UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16 UNDER

THE SECURITIES EXCHANGE ACT OF 1934

For the month of August, 2024

Commission File Number: 001-38049

Azul S.A.

(Name of Registrant)

Edifício Jatobá, 8th floor, Castelo Branco Office Park

Avenida Marcos Penteado de Ulhôa Rodrigues, 939

Tamboré, Barueri, São Paulo, SP 06460-040, Brazil.

+55 (11) 4831 2880

(Address of Principal Executive Office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F x Form 40-F ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes ¨ No x

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes ¨ No x

| Second Quarter Results 2024 |

| | |

Azul Reports 2Q Results

with EBITDA of R$1.1 billion

São Paulo, August 12, 2024 –

Azul S.A., “Azul” (B3:AZUL4, NYSE:AZUL), the largest airline in Brazil by number of cities and departures, announces today

its results for the second quarter of 2024 (“2Q24”). The following financial information, unless stated otherwise, is presented

in Brazilian reais and in accordance with International Financial Reporting Standards (IFRS).

Financial and Operating Highlights

| § | EBITDA reached R$1.1

billion, with a margin of 25.2%, and operating income of R$441.2 million, representing a 10.6% margin. |

| § | Operating revenue reached R$4.2 billion, down 2.3% compared to 2Q23, mainly due the impact of the Rio Grande do Sul floods in May and

the temporary reduction in our international capacity, which fell 8.0% year over year. Without these impacts, we estimate that our top-line

revenues would have been above 2Q23. |

| § | CASK in 2Q24 was R$34.18 cents, a reduction of 1.8% compared to 2Q23, as a result of our moreoperational efficient operationgains and

the higher utilization of our next-generation aircraft, partially offset by the 5.3% average depreciation of the Brazilian real against

the US dollar, 1.4% higher fuel prices, and a 4.2% inflation over the last 12 months. |

| § | Passenger traffic (RPK) increased

3.9% over a capacity increase of 3.4%, resulting in a load factor of 80.3%. |

| 2Q24 Highlights |

2Q24 |

2Q23¹ |

Change |

1H24 |

1H23¹ |

Change |

| Total operating revenue (R$ million) |

4,172.7 |

4,269.4 |

-2.3% |

8,851.2 |

8,747.7 |

1.2% |

| Operating income (R$ million) |

441.2 |

591.9 |

(150.7) |

1,241.9 |

1,054.3 |

187.6 |

| Operating margin (%) |

10.6% |

13.9% |

-3.3 p.p. |

14.0% |

12.1% |

+2.0 p.p. |

| EBITDA (R$ million) |

1,052.6 |

1,156.9 |

(104.3) |

2,467.8 |

2,186.9 |

280.9 |

| EBITDA margin (%) |

25.2% |

27.1% |

-1.9 p.p. |

27.9% |

25.0% |

+2.9 p.p. |

| ASK (million) |

10,918 |

10,563 |

3.4% |

21,996 |

21,362 |

3.0% |

| RASK (R$ cents) |

38.22 |

40.42 |

-5.4% |

40.24 |

40.95 |

-1.7% |

| PRASK (R$ cents) |

35.34 |

37.38 |

-5.4% |

37.35 |

38.00 |

-1.7% |

| Yield (R$ cents) |

44.03 |

46.81 |

-5.9% |

46.93 |

47.66 |

-1.5% |

| CASK (R$ cents) |

34.18 |

34.81 |

-1.8% |

34.59 |

36.01 |

-3.9% |

| Fuel cost per liter (R$) |

4.35 |

4.30 |

1.4% |

4.30 |

4.78 |

-10.0% |

¹ 2Q23 and 1H23 operating results were adjusted

for non-recurring items.

| § | Immediate liquidity was R$2.5

billion, 23.7% higher compared to 2Q23, representing 13.4% of the last twelve months’ revenues. In the quarter, we continued to

deleverage and paid down over R$1.5 billion in current and deferred leases and debt amortizations. |

| § | Azul’s leverage ratio measured

as net debt to LTM EBITDA was 4.5x, solely due to the 11.7% end of period depreciation of the Brazilian real against the US dollar in

the quarter, which impacted our dollar-denominated debt. Considering an end-of-period exchange rate of R$5.00, Azul’s leverage ratio

would have been 3.75x, flat compared to 1Q24. |

| § | Booking trends in the

third quarter have been very encouraging, with an acceleration in corporate demand, leading to an increase in fares. We expect this trend

to accelerate into the second half of the year, our strongest period seasonally. |

| | Second Quarter Results 2024 |

| | |

Management Comments

First, I wish to express solidarity with Voepass

and everyone involved in the tragedy that occurred last Friday. We offer them our condolences and support during this difficult time.

I would also like to thank our Crewmembers

for all their passion and dedication during 2Q24. Our strong culture has been essential as we successfully navigated the quarter and some

of its challenges.

In May, the state of Rio Grande do Sul was

impacted by severe flooding. We were deeply saddened by the loss of lives, displacement of people, and widespread destruction in the region.

Once again, our Crewmembers and Clients stepped up, contributing over 3,000 tons in donations, which we delivered safely and swiftly to

those who needed them most. Also, Porto Alegre airport was forced to close, with a partial reopening expected for October. Rio Grande

do Sul is the fourth largest state in the country in terms of economic activity and represents over 10% of our total capacity. We estimate

that the operational reduction in that region negatively impacted our 2Q24 results by at least R$200 million.

The quick

devaluation of the Brazilian real also impacted our 2Q24 results. End of period exchange rate was 11.7% weaker

in the quarter, at the same time that fuel prices increased 2.4%. Finally, our 2Q24 revenues were

also affected by a temporary reduction in our international capacity, which fell 8.0% year over year in this period. Even with all of

these headwinds, we continued to generate strong operational results, with EBITDA reaching R$1.1 billion. Our EBITDA margin of 25.2% is

one of the highest in the industry.

Azul operates in a dynamic, high-growth environment

with often fast-changing conditions. Azul’s continued success is explained in large part by its the ability to evolve and adapt.

We launched Azul 15 years ago with a single fleet type model, aiming to serve regional destinations within Brazil. We soon identified

that the opportunity was bigger than expected and over time incorporated other aircraft types into our operation. We then merged with

TRIP, which allowed us to build by far the largest network in the country. We expanded into international markets, bringing Brazilians

to destinations in three different continents. Most recently, our response to the pandemic and an amicable approach to negotiating with

all stakeholders was another example of our capacity to innovate.

Throughout that time, we have stayed true

to our core strengths, anchored by an exclusive network, exceptional Crewmembers, and an efficient operation, generating a solid track

record of high growth and sustainable results.

In 2Q24, we continued building upon last year’s

successful capital optimization plan, moving on to the next step of unlocking all the value available to Azul. We have developed and started

implementing a plan, called “Elevate”, with multiple opportunities to increase revenue and reduce costs, once again allowing

Azul to adapt and continue expanding profitability and cash generation.

Our fleet transformation plan remains on track,

generating a reduction of 2.0% year over year in our fuel consumption per ASK. In the second quarter, we received 2 Airbus A320s, 2 Airbus

A330neo and 1 Embraer E2, with more to come in the upcoming months.

We are proud of the performance of our business

units, which accounted for over 20% of our RASK and around 30% of our EBITDA. Azul Fidelidade performance remained strong, with an all-time

record in members, gross billings, and active co-branded credit cards. Azul Viagens, our vacations business, grew 63% in gross bookings

2Q24 versus 2Q23. Our logistics business remained strong, with revenue growing quarter over quarter, even with the impact of the Rio Grande

do Sul floods on our operations.

We maintained a liquidity position of R$2.5

billion, 13% of our last twelve months’ revenue. Including long-term investments and receivables, security deposits and reserves,

our total liquidity was R$6.4 billion.

As we enter the seasonally strong spring and summer periods in Brazil,

with additional next-generation aircraft entering our fleet, we remain optimistic about the future. Bookings have been improving over

the last four weeks, and we expect this trend to accelerate. Our commitment remains steadfast in delivering outstanding value to our customers,

shareholders, and Crewmembers.

John Rodgerson, CEO of Azul S.A.

| | Second Quarter Results 2024 |

| | |

Consolidated Financial Results

The following income statement and operating data should

be read in conjunction with the quarterly results comments presented below:

| Income statement (R$ million) |

2Q24 |

2Q23¹ |

% Δ |

1H24 |

1H23¹ |

% ∆ |

| Operating Revenue |

|

|

|

|

|

|

| Passenger revenue |

3,859.1 |

3,948.5 |

-2.3% |

8,216.1 |

8,118.4 |

1.2% |

| Cargo revenue and other |

313.7 |

320.9 |

-2.2% |

635.1 |

629.3 |

0.9% |

| Total operating revenue |

4,172.7 |

4,269.4 |

-2.3% |

8,851.2 |

8,747.7 |

1.2% |

| Operating Expenses |

|

|

|

|

|

|

| Aircraft fuel |

(1,373.6) |

(1,338.2) |

2.6% |

(2,726.9) |

(3,011.6) |

-9.5% |

| Salaries and benefits |

(655.9) |

(568.5) |

15.4% |

(1,330.6) |

(1,105.9) |

20.3% |

| Depreciation and amortization |

(611.4) |

(565.0) |

8.2% |

(1,225.9) |

(1,132.6) |

8.2% |

| Airport fees |

(239.6) |

(247.0) |

-3.0% |

(481.8) |

(509.4) |

-5.4% |

| Traffic and customer servicing |

(207.2) |

(189.5) |

9.3% |

(414.7) |

(385.1) |

7.7% |

| Sales and marketing |

(191.5) |

(179.8) |

6.5% |

(393.4) |

(353.8) |

11.2% |

| Maintenance and repairs |

(170.7) |

(200.3) |

-14.8% |

(368.4) |

(358.2) |

2.8% |

| Other |

(281.7) |

(389.2) |

-27.6% |

(667.5) |

(836.7) |

-20.2% |

| Total Operating Expenses |

(3,731.6) |

(3,677.5) |

1.5% |

(7,609.2) |

(7,693.4) |

-1.1% |

| Operating Result |

441.2 |

591.9 |

-25.5% |

1,241.9 |

1,054.3 |

17.8% |

| Operating margin |

10.6% |

13.9% |

-3.3 p.p. |

14.0% |

12.1% |

+2.0 p.p. |

| EBITDA |

1,052.6 |

1,156.9 |

-9.0% |

2,467.8 |

2,186.9 |

12.8% |

| EBITDA margin |

25.2% |

27.1% |

-1.9 p.p. |

27.9% |

25.0% |

+2.9 p.p. |

| Financial Result |

|

|

|

|

|

|

| Financial income |

51.0 |

51.0 |

0.0% |

95.9 |

104.5 |

-8.2% |

| Financial expenses² |

(1,268.3) |

(1,135.0) |

11.7% |

(2,430.2) |

(2,330.6) |

4.3% |

| Derivative financial instruments, net² |

(37.1) |

(46.8) |

-20.8% |

1.3 |

(240.8) |

n.a. |

| Foreign currency exchange, net |

(3,085.0) |

1,036.8 |

n.a. |

(3,932.3) |

1,588.3 |

n.a. |

| Result Before Income Taxes |

(3,898.2) |

497.9 |

n.a. |

(5,023.4) |

175.7 |

n.a. |

| Income tax and social contribution |

(0.3) |

- |

n.a. |

(0.3) |

- |

n.a. |

| Deferred income tax and social contribution |

32.7 |

- |

n.a. |

39.5 |

- |

n.a. |

| Net Result² |

(3,865.7) |

497.9 |

n.a. |

(4,984.1) |

175.7 |

n.a. |

| Net margin |

-92.6% |

11.7% |

n.a. |

-56.3% |

2.0% |

n.a. |

| Adjusted Net Result² ³ |

(744.4) |

(566.8) |

31.3% |

(1,068.6) |

(1,294.4) |

-17.4% |

| Adjusted net margin² ³ |

-17.8% |

-13.3% |

-4.6 p.p. |

-12.1% |

-14.8% |

+2.7 p.p. |

| Shares outstanding⁴ |

347.4 |

347.5 |

0.0% |

347.4 |

347.4 |

0.0% |

| EPS |

(11.13) |

1.43 |

n.a. |

(14.35) |

0.51 |

n.a. |

| EPS (US$) |

(2.14) |

0.29 |

n.a. |

(2.82) |

0.10 |

n.a. |

| EPADR (US$) |

(6.41) |

0.87 |

n.a. |

(8.47) |

0.30 |

n.a. |

| Adjusted EPS³ |

(2.14) |

(1.63) |

31.4% |

(3.08) |

(3.73) |

-17.5% |

| Adjusted EPS³ (US$) |

(0.41) |

(0.33) |

24.8% |

(0.61) |

(0.73) |

-17.6% |

| Adjusted EPADR³ (US$) |

(1.23) |

(0.99) |

24.8% |

(1.82) |

(2.20) |

-17.6% |

¹ 2Q23 and 1H23 operating results were adjusted

for non-recurring items.

² Excludes conversion rights related to convertible

debentures.

³ Adjusted for unrealized derivative results and

foreign currency. One ADR equals three preferred shares (PNs).

⁴ Shares outstanding do not include dilution

related to convertible and equity instruments.

| | Second Quarter Results 2024 |

| | |

| Operating Data |

2Q24 |

2Q23¹ |

% Δ |

1H24 |

1H23¹ |

% ∆ |

| ASK (million) |

10,918 |

10,563 |

3.4% |

21,996 |

21,362 |

3.0% |

| Domestic |

8,820 |

8,282 |

6.5% |

17,839 |

16,787 |

6.3% |

| International |

2,098 |

2,281 |

-8.0% |

4,156 |

4,575 |

-9.2% |

| RPK (million) |

8,764 |

8,435 |

3.9% |

17,506 |

17,033 |

2.8% |

| Domestic |

6,927 |

6,490 |

6.7% |

13,955 |

13,193 |

5.8% |

| International |

1,838 |

1,945 |

-5.5% |

3,551 |

3,840 |

-7.5% |

| Load factor (%) |

80.3% |

79.9% |

+0.4 p.p. |

79.6% |

79.7% |

-0.1 p.p. |

| Domestic |

78.5% |

78.4% |

+0.2 p.p. |

78.2% |

78.6% |

-0.4 p.p. |

| International |

87.6% |

85.3% |

+2.3 p.p. |

85.4% |

83.9% |

+1.5 p.p. |

| Average fare (R$) |

521.2 |

550.1 |

-5.2% |

562.3 |

570.3 |

-1.4% |

| Passengers (thousands) |

7,404 |

7,178 |

3.1% |

14,613 |

14,236 |

2.6% |

| Block hours |

136,586 |

133,590 |

2.2% |

274,044 |

271,292 |

1.0% |

| Aircraft utilization (hours per day)² |

11.3 |

9.5 |

19.2% |

11.4 |

9.7 |

18.0% |

| Departures |

79,394 |

77,867 |

2.0% |

157,929 |

156,606 |

0.8% |

| Average stage length (km) |

1,143 |

1,131 |

1.0% |

1,152 |

1,146 |

0.5% |

| End of period operating passenger aircraft |

182 |

181 |

0.6% |

182 |

181 |

0.6% |

| Fuel consumption (thousands of liters) |

315,424 |

311,482 |

1.3% |

633,725 |

629,943 |

0.6% |

| Fuel consumption per ASK |

28.9 |

29.5 |

-2.0% |

28.8 |

29.5 |

-2.3% |

| Full-time-equivalent employees |

15,763 |

14,007 |

12.5% |

15,763 |

14,007 |

12.5% |

| End of period FTE per aircraft |

87 |

77 |

11.9% |

87 |

77 |

11.9% |

| Yield (R$ cents) |

44.03 |

46.81 |

-5.9% |

46.93 |

47.66 |

-1.5% |

| RASK (R$ cents) |

38.22 |

40.42 |

-5.4% |

40.24 |

40.95 |

-1.7% |

| PRASK (R$ cents) |

35.34 |

37.38 |

-5.4% |

37.35 |

38.00 |

-1.7% |

| CASK (R$ cents) |

34.18 |

34.81 |

-1.8% |

34.59 |

36.01 |

-3.9% |

| CASK ex-fuel (R$ cents) |

21.60 |

22.15 |

-2.5% |

22.20 |

21.92 |

1.3% |

| Fuel cost per liter (R$) |

4.35 |

4.30 |

1.4% |

4.30 |

4.78 |

-10.0% |

| Break-even load factor (%) |

71.8% |

68.8% |

+3.0 p.p. |

68.4% |

70.1% |

-1.7 p.p. |

| Average exchange rate (R$ per US$) |

5.21 |

4.95 |

5.3% |

5.08 |

5.07 |

0.2% |

| End of period exchange rate |

5.56 |

4.82 |

15.3% |

5.56 |

4.82 |

15.3% |

| Inflation (IPCA/LTM) |

4.23% |

4.96% |

-0.7 p.p. |

4.23% |

4.96% |

-0.7 p.p. |

| WTI (average per barrel, US$) |

80.01 |

71.84 |

11.4% |

79.55 |

74.52 |

6.8% |

| Heating oil (US$ per gallon) |

2.51 |

2.44 |

2.7% |

2.61 |

2.68 |

-2.7% |

¹ 2Q23 and 1H23 operating results were adjusted

for non-recurring items.

² Excludes Cessna aircraft and freighters.

Operating Revenue

In 2Q24,

Azul recorded total operating revenues of R$4.2 billion, 2.3% or R$96.7 million lower than

2Q23 mainly due the impact of the Rio Grande do Sul floods on our operation and the temporary

reduction in our international capacity, which fell 8.0% year over year. Without these impacts, we estimate that our top-line revenues

would have been above 2Q23.

Cargo revenue and other totaled R$313.7million,

2.2% lower than 2Q23, also impacted by the reduction in our domestic capacity in Rio Grande do Sul state, and the temporary reduction

in international capacity. In 2Q24, Cargo revenue increased 11.9% compared to 1Q24.

| | Second Quarter Results 2024 |

| | |

| R$ cents |

2Q24 |

2Q23¹ |

% Δ |

1H24 |

1H23¹ |

% Δ |

| Operating revenue per ASK |

|

|

|

|

|

|

| Passenger revenue |

35.34 |

37.38 |

-5.4% |

37.35 |

38.00 |

-1.7% |

| Cargo revenue and other |

2.87 |

3.04 |

-5.4% |

2.89 |

2.95 |

-2.0% |

| Operating revenue (RASK) |

38.22 |

40.42 |

-5.4% |

40.24 |

40.95 |

-1.7% |

| Operating expenses per ASK |

|

|

|

|

|

|

| Aircraft fuel |

(12.58) |

(12.67) |

-0.7% |

(12.40) |

(14.10) |

-12.1% |

| Salaries and benefits |

(6.01) |

(5.38) |

11.6% |

(6.05) |

(5.18) |

16.8% |

| Depreciation and amortization |

(5.60) |

(5.35) |

4.7% |

(5.57) |

(5.30) |

5.1% |

| Airport fees |

(2.19) |

(2.34) |

-6.2% |

(2.19) |

(2.38) |

-8.1% |

| Traffic and customer servicing |

(1.90) |

(1.79) |

5.8% |

(1.89) |

(1.80) |

4.6% |

| Sales and marketing |

(1.75) |

(1.70) |

3.0% |

(1.79) |

(1.66) |

8.0% |

| Maintenance and repairs |

(1.56) |

(1.90) |

-17.5% |

(1.67) |

(1.68) |

-0.1% |

| Other operating expenses |

(2.58) |

(3.68) |

-30.0% |

(3.03) |

(3.92) |

-22.5% |

| Total operating expenses (CASK) |

(34.18) |

(34.81) |

-1.8% |

(34.59) |

(36.01) |

-3.9% |

| Operating income per ASK (RASK-CASK) |

4.04 |

5.60 |

-27.9% |

5.65 |

4.94 |

14.4% |

¹ 2Q23 and 1H23 operating results were adjusted

for non-recurring items.

Operating Expenses

In 2Q24, operating expenses were R$3.7 billion,

1.5% higher than 2Q23 mainly explained by the 3.4% increase in total capacity, 5.3% depreciation of the Brazilian real against the US

dollar and 1.4% increase in fuel price, partially offset by higher productivity and cost-reduction initiatives.

The breakdown of our main operating expenses

compared to 2Q23 is as follows:

| § | Aircraft fuel increased

2.6% to R$1,373.6 million mostly due to a 3.4% increase in total capacity, a 1.4% increase in fuel price per liter (excluding hedges),

partially offset by a reduction of 2.0% in fuel burn per ASK as a result of the higher utilization of our next-generation fleet. |

| § | Salaries and benefits

increased R$87.5 million compared to 2Q23, mainly driven by our capacity increase of 3.4%, a 5.5% union increase in salaries as a result

of collective bargaining agreements with unions applicable to all airline employees in Brazil, the insourcing of certain activities to

reduce total costs, and hirings made in 4Q23 to reduce ground time and support our upcoming growth. |

| § | Depreciation and amortization

increased 8.2% or R$46.4 million, driven by the increase in the right-of-use asset as a result of lease contract renegotiations with lessors

and the 5.3% depreciation of the Brazilian real against the US dollar. |

| § | Airport fees reduced 3.0%

or R$7.4 million, mostly driven by an 8.0% reduction in international capacity, partially offset by a 6.5% increase in our domestic capacity.

|

| § | Traffic and customer servicing

increased 9.3% or R$17.7 million, primarily due to the 3.1% growth in passengers and the 4.2% inflation in the period. |

| § | Sales and marketing increased

6.5% or R$11.7 million, mostly driven by higher advertising campaigns during the Olympic Games and regional events, partially offset by

the 2.3% reduction in our passenger revenue, leading to a reduction in credit card fees and commissions. |

| § | Maintenance and repairs

reduced R$29.6 million compared to 2Q23, mainly due to savings from insourcing of maintenance events and renegotiations with suppliers,

partially offset by the 5.3% depreciation of the Brazilian real against the US dollar. |

| § | Other reduced R$107.5

million, mainly due to cost-reduction initiatives and lower number of judicial claims in the period, partially offset by the 5.3% depreciation

of the Brazilian real against the US dollar.

|

| | Second Quarter Results 2024 |

| | |

Non-Operating Results

| Net financial results (R$ million)¹ |

2Q24 |

2Q23 |

% Δ |

1H24 |

1H23 |

% ∆ |

| Net financial expenses |

(1,217.3) |

(1,084.0) |

12.3% |

(2,334.3) |

(2,226.2) |

4.9% |

| Derivative financial instruments, net |

(37.1) |

(46.8) |

-20.8% |

1.3 |

(240.8) |

n.a. |

| Foreign currency exchange, net |

(3,085.0) |

1,036.8 |

n.a. |

(3,932.3) |

1,588.3 |

n.a. |

| Net financial results |

(4,339.4) |

(94.0) |

4515.8% |

(6,265.3) |

(878.6) |

613.1% |

¹ Excludes the conversion right related to the

convertible debentures.

Net financial expenses were

R$1,217.3 million in the quarter, with R$596.1 million in leases recognized as interest expense and R$345.3 million in interest on

loans and financing in 2Q24.

Derivative

financial instruments resulted in a net loss of R$37.1 million in 2Q24 mostly due to fuel hedge

losses recorded during the period. As of June 30, 2024, Azul had hedged approximately 15.1% of

its expected fuel consumption for the next twelve months by using forward contracts and options.

Foreign

currency exchange, net registered a net loss of R$3,085.0 million in 2Q24 due to the 11.7%

end of period depreciation of the Brazilian real against the US dollar, resulting in an increase in lease liabilities and loans denominated

in foreign currency.

Liquidity and Financing

Azul ended

the second quarter with total liquidity of R$6.4 billion including short and long-term investments, accounts receivable, security deposits

and maintenance. Immediate liquidity as of June 30, 2024 was R$2.5 billion representing 13.4% of our LTM revenues, after we paid down

over R$1.5 billion in debt amortization and leases.

Immediate liquidity was 23.7% higher than

2Q23, as a result of the capital optimization plan implemented last year. In that plan, we also created additional cash-raising capacity

secured by Azul Cargo, which remains available for us to raise first-out debt as we continually evaluate opportunities to manage our debt

maturity profile and liquidity position.

| Liquidity (R$ million) |

2Q24 |

1Q24 |

% Δ |

2Q23 |

% Δ |

| Cash, cash equivalents and short-term investments |

1,475.5 |

1,337.6 |

10.3% |

616.2 |

139.4% |

| Accounts receivable |

1,042.3 |

1,376.3 |

-24.3% |

1,418.8 |

-26.5% |

| Immediate liquidity |

2,517.8 |

2,713.9 |

-7.2% |

2,035.0 |

23.7% |

| Cash as % of LTM revenue |

13.4% |

14.4% |

-1.0 p.p. |

11.6% |

+1.8 p.p. |

| Long-term investments and receivables |

961.9 |

805.1 |

19.5% |

814.6 |

18.1% |

| Security deposits and maintenance reserves |

2,899.0 |

2,470.0 |

17.4% |

2,617.3 |

10.8% |

| Total Liquidity |

6,378.7 |

5,989.0 |

6.5% |

5,466.9 |

16.7% |

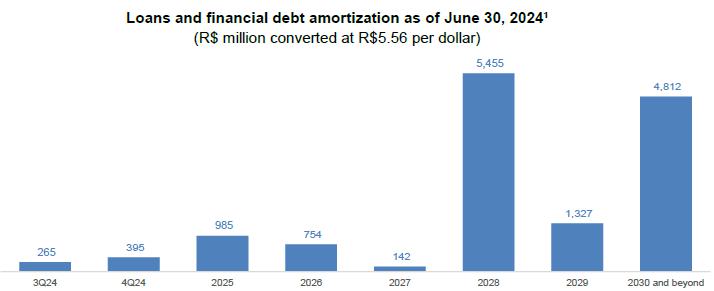

Azul’s debt

amortization schedule as of June 30, 2024 is presented below. The chart converts our dollar-denominated debt to reais using the quarter-end

foreign exchange rate of R$5.56.

| | Second Quarter Results 2024 |

| | |

¹Excludes convertible

debentures, equity instruments and OEMs’ notes.

Compared to 1Q24, gross debt increased R$3,722.6 million to R$28,106.7

million, mostly due to the 11.7% end of period depreciation of the Brazilian real against the US dollar in the quarter, resulting in an

increase in lease liabilities and loans denominated in foreign currency, in addition to the issuance of local debentures, partially offset

by our continued deleveraging process with R$1.5 billion in payments of current and deferred leases and debt amortizations during the

quarter. As of June 30, 2024, Azul’s average debt maturity excluding lease liabilities and convertible debentures was 4.1 years,

with an average interest rate of 11.0%. Average interest rate on local and dollar-denominated obligations were equivalent to CDI + 4%

and 10.5%, respectively.

| Loans and financing (R$ million)¹ |

2Q24 |

1Q24 |

% Δ |

2Q23 |

% Δ |

| Lease liabilities |

13,591.5 |

11,537.0 |

17.8% |

12,885.2 |

5.5% |

| Lease notes |

1,203.9 |

1,072.6 |

12.2% |

- |

n.a. |

| Finance lease liabilities |

716.0 |

644.7 |

11.1% |

589.5 |

21.5% |

| Other aircraft loans and financing |

525.1 |

347.7 |

51.0% |

664.3 |

-21.0% |

| Loans and financing |

12,068.7 |

10,782.1 |

11.9% |

6,429.8 |

87.7% |

| % of non-aircraft debt in local currency |

13% |

13% |

+0.4 p.p. |

25% |

-11.9 p.p. |

| % of total debt in local currency |

6% |

6% |

-0.1 p.p. |

8% |

-2.1 p.p. |

| Gross debt |

28,105.2 |

24,384.1 |

15.3% |

20,568.8 |

36.6% |

¹Considers the effect of hedges on debt.

Excludes convertible debentures, equity instruments and OEM notes. Consistently, shares outstanding should be adjusted to 513.3 million.

Azul’s leverage ratio measured as net debt to LTM EBITDA was

4.5x, mainly due to the 11.7% end of period depreciation of the Brazilian real against the US dollar in the quarter, which impacted our

dollar-denominated debt. Considering the end-of-period exchange rate of R$5.00, Azul’s leverage ratio would have been 3.75x, stable

compared to 1Q24.

| Key financial ratios (R$ million) |

2Q24 |

1Q24 |

% Δ |

2Q23 |

% Δ |

| Cash¹ |

3,479.7 |

3,519.0 |

-1.1% |

2,849.6 |

22.1% |

| Gross debt² |

28,106.7 |

24,384.1 |

15.3% |

20,568.8 |

36.6% |

| Net debt |

24,627.0 |

20,865.1 |

18.0% |

17,719.2 |

39.0% |

| Net debt / EBITDA (LTM) |

4.5x |

3.7x |

0.8x |

4.2x |

0.3x |

¹ Includes cash, cash equivalents, receivables, short and long-term

investments.

² Excludes convertible debentures, equity instruments and OEM notes.

| | Second Quarter Results 2024 |

| | |

Fleet and Capex Expenditures

As of June 30, 2024, Azul had a passenger

operating fleet of 182 aircraft and a passenger contractual fleet of 183 aircraft, with an average aircraft age of 7.2 years excluding

Cessna aircraft. At the end of 2Q24, the aircraft not included in our operating passenger fleet consisted of one Embraer E1 subleased

to Breeze.

Azul ended 2Q24 with approximately 83% of

its capacity coming from next-generation aircraft, considerably higher than any competitor in the region.

| Passenger Contractual Fleet¹ |

2Q24 |

1Q24 |

% Δ |

2Q23 |

% Δ |

| Airbus widebody |

11 |

9 |

22.2% |

12 |

-8.3% |

| Airbus narrowbody |

57 |

55 |

3.6% |

54 |

5.6% |

| Embraer E2 |

21 |

20 |

5.0% |

17 |

23.5% |

| Embraer E1 |

34 |

39 |

-12.8% |

47 |

-27.7% |

| ATR |

36 |

36 |

- |

42 |

-14.3% |

| Cessna |

24 |

24 |

- |

24 |

- |

| Total¹ |

183 |

183 |

- |

196 |

-6.6% |

| Aircraft under operating leases |

163 |

157 |

3.8% |

169 |

-3.6% |

1 Includes 1 subleased aircraft.

| Passenger Operating Fleet |

2Q24 |

1Q24 |

% Δ |

2Q23 |

% Δ |

| Airbus widebody |

11 |

9 |

22.2% |

11 |

- |

| Airbus narrowbody |

57 |

55 |

3.6% |

54 |

5.6% |

| Embraer E2 |

21 |

20 |

5.0% |

17 |

23.5% |

| Embraer E1 |

33 |

37 |

-10.8% |

38 |

-13.2% |

| ATR |

36 |

36 |

- |

37 |

-2.7% |

| Cessna |

24 |

24 |

- |

24 |

- |

| Total |

182 |

181 |

0.6% |

181 |

0.6% |

Capex

Capital expenditures totaled R$305.5 million in 2Q24,

mostly due to the capitalization of engine overhaul events, the acquisition of spare parts and pre-delivery payments in the quarter.

| Capex (R$ million) |

2Q24 |

2Q23 |

% Δ |

1H24 |

1H23 |

% Δ |

| Aircraft and maintenance and checks |

81.7 |

138.3 |

-40.9% |

361.8 |

174.2 |

107.7% |

| Intangible assets |

49.6 |

52.3 |

-5.3% |

78.4 |

92.5 |

-15.3% |

| Pre-delivery payments |

155.1 |

15.3 |

916.6% |

276.8 |

15.3 |

1714.4% |

| Other |

19.1 |

16.0 |

19.8% |

34.7 |

21.7 |

60.2% |

| Capex |

305.5 |

221.8 |

37.7% |

751.7 |

303.6 |

147.6% |

| Sale and leaseback |

- |

- |

n.a. |

- 10.3 |

- |

n.a. |

| Net capex from sales and leaseback |

305.5 |

221.8 |

37.7% |

741.4 |

303.6 |

144.2% |

| | Second Quarter Results 2024 |

| | |

Environmental, Social and Governance (“ESG”)

Responsibility

The table below presents Azul’s key

ESG information according to the Sustainability Accounting Standards Board (SASB) standard for the airline industry:

| ESG Key Indicators |

2Q24 |

1Q24 |

% Δ |

| Environmental |

|

|

|

| Fuel |

|

|

|

| Total fuel consumed per ASK (GJ / ASK) |

1,085 |

1,079 |

0.5% |

| Total fuel consumed (GJ x 1000) |

11,849 |

11,957 |

-0.9% |

| Fleet |

|

|

|

| Average age of operating fleet¹ (years) |

7.2 |

7.4 |

-2.3% |

| Social |

|

|

|

| Labor Relations |

|

|

|

| Employee gender: male (%) |

59.4% |

59.2% |

0.2 p.p. |

| Employee gender: female (%) |

40.6% |

40.8% |

-0.2 p.p. |

| Employee monthly turnover (%) |

0.6% |

0.9% |

-0.4 p.p. |

| Employee covered under collective bargaining agreements (%) |

100% |

100% |

- |

| Volunteers (#) |

7,043 |

6,385 |

10.3% |

| Governance |

|

|

|

| Management |

|

|

|

| Independent directors (%) |

92% |

92% |

- |

| Percent of Board members that are women (%) |

25% |

25% |

- |

| Board of Directors' average age (years) |

59 |

58 |

0.4% |

| Director meeting attendance (%) |

100% |

100% |

- |

| Board size (#) |

12 |

12 |

- |

| Participation of women in leadership positions (%) |

38% |

38% |

- |

¹ Excludes Cessna aircraft.

| | Second Quarter Results 2024 |

| | |

Conference Call Details

Monday, August 12, 2024

11:00 a.m. (EDT) | 12:00 p.m. (Brasília time)

USA: +1 253 205-0468

Brazil: +55 11 4632-2237 or +55 21 3958-7888

Code: 834 3552 8043

Webcast: ri.voeazul.com.br/en/

About Azul

Azul S.A. (B3: AZUL4, NYSE: AZUL), the largest airline

in Brazil by number of flight departures and cities served, offers 1,000 daily flights to over 160 destinations. With an operating fleet

of over 180 aircraft and more than 15,000 Crewmembers, the Company has a network of 300 non-stop routes. Azul was named by Cirium (leading

aviation data analysis company) as the most on-time airline in the world in 2022, being the first Brazilian airline to obtain this honor.

In 2020 Azul was awarded best airline in the world by TripAdvisor, the first time a Brazilian flag carrier earned the number one ranking

in the Traveler’s Choice Awards. For more information visit ri.voeazul.com.br/en/.

Contact:

Investor Relations

Tel: +55 11 4831 2880

invest@voeazul.com.br

|

Media Relations

Tel: +55 11 4831 1245

imprensa@voeazul.com.br

|

| |

|

| | Second Quarter Results 2024 |

| | |

Balance Sheet – IFRS

| (R$ million) |

June 30, 2024 |

March 31, 2024 |

June 30, 2023 |

| Assets |

22.831,2 |

20.895,9 |

17.122,0 |

| Current assets |

4.954,5 |

4.863,2 |

4.628,3 |

| Cash and cash equivalents |

1.439,6 |

1.337,6 |

616,2 |

| Short-term investments |

35,9 |

- |

- |

| Accounts receivable |

1.034,0 |

1.361,2 |

1.351,2 |

| Sublease receivables |

8,3 |

15,1 |

67,6 |

| Inventories |

1.000,4 |

943,3 |

722,7 |

| Security deposits and maintenance reserves |

698,6 |

503,2 |

1.286,0 |

| Taxes recoverable |

218,4 |

205,3 |

188,0 |

| Derivative financial instruments |

4,3 |

20,8 |

29,5 |

| Prepaid expenses |

193,5 |

203,5 |

354,8 |

| Other current assets |

321,6 |

273,2 |

12,3 |

| Non-current assets |

17.876,7 |

16.032,7 |

12.493,7 |

| Long-term investments |

956,3 |

791,5 |

742,1 |

| Sublease receivables |

5,6 |

13,6 |

72,5 |

| Security deposits and maintenance reserves |

2.200,4 |

1.966,8 |

1.331,3 |

| Derivative financial instruments |

0,1 |

0,1 |

0,4 |

| Prepaid expenses |

- |

- |

188,5 |

| Other non-current assets |

530,9 |

311,2 |

8,4 |

| Right of use – leased aircraft and other assets |

8.855,3 |

7.933,9 |

6.040,2 |

| Right of use – maintenance of leased aircraft |

1.037,4 |

1.007,1 |

717,9 |

| Property and equipment |

2.787,1 |

2.529,3 |

1.924,6 |

| Intangible assets |

1.503,7 |

1.479,1 |

1.467,8 |

| Liabilities and equity |

22.831,2 |

20.895,9 |

17.122,0 |

| Current liabilities |

17.403,6 |

14.411,9 |

16.823,0 |

| Loans and financing |

1.495,2 |

1.245,7 |

1.694,5 |

| Convertible instruments |

29,0 |

63,2 |

12,9 |

| Leases |

3.642,2 |

3.108,4 |

4.641,3 |

| Lease notes |

139,3 |

125,2 |

- |

| Lease equity |

713,0 |

428,5 |

- |

| Accounts payable |

3.193,3 |

2.338,6 |

2.912,6 |

| Factoring |

45,5 |

117,3 |

- |

| Air traffic liability |

5.821,5 |

5.168,7 |

4.476,1 |

| Salaries and benefits |

533,2 |

490,3 |

474,4 |

| Insurance payable |

1,1 |

1,1 |

21,9 |

| Taxes payable |

161,8 |

132,7 |

129,5 |

| Derivative financial instruments |

35,5 |

15,6 |

120,5 |

| Provisions |

624,7 |

399,1 |

1.006,7 |

| Airport fees |

757,5 |

628,5 |

1.192,2 |

| Other |

210,9 |

148,8 |

140,5 |

| Non-current liabilities |

31.594,2 |

28.852,5 |

19.981,0 |

| Loans and financing |

11.098,6 |

9.884,1 |

5.399,6 |

| Convertible instruments |

972,0 |

1.070,3 |

1.641,5 |

| Leases |

10.666,9 |

9.073,3 |

8.833,4 |

| Lease notes |

1.064,6 |

947,4 |

- |

| Lease equity |

1.659,9 |

1.634,2 |

- |

| Accounts payable |

1.330,0 |

1.296,4 |

436,2 |

| Derivative financial instruments |

0,0 |

0,1 |

0,1 |

| Provision |

2.972,9 |

2.846,8 |

2.071,2 |

| Airport fees |

913,1 |

1.140,3 |

513,3 |

| Other non-current liabilities |

916,2 |

959,6 |

1.085,7 |

| Equity |

(26.166,6) |

(22.368,4) |

(19.682,0) |

| Issued capital |

2.315,6 |

2.315,6 |

2.314,0 |

| Advance for future capital increase |

- |

0,0 |

0,8 |

| Capital reserve |

2.053,3 |

2.041,8 |

2.010,4 |

| Treasury shares |

(11,6) |

(11,6) |

(13,1) |

| Accumulated other comprehensive result |

3,1 |

3,1 |

5,3 |

| Accumulated losses |

(30.527,0) |

(26.717,4) |

(23.999,4) |

| | Second Quarter Results 2024 |

| | |

Cash Flow

Statement – IFRS

| (R$

million) |

2Q24 |

2Q23 |

%

Δ |

1H24 |

1H23 |

%

Δ |

| Cash flows from operating activities |

|

|

|

|

|

|

| Net profit (loss)

for the period |

(3,809.6) |

23.9

|

n.a. |

(4,859.9) |

(712.7) |

581.9% |

| Total non-cash adjustments |

|

|

|

|

|

|

| Depreciation and

amortization |

611.4

|

627.2

|

-2.5% |

1,225.9

|

1,194.8

|

2.6% |

| Unrealized derivatives |

(168.5) |

235.6

|

n.a. |

(358.4) |

510.6

|

n.a. |

| Exchange gain and

(losses) in foreign currency |

3,145.0

|

(1,096.7) |

n.a. |

3,989.5

|

(1,680.0) |

n.a. |

| Financial income

and expenses, net |

1,250.4

|

1,243.2

|

0.6% |

2,414.8

|

2,219.1

|

8.8% |

| Provisions |

(35.1) |

36.5

|

n.a. |

33.8

|

134.1

|

-74.8% |

| Result from modification

of lease and provision |

(61.2) |

(27.6) |

121.8% |

(88.9) |

(50.0) |

77.8% |

| Other |

(317.0) |

38.9

|

n.a. |

(540.9) |

253.6

|

n.a. |

| Changes in operating assets and

liabilities |

|

|

|

|

|

|

| Trade and other

receivables |

454.6

|

83.5

|

444.6% |

248.0

|

522.8

|

-52.6% |

| Sublease receivables |

-

|

5.6

|

n.a. |

-

|

16.8

|

n.a. |

| Security deposits

and maintenance reserves |

(172.9) |

(131.4) |

31.6% |

(230.5) |

(121.9) |

89.1% |

| Advances to suppliers |

(316.9) |

(428.5) |

-26.0% |

(840.4) |

(924.7) |

-9.1% |

| Other assets |

(217.9) |

(23.9) |

812.7% |

(327.9) |

(70.4) |

366.1% |

| Derivatives |

(0.8) |

(74.7) |

-99.0% |

(15.4) |

(122.6) |

-87.4% |

| Accounts payable |

863.5 |

629.3 |

37.2% |

1,291.1 |

978.7 |

31.9% |

| Salaries and benefits |

80.1

|

(22.5) |

n.a. |

96.4

|

31.4

|

207.3% |

| Air traffic liability |

593.3 |

400.9 |

48.0% |

497.7 |

307.2 |

62.0% |

| Provisions |

(138.2) |

(199.2) |

-30.6% |

(200.1) |

(249.1) |

-19.7% |

| Other liabilities |

52.9 |

(2.5) |

n.a. |

(96.8) |

244.0 |

n.a. |

| Interest paid |

(635.0) |

(724.3) |

-12.3% |

(1,123.1) |

(845.3) |

32.9% |

| Net cash generated (used) by operating

activities |

1,178.1 |

593.3 |

98.6% |

1,114.9 |

1,636.4

|

-31.9% |

| |

|

|

|

|

|

|

| Cash flows from investing activities |

|

|

|

|

|

|

| Short-term investment |

(107.4) |

-

|

n.a. |

(107.4) |

-

|

n.a. |

| Sales and leaseback |

-

|

-

|

n.a. |

10.3 |

-

|

n.a. |

| Acquisition

of intangible |

(49.6) |

(52.3) |

-5.3% |

(78.4) |

(92.5) |

-15.3% |

| Acquisition of property and equipment |

(256.0) |

(169.5) |

51.0% |

(673.3) |

(211.1) |

219.0% |

| Net cash

generated (used) in investing activities |

(412.9) |

(221.8) |

86.2% |

(848.8) |

(303.6) |

179.6% |

| |

|

|

|

|

|

|

| Cash

flows from financing activities |

|

|

|

|

|

|

| Loans and financing |

|

|

|

|

|

|

| Proceeds |

839.3 |

600.0

|

39.9% |

2,279.9 |

902.3

|

152.7% |

| Repayment |

(672.2) |

(253.4) |

165.2% |

(1,068.7) |

(580.5) |

84.1% |

| Lease

repayment |

(720.0) |

(567.4) |

26.9% |

(1,533.6) |

(975.1) |

57.3% |

| Factoring |

(115.3) |

- |

n.a. |

(402.8) |

(727.4) |

-44.6% |

| Capital

increase |

-

|

0.8

|

n.a. |

0.0

|

0.8

|

-97.8% |

| Treasury shares |

(0.1) |

- |

n.a. |

(2.6) |

(2.9) |

-10.0% |

| Net cash

generated (used) in financing activities |

(668.3) |

(220.0) |

203.7% |

(727.7) |

(1,382.9) |

-47.4% |

| |

|

|

|

|

|

|

| Exchange

gain (loss) on cash and cash equivalents |

5.1 |

(1.5) |

n.a. |

3.9

|

(2.1) |

n.a. |

| |

|

|

|

|

|

|

| Net decrease

in cash and cash equivalents |

102.0 |

149.9

|

-32.0% |

(457.8) |

(52.1) |

777.9% |

| |

|

|

|

|

|

|

| Cash and

cash equivalents at the beginning of the period |

1,337.6 |

466.4 |

186.8% |

1,897.3 |

668.3 |

183.9% |

| |

|

|

|

|

|

|

| Cash

and cash equivalents at the end of the period |

1,439.6

|

616.2 |

133.6% |

1,439.6

|

616.2 |

133.6% |

| | Second Quarter Results 2024 |

| | |

Glossary

Aircraft Utilization

Average number of block hours per day per aircraft operated.

Available Seat Kilometers (ASK)

Number of aircraft seats multiplied by the

number of kilometers flown.

Completion Factor

Percentage of scheduled

flights that were executed.

Cost per ASK (CASK)

Operating expenses divided by available seat kilometers.

Cost per ASK ex-fuel (CASK ex-fuel)

Operating expenses

divided by available seat kilometers excluding fuel expenses.

EBITDA

Earnings before interest, taxes, depreciation,

and amortization. Adjusted EBITDA excludes non-recurring items.

FTE (Full-Time Equivalent)

Equivalent number of employees assuming

all work full-time.

Immediate Liquidity

Cash, cash equivalents, short-term investments,

and receivables.

Load Factor

Number of passengers as a percentage of

number of seats flown (calculated by dividing RPK by ASK).

LTM

Last twelve months ended on the last day

of the quarter presented.

Revenue Passenger Kilometers (RPK)

One-fare paying passenger transported one

kilometer. RPK is calculated by multiplying the number of revenue passengers by the number of kilometers flown.

Passenger Revenue per Available Seat

Kilometer (PRASK)

Passenger revenue divided by available seat

kilometers (also equal to load factor multiplied by yield).

Revenue per ASK (RASK)

Operating revenue divided by available seat kilometers.

Stage Length

The average number of kilometers flown per flight.

Trip Cost

Average cost of each flight calculated by dividing total operating expenses by total number of departures.

Yield

Average amount paid per passenger to fly

one kilometer. Usually, yield is calculated as average revenue per revenue passenger kilometer.

| | Second Quarter Results 2024 |

| | |

This press release includes estimates and

forward-looking statements within the meaning of the U.S. federal securities laws. These estimates and forward-looking statements are

based mainly on our current expectations and estimates of future events and trends that affect or may affect our business, financial condition,

results of operations, cash flow, liquidity, prospects, and the trading price of our preferred shares, including in the form of ADSs.

Although we believe that these estimates and forward-looking statements are based upon reasonable assumptions, they are subject to many

significant risks, uncertainties and assumptions and are made in light of information currently available to us. In addition, in this

release, the words “may,” “will,” “estimate,” “anticipate,” “intend,” “expect,”

“should” and similar words are intended to identify forward-looking statements. You should not place undue reliance on such

statements, which speak only as of the date they were made. Azul is not under the obligation to update publicly or to revise any forward-looking

statements after we distribute this press release because of new information, future events, or other factors. Our independent public

auditors have neither examined nor compiled the forward-looking statements and, accordingly, do not provide any assurance with respect

to such statements. In light of the risks and uncertainties described above, the future events and circumstances discussed in this release

might not occur and are not guarantees of future performance. Because of these uncertainties, you should not make any investment decision

based upon these estimates and forward-looking statements.

In this press release, we present EBITDA

and EBITDA margin, which are non-IFRS performance measures and are not financial performance measures determined in accordance with IFRS

and should not be considered in isolation or as alternatives to operating income or net income or loss, or as indications of operating

performance, or as alternatives to operating cash flows, or as indicators of liquidity, or as the basis for the distribution of dividends.

Accordingly, you are cautioned not to place undue reliance on this information.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

Date: August 12, 2024

Azul S.A.

By: /s/ Alexandre Wagner Malfitani

Name: Alexandre Wagner Malfitani

Title: Chief Financial Officer

Azul (NYSE:AZUL)

Historical Stock Chart

From Nov 2024 to Dec 2024

Azul (NYSE:AZUL)

Historical Stock Chart

From Dec 2023 to Dec 2024