UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-21786

Voya Global Advantage

and Premium Opportunity Fund

(Exact name of registrant as specified in charter)

| 7337

East Doubletree Ranch Road, Suite 100, Scottsdale, AZ |

|

85258 |

| (Address

of principal executive offices) |

|

(Zip

code) |

The Corporation Trust Company, 1209 Orange Street,

Wilmington, DE 19801

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-800-992-0180

Date of fiscal year end: February 28

Date of reporting period: February 29, 2024

Item 1. Reports to Stockholders.

(a) The following is a copy

of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1):

Annual Report

February 29, 2024

Voya Global Advantage and Premium Opportunity Fund

As permitted by regulations adopted

by the U.S. Securities and Exchange Commission, paper copies of the fund’s annual and semi-annual shareholder reports, like

this annual report, are not sent by mail, unless you specifically request paper copies of the reports. Instead, the reports

will be made available on the Voya funds’ website (www.voyainvestments.com/literature), and you will be notified by mail

each time a report is posted and provided with a website link to access the report.

If you already elected to receive

shareholder reports electronically, you need not take any action. You may elect to receive shareholder reports and other communications

from a fund electronically anytime by contacting your financial intermediary (such as a broker-dealer or bank) or, if you are

a direct investor, by calling 1-800-992-0180 or by sending an e-mail request to Voyaim_literature@voya.com.

You may elect to receive all

future reports in paper free of charge. If you received this document in the mail, please follow the instructions to elect to

continue receiving paper copies of your shareholder reports. If you received this document through a financial intermediary,

you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports.

If you invest directly with us, you can call 1-800-992-0180 or send an email request to Voyaim_literature@voya.com to let a

fund know you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper

will apply to all funds held in your account if you invest through your financial intermediary or all funds held with the

Voya funds complex if you invest directly with the funds.

This report is submitted for general

information to shareholders of the Voya mutual funds. It is not authorized for distribution to prospective shareholders unless

accompanied or preceded by a prospectus which includes details regarding the fund’s investment objectives, risks, charges,

expenses and other information. This information should be read carefully.

| |

|

E-Delivery Sign-up – details

inside |

| INVESTMENT MANAGEMENT |

|

voyainvestments.com

Managed Distribution Policy

The Fund was granted exemptive relief by the U.S.

Securities and Exchange Commission (the “Order”), which under the Investment Company Act of 1940, as amended (the “1940

Act”), permits the Fund to include realized long-term capital gains as a part of its regular distributions to Common Shareholders

more frequently than once per taxable year (“Managed Distribution Policy”). Pursuant to the Order, the Fund’s Board

of Trustees (the “Board”) approved the Managed Distribution Policy and the Fund adopted the policy which allows the Fund to

make periodic distributions of long-term capital gains.

Under the Managed Distribution Policy, the Fund

makes quarterly* distributions of an amount equal to $0.197 per share. You should not draw any conclusions about the Fund’s investment

performance from the amount of this distribution or from the terms of the Fund’s Plan.

The Managed Distribution Policy will be subject

to periodic review by the Fund’s Board and the Board may amend or terminate the Managed Distribution Policy at any time without

prior notice to the Fund’s shareholders; any such change or termination may have an adverse effect on the market price of the Fund’s

shares.

The Fund may distribute more than its net investment

income and net realized capital gains; therefore, a portion of your distribution may include a return of capital. A return of capital

may occur for example, when some or all of the money that you invested in the Fund is paid back to you. A return of capital distribution

does not necessarily reflect the Fund’s investment performance and should not be confused with ‘yield’ or ‘income.’

With each distribution, the Fund will issue a notice to shareholders and a press release containing information about the amounts and

sources of distribution and other related information. The amounts and sources of the distributions contained in a notice and press release

are only estimates and are not provided for tax reporting purposes. The actual amounts and sources of the amounts for tax reporting purposes

will depend upon the Fund’s investment experience during the remainder of its fiscal year and may be subject to changes based on

tax regulations. The Fund will send you a Form 1099-DIV for the calendar year that will tell you how to report these distributions for

federal income tax purposes.

* Effective

April 1, 2024, under the managed distribution policy the Fund will make monthly distributions.

TABLE

OF CONTENTS

| |

Go Paperless with E-Delivery! |

|

| Sign up now for on-line prospectuses, fund reports, and proxy

statements. |

| |

| Just go to individuals.voya.com/page/e-delivery, follow the directions

and complete the quick 5 Steps to Enroll. |

| |

| You will be notified by e-mail when these communications become

available on the internet. |

PROXY VOTING INFORMATION

A description of the policies and procedures

that the Fund uses to determine how to vote proxies related to portfolio securities is available: (1) without charge, upon request, by

calling Shareholder Services toll-free at (800) 992-0180; (2) on the Fund’s website at www.voyainvestments.com; and (3) on the

U.S. Securities and Exchange Commission’s (“SEC’s”) website at www.sec.gov. Information regarding how the Fund

voted proxies related to portfolio securities during the most recent 12-month period ended June 30 is available without charge on the

Fund’s website at www.voyainvestments.com and on the SEC’s website at www.sec.gov.

QUARTERLY PORTFOLIO HOLDINGS

The Fund files its complete schedule of portfolio

holdings with the SEC for the first and third quarters of each fiscal year on Form NPORT-P. The Fund’s Forms NPORT-P are available

on the SEC’s website at www.sec.gov. The Fund’s complete schedule of portfolio holdings is available at: www.voyainvestments.com

and without charge upon request from the Fund by calling Shareholder Services toll-free at (800) 992-0180.

BENCHMARK

DESCRIPTIONS

| Index |

Description |

| MSCI World Value IndexSM |

The index captures large and mid cap securities exhibiting overall value style characteristics across 23 Developed Markets countries. |

| VOYA GLOBAL

ADVANTAGE |

PRINCIPAL INVESTMENT

STRATEGIES AND |

| AND PREMIUM

OPPORTUNITY FUND |

PORTFOLIO

MANAGERS’ COMMENTARY |

Voya

Global Advantage and Premium Opportunity Fund (the “Fund”) is a diversified closed-end fund with the primary investment objective

of providing a high level of income. Capital appreciation is a secondary investment objective. The Fund seeks to achieve its investment

objectives by:

| ● | investing at least 80% of its

managed assets in a portfolio of common stocks of companies located in a number of different countries throughout the world, including

the United States; and |

| ● | utilizing

an integrated derivatives strategy. |

Portfolio Management*: The Fund is

managed by Susanna Jacob, Justin Montminy, CFA, Vincent Costa, CFA, and Steve Wetter, Voya Investment Management Co. LLC — the Sub-Adviser.

Equity Portfolio Construction: Under

normal market conditions, the Fund seeks to achieve its investment objective by investing at least 80% of its managed assets in a portfolio

of common stocks of companies located in a number of different countries throughout the world, including the United States; and utilizing

an integrated derivatives strategy.

Under normal market conditions, the Fund will invest

at least 80% of its managed assets in a diversified portfolio of common stocks across a broad range of countries, industries and market

sectors. Equity securities held by the Fund may be denominated in both U.S. dollars and non-U.S. currencies. The Fund may invest up to

20% of its managed assets in securities issued by companies located in emerging markets when the Sub-Adviser believes they present attractive

investment opportunities.

The Fund seeks to invest in a portfolio of equity

securities included in the MSCI World Value IndexSM (the “Index”) and will select securities based upon quantitative

analysis. The Sub-Adviser creates a target universe that consists of dividend paying securities by screening for companies that exhibit

stable dividend yields within each industry sector. Once the Sub-Adviser creates this target universe, the Sub-Adviser seeks to identify

the most attractive securities within various geographic regions and sectors by ranking each security relative to other securities within

its region or sector, as applicable, using proprietary fundamental sector-specific models. The Sub-Adviser then uses optimization techniques

to seek to achieve the portfolio’s target dividend yield, which is expected to be higher than the Index in aggregate, manage target

beta, determine active weights, and neutralize region and sector exposures in order to create a portfolio that the Sub-Adviser believes

will provide the potential for maximum total return consistent with maintaining lower volatility than the Index. Under certain market

conditions, the Fund will likely earn a lower level of total return than it would in the absence of its strategy of maintaining a relatively

lower level of volatility.

Geographic

Diversification

as

of February 29, 2024

(as

a percentage of net assets)

| United States | |

66.4 | % |

| Japan | |

6.9 | % |

| United Kingdom | |

4.2 | % |

| Australia | |

2.3 | % |

| Canada | |

2.2 | % |

| France | |

2.2 | % |

| Spain | |

1.9 | % |

| Netherlands | |

1.8 | % |

| Hong Kong | |

1.5 | % |

| Switzerland | |

1.4 | % |

| Countries between 0.1% - 1.4%^ | |

6.8 | % |

| Assets in Excess of Other Liabilities* | |

2.4 | % |

| Net Assets | |

100.0 | % |

| * | Includes

short-term investments and exchange-traded funds. |

| ^ | Includes

12 countries, which each 0.1% - 1.4% of net assets. |

Portfolio

holdings are subject to change daily.

Top

Ten Holdings

as

of February 29, 2024

(as

a percentage of net assets)

| Johnson & Johnson |

1.8% |

| Merck & Co., Inc. |

1.8% |

| AbbVie, Inc. |

1.7% |

| Chevron Corp. |

1.4% |

| Procter & Gamble Co. |

1.3% |

| PepsiCo, Inc. |

1.2% |

| Cisco Systems, Inc. |

1.2% |

| Verizon Communications, Inc. |

1.1% |

| Amgen, Inc. |

1.0% |

| Cigna Group |

1.0% |

Portfolio

holdings are subject to change daily.

In

evaluating investments for the Fund, the Sub-Adviser normally expects to take into account environmental, social, and governance (“ESG”)

factors, to determine whether any or all of those factors might have a material effect on the value, risks, or prospects of a company.

The Sub-Adviser intends to rely primarily on factors identified through its proprietary empirical research as material to a particular

company or the industry in which it operates and on third-party evaluations of a company’s ESG standing. The Sub-Adviser may give

environmental, social, and governance factors equal consideration or may focus on one or more of those factors as the Sub-Adviser considers

appropriate. The Sub-Adviser may consider specific ESG metrics or a company’s progress or lack of progress toward meeting ESG targets.

ESG factors will be only one consideration in the Sub-Adviser’s evaluation of any potential investment, and the effect, if any,

of ESG factors on the Sub-Adviser’s decision whether to invest in any case will vary depending on the judgment of the Sub-Adviser.

The Fund’s Integrated Option Strategy:

The option strategy of the Fund is designed to seek gains and lower volatility of total returns over a market cycle by generally

writing (selling) index call options on selected indices and/or exchange traded funds (“ETFs”) in an amount equal to approximately

35% to 100% of the value of the Fund’s holdings in common stocks.

| PRINCIPAL INVESTMENT

STRATEGIES AND |

VOYA GLOBAL

ADVANTAGE |

| PORTFOLIO

MANAGERS’ COMMENTARY |

AND PREMIUM

OPPORTUNITY FUND |

The

extent of call option writing activity depends upon market conditions and the Sub-Adviser’s ongoing assessment of the attractiveness

of writing call options on selected indices and/or ETFs. Call options will be written (sold) usually at-the money, out-of-the-money or

near-the-money and can be written both in exchange-listed option markets and over-the-counter markets with major international banks,

broker-dealers and financial institutions.

The Fund writes call options that are generally

short-term (between 10 days and three months until expiration). The Fund typically maintains its call positions until expiration, but

it retains the option to buy back the call options and sell new call options.

Additionally, in order to reduce volatility of

net asset value (“NAV”) returns, the Fund generally employs a policy to hedge major foreign currencies using foreign currency

forwards or zero-cost collars.

In addition to the intended strategy of selling

index call options, the Fund may invest in other derivative instruments such as futures for investment, hedging and risk-management purposes

to gain or reduce exposure to securities, security markets and market indices consistent with its investment objectives and strategies.

Such derivative instruments are acquired to enable the Fund to make market directional tactical decisions to enhance returns, to protect

against a decline in its assets or as a substitute for the purchase or sale of equity securities.

Performance: Based on net asset value

(“NAV”), the Fund provided a total return of 9.10% for the year ended February 29, 2024.(1) This NAV return reflects

a decrease in the Fund’s NAV from $10.04 on February 28, 2023 to $9.99 on February 29, 2024, after taking into account quarterly

distributions. Based on its share price as of February 29, 2024, the Fund provided a total return of 5.82% for the year.(1)

This share price return reflects a decrease in the Fund’s share price from $8.88 on February 28, 2023 to $8.57 on February 29, 2024,

after taking into account quarterly distributions. The Fund’s reference index, the MSCI World Value IndexSM, returned

12.69% for the year. During the year, the Fund made quarterly distributions totaling $0.79 per share, which were characterized as $0.45

per share from return of capital and $0.34 per share from net investment income.(2) As of February 29, 2024, the Fund had 15,341,392

shares outstanding.

Portfolio Specifics: Equity Portfolio: The

Fund underperformed its reference Index during the reporting period. In terms of portfolio performance attribution, size factor was the

largest detractor while the core model and the higher dividend yield contributed. Within the core model, the sentiment indicator contributed

the most.

Regionally, stock selection in Europe contributed to results, while

selection in North America detracted.

At the sector level, stock selection was strongest

among the energy, materials and health care sectors. At the individual stock level, key contributors included exposure to non-benchmark

stocks Sage Group PLC. and NVIDIA Corp. and not owning Exxon Mobil Corp.

Conversely, stock selection was negative in information

technology, industrials and consumer staples sectors. Among the key detractors were not owning Toyota Motor Corp., Intel Corp. and Broadcom

Inc.

Option Portfolio: The Fund's covered

call strategy seeks to generate premiums and retain some potential for upside appreciation. The Fund's option strategy detracted from

returns during the period, as the positive performance of the equity markets resulted in losses on the short call options. The Fund implemented

this strategy by typically writing call options on regional indexes, the selection and allocation of which resulted from an optimization

intended to track closely the Fund's reference index. The options typically were written with maturities around six weeks and with strike

prices out of the money or near the money.

Outlook and Current Strategy: After

a strong year for the U.S. economy and capital markets, many investors entered 2024 with an upbeat outlook. We are generally optimistic

about the year ahead but in our opinion, we see a few factors that could limit the upside potential for stocks.

We believe the progress on inflation and the resilience

of American consumers and corporations is encouraging, and U.S. companies appear, in our view, to be on sound financial footing. We expect

disinflation to continue, as core personal consumption expenditures ("PCE") inflation has trended sharply lower, and supply

chain issues have eased considerably. However, we also foresee weaker wage growth and consumer spending as the lagging impact of tighter

monetary policy filters into the U.S. labor market. Despite our slowing growth outlook and expectation of modestly higher unemployment,

we are not forecasting a significant deterioration in the jobs market.

In our view, obstacles to the upside potential

in U.S. equities this year include slower economic growth, expensive valuations and optimistic forecasts of rate cuts. Even with these

challenges, we believe that current macroeconomic conditions present opportunities for investors to benefit from divergences in global

policy and business cycles.

| VOYA GLOBAL

ADVANTAGE |

PRINCIPAL INVESTMENT

STRATEGIES AND |

| AND PREMIUM

OPPORTUNITY FUND |

PORTFOLIO

MANAGERS’ COMMENTARY |

*

Effective March 1, 2024, Peg DiOrio was removed as one of the portfolio managers to the Fund. In addition, effective December 31, 2023,

Paul Zemsky retired from Voya Investment Management Co. LLC and is no longer one of the portfolio managers to the Fund. Lastly, effective

September 30, 2023, Susanna Jacob was added as a portfolio manager to the Fund.

(1) Total returns

shown include, if applicable, the effect of fee waivers and/or expense reimbursements by the investment adviser. Had all fees and expenses

been considered, the total returns would have been lower.

(2) The

final tax composition of dividends and distributions will not be determined until after the Fund’s tax year-end.

The views expressed in this commentary

are informed opinions. They should not be considered promises or advice. The views expressed reflect those of the portfolio managers,

only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based

on market and other conditions.

Portfolio holdings and characteristics

are subject to change and may not be representative of current holdings and characteristics. Fund holdings are subject to change daily.

The outlook for this Fund may differ from that presented for other Voya mutual funds. This report contains statements that may be “forward-looking”

statements. Actual results may differ materially from those projected in the “forward-looking” statements. The Fund’s

performance returns shown reflect applicable fee waivers and/or expense limits in effect during this period. Absent such fee waivers/expense

limitations, if any, performance would have been lower. Performance for the different classes of shares will vary based on differences

in fees associated with each class. An index has no cash in its portfolio and imposes no sales charges. An investor cannot invest directly

in an index.

| Principal

Investment

Strategies

and |

Voya

Global

Advantage |

| PORTFOLIO

MANAGERS’

COMMENTARY |

AND PREMIUM

OPPORTUNITY

FUND |

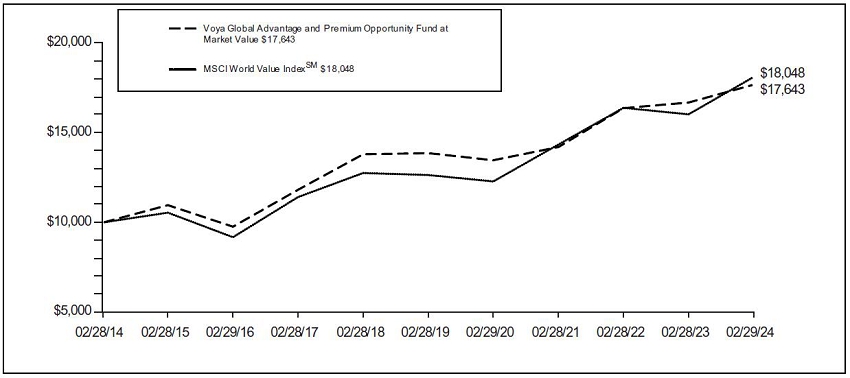

| Average Annual Total Returns for the Periods Ended February 29, 2024 |

| |

1 Year |

5 Year |

10 Year |

| Voya Global Advantage and Premium Opportunity Fund at Market Value |

5.82% |

4.96% |

5.84% |

| MSCI World Value IndexSM |

12.69% |

7.39% |

6.08% |

Based on a $10,000

initial investment, the graph and table above illustrate the total return of Voya Global Advantage and Premium Premium Opportunity Fund

against the reference index indicated. The reference index is unmanaged and has no cash in its portfolio and imposes no sales charges.

An investor cannot invest directly in a reference index.

The performance shown

includes, if applicable, the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers,

which have the effect of increasing total net return. Had all fees and expenses been considered, the total net returns would have been

lower.

Performance

data represents past performance and is no assurance

of future results.

Investment return and principal value of an investment in the Fund will fluctuate. Shares, when sold, may be worth more or less than

their original cost. The Fund’s current performance may be lower or higher than the performance data shown. Please log on to www.voyainvestments.com

or call (800) 992-0180 to get performance through the most recent month end.

Fund holdings are subject to change

daily.

The Fund’s performance

prior to May 6, 2019 reflects returns achieved by a different sub-adviser and pursuant to a different investment objective and principal

investment strategies. If the Fund’s current sub-adviser, objective and strategies had been in place for the prior period, the

performance information shown would have been different.

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING

FIRM

To

the Shareholders and Board of Trustees of Voya Global Advantage and Premium Opportunity Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets

and liabilities of Voya Global Advantage and Premium Opportunity Fund (the “Fund”), including the portfolio of investments,

as of February 29, 2024, and the related statement of operations for the year then ended, the statements of changes in net assets for

each of the two years in the period then ended, the financial highlights for each of the five years in the period then ended and the related

notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in

all material respects, the financial position of the Fund at February 29, 2024, the results of its operations for the year then ended,

the changes in its net assets for each of the two years in the period then ended and its financial highlights for each of the five years

in the period then ended, in conformity with U.S. generally accepted accounting principles.

The financial highlights for each of the years

in the five-year period ended February 28, 2019, were audited by another independent registered public accounting firm whose report, dated

April 26, 2019, expressed an unqualified opinion on those financial highlights.

Basis for Opinion

These financial statements are the responsibility

of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits.

We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required

to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations

of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the

standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial

statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to

perform, an audit of the Fund’s internal control over financial reporting. As part of our audits, we are required to obtain an understanding

of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund’s

internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess

the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond

to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial

statements. Our procedures included confirmation of securities owned as of February 29, 2024, by correspondence with the custodian, brokers

and others; when replies were not received from brokers and others, we performed other auditing procedures. Our audits also included

evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation

of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

We have served as the auditor of one or more Voya investment companies

since 2019.

Boston, Massachusetts

April 26, 2024

STATEMENT OF ASSETS

AND LIABILITIES As oF FEBRUARY

29, 2024

| ASSETS: | |

| | |

| Investments

in securities at fair value* | |

$ | 151,055,267 | |

| Short-term

investments at fair value† | |

| 666,000 | |

| Cash | |

| 309,271 | |

| Cash pledged

as collateral for OTC derivatives (Note 2) | |

| 1,360,000 | |

| Foreign currencies

at value‡ | |

| 7,434 | |

| Receivables: | |

| | |

| Investment

securities sold | |

| 6,311 | |

| Dividends | |

| 336,206 | |

| Interest | |

| 531 | |

| Foreign

tax reclaims | |

| 188,375 | |

| Unrealized

appreciation on forward foreign currency contracts | |

| 1,089,157 | |

| Prepaid expenses | |

| 1,149 | |

| Other assets | |

| 9,281 | |

| Total assets | |

| 155,028,982 | |

| | |

| | |

| LIABILITIES: | |

| | |

| Payable for

investment securities purchased | |

| 6,317 | |

| Payable for

investment management fees | |

| 101,023 | |

| Payable to

trustees under the deferred compensation plan (Note 6) | |

| 9,281 | |

| Payable for

trustee fees | |

| 380 | |

| Other accrued

expenses and liabilities | |

| 169,968 | |

| Written

options, at fair value^ | |

| 1,428,806 | |

| Total liabilities | |

| 1,715,775 | |

| NET

ASSETS | |

$ | 153,313,207 | |

| | |

| | |

| NET

ASSETS WERE COMPRISED OF: | |

| | |

| Paid-in capital | |

$ | 139,341,159 | |

| Total distributable

earnings | |

| 13,972,048 | |

| NET

ASSETS | |

$ | 153,313,207 | |

| | |

| | |

| * Cost

of investments in securities | |

$ | 134,744,399 | |

| † Cost

of short-term investments | |

$ | 666,000 | |

| ‡ Cost

of foreign currencies | |

$ | 7,435 | |

| ^ Premiums

received on written options | |

$ | 902,879 | |

| | |

| | |

| Net assets | |

$ | 153,313,207 | |

| Shares authorized | |

| unlimited | |

| Par value | |

$ | 0.010 | |

| Shares outstanding | |

| 15,341,392 | |

| Net asset value | |

$ | 9.99 | |

See Accompanying Notes to

Financial Statements

STATEMENT OF OPERATIONS

FOR THE YEAR ENDED FEBRUARY

29, 2024

| INVESTMENT

INCOME: | |

| | |

| Dividends,

net of foreign taxes withheld* | |

$ | 5,582,999 | |

| Interest | |

| 19,101 | |

| Other | |

| 938 | |

| Total

investment income | |

| 5,603,038 | |

| | |

| | |

| EXPENSES: | |

| | |

| Investment

management fees | |

| 1,289,505 | |

| Transfer

agent fees | |

| 16,390 | |

| Shareholder

reporting expense | |

| 45,260 | |

| Professional

fees | |

| 82,190 | |

| Custody

and accounting expense | |

| 39,601 | |

| Trustee

fees | |

| 3,794 | |

| Miscellaneous

expense | |

| 23,809 | |

| Total

expenses | |

| 1,500,549 | |

| Waived

and recouped fees | |

| 20,088 | |

| Net

expenses | |

| 1,520,637 | |

| Net

investment income | |

| 4,082,401 | |

| REALIZED

AND UNREALIZED GAIN (LOSS): | |

| | |

| Net

realized gain (loss) on: | |

| | |

| Investments | |

| 1,269,087 | |

| Forward

foreign currency contracts | |

| 524,208 | |

| Foreign

currency related transactions | |

| 137,705 | |

| Written

options | |

| (3,315,125 | ) |

| Net

realized loss | |

| (1,384,125 | ) |

| Net

change in unrealized appreciation (depreciation) on: | |

| | |

| Investments | |

| 8,587,655 | |

| Forward

foreign currency contracts | |

| 731,829 | |

| Foreign

currency related transactions | |

| 4,642 | |

| Written

options | |

| (1,309,610 | ) |

| Net

change in unrealized appreciation (depreciation) | |

| 8,014,516 | |

| Net

realized and unrealized gain | |

| 6,630,391 | |

| Increase

in net assets resulting from operations | |

$ | 10,712,792 | |

| * Foreign

taxes withheld | |

$ | 310,760 | |

See

Accompanying Notes to Financial Statements

STATEMENTS

OF CHANGES IN NET ASSETS

| | |

Year

Ended

February 29, 2024 | | |

Year

Ended

February 28, 2023 | |

| FROM

OPERATIONS: | |

| | | |

| | |

| Net

investment income | |

$ | 4,082,401 | | |

$ | 3,947,338 | |

| Net

realized gain (loss) | |

| (1,384,125 | ) | |

| 8,666,802 | |

| Net

change in unrealized appreciation (depreciation) | |

| 8,014,516 | | |

| (8,164,749 | ) |

| Increase

in net assets resulting from operations | |

| 10,712,792 | | |

| 4,449,391 | |

| | |

| | | |

| | |

| FROM

DISTRIBUTIONS TO SHAREHOLDERS: | |

| | | |

| | |

| Total

distributions (excluding return of capital) | |

| (5,287,864 | ) | |

| (8,758,104 | ) |

| Return

of capital | |

| (6,953,868 | ) | |

| (3,920,567 | ) |

| Total

distributions | |

| (12,241,732 | ) | |

| (12,678,671 | ) |

| | |

| | | |

| | |

| FROM

CAPITAL SHARE TRANSACTIONS: | |

| | | |

| | |

| Cost

of shares repurchased | |

| (4,389,547 | ) | |

| (4,638,655 | ) |

| Net

decrease in net assets resulting from capital share transactions | |

| (4,389,547 | ) | |

| (4,638,655 | ) |

| Net

decrease in net assets | |

| (5,918,487 | ) | |

| (12,867,935 | ) |

| | |

| | | |

| | |

| NET

ASSETS: | |

| | | |

| | |

| Beginning

of year or period | |

| 159,231,694 | | |

| 172,099,629 | |

| End

of year or period | |

$ | 153,313,207 | | |

$ | 159,231,694 | |

See

Accompanying Notes to Financial Statements

FINANCIAL

HIGHLIGHTS

Selected

data for a share of beneficial interest outstanding throughout each year or period.

| | |

Per

Share Operating Performance | | |

Ratios

and Supplemental Data | |

| | |

| | | Income

(loss) from

investment

operations |

|

| |

Less

Distributions |

| | |

| | | |

| |

| | | |

| |

| | | |

| |

Ratios

to average

net assets | |

| |

| | |

|  | | |

| |

|  | | |

| |

|  | | |

| |

|  | |

|  | |

|  | | |

| |

|  | | |

| |

|  | | |

| |

|  | | |

| |

|  | | |

| |

Year or

period ended |

|

| ($) | | |

($) | |

| ($) | | |

($) | |

| ($) | | |

($) | |

| ($) | |

| ($) | |

| ($) | | |

($) | |

| ($) | | |

(%) | |

| (%) | | |

($000's) | |

| (%) | | |

(%) | |

| (%) | | |

(%) | |

| |

|

| | | |

| |

| | | |

| |

| | | |

| |

| | |

| | |

| | | |

| |

| | | |

| |

| | | |

| |

| | | |

| |

| | | |

| |

| 02-29-24 |

|

|

10.04 |

|

|

0.26• |

|

|

0.48 |

|

|

0.74 |

|

|

0.34 |

|

|

— |

|

|

0.45 |

|

|

0.79 |

|

|

— |

|

|

9.99 |

|

|

8.57 |

|

|

9.10 |

|

|

5.82 |

|

|

153,313 |

|

|

0.99 |

|

|

1.00 |

|

|

2.69 |

|

|

74 |

|

| 02-28-23 |

|

|

10.51 |

|

|

0.25• |

|

|

0.07 |

|

|

0.32 |

|

|

0.42 |

|

|

0.12 |

|

|

0.25 |

|

|

0.79 |

|

|

— |

|

|

10.04 |

|

|

8.88 |

|

|

4.15 |

|

|

1.91 |

|

|

159,232 |

|

|

1.02 |

|

|

0.99 |

|

|

2.40 |

|

|

81 |

|

| 02-28-22 |

|

|

9.89 |

|

|

0.18• |

|

|

1.20 |

|

|

1.38 |

|

|

0.21 |

|

|

— |

|

|

0.58 |

|

|

0.79 |

|

|

0.03 |

|

|

10.51 |

|

|

9.50 |

|

|

15.02 |

|

|

15.28 |

|

|

172,100 |

|

|

1.10 |

|

|

1.09 |

|

|

1.72 |

|

|

66 |

|

| 02-28-21 |

|

|

10.42 |

|

|

0.19• |

|

|

0.07 |

|

|

0.26 |

|

|

0.15 |

|

|

0.40 |

|

|

0.24 |

|

|

0.79 |

|

|

— |

|

|

9.89 |

|

|

8.92 |

|

|

4.27 |

|

|

5.48 |

|

|

180,073 |

|

|

0.97 |

|

|

0.97 |

|

|

2.00 |

|

|

74 |

|

| 02-29-20 |

|

|

11.43 |

|

|

0.27 |

|

|

(0.44) |

|

|

(0.17) |

|

|

0.40 |

|

|

0.44 |

|

|

— |

|

|

0.84 |

|

|

— |

|

|

10.42 |

|

|

9.29 |

|

|

(1.35) |

|

|

(2.87) |

|

|

190,658 |

|

|

0.96 |

|

|

0.96 |

|

|

2.37 |

|

|

130 |

|

| 02-28-19 |

|

|

12.12 |

|

|

0.21 |

|

|

0.00* |

|

|

0.21 |

|

|

0.41 |

|

|

0.49 |

|

|

— |

|

|

0.90 |

|

|

— |

|

|

11.43 |

|

|

10.35 |

|

|

2.43 |

|

|

0.46 |

|

|

209,174 |

|

|

0.99 |

|

|

0.99 |

|

|

1.76 |

|

|

70 |

|

| 02-28-18 |

|

|

11.62 |

|

|

0.19• |

|

|

1.21 |

|

|

1.40 |

|

|

0.04 |

|

|

0.78 |

|

|

0.08 |

|

|

0.90 |

|

|

— |

|

|

12.12 |

|

|

11.19 |

|

|

13.07 |

|

|

16.75 |

|

|

221,924 |

|

|

0.99 |

|

|

0.99 |

|

|

1.55 |

|

|

92 |

|

| 02-28-17 |

|

|

10.71 |

|

|

0.18 |

|

|

1.80 |

|

|

1.98 |

|

|

0.42 |

|

|

0.16 |

|

|

0.49 |

|

|

1.07 |

|

|

— |

|

|

11.62 |

|

|

10.39 |

|

|

20.77 |

|

|

21.11 |

|

|

213,271 |

|

|

1.00 |

|

|

1.00 |

|

|

1.59 |

|

|

98 |

|

| 02-29-16 |

|

|

12.93 |

|

|

0.17 |

|

|

(1.27) |

|

|

(1.10) |

|

|

0.39 |

|

|

0.73 |

|

|

— |

|

|

1.12 |

|

|

— |

|

|

10.71 |

|

|

9.55 |

|

|

(8.48)(5) |

|

|

(10.96) |

|

|

196,576 |

|

|

1.00 |

|

|

1.00 |

|

|

1.36 |

|

|

117 |

|

| 02-28-15 |

|

|

13.09 |

|

|

0.17 |

|

|

0.79 |

|

|

0.96 |

|

|

0.59 |

|

|

— |

|

|

0.53 |

|

|

1.12 |

|

|

— |

|

|

12.93 |

|

|

11.85 |

|

|

8.72 |

|

|

9.52 |

|

|

237,394 |

|

|

0.95 |

|

|

0.97 |

|

|

1.32 |

|

|

17 |

|

| (1) | Total

investment return at net asset value has been calculated assuming a purchase at net asset

value at the beginning of each period and a sale at net asset value at the end of each period

and assumes reinvestment of dividends, capital gain distributions and return of capital distributions/allocations,

if any, in accordance with the provisions of the dividend reinvestment plan. Total investment

return at net asset value is not annualized for periods less than one year. |

| (2) | Total

investment return at market value measures the change in the market value of your investment

assuming reinvestment of dividends, capital gain distributions and return of capital distributions/allocations,

if any, in accordance with the provisions of the Fund’s dividend reinvestment plan.

Total investment return at market value is not annualized for periods less than one year. |

| (3) | Annualized

for periods less than one year. |

| (4) | The

Investment Adviser has entered into a written expense limitation agreement with the Fund

under which it will limit the expenses of the Fund (excluding interest, taxes, investment-related

costs, leverage expenses, extraordinary expenses and acquired fund fees and expenses) subject

to possible recoupment by the Investment Adviser within three years of being incurred. |

| (5) | Excluding

amounts related to a foreign currency settlement recorded in the fiscal year ended February

29, 2016, total investment return at net asset value would have been (8.65)%. |

| ● | Calculated

using average number of shares outstanding throughout the year or period. |

| * | Amount

is less than $0.005 or 0.005% or more than $(0.005) or (0.005)%. |

See

Accompanying Notes to Financial Statements

NOTES

TO FINANCIAL STATEMENTS As oF FEBRUARY

29, 2024

NOTE 1 —

ORGANIZATION

Voya

Global Advantage and Premium Opportunity Fund (the “Fund”) is a diversified, closed-end management investment company registered

under the Investment Company Act of 1940, as amended (the “1940 Act”). The Fund is organized as a Delaware statutory trust.

Voya

Investments, LLC (“Voya Investments” or the “Investment Adviser”), an Arizona limited liability company, serves

as the Investment Adviser to the Fund. The Investment Adviser has engaged Voya Investment Management Co. LLC (“Voya IM” or

the “Sub-Adviser”), a Delaware limited liability company, to serve as the Sub-Adviser to the Fund.

NOTE 2 —

SIGNIFICANT ACCOUNTING POLICIES

The

following significant accounting policies are consistently followed by the Fund in the preparation of its financial statements. The Fund

is considered an investment company under U.S. generally accepted accounting principles (“GAAP”) and follows the accounting

and reporting guidance applicable to investment companies.

A.

Security Valuation. The Fund is open for business every day the New York Stock Exchange (“NYSE”) opens for

regular trading (each such day, a “Business Day”). The net asset value (“NAV”) per share of the Fund is determined

each Business Day as of the close of the regular trading session (“Market Close”), as determined by the Consolidated Tape

Association (“CTA”), the central distributor of transaction prices for exchange-traded securities (normally 4:00 p.m. Eastern

Time unless otherwise designated by the CTA). The NAV per share of the Fund is calculated by taking the value of the Fund’s assets,

subtracting the Fund’s liabilities, and dividing by the number of shares that are outstanding. On days when the Fund is closed

for business, Fund shares will not be priced and the Fund does not transact purchase and redemption orders. To the extent the Fund’s

assets are traded in other markets on days when the Fund does not price its shares, the value of the Fund’s assets will likely

change and you will not be able to purchase or redeem shares of the Fund.

Portfolio

securities for which market quotations are readily available are valued at market value. Investments in open-end registered investment

companies that do not trade on an exchange are valued at the end of day NAV per share. The prospectuses of the open-end registered investment

companies in which the Fund may invest explain the circumstances under which they will use fair value pricing and the effects of using

fair value pricing. Foreign securities’ prices are converted into U.S. dollar amounts using the applicable exchange rates as of

Market Close.

When

a market quotation for a portfolio security is not readily

available

or is deemed unreliable (for example when trading has been halted or there are unexpected market closures or other material events that

would suggest that the market quotation is unreliable) and for purposes of determining the value of other Fund assets, the asset is priced

at its fair value. The Board has designated the Investment Adviser, as the valuation designee, to make fair value determinations in good

faith. In determining the fair value of the Fund’s assets, the Investment Adviser, pursuant to its fair valuation policy, may consider

inputs from pricing service providers, broker-dealers, or the Fund’s sub-adviser(s). Issuer specific events, transaction price,

position size, nature and duration of restrictions on disposition of the security, market trends, bid/ask quotes of brokers and other

market data may be reviewed in the course of making a good faith determination of an asset’s fair value. Because trading hours

for certain foreign securities end before Market Close, closing market quotations may become unreliable. The prices of foreign securities

will generally be adjusted based on inputs from an independent pricing service that are intended to reflect valuation changes through

the NYSE close. Because of the inherent uncertainties of fair valuation, the values used to determine the Fund’s NAV may materially

differ from the value received upon actual sale of those investments. Thus, fair valuation may have an unintended dilutive or accretive

effect on the value of shareholders’ investments in the Fund.

The

Fund’s financial instruments are valued at the close of the NYSE and are reported at fair value, which GAAP defines as the price

that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the

measurement date.

Various

valuation techniques and inputs are used to determine the fair value of financial instruments. GAAP establishes the following fair value

hierarchy that categorizes the inputs used to measure fair value:

Level

1 – quoted prices (unadjusted) in active markets for identical financial instruments that the fund can access at the reporting

date.

Level

2 – inputs other than Level 1 quoted prices that are observable, either directly or indirectly (including, but not limited to,

quoted prices for similar financial instruments in active markets, quoted prices for identical or similar financial instruments in inactive

markets, interest rates and yield curves, implied volatilities, and credit spreads).

Level

3 – unobservable inputs (including the fund’s own assumptions in determining fair value).

Observable

inputs are developed using market data, such

NOTES

TO FINANCIAL STATEMENTS As OF FEBRUARY

29, 2024 (CONTINUED)

NOTE

2 — SIGNIFICANT ACCOUNTING POLICIES

(continued)

as

publicly available information about actual events or transactions, and reflect the assumptions that market participants would use to

price the financial instrument. Unobservable inputs are those for which market data are not available and are developed using the best

information available about the assumptions that market participants would use to price the financial instrument. GAAP requires valuation

techniques to maximize the use of relevant observable inputs and minimize the use of unobservable inputs. When multiple inputs are used

to derive fair value, the financial instrument is assigned to the level within the fair value hierarchy based on the lowest-level input

that is significant to the fair value of the financial instrument. Input levels are not necessarily an indication of the risk or liquidity

associated with financial instruments at that level but rather the degree of judgment used in determining those values.

A

table summarizing the Fund’s investments under these levels of classification is included within the Portfolio of Investments.

Each

investment asset or liability of the Fund is assigned a level at measurement date based on the significance and source of the inputs

to its valuation. Quoted prices in active markets for identical securities are classified as “Level 1,” inputs other than

quoted prices for an asset or liability that are observable are classified as “Level 2” and significant unobservable inputs,

including the Sub-Adviser’s or Pricing Committee’s judgment about the assumptions that a market participant would use in

pricing an asset or liability are classified as “Level 3.” The inputs used for valuing securities are not necessarily an

indication of the risks associated with investing in those securities. Short-term securities of sufficient credit quality are generally

considered to be Level 2 securities under applicable accounting rules. A table summarizing the Fund’s investments under

these levels of classification is included within the Portfolio of Investments. GAAP requires a reconciliation of the beginning to ending

balances for reported fair values that presents changes attributable to total realized and unrealized gains or losses, purchases and

sales, and transfers in or out of the Level 3 category during the period. The beginning of period timing recognition is used for the

transfers between levels of the Fund’s assets and liabilities. A reconciliation of Level 3

investments is presented only when the Fund has a significant amount of Level 3 investments.

B.

Securities Transactions and Revenue Recognition. Securities transactions are recorded on the trade date. Realized gains

or losses on sales of investments are calculated on the identified cost basis. Interest income is recorded on the accrual basis. Premium

amortization and

discount

accretion are determined using the effective yield method. Dividend income is recorded on the ex-dividend date, or in the case of some

foreign dividends, when the information becomes available to the Fund.

C.

Foreign Currency Translation. The books and records of the Fund are maintained in U.S. dollars. Any foreign currency amounts

are translated into U.S. dollars on the following basis:

| (1) | Market

value of investment securities, other assets and liabilities — at the exchange rates

prevailing at Market Close. |

| (2) | Purchases

and sales of investment securities, income and expenses — at the rates of exchange

prevailing on the respective dates of such transactions. |

Although

the net assets and the market values are presented at the foreign exchange rates at Market Close, the Fund does not isolate the portion

of the results of operations resulting from changes in foreign exchange rates on investments from the fluctuations arising from changes

in market prices of securities held. Such fluctuations are included with the net realized and unrealized gains or losses from investments.

For securities, which are subject to foreign withholding tax upon disposition, liabilities are recorded on the Statement of Assets and

Liabilities for the estimated tax withholding based on the securities’ current market value. Upon disposition, realized gains or

losses on such securities are recorded net of foreign withholding tax.

Reported

net realized foreign exchange gains or losses arise from sales of foreign currencies, currency gains or losses realized between the trade

and settlement dates on securities transactions, the difference between the amounts of dividends, interest, and foreign withholding taxes

recorded on the Fund’s books and the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized foreign exchange

gains and losses arise from changes in the value of assets and liabilities other than investments in securities, resulting from changes

in the exchange rate. Foreign security and currency transactions may involve certain considerations and risks not typically associated

with investing in U.S. companies and U.S. government securities. These risks include, but are not limited to, revaluation of currencies

and future adverse political and economic developments which could cause securities and their markets to be less liquid and prices more

volatile than those of comparable U.S. companies and U.S. government securities. The foregoing risks are even greater with respect to

securities of issuers in emerging markets.

NOTES

TO FINANCIAL STATEMENTS As OF FEBRUARY

29, 2024 (CONTINUED)

NOTE

2 — SIGNIFICANT ACCOUNTING POLICIES

(continued)

D.

Distributions to Shareholders. The

Fund intends to make quarterly distributions from its cash available for distribution, which consists of the Fund’s dividends and

interest income after payment of Fund expenses, net option premiums and net realized and unrealized gains on investments. Such quarterly

distributions may also consist of return of capital. Under the Managed Distribution Policy, the Fund may make periodic distributions

of long-term capital gains more frequently than once per taxable year. Distributions are recorded on the ex-dividend date. Distributions

are determined annually in accordance with federal tax regulations, which may differ from GAAP for investment companies.

The

tax treatment and characterization of the Fund’s distributions may vary significantly from time to time depending on whether the

Fund has gains or losses on the call options written in its portfolio versus gains or losses on the equity securities in the portfolio.

Each quarter, the Fund will provide disclosures with distribution payments made that estimate the percentages of that distribution that

represent net investment income, other income or capital gains, and return of capital, if any. The final composition of the tax characteristics

of the distributions cannot be determined with certainty until after the end of the Fund’s tax year, and will be reported to shareholders

at that time. A significant portion of the Fund’s distributions may constitute a return of capital. The amount of quarterly distributions

will vary, depending on a number of factors. As portfolio and market conditions change, the rate of dividends on the common shares will

change. There can be no assurance that the Fund will be able to declare a dividend in each period.

E.

Federal Income Taxes.

It is the policy of the Fund to comply with the requirements of subchapter M of the Internal Revenue Code that are applicable to regulated

investment companies and to distribute substantially all of its net investment income and any net realized capital gains to its shareholders.

Therefore, a federal income tax or excise tax provision is not required. Management has considered the sustainability of the Fund’s

tax positions taken on federal income tax returns for all open tax years in making this determination. The Fund may utilize equalization

accounting for tax purposes, whereby a portion of redemption payments are treated as distributions of income or gain.

F.

Use of Estimates. The

preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported

amounts of assets and liabilities and disclosure of contingent

assets

and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations

during the reporting period. Actual results could differ from those estimates.

G.

Risk Exposures and the Use of Derivative

Instruments. The Fund’s investment objectives

permit the Fund to enter into various types of derivatives contracts, including, but not limited to, forward foreign currency exchange

contracts and purchased and written options. In doing so, the Fund will employ strategies in differing combinations to permit it to increase

or decrease the level of risk, or change the level or types of exposure to risk factors. This may allow the Fund to pursue its objectives

more quickly and efficiently, than if it were to make direct purchases or sales of securities capable of affecting a similar response

to market or credit factors.

In

pursuit of its investment objectives, the Fund may seek to increase or decrease its exposure to the following market or credit risk factors:

Credit

Risk. The price of a bond or other debt instrument is likely to fall if the issuer’s actual or perceived financial health

deteriorates, whether because of broad economic or issuer-specific reasons. In certain cases, the issuer could be late in paying interest

or principal, or could fail to pay its financial obligations altogether.

Equity

Risk. Stock prices may be volatile or have reduced liquidity in response to real or perceived impacts of factors including, but

not limited to, economic conditions, changes in market interest rates, and political events. Stock markets tend to be cyclical, with

periods when stock prices generally rise and periods when stock prices generally decline. Any given stock market segment may remain out

of favor with investors for a short or long period of time, and stocks as an asset class may underperform bonds or other asset classes

during some periods. Additionally, legislative, regulatory or tax policies or developments in these areas may adversely impact the investment

techniques available to a manager, add to costs and impair the ability of the Fund to achieve its investment objectives.

Foreign

Exchange Rate Risk. To the extent that the Fund invests directly in foreign (non-U.S.) currencies or in securities denominated

in, or that trade in, foreign (non-U.S.) currencies, it is subject to the risk that those foreign (non-U.S.) currencies will decline

in value relative to the U.S. dollar or, in the case of hedging positions, that the U.S. dollar will decline in value relative to the

currency being hedged by the Fund through foreign currency exchange transactions.

Currency

rates may be affected by changes in market interest rates, intervention (or the failure to intervene) by U.S. or foreign governments,

central banks or supranational

NOTES

TO FINANCIAL STATEMENTS As OF FEBRUARY

29, 2024 (CONTINUED)

NOTE

2 — SIGNIFICANT ACCOUNTING POLICIES

(continued)

entities

such as the International Monetary Fund, by the imposition of currency controls, or other political or economic developments in the United

States or abroad.

Interest

Rate Risk. Changes in short-term market interest rates will directly affect the yield on Common Shares. If short-term market

interest rates fall, the yield on Common Shares will also fall. To the extent that the interest rate spreads on loans in the Fund’s

portfolio experience a general decline, the yield on the Common Shares will fall and the value of the Fund’s assets may decrease,

which will cause the Fund’s NAV to decrease. Conversely, when short-term market interest rates rise, because of the lag between

changes in such short-term rates and the resetting of the floating rates on assets in the Fund’s portfolio, the impact of rising

rates will be delayed to the extent of such lag. With respect to investments in fixed rate instruments, a rise in market interest rates

generally causes values of such instruments to fall. The values of fixed rate instruments with longer maturities or duration are more

sensitive to changes in market interest rates.

As

of the date of this report, the United States experiences a rising market interest rate environment, which may increase the Fund’s

exposure to risks associated with rising market interest rates. Rising market interest rates have unpredictable effects on the markets

and may expose fixed-income and related markets to heightened volatility which could reduce liquidity for certain investments, adversely

affect values, and increase costs. If dealer capacity in fixed-income and related markets is insufficient for market conditions, it may

further inhibit liquidity and increase volatility in the fixed-income and related markets. Further, recent and potential changes in government

policy may affect interest rates.

Risks

of Investing in Derivatives. The Fund’s use of derivatives can result in losses due to unanticipated changes in the market

or credit risk factors and the overall market. In instances where the Fund is using derivatives to decrease, or hedge, exposures to market

or credit risk factors for securities held by the Fund, there are also risks that those derivatives may not perform as expected, resulting

in losses for the combined or hedged positions.

Derivative

instruments are subject to a number of risks, including the risk of changes in the market price of the underlying securities, credit

risk with respect to the counterparty, risk of loss due to changes in market interest rates and liquidity and volatility risk. The amounts

required to purchase certain derivatives may be small relative to the magnitude of exposure assumed by the Fund. Therefore, the purchase

of certain derivatives may have an economic leveraging effect on the Fund and exaggerate any increase

or

decrease in the NAV. Derivatives may not perform as expected, so the Fund may not realize the intended benefits. When used for hedging

purposes, the change in value of a derivative may not correlate as expected with the currency, security or other risk being hedged. When

used as an alternative or substitute for direct cash investments, the return provided by the derivative may not provide the same return

as direct cash investment. In addition, given their complexity, derivatives expose the Fund to the risk of improper valuation.

Generally,

derivatives are sophisticated financial instruments whose performance is derived, at least in part, from the performance of an underlying

asset or assets. Derivatives include, among other things, swap agreements, options, forwards and futures. Investments in derivatives

are generally negotiated over-the-counter (“OTC”) with a single counterparty and as a result are subject to credit risks

related to the counterparty’s ability or willingness to perform its obligations; any deterioration in the counterparty’s

creditworthiness could adversely affect the value of the derivative. In addition, derivatives and their underlying securities may experience

periods of illiquidity which could cause the Fund to hold a security it might otherwise sell, or to sell a security it otherwise might

hold at inopportune times or at an unanticipated price. A manager might imperfectly judge the direction of the market. For instance,

if a derivative is used as a hedge to offset investment risk in another security, the hedge might not correlate to the market’s

movements and may have unexpected or undesired results such as a loss or a reduction in gains.

Counterparty

Credit Risk and Credit Related Contingent Features. Certain derivative positions are subject to counterparty credit risk, which

is the risk that the counterparty will not fulfill its obligation to the Fund. The Fund’s derivative counterparties are financial

institutions who are subject to market conditions that may weaken their financial position. The Fund intends to enter into financial

transactions with counterparties that it believes to be creditworthy at the time of the transaction. To reduce this risk, the Fund generally

enters into master netting arrangements, established within the Fund’s International Swap and Derivatives Association, Inc. (“ISDA”)

Master Agreements (“Master Agreements”). These agreements are with select counterparties and they govern transactions, including

certain OTC derivative and forward foreign currency contracts, entered into by the Fund and the counterparty. The Master Agreements maintain

provisions for general obligations, representations, agreements, collateral, and events of default or termination. The occurrence of

a specified event of termination may give a counterparty the right to terminate all of its contracts and affect settlement of all outstanding

transactions under the applicable Master Agreement.

NOTES

TO FINANCIAL STATEMENTS As OF FEBRUARY

29, 2024 (CONTINUED)

NOTE

2 — SIGNIFICANT ACCOUNTING POLICIES

(continued)

The

Fund may also enter into collateral agreements with certain counterparties to further mitigate counterparty credit risk associated with

OTC derivative and forward foreign currency contracts. Subject to established minimum levels, collateral is generally determined based

on the net aggregate unrealized gain or loss on contracts with a certain counterparty. Collateral pledged to the Fund is held in a segregated

account by a third-party agent and can be in the form of cash or debt securities issued by the U.S. government or related agencies.

As

of February 29, 2024, the maximum amount of loss the Fund would incur if the counterparties to its derivative transactions failed to

perform would be $1,089,157 which represents the gross payments to be received by the Fund on open forward foreign currency contracts

were they to be unwound as of February 29, 2024. As of February 29, 2024, the Fund did not receive any cash collateral for its open OTC

derivative transactions.

The

Fund’s master agreements with derivative counterparties have credit related contingent features that if triggered would allow its

derivatives counterparties to close out and demand payment or additional collateral to cover their exposure from the Fund. Credit related

contingent features are established between the Fund and its derivatives counterparties to reduce the risk that the Fund will not fulfill

its payment obligations to its counterparties. These triggering features include, but are not limited to, a percentage decrease in the

Fund’s net assets and/or a percentage decrease in the Fund’s NAV, which could cause the Fund to accelerate payment of any

net liability owed to the counterparty. The contingent features are established within the Fund’s Master Agreements.

Written

options by the Fund do not give rise to counterparty credit risk, as written options obligate the Fund to perform and not the counterparty.

As of February 29, 2024, the Fund had a liability position of $1,428,806 on open forward foreign currency contracts and written options

with credit related contingent features. If a contingent feature would have been triggered as of February 29, 2024, the Fund could have

been required to pay this amount in cash to its counterparties. As of February 29, 2024, the Fund had pledged $1,360,000 in cash collateral

for its open OTC derivatives transactions. There were no credit events during the year ended February 29, 2024 that triggered any credit

related contingent features.

H.

Forward Foreign Currency Contracts and Futures Contracts. The Fund may enter into forward foreign currency contracts primarily

to hedge against foreign currency exchange rate risks on its non-U.S. dollar denominated investment securities. When entering into a

forward foreign

currency

contract, the Fund agrees to receive or deliver a fixed quantity of foreign currency for an agreed-upon price on an agreed future date.

These contracts are valued daily and the Fund’s net equity therein, representing unrealized gain or loss on the contracts as measured

by the difference between the forward foreign exchange rates at the dates of entry into the contracts and the forward rates at the reporting

date, is included in the statement of assets and liabilities. Realized and unrealized gains and losses on forward foreign currency contracts

are included on the Statement of Operations. These instruments involve market and/or credit risk in excess of the amount recognized in

the statement of assets and liabilities. Risks arise from the possible inability of counterparties to meet the terms of their contracts

and from movement in currency and securities values and interest rates.

During

the year ended February 29, 2024, the Fund used forward foreign currency contracts to hedge its investments in non-U.S. dollar denominated

equity securities in an attempt to decrease the volatility of the Fund’s NAV.

During

the year ended February 29, 2024, the Fund had average contract amounts on forward foreign currency contracts to buy and sell of $832,778

and $42,368,679, respectively. Please refer to the table within the Portfolio of Investments for open forward foreign currency contracts

at February 29, 2024.

The

Fund may enter into futures contracts involving foreign currency, interest rates, securities and securities indices. A futures contract

is a commitment to buy or sell a specific amount of a financial instrument at a negotiated price on a stipulated future date. The Fund

may buy and sell futures contracts. Futures contracts traded on a commodities or futures exchange will be valued at the final settlement

price or official closing price on the principal exchange as reported by such principal exchange at its trading session ending at, or

most recently prior to, the time when the Fund’s assets are valued.

Upon

entering into a futures contract, the Fund is required to deposit either cash or securities (initial margin) in an amount equal to a

certain percentage of the contract value. Subsequent payments (variation margin) are made or received by the Fund each day. The variation

margin payments are equal to the daily changes in the contract value and are recorded as unrealized gains and losses and, if any, shown

as variation margin receivable or payable on futures contracts on the Statement of Assets and Liabilities. Open futures contracts are

reported on a table following the Fund’s Portfolio of Investments. Securities held in collateralized accounts to cover initial

margin requirements on open futures contracts are footnoted in the Portfolio of Investments. Cash collateral held by the broker to cover

initial margin requirements on open futures contracts are

NOTES

TO FINANCIAL STATEMENTS As OF FEBRUARY

29, 2024 (CONTINUED)

NOTE

2 — SIGNIFICANT ACCOUNTING POLICIES

(continued)

noted

in the Fund’s Statement of Assets and Liabilities. The net change in unrealized appreciation and depreciation is reported in the

Fund’s Statement of Operations. Realized gains (losses) are reported in the Fund’s Statement of Operations at the closing

or expiration of futures contracts.

Futures

contracts are exposed to the market risk factor of the underlying financial instrument. The Fund purchases and sells futures contracts

on various equity indices to enable the Fund to make market directional tactical decisions to enhance returns, to protect against a decline

in its assets or as a substitute for the purchase or sale of equity securities. Additional associated risks of entering into futures

contracts include the possibility that there may be an illiquid market where the Fund is unable to liquidate the contract or enter into

an offsetting position and, if used for hedging purposes, the risk that the price of the contract will correlate imperfectly with the

prices of the Fund’s securities. With futures, there is minimal counterparty credit risk to the Fund since futures are exchange

traded and the exchange’s clearinghouse, as counterparty to all exchange traded futures, guarantees the futures against default.

The

Fund did not enter into any futures contracts during the year ended February 29, 2024.

I.

Options Contracts. The Fund may purchase put and call options and may write (sell) put options and covered call options.

The premium received by the Fund upon the writing of a put or call option is included in the Statement of Assets and Liabilities as a

liability which is subsequently marked-to-market until it is exercised or closed, or it expires. The Fund will realize a gain or loss

upon the expiration or closing of the option contract. When an option is exercised, the proceeds on sales of the underlying security

for a written call option or purchased put option or the purchase cost of the security for a written put option or a purchased call option

is adjusted by the amount of premium received or paid. The risk in writing a call option is that the Fund gives up the opportunity for

profit if the market price of the security increases and the option is exercised. The risk in buying an option is that the Fund pays

a premium whether or not the option is exercised. Risks may also arise from an illiquid secondary market or from the inability of counterparties

to meet the terms of the contract.

The

Fund generates premiums and seeks gains by writing call options on indices on a portion of the value of the equity. During the year ended

February 29, 2024, the Fund had an average notional amount of $75,771,764. Please refer to the table within the Portfolio of Investments

for open written options contracts at February 29, 2024.

J.

Indemnifications. In the normal course of business, the Fund may enter into contracts that provide certain indemnifications.

The Fund’s maximum exposure under these arrangements is dependent on future claims that may be made against the Fund and, therefore,

cannot be estimated; however, based on experience, management considers risk of loss from such claims remote.

NOTE 3 —

INVESTMENT TRANSACTIONS

The

cost of purchases and the proceeds from sales of investments for the year ended February 29, 2024, excluding short-term securities, were

$111,568,076 and $125,999,086, respectively.

NOTE 4 —

INVESTMENT MANAGEMENT FEES

The

Fund has entered into an investment management agreement (“Management Agreement”) with the Investment Adviser. The Investment

Adviser has overall responsibility for the management of the Fund. The Investment Adviser oversees all investment management and portfolio

management services for the Fund and assists in managing and supervising all aspects of the general day-to-day business activities and

operations of the Fund, including custodial, transfer agency, dividend disbursing, accounting, auditing, compliance and related services.

This Management Agreement compensates the Investment Adviser with a management fee, payable monthly, based on an annual rate of 0.85%

of the Fund’s average daily managed assets. For purposes of the Management Agreement, managed assets are defined as the Fund’s

average daily gross asset value, minus the sum of the Fund’s accrued and unpaid dividends on any outstanding preferred shares and

accrued liabilities (other than liabilities for the principal amount of any borrowings incurred, commercial paper or notes issued by

the Fund and the liquidation preference of any outstanding preferred shares). As of February 29, 2024, there were no preferred shares

outstanding.

The

Investment Adviser has entered into a sub-advisory agreement with Voya IM. Voya IM provides investment advice for the Fund and is paid

by the Investment Adviser based on the average daily managed assets of the Fund. Subject to policies as the Board or the Investment Adviser

may determine, Voya IM manages the Fund’s assets in accordance with the Fund’s investment objectives, policies and limitations.

NOTE 5 —

EXPENSE LIMITATION AGREEMENT

The

Investment Adviser has entered into a written expense limitation agreement (“Expense Limitation Agreement”) with the Fund

under which it will limit the expenses of the Fund, excluding interest, taxes, investment-related costs,

NOTES