill Mining Corp. (Exercise Price $0.37,

Exp. Date 4/1/25) | |

| 5,000,000 | | |

| 0 | | |

| 0.0 | |

| Bunker Hill Mining Corp. (Exercise Price $0.60,

Exp. Date 2/9/26) | |

| 1,250,000 | | |

| 0 | | |

| 0.0 | |

| Emerita Resources Corp. (Exercise Price $1.50,

Exp. Date 1/15/24) | |

| 1,375,000 | | |

| 0 | | |

| 0.0 | |

| Integra Resources Corp. (Exercise Price $1.38,

Exp. Date 6/16/24) | |

| 1,689,165 | | |

| 0 | | |

| 0.0 | |

| Red Pine Exploration, Inc.

(Exercise Price $0.25, Exp. Date 5/5/24) | |

| 8,350,000 | | |

| 0 | | |

| 0.0 | |

| | |

| | | |

| 0 | | |

| 0.0 | |

| Total diversified metals mining, exploration, development and royalty companies (Cost $465,631) |

| 449,519 | | |

| 0.1 | |

| Gold mining, exploration, development

and royalty companies |

| Canada |

| American Pacific Mining Corp. (Exercise Price

$1.40, Exp. Date 12/10/23) | |

| 1,500,000 | | |

| 0 | | |

| 0.0 | |

| Angel Wing Metals, Inc. (Exercise Price $0.80,

Exp. Date 6/16/24) | |

| 1,975,000 | | |

| 0 | | |

| 0.0 | |

| Angel Wing Metals, Inc. (Exercise Price $0.50,

Exp. Date 5/4/25) | |

| 350,000 | | |

| 0 | | |

| 0.0 | |

| Atex Resources, Inc. (Exercise Price $1.00,

Exp. Date 8/31/25) | |

| 675,000 | | |

| 49,744 | | |

| 0.0 | |

| Desert Gold Ventures, Inc. (Exercise Price $0.25,

Exp. Date 12/31/24) | |

| 594,132 | | |

| 0 | | |

| 0.0 | |

| G Mining Ventures Corp. (Exercise Price $1.90,

Exp. Date 9/9/24) | |

| 3,500,000 | | |

| 283,724 | | |

| 0.1 | |

| Gold Mountain Mining Corp. (Exercise Price $1.75,

Exp. Date 4/21/24) | |

| 2,200,000 | | |

| 0 | | |

| 0.0 | |

| Lahontan Gold Corp. (Exercise Price $0.65, Exp.

Date 3/24/24) | |

| 2,250,000 | | |

| 0 | | |

| 0.0 | |

| Lahontan Gold Corp. (Exercise Price $0.13, Exp.

Date 9/1/26) | |

| 4,150,000 | | |

| 0 | | |

| 0.0 | |

| Lotus Gold Corp. (Exercise Price $0.75, Exp.

Date 8/16/25) | |

| 2,200,000 | | |

| 16,213 | | |

| 0.0 | |

| Lotus Gold Corp. (Exercise Price $0.75, Exp.

Date 11/27/25) | |

| 506,250 | | |

| 3,731 | | |

| 0.0 | |

| Marathon Gold Corp. (Exercise Price $1.35, Exp.

Date 9/20/24) | |

| 1,675,000 | | |

| 12,344 | | |

| 0.0 | |

| Monarch Mining Corp. (Exercise Price $0.95,

Exp. Date 4/6/27) | |

| 1,700,000 | | |

| 0 | | |

| 0.0 | |

| Nighthawk Gold Corp. (Exercise Price $1.05,

Exp. Date 5/3/24) | |

| 900,000 | | |

| 0 | | |

| 0.0 | |

| Prime Mining Corp. (Exercise Price $5.00, Exp.

Date 4/27/24) | |

| 400,000 | | |

| 0 | | |

| 0.0 | |

| Prime Mining Corp. (Exercise Price $1.10, Exp.

Date 6/10/25) | |

| 920,000 | | |

| 393,235 | | |

| 0.1 | |

| TDG Gold Corp. (Exercise Price $0.75, Exp. Date

12/22/23) | |

| 225,000 | | |

| 0 | | |

| 0.0 | |

| Thesis Gold, Inc. (Exercise

Price $1.69, Exp. Date 9/28/24) | |

| 576,923 | | |

| 0 | | |

| 0.0 | |

| | |

| | | |

| 758,991 | | |

| 0.2 | |

| Total gold mining, exploration, development and royalty companies (Cost $1,602,122) | |

| 758,991 | | |

| 0.2 | |

| Silver mining, exploration, development

and royalty companies |

| Canada |

| Silver

Mountain Resources, Inc. (Exercise Price $0.50, Exp. Date 1/31/24) | |

| 5,000,000 | | |

| 0 | | |

| 0.0 | |

| Total silver mining, exploration, development and royalty companies (Cost $236,007) | 0 | | |

| 0.0 | |

| Total

warrants (Cost $2,303,760) | |

| | | |

| 1,208,510 | | |

| 0.3 | |

| Money Market Fund |

| Federated

US Treasury Cash Reserve Fund - Institutional Shares, 5.24% (4) | |

| 666,989 | | |

| 666,989 | | |

| 0.2 | |

| Total

money market fund (Cost $666,989) | |

| | | |

| 666,989 | | |

| 0.2 | |

| | |

| | | |

| | | |

| | |

Investments, at value (Cost $289,466,897)

| |

| | | |

| 330,383,248 | | |

| 98.6 | |

| Cash,

receivables and other assets less other liabilities | |

| | | |

| 4,529,215 | | |

| 1.4 | |

| Net

assets | |

| | | |

$ | 334,912,463 | | |

| 100.0 | % |

| ADR |

American Depositary Receipt |

| PLC |

Public Limited Company |

| 12 | The

notes to financial statements form an integral part of these statements. |

Schedule

of Investments (continued)

November

30, 2023

| (1) |

Security

fair valued in accordance with procedures adopted by the Board of Directors. At the period

end, the value of these securities amounted to $13,667,118 or 4.1% of net assets. |

| (2) |

Non-income producing

security. |

| (3) |

Security

exempt from registration under Rule 144A under the Securities Act of 1933. At the period

end, the value of these securities amounted to $1,503,114 or 0.5% of net assets. |

| (4) |

Dividend

yield changes daily to reflect current market conditions. Rate was the quoted yield as

of November 30, 2023. |

Portfolio

Statistics (Unaudited)

November

30, 2023

| Geographic Breakdown* | |

| |

|

| Australia | |

| 20.3 | % |

|

| Canada | |

| 65.4 | |

|

| Cayman Islands | |

| 4.9 | |

|

| South Africa | |

| 3.1 | |

|

| United Kingdom | |

| 1.6 | |

|

| United States | |

| 3.3 | |

|

| Other assets less other

liabilities | |

| 1.4 | |

|

| | |

| 100.0 | % |

|

*Geographic

breakdown, which is based on company domiciles, is expressed as a percentage of total net assets including cash.

| The notes to financial statements

form an integral part of these statements. |

13 |

Statement

of Assets and Liabilities

November

30, 2023

| Assets | |

| |

| Investments, at value (Cost $289,466,897) | |

$ | 330,383,248 | |

| Cash | |

| 77,792 | |

| Foreign currency (Cost $4,702,892) | |

| 4,741,161 | |

| Dividends and interest receivable, net of withholding taxes payable | |

| 328,234 | |

| Prepaid expenses | |

| 88,561 | |

| Total assets | |

$ | 335,618,996 | |

| | |

| | |

Liabilities | |

| | |

| Accrued investment adviser fees | |

| 175,736 | |

| Accrued fund service fees | |

| 27,242 | |

| Liability for retirement benefits due to retired directors | |

| 335,956 | |

| Other expenses | |

| 167,599 | |

| Total liabilities | |

| 706,533 | |

| Net assets | |

$ | 334,912,463 | |

| | |

| | |

Common shares $1 par value

Authorized: 40,000,000 shares

Issued and Outstanding: 19,289,905 shares | |

$ | 19,289,905 | |

| Share premium (capital surplus) | |

| 1,372,500 | |

| Distributable earnings | |

| 314,250,058 | |

| Net assets | |

$ | 334,912,463 | |

| Net asset value per share | |

$ | 17.36 | |

The

closing price of the Company’s shares on the New York Stock Exchange was $15.31 on November 30, 2023.

| 14 | The

notes to financial statements form an integral part of these statements. |

Statement

of Operations

For

the year ended November 30, 2023

| Investment income | |

| |

| Dividend income (net of withholding taxes of 402,241) | |

$ | 2,297,437 | |

| Interest income | |

| 97,114 | |

| Total investment income | |

| 2,394,551 | |

| | |

| | |

| Expenses | |

| | |

| Investment adviser fees | |

| 2,377,025 | |

| Fund services fees | |

| 185,830 | |

| Compliance services fees | |

| 80,000 | |

| Transfer agent fees | |

| 61,956 | |

| Custodian fees | |

| 125,936 | |

| Directors’ fees and expenses | |

| 242,466 | |

| Retired directors’ fees | |

| 74,992 | |

| Insurance fees | |

| 121,348 | |

| Legal fees | |

| 123,442 | |

| Audit fees | |

| 35,000 | |

| Shareholder reports and proxy expenses | |

| 39,326 | |

| Dues and listing fees | |

| 25,000 | |

| Other expenses | |

| 57,578 | |

| Total expenses | |

| 3,549,899 | |

| Change in retirement benefits due to retired directors | |

| (43,286 | ) |

| Investment adviser fees waived | |

| (32,028 | ) |

| Net expenses | |

| 3,474,585 | |

| Net investment loss | |

| (1,080,034 | ) |

| |

| Net realized and unrealized gain (loss) from investments and foreign currency transactions |

| Proceeds from sales | |

| 34,858,600 | |

| Cost of securities sold | |

| (25,895,680 | ) |

| Net realized gain from investments | |

| 8,962,920 | |

| Net realized gain (loss) from foreign currency transactions | |

| | |

| Investments | |

| 25,848 | |

| Foreign currency | |

| 155,246 | |

| Net realized gain from foreign currency transactions | |

| 181,094 | |

| Net increase in unrealized appreciation (depreciation) on investments | |

| | |

| Balance, beginning of year | |

| 39,254,852 | |

| Balance, end of year | |

| 40,916,351 | |

| Net increase in unrealized appreciation (depreciation) on investments | |

| 1,661,499 | |

| Net unrealized gain on translation of assets and liabilities in foreign currency | |

| 153 | |

| Net realized and unrealized gain from investments and foreign currency transactions | |

| 10,805,666 | |

| Net increase in net assets resulting from operations | |

$ | 9,725,632 | |

| The notes to financial statements

form an integral part of these statements. |

15 |

Statements

of Changes in Net Assets

| | |

Year Ended November 30,

2023 | | |

Year Ended November 30,

2022 | |

| Net investment loss | |

$ | (1,080,034 | ) | |

$ | (1,404,855 | ) |

| Net realized gain | |

| 8,962,920 | | |

| 26,955,986 | |

| Net realized gain (loss) from foreign currency transactions | |

| 181,094 | | |

| (187,107 | ) |

Net increase (decrease) in unrealized appreciation (depreciation) on investments

| |

| 1,661,499 | | |

| (181,343,210 | ) |

| Net unrealized gain on translation of assets and liabilities in foreign currency | |

| 153 | | |

| 39,158 | |

| Net increase (decrease) in net assets resulting from operations | |

| 9,725,632 | | |

| (155,940,028 | ) |

| Dividends paid/payable | |

| (385,798 | ) | |

| (385,798 | ) |

| Net increase (decrease) in net assets | |

| 9,339,834 | | |

| (156,325,826 | ) |

| Net assets, beginning of year | |

| 325,572,629 | | |

| 481,898,455 | |

| Net assets, end of year | |

$ | 334,912,463 | | |

$ | 325,572,629 | |

| 16 | The

notes to financial statements form an integral part of these statements. |

Notes

to Financial Statements

Year

ended November 30, 2023

1.

Organization

ASA

Gold and Precious Metals Limited (the “Company”) is a non-diversified, closed-end investment company registered under

the Investment Company Act of 1940, as amended (the “1940 Act”).

The

Company was initially organized as a public limited liability company in the Republic of South Africa in June 1958. On November

11, 2004, the Company’s shareholders approved a proposal to move the Company’s place of incorporation from the Republic

of South Africa to the Commonwealth of Bermuda by reorganizing itself into an exempted limited liability company formed in Bermuda.

The Company is registered with the Securities and Exchange Commission (the “SEC”) pursuant to an order under Section

7(d) of the 1940 Act.

The

Company seeks long-term capital appreciation primarily through investing in companies engaged in the exploration for, development

of projects or mining of precious metals and minerals. The Company is managed by Merk Investments LLC (the “Adviser”).

2.

Summary of significant accounting policies

The

following is a summary of the significant accounting policies:

A.

Security valuation

The

net asset value of the Company generally is determined as of the close of regular trading on the New York Stock Exchange (the

“NYSE”) on the date for which the valuation is being made (the “Valuation Time”). Portfolio securities

listed on U.S. and foreign stock exchanges generally are valued at the last reported sale price as of the Valuation Time on the

exchange on which the securities are primarily traded, or the last reported bid price if a sale price is not available.

Pursuant

to Rule 2a-5 under the Investment Company Act, the Company’s Board of Directors (the "Board") has designated the

Adviser, as defined in Note 4, as the Company’s valuation designee to perform any fair value determinations for securities

and other assets held by the Company. The Adviser is subject to the oversight of the Board and certain reporting and other requirements

intended to provide the Board the information needed to oversee the Adviser's fair value determinations. The Adviser is responsible

for determining the fair value of investments in accordance with policies and procedures that have been approved by the Board.

Under these procedures, the Adviser convenes on a regular and ad hoc basis to review such investments and considers a number of

factors, including valuation methodologies and unobservable inputs, when arriving at fair value. The Board has approved the Adviser’s

fair valuation procedures as a part of the Company’s compliance program and will review any changes made to the procedures.

Securities

traded over the counter are valued at the last reported sale price or the last reported bid price if a sale price is not available.

Securities listed on foreign stock exchanges may be fair valued at a value other than the last reported sale price or last reported

bid price based on significant events that have occurred subsequent to the close of the foreign markets. Shares of non-exchange

traded open-end mutual funds are valued at net asset value (“NAV”). To value its warrants, the Company's valuation

designee typically utilizes the Black-Scholes model using the listed price for the underlying common shares. The valuation is

a combination of value of the stock price less the exercise price, plus some value related to the volatility of the stock over

the remaining time period prior to expiration.

Securities

for which current market quotations are not readily available are valued at their fair value as determined in accordance with

procedures approved by the Board. If a security is valued at a “fair value,” that value may be different from the

last quoted price for the security. Various factors may be reviewed in order to make a good faith determination of a security’s

fair value. These factors include, but are not limited to, the nature of the security; relevant financial or business developments

of the issuer; actively traded similar or related securities; conversion rights on the security; and changes in overall market

conditions.

The

difference between cost and market value is reflected separately as net unrealized appreciation (depreciation) on investments.

The net realized gain or loss from the sale of securities is determined for accounting purposes on the identified cost basis.

B.

Fair value measurement

In

accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”), fair

value is defined as the price that the Company would receive to sell an investment or pay to transfer a liability in a timely

transaction with an independent buyer in the principal market, or in the absence of a principal market the most advantageous

market for the investment or liability. U.S. GAAP establishes a three-tier hierarchy to distinguish between (1) inputs that

reflect the assumptions market participants would use in pricing an asset or liability developed based on

Notes

to Financial Statements (continued)

Year

ended November 30, 2023

2.

Summary of significant accounting policies (continued)

B.

Fair value measurement (continued)

market

data obtained from sources independent of the reporting entity (observable inputs) and (2) inputs that reflect the reporting entity’s

own assumptions about the assumptions market participants would use in pricing an asset or liability developed based on the best

information available in the circumstances (unobservable inputs) and to establish classification of fair value measurements for

disclosure purposes. Various inputs are used in determining the value of the Company’s investments. The inputs are summarized

in the three broad levels listed below.

| Level

1 – | Unadjusted quoted prices in active markets for identical assets or liabilities that the Company has the ability to access. |

| Level

2 – | Observable

inputs other than quoted prices included in level 1 that are observable for the asset

or liability either directly or indirectly. These inputs may include quoted prices for

identical instruments on an inactive market, prices for similar investments, interest

rates, prepayment speeds, credit risk, yield curves, default rates, and similar data. |

| Level

3 – | Unobservable

inputs for the assets or liability to the extent that relevant observable inputs are not available, representing the

Company’s own assumptions about the assumptions that a market participant would use in valuing the asset or

liability, and that would be based on the best information available. |

The

inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those

securities.

The

following is a summary of the inputs used as of November 30, 2023 in valuing the Company’s investments at fair value:

Investment

in Securities (1)

Measurements

at November 30, 2023

| | |

Level 1 | | |

Level 2 | | |

Level 3 | | |

Total | |

| Corporate Convertible Bond | |

| | | |

| | | |

| | | |

| | |

| Gold mining, exploration, development and royalty companies | |

$ | — | | |

$ | — | | |

$ | 2,889,300 | | |

$ | 2,889,300 | |

| Common Shares | |

| | | |

| | | |

| | | |

| | |

| Gold mining, exploration, development and royalty companies | |

| 256,624,081 | | |

| 1,985,544 | | |

| 2,205,498 | | |

| 260,815,123 | |

| Diversified metals mining, exploration, development and royalty companies | |

| 47,740,054 | | |

| 13,652 | | |

| 7,272,002 | | |

| 55,025,708 | |

| Silver mining, exploration, development and royalty companies | |

| 9,685,810 | | |

| — | | |

| — | | |

| 9,685,810 | |

| Rights | |

| | | |

| | | |

| | | |

| | |

| Silver mining, exploration, development and royalty companies | |

| — | | |

| — | | |

| 91,808 | | |

| 91,808 | |

| Warrants | |

| | | |

| | | |

| | | |

| | |

| Diversified metals mining, exploration, development and royalty companies | |

| — | | |

| — | | |

| 449,519 | | |

| 449,519 | |

| Gold mining, exploration, development and royalty companies | |

| — | | |

| — | | |

| 758,991 | | |

| 758,991 | |

| Silver mining, exploration, development and royalty companies | |

| — | | |

| — | | |

| 0 | | |

| 0 | |

| Money Market Fund | |

| 666,989 | | |

| — | | |

| — | | |

| 666,989 | |

| Total Investments | |

$ | 314,716,934 | | |

$ | 1,999,196 | | |

$ | 13,667,118 | | |

$ | 330,383,248 | |

| (1) | See

schedule of investments for country classifications. |

Notes

to Financial Statements (continued)

Year

ended November 30, 2023

2.

Summary of significant accounting policies (continued)

B.

Fair value measurement (continued)

The

following is a reconciliation of Level 3 investments for which significant unobservable inputs were used to determine fair value.

| | |

Corporate

Convertible

Bond | | |

Common

Stock | | |

Rights | | |

Warrants | |

| Balance November 30, 2022 | |

$ | — | | |

$ | 2,511,245 | | |

$ | 96,088 | | |

$ | 5,939,911 | |

| Purchases | |

| 2,940,000 | | |

| 5,309,217 | | |

| — | | |

| 150,286 | |

| Sales | |

| — | | |

| — | | |

| — | | |

| (334,848 | ) |

| Realized loss | |

| — | | |

| — | | |

| — | | |

| (1,427,016 | ) |

| Accretion of discount | |

| 8,813 | | |

| — | | |

| — | | |

| — | |

| Transfers in from level 1* | |

| — | | |

| 352,749 | | |

| — | | |

| — | |

| Net change in unrealized appreciation (depreciation) | |

| (59,513 | ) | |

| 1,304,289 | | |

| (4,280 | ) | |

| (3,119,823 | ) |

| Balance November 30, 2023 | |

$ | 2,889,300 | | |

$ | 9,477,500 | | |

$ | 91,808 | | |

$ | 1,208,510 | |

| Net change in unrealized appreciation (depreciation) from investments held as of November 30, 2023** | |

$ | (59,513 | ) | |

$ | 1,304,289 | | |

$ | (4,280 | ) | |

$ | (3,119,823 | ) |

*

The Company has adopted a policy of recording any transfers of investment securities between the different level in the fair value

hierarchy as of the end of the year

**

The change in unrealized appreciation/(depreciation) is included in net change in unrealized appreciation/(depreciation) of investments

in the accompanying Statement of Operations.

Notes

to Financial Statements (continued)

Year

ended November 30, 2023

2.

Summary of significant accounting policies (continued)

B.

Fair value measurement (continued)

Significant

unobservable inputs developed by the valuation designee for Level 3 investments held at November 30, 2023 are as follows:

| Asset Categories | |

Fair Value | | |

Valuation

Technique(s) | |

Unobservable

Input | |

Range

(Weighted

Average) | | |

Impact to

Valuation from an

Increase

in Input1 |

| Corporate Convertible Bond2 | |

$ | 2,889,300 | | |

Implied Interest Rate | |

Discount | |

13% (13%) | | |

Increase |

| Common Shares3 | |

| 9,477,500 | | |

Transaction Cost/Latest Round of Financing | |

None | |

None | | |

None |

| Rights4 | |

| 91,808 | | |

Market Transaction | |

Discount | |

70% (70%) | | |

Increase |

| Warrants5 | |

| 1,208,510 | | |

Black Scholes Method | |

Volatility | |

20% - 50% (38%) | | |

Increase |

1

This column represents the directional change in the fair value of the level 3 investments that would result from an increase

to the corresponding unobservable input. A decrease to the unobservable input would have the opposite effect

2

Fair valued corporate convertible bonds are valued based on applying a fixed discount rate to the fixed income portion,

which represents the implied interest rate that would have valued the entire corporate convertible bond at the time of issuance.

3

Fair valued common shares with no public market are valued based on transaction cost or latest round of financing.

4

Fair valued rights are valued based on the specifics of the rights at a discount to the market price of the underlying security.

5

Warrants are priced based on the Black Scholes Method; the key input to this method is modeled volatility of the investment; the

lower the modeled volatility, the lower the valuation of the warrant.

C.

Foreign Currency Translation

Portfolio

securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollar amounts at the rate

of exchange reported by independent data providers. Purchases and sales of investment securities and income and expense items

denominated in foreign currencies are translated into U.S. dollar amounts on the respective dates of such transactions. The portion

of the results arising from changes in the exchange rates and the portion due to fluctuations arising from changes in the market

prices of securities are not isolated. The resulting net foreign currency gain or loss is included on the Statements of Operations.

Realized foreign currency gains or losses arise from sales of foreign currencies, currency gains or losses realized between the

trade and settlement dates on securities transactions and the difference between the amounts of dividends, interest, and foreign

withholding taxes recorded on the Company’s books and the U.S. dollar equivalent of the amounts actually received or paid.

D.

Securities Transactions and Investment Income

During

the year ended November 30, 2023, sales and purchases of portfolio securities (other than temporary short-term investments) amounted

to $34,858,600 and $33,787,778, respectively.

As

of November 30, 2023, a significant portion of the Company’s assets consisted of securities of junior and intermediate mining

company issuers.

Dividend

income is recorded on the ex-dividend date, net of withholding taxes or ADR fees, if any. Interest income is recognized on the

accrual basis. Premium is amortized to the next call date above par and discount is accreted to maturity using the effective interest

method.

Notes

to Financial Statements (continued)

Year

ended November 30, 2023

2.

Summary of significant accounting policies (continued)

E.

Dividends to Shareholders

Dividends

to shareholders are recorded on the ex-dividend date. The reporting for financial statement purposes of dividends paid from net

investment income and/or net realized gains may differ from their ultimate reporting for U.S. federal income tax purposes, primarily

because of the separate line item reporting for financial statement purposes of foreign exchange gains or losses.

F.

Use of Estimates

The

preparation of the financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that

affect amounts reported in the financial statements and accompanying notes. Actual results could differ from those estimates.

It is management’s opinion that all adjustments necessary for a fair statement of the results of the interim periods presented

have been made. All adjustments are of a normal recurring nature.

G.

Basis of Presentation

The

financial statements are presented in U.S. dollars. The Company is an investment company and accordingly follows the investment

company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standard

Codification, Topic 946 “Financial Services - Investment Companies”.

H.

Income Taxes

In

accordance with U.S. GAAP requirements regarding accounting for uncertainties on income taxes, management has analyzed the Company’s

tax positions taken on federal and state income tax returns, as applicable, for all open tax years (2020-2023). As of November

30, 2023, the Company has not recorded any unrecognized tax benefits. The Company’s policy, if it had unrecognized benefits,

is to recognize accrued interest and penalties in operating expenses.

3.

Tax status of the Company

The

Company is a “passive foreign investment company” (“PFIC”) for U.S. federal income tax purposes and is

not subject to Bermuda tax as an exempted limited liability company organized under the laws of Bermuda. Nor is the Company generally

subject to U.S. federal income tax, since it is a non-U.S. corporation whose only business activity in the United States is trading

in stocks or securities for its own account; under the U.S. federal tax law that activity does not constitute engaging in the

conduct of a trade or business within the United States, even if its principal office is located therein. As a result, its gross

income is not subject to U.S. federal income tax, though certain types of income it earns from U.S. sources (such as dividends

of U.S. payors) are subject to U.S. federal withholding tax.

4.

Fees and Expenses and Other Transactions with Affiliates

Investment

Adviser – Merk Investments LLC (the “Adviser”) is the investment adviser to the Company. Pursuant to an investment

advisory agreement, the Adviser receives an advisory fee, payable monthly, from the Company at an annual rate of 0.70% of the

Company’s average daily net assets.

The

Adviser voluntarily agreed to waive a portion of its advisory fee, equal to an annual rate of 0.05% of the Company’s net

assets exceeding $300 million, and an additional 0.10% of the Company’s net assets exceeding $500 million. The Adviser may

waive additional fees at any time. The Adviser waived $32,028 for the year ended November 30, 2023.

Other

Service Providers – Apex US Holdings LLC (d/b/a Apex Fund Services) (“Apex”) provides fund accounting, fund

administration and compliance services to the Company. The fees related to these services are included in fund services fees within

the Statement of Operations. Apex also provides certain shareholder report production and EDGAR conversion and filing services.

Pursuant to an Apex services agreement, the Company pays Apex customary fees for its services. Apex provides a Principal Financial

Officer, as well as certain additional compliance support functions.

Foreside

Fund Services, LLC, a wholly owned subsidiary of ACA Group, provides a Chief Compliance Officer to the Company.

5.

Exemptive order

The

Company is a closed-end investment company and operates pursuant to an exemptive order issued by the Securities and Exchange Commission

(the “SEC”) pursuant to Section 7(d) of the 1940 Act (the “Order”). The Order is conditioned upon, among

other things, the Company complying with certain requirements relating to the custody of assets and settlement of securities transactions

outside of the United States different than those required of other registered

Notes

to Financial Statements (continued)

Year

ended November 30, 2023

5.

Exemptive order (continued)

investment

companies. These conditions make it more difficult for the Company to implement a flexible investment strategy and to fully achieve

its desired portfolio diversification than if it were not subject to such requirements.

6.

Retirement plans

The

Company has recorded a liability for retirement benefits due to retired directors. The liability for these benefits at November

30, 2023 was $335,956. A director whose first election to the Board of Directors was prior to January 1, 2008 qualifies to receive

retirement benefits if he has served the Company (and any of its predecessors) for at least twelve years prior to retirement.

Directors first elected on or after January 1, 2008 are not eligible to participate in the plan.

7.

Indemnifications

In

the ordinary course of business, the Company enters into contracts that contain a variety of indemnification provisions. The

Company’s maximum exposure under these arrangements is unknown.

8.

Share repurchase

The

Company may from time to time purchase its common shares at a discount to NAV on the open market in such amounts and at such prices

as the Company may deem advisable.

The

Company had 19,289,905 shares outstanding as of November 30, 2023. There were no repurchases during the years ended November 30,

2023 and 2022.

9.

Subsequent events

In

accordance with U.S. GAAP provisions, management has evaluated the possibility of subsequent events existing in the Company’s

financial statements through the date the financial statements were issued.

On

December 31, 2023, the Company’s Board unanimously adopted a limited-duration shareholder rights plan (“Rights Plan”)

to protect the interests of the Company and all of its shareholders. The Rights Plan is currently effective and will expire on

April 29, 2024. The limited-duration Rights Plan was adopted in response to the rapid and significant accumulation of Company

shares by Saba Capital Management, LP (“Saba”), and is intended to prevent Saba’s unilateral attempt to obtain

creeping control of the Company, which the Board believes would undermine the Company’s strategic focus on long-term capital

appreciation in the global gold mining industry. Saba has advised the Company that it intends to nominate a control slate of directors

for election to the Board at the Company’s 2024 annual meeting of shareholders.

The

Rights Plan is designed to enable the Company’s shareholders to realize the long-term value of their investment, provide

an opportunity for all shareholders to receive fair and equal treatment in the event of any proposed takeover of the Company and

guard against tactics to gain control of the Company without paying all shareholders, what the Board considers to be an appropriate

premium for that control. The Company will issue one right for each common share of the Company outstanding as of the close of

business on January 12, 2024. The rights will initially trade with the Company’s common shares and will become exercisable

only if a person acquires 15% or more of the Company’s outstanding common shares. Any shareholders with beneficial ownership

of 15% or more of the Company’s outstanding common shares (including Saba) prior to the adoption of the Rights Plan are

grandfathered at their beneficial ownership levels at the date the Rights Plan was adopted, but are not permitted to acquire additional

common shares representing 0.25% or more of the outstanding common shares without triggering the Rights Plan.

Pursuant

to the Rights Plan, should it be triggered, the Board may decide that each holder of a right (other than the acquiring person,

whose rights will have become void and will not be exercisable) will be entitled to purchase, for a purchase price of $1.00 per

share, one common share of the company. Alternatively, (on a cashless basis) each outstanding right (other than the rights held

by the acquiring person, whose rights will have become void) will be exchanged for one common share. Further details about the

Rights Plan are contained in a Form 8-K and Form 8-A filed by the Company with the U.S. Securities and Exchange Commission.

Financial

Highlights

| | |

| |

For

the Years Ended November 30, | |

|

| Per share

operating performance(1) | |

2023 |

| |

2022 |

| |

2021 |

| |

2020 |

| |

2019 |

|

| Net

asset value, beginning of year | |

$16.88 | | |

$24.98 | | |

$24.05 | | |

$14.82 | | |

$10.10 | |

| Net

investment loss | |

(0.06 | ) | |

(0.07 | ) | |

(0.09 | ) | |

(0.13 | ) | |

(0.06 | ) |

| Net

realized gain (loss) from investments | |

0.46 | | |

1.40 | | |

1.37 | | |

1.83 | | |

0.09 | |

| Net

realized gain (loss) from foreign currency transactions | |

0.01 | | |

(0.01 | ) | |

(0.01 | ) | |

0.05 | | |

(0.06 | ) |

| Net

increase (decrease) in unrealized appreciation on investments | |

0.09 | | |

(9.40 | ) | |

(0.32 | ) | |

7.50 | | |

4.77 | |

| Net

unrealized gain on translation of assets and liabilities in foreign currency | |

0.00 | | |

0.00 | | |

0.00 | | |

0.00 | | |

0.00 | |

| Net

increase (decrease) in net assets resulting from operations | |

0.50 | | |

(8.08 | ) | |

0.95 | | |

9.25 | | |

4.74 | |

| Dividends | |

| | |

| | |

| | |

| | |

| |

| From

net investment income | |

— | | |

— | | |

— | | |

(0.02 | ) | |

(0.02 | ) |

| From

net realized gain on investments | |

(0.02 | ) | |

(0.02 | ) | |

(0.02 | ) | |

— | | |

— | |

| Net

asset value, end of year | |

$17.36 | | |

$16.88 | | |

$24.98 | | |

$24.05 | | |

$14.82 | |

| Market

value per share, end of year | |

$15.31 | | |

$14.26 | | |

$20.70 | | |

$19.91 | | |

$12.20 | |

| | |

| | |

| | |

| | |

| | |

| |

| Total

investment return | |

| | |

| | |

| | |

| | |

| |

| Based

on market price (2) | |

7.51 | % | |

(31.02 | )% | |

4.06 | % | |

63.38 | % | |

41.14 | % |

| Based

on net asset value (3) | |

2.98 | % | |

(32.34 | )% | |

3.96 | % | |

62.46 | % | |

47.01 | % |

| | |

| | |

| | |

| | |

| | |

| |

| Ratio

of average net assets | |

| | |

| | |

| | |

| | |

| |

| Expenses | |

1.05 | % | |

1.00 | % | |

0.94 | % | |

1.02 | % | |

1.38 | % |

| Net

expenses (4) | |

1.02 | % | |

1.00 | % | |

0.91 | % | |

1.02 | % | |

1.38 | % |

| Net

investment loss | |

(0.32 | )% | |

(0.36 | )% | |

(0.35 | )% | |

(0.67 | )% | |

(0.44 | )% |

| | |

| | |

| | |

| | |

| | |

| |

| Supplemental

data | |

| | |

| | |

| | |

| | |

| |

| Net

assets, end of year (000 omitted) | |

$334,912 | | |

$325,573 | | |

$481,898 | | |

$463,936 | | |

$285,879 | |

| Portfolio

turnover rate | |

10 | % | |

13 | % | |

17 | % | |

31 | % | |

45 | % |

| Shares

outstanding (000 omitted) | |

19,290 | | |

19,290 | | |

19,290 | | |

19,290 | | |

19,290 | |

| (1) | Per

share amounts from operations have been calculated using the average shares method. |

| (2) | Total

investment return is calculated assuming a purchase of shares at the current market price

at close the day before and a sale at the current market price on the last day of each

period reported. Dividends are assumed, for purposes of this calculation, to be reinvested

at prices obtained under the Company’s dividend reinvestment plan. |

| (3) | Total

investment return is calculated assuming a purchase of shares at the current net asset

value at close the day before and a sale at the current net asset value on the last day

of each period reported. Dividends are assumed, for purposes of this calculation, to

be reinvested at prices obtained under the Company’s dividend reinvestment plan. |

| (4) | Reflects

the expense ratio excluding any waivers and the change in retirement benefits due to

retired directors. |

Certain

Tax Information for U.S. Shareholders (Unaudited)

The