UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 8-K

CURRENT

REPORT

PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

Date of Report (Date of earliest event reported): January 4, 2024

Lions Gate Entertainment Corp.

(Exact name of registrant as specified in charter)

British

Columbia, Canada

(State or Other Jurisdiction of Incorporation)

|

|

|

| 1-14880 |

|

N/A |

| (Commission

File Number) |

|

(IRS Employer

Identification No.) |

(Address of principal executive offices)

250 Howe Street 20th Floor

Vancouver, British Columbia V6C 3R8

and

2700 Colorado Avenue

Santa Monica, California 90404

Registrant’s telephone number, including area code: (877) 848-3866

No Change

(Former name

or former address, if changed since last report)

Check the appropriate box below

if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ☐ |

Written Communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ☒ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17

CFR 240.14a-12) |

| ☐ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ☐ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the

Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the

Act:

|

|

|

|

|

| Title of Each Class |

|

Trading

Symbol(s) |

|

Name of Each Exchange

on Which Registered |

| Class A Voting Common Shares, no par value per share |

|

LGF.A |

|

New York Stock Exchange |

| Class B Non-Voting Common Shares, no par value per share |

|

LGF.B |

|

New York Stock Exchange |

Indicate by check mark whether the registrant is an emerging growth company as defined in as defined in Rule 405 of the

Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ☐

If an emerging

growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange

Act. ☐

| Item 7.01. |

Regulation FD. |

On January 4, 2024, Lions Gate Entertainment Corp. held an investor presentation conference call in connection with a proposed business combination

involving its studio business and Screaming Eagle Acquisition Corp. A transcript of the call, and an updated investor presentation referenced in the transcript and used during the call, are each being furnished with this Current Report on Form 8-K as Exhibit 99.1 and 99.2, respectively, each of which is incorporated by reference herein.

The information set

forth in this Item 7.01 of this Current Report on Form 8-K is being furnished and shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the

“Exchange Act”), nor shall it be deemed incorporated by reference in any filing under the Securities Act of 1933, as amended, or the Exchange Act, except as shall be expressly set forth by specific reference in such a filing.

| Item 9.01 |

Financial Statements and Exhibits. |

(d) Exhibits

|

|

|

| Exhibit

No. |

|

Description of Exhibits |

|

|

| 99.1 |

|

Transcript of investor presentation conference call, dated January 4, 2024 |

|

|

| 99.2 |

|

Investor Presentation, dated January 4, 2024 |

|

|

| 104 |

|

Cover Page Interactive Data File (embedded within the Inline XBRL document) |

[End of Communication]

Additional Information and Where to Find It

In

connection with the proposed transactions, SEAC II Corp. (“New SEAC”), a subsidiary of Screaming Eagle Acquisition Corp. (“SEAC”) intends to file with the SEC a registration statement on Form S-4, which will include a preliminary

proxy statement of SEAC and a preliminary prospectus of New SEAC, and after the registration statement is declared effective, SEAC will mail the definitive proxy statement/prospectus relating to the proposed transactions to SEAC’s shareholders

and public warrant holders as of the respective record dates to be established for voting at the SEAC shareholders meeting and the SEAC public warrant holders meeting. The registration statement, including the proxy statement/prospectus contained

therein, will contain important information about the proposed transactions and the other matters to be voted upon at SEAC shareholders meeting and the SEAC public warrant holders meeting. This communication does not contain all the information that

should be considered concerning the proposed transactions and other matters and is not intended to provide the basis for any investment decision or any other decision in respect of such matters. SEAC, New SEAC and Lionsgate may also file other

documents with the SEC regarding the proposed transactions. SEAC’s shareholders, public warrant holders and other interested persons are advised to read, when available, the registration statement, including the preliminary proxy

statement/prospectus contained therein, the amendments thereto and the definitive proxy statement/prospectus and other documents filed in connection with the proposed transactions, as these materials will contain important information about SEAC,

New SEAC, Lionsgate, the studio business and the proposed transactions. SEAC’s shareholders, public warrant holders and other interested persons will be able to obtain copies of the Registration Statement, including the preliminary proxy

statement/prospectus contained therein, the definitive proxy statement/prospectus and other documents filed or that will be filed with the SEC, free of charge, by SEAC, New SEAC and Lionsgate through the website maintained by the SEC at www.sec.gov.

Participants in the Solicitation

SEAC, New SEAC,

Lionsgate, LG Orion Holdings Inc. (“StudioCo”) and their respective directors and officers may be deemed participants in the solicitation of proxies of SEAC shareholders and public warrant holders in connection with the proposed

transactions. more detailed information regarding the directors and officers of SEAC, and a description of their interests in SEAC, is contained in SEAC’s filings with the SEC, including its Annual Report on Form 10-K for the fiscal

year ended December 31, 2022, which was filed with the SEC on March 1, 2023, and is available free of charge at the SEC’s website at www.sec.gov. Information regarding the persons who may, under SEC rules, be deemed participants in

the solicitation of proxies of SEAC’s shareholders and public warrant holders in connection with the proposed transactions and other matters to be voted upon at the SEAC shareholders meeting and the SEAC public warrant holders meeting will be

set forth in the registration statement for the proposed transactions when available.

Forward-Looking Statements

This communication includes certain statements that may constitute “forward-looking statements” within the meaning of Section 27A of the

Securities Act, and Section 21E of the Exchange Act. Forward-looking statements include, but are not limited to, statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any

underlying assumptions. The words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intends,” “may,” “might,” “plan,”

“possible,” “potential,” “predict,” “project,” “seek,” “should,” “target,” “would” and similar expressions may identify forward-looking statements, but the absence of

these words does not mean that a statement is not forward-looking. Forward-looking statements may include, for example, statements about SEAC or Lionsgate’s ability to effectuate the proposed transactions discussed in this document; the

benefits of the proposed transactions; the future financial performance of the go-forward public company following the completion of the proposed transactions (“Pubco”) following the proposed transactions; changes in

Lionsgate’s strategy, future operations, financial position, estimated revenues and losses, projected costs, prospects, plans and objectives of management. These forward-looking statements are based on information available as of the date of

this document, and current expectations, forecasts and assumptions, and involve a number of judgments, risks and uncertainties. Accordingly, forward-looking statements should not be relied upon as representing SEAC, Lionsgate, StudioCo or New

SEAC’s views as of any subsequent date, and none

of SEAC, Lionsgate, StudioCo or New SEAC undertakes any obligation to update forward-looking statements to reflect events or circumstances after the date they were made, whether as a result of

new information, future events or otherwise, except as may be required under applicable securities laws. Neither Lionsgate, StudioCo, New SEAC nor SEAC gives any assurance that any of New SEAC, StudioCo, Pubco or SEAC will achieve its expectations.

You should not place undue reliance on these forward-looking statements. As a result of a number of known and unknown risks and uncertainties, Pubco’s actual results or performance may be materially different from those expressed or implied by

these forward-looking statements. Some factors that could cause actual results to differ include: (i) the timing to complete the proposed transactions by SEAC’s business combination deadline and the potential failure to obtain an extension

of the business combination deadline if sought by SEAC; (ii) the occurrence of any event, change or other circumstances that could give rise to the termination of the definitive agreements relating to the proposed transactions; (iii) the

outcome of any legal, regulatory or governmental proceedings that may be instituted against Pubco, SEAC, Lionsgate, StudioCo or New SEAC or any investigation or inquiry following announcement of the proposed transactions, including in connection

with the proposed transactions; (iv) the inability to complete the proposed transactions due to the failure to obtain approval of SEAC’s shareholders or public warrant holders; (v) Lionsgate’s and Pubco’s success in

retaining or recruiting, or changes required in, its officers, key employees or directors following the proposed transactions; (vi) the ability of the parties to obtain the listing of Pubco Common Shares on Nasdaq or another stock exchange upon

the Closing; (vii) the risk that the proposed transactions disrupts current plans and operations of Lionsgate; (viii) the ability to recognize the anticipated benefits of the proposed transactions; (ix) unexpected costs related to the

proposed transactions; (x) the amount of redemptions by SEAC’s public shareholders being greater than expected; (xi) the management and board composition of Pubco following completion of the proposed transactions; (xii) limited

liquidity and trading of Pubco’s securities following completion of the proposed transactions; (xiii) changes in domestic and foreign business, market, financial, political and legal conditions; (xiv) the possibility that Lionsgate,

StudioCo, Pubco, New SEAC or SEAC may be adversely affected by other economic, business, and/or competitive factors; (xv) operational risks; (xvi) litigation and regulatory enforcement risks, including the diversion of management time and

attention and the additional costs and demands on Lionsgate’s resources; (xvii) the risk that the consummation of the proposed transactions is substantially delayed or does not occur; and (xviii) other risks and uncertainties

indicated from time to time in the registration statement, including those under “Risk Factors” therein, and in the other filings of SEAC, Lionsgate, StudioCo, New SEAC and Pubco with the SEC.

No Offer or Solicitation

This communication relates

to a proposed transaction between Lionsgate and SEAC. This document does not constitute a solicitation of a proxy, consent or authorization with respect to any securities or in respect of the proposed transactions. This document does not constitute

an offer to sell or exchange, or the solicitation of an offer to buy or exchange, any securities, nor shall there be any offer, sale or exchange of securities in any state or jurisdiction in which such offer, solicitation, sale or exchange would be

unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offering of securities will be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act or an

exemption therefrom. No securities commission or securities regulatory authority in the United States or any other jurisdiction has in any way passed upon the merits of the transaction or the accuracy or adequacy of this communication.

Signature

Pursuant to the requirements of the Securities Exchange Act of 1934, as amended, the Registrant has duly caused this report to be signed on its behalf by the

undersigned hereunto duly authorized.

Date: January 5, 2024

|

|

|

| LIONS GATE ENTERTAINMENT CORP. |

| (Registrant) |

|

|

| By: |

|

/s/ James W. Barge |

| Name: |

|

James W. Barge |

| Title: |

|

Chief Financial Officer |

Exhibit 99.1

Included below is a transcript of the investor presentation conference call held by Lions Gate Entertainment Corp. (“Lionsgate”) on

January 4, 2024, in connection with the proposed business combination involving Screaming Eagle Acquisition Corp. (“Screaming Eagle”) and Lionsgate, pursuant to the terms of that certain Business Combination Agreement, dated as of

December 22, 2023.

An updated investor presentation referenced in the transcript and used during the call is also included below.

Call Transcript

Operator: Good afternoon

and welcome to the Lionsgate Studios Transaction Conference Call. All participants will be in listen-only mode. After today’s presentation, there will be an opportunity to ask questions. Please note this event is being recorded. I would now

like to turn the conference call over to Nilay Shah, Head of Investor Relations. Please go ahead.

Nilay Shah: Good afternoon. The matters

discussed on this call include the proposed business combination of our motion picture group and television studio segments and our film and television library with Screaming Eagle Acquisition Corp. to launch Lionsgate Studios. We urge you to read

the relevant materials that we and Screaming Eagle have filed and will file with the SEC, including in our Form 8-K, filed on December 22, 2023, and a registration statement on Form S-4 to be filed with the SEC. That will include a preliminary prospectus/proxy statement. The information in the prospectus/proxy statement will not be complete and may be changed. You can find these materials and

other documents filed and to be filed with the SEC free of charge at the SEC’s website, at sec.gov or on our Investor Relations website.

The matters

discussed on this call also include forward looking statements, including those regarding the performance of future fiscal years. Such statements are subject to a number of risks and uncertainties. Actual results could differ materially and

adversely from those described in the forward-looking statements as a result of various factors. This includes the risk factors set forth in Lionsgate’s most recent annual report on Form 10-K as amended

in our most recent quarterly report on Form 10-Q filed with the SEC and in the Form S-4 to be filed with the SEC.

The company undertakes no obligation to publicly release the results of any revisions to these forward-looking statements that may be made to reflect any

future events or circumstances. Moreover, Lionsgate, its subsidiary, LG Orion Holdings, our Directors, Executive officers and certain other employees and other persons may be deemed to be participants in the solicitation of proxies from shareholders

of Screaming Eagle in favor of the proposed business combination under SEC rules.

Information about participants and their direct and indirect interests

will be included in the prospectus/proxy statement and the relevant and the other relevant documents filed with the SEC as available. No offer to sell or solicitation of an offer to buy securities will be made except pursuant to an effective Form S-4 or an exemption.

I’ll now turn the call over to Jon.

Jon Feltheimer: Thank you, Nilay, and good afternoon, everyone. Thank you for joining us. I hope you had an enjoyable holiday. I want to welcome the

analysts and current shareholders who are familiar with our company, as well as those investors who may be new to Lionsgate’s story. We wrapped up the calendar year with three strategic initiatives designed to enhance our studio business. The

acquisition of the global content platform eOne adding thousands of titles to our film and television library. And strengthening our scripted and unscripted television business. And additional equity investment in leading talent management and

production company 3 Arts Entertainment as it continues its strong and profitable growth.

And our launch of Lionsgate Studios as one of the world’s largest publicly traded, pure play standalone

content companies in a transaction that we expect to close in the spring. I’ll begin by framing the opportunity and rationale for the Lionsgate Studios transaction. While you may have seen the investor presentation regarding the transaction on

our website, Michael will take you through an updated version of the slides and Jimmy will drill down on the transaction structure itself along with our Fiscal 2025 financial outlook we provided for Lionsgate Studios.

We had a number of options available for executing this step in our overall strategic plan. We believe that we selected the best option for aligning with our

goal of a full separation, raising capital efficiently with substantial proceeds available to de-lever and establishing an appropriate valuation for our studio supported by blue chip investors. Several

considerations drove the rationale for this transaction.

First, the structure basically replicates a subsidiary IPO, but with a few distinct advantages.

We were able to launch Lionsgate Studios on a tighter and more defined timeline and provide certainty by setting a fixed valuation, anchoring the $175 million equity commitment.

Second, upon completion, this transaction enables us to raise $350 million of total proceeds to accelerate deleveraging and to facilitate strategic

initiatives like the eOne acquisition and the increased position in 3 Arts.

As today’s presentation will show, the combination of a pure play studio

and a strong balance sheet will be a key driver in continuing to grow shareholder value.

Third, by separating the studio with a single class of shares,

we’re executing on an investor priority by isolating the value of one of the only pure play studios in the market today. We believe this transaction sets a valuation for the studio and increases our strategic optionality as we move towards

separation.

Finally, the transaction will not limit the studio’s ongoing working relationship with Starz, which remains a wholly owned subsidiary of

parent company Lionsgate. Starz will have the ability to continue strengthening its position as a profitable premium platform with a domestic content strategy focused on valuable core demos, a largely digital subscriber base and a continued reliable

supply of content from the Lionsgate television and motion picture groups.

In that regard, I’m pleased to report that Starz continued its domestic

OTT subscriber growth in the quarter. In closing, when Michael and I started running the company more than 20 years ago, we place a bet on the enduring value of great intellectual property. Today, our content businesses are thriving with more buyers

and more options for monetizing our content than ever before. We finish the calendar year with our first $1 billion plus year at the worldwide box office since 2019, driven by successful new chapters of three of our biggest franchises. Strong

and growing profitability in our television group. And a film and television library that is approaching $900 million in trailing 12-month revenue.

The continued strength of our content business underlies the Fiscal 2025 Lionsgate Studio’s financial outlook that Jimmy will discuss. But first,

I’ll turn the presentation over to Michael.

Michael Burns: Thanks, Jon. While many of you on this call know the Lionsgate Studio story quite

well, I wanted to give a brief overview of why we believe a standalone Lionsgate Studios will make a highly attractive equity investment. While you may have seen the full investor presentation that we shared when we announced the transaction, please

see the updated January 4th conference call slide deck on the events portion of our IRR website for an updated version of slides that Jimmy and I will be referring to.

Let’s start with slide number 4. This transaction is about separating the Studio and Starz, which we strongly believe will unlock significant shareholder

value by enabling direct investment in the studio with a single class of stock. I’ll be discussing a few metrics to demonstrate why Lionsgate Studios is positioned so well in this environment. Jimmy will speak later about the outlook, but

clearly we are seeing strength in our business beyond fiscal year 2024 as shown with the double-digit OIBDA growth for Studio in Fiscal 2025.

Library our growing high margin, perhaps the most important asset of the company continues to do well. We

are selling a minority stake in a studio at 10.7 times multiple, which establishes the initial studio value and gets us poised for full separation. We’re about content, content and content, specifically premium content in our motion picture and

television businesses that ultimately bolsters our library.

Let’s turn to the next slide number 5, which drill downs on our studio business. Our

business is propelled by three primary drivers. Our motion pictures studio, which releases 40 to 50 titles per year, ranging from the recognizable franchise films such as John Wick and Hunger Games to

mid-range budget films like Plane to small budget indie films. Motion Picture generated $1.6 billion in revenue over the past 12-months. Our television

studio, which is producing over 80 series for 50 networks across all major streamers and broadcasters, covers the entire gamut with capabilities across scripted, unscripted and syndicated programming.

Our television business generated $1.5 billion in revenue over the past 12 months, and our library and distribution group, which distributes over 20,000

plus pieces of content across film and television to all sorts of global buyers, whether SVOD, AVOD, linear, fast or cable channels. Revenue from our library is included in our motion picture and television revenue and it’s important to

highlight that our library generated $870 million in revenue over the last 12 months.

So what’s driving this? Over time, our strategy has

evolved, but the key tenets of why we are different can be broken down to two primary drivers. We are different because we focus on maximizing monetization of content rather than being beholden to a consumer-driven streaming or television network

business. While Lionsgate Studios and will continue to have a very strong relationship with Starz, our content creation strategy is 100% focused on driving the highest returns on each item of content, rather than serving as a funnel for an own

streaming or television platform. This ensures we maximize returns on all of our spend, while a number of our peers are primarily using their studio business as a conduit to try to prop up their DTC streaming businesses. This goes for our library

content as well.

We de-risk the film business via international licenses. As I’ll discuss on the next slide,

we have a very high hit rate on making profitable films. This stems from the fact that we only take box office marketing and P&A risk in a few key markets, including the United States, Canada, the U.K. and Latin America. Everywhere else, we

license the films rights to regional or global buyers that take on the distribution marketing spend for that market. Let’s take a closer look at our model on Slide 6.

Our pure content strategy has led others to call us a benevolent arms dealer, which is a moniker we embrace. As you can see on the next slide, number 7, the

universe of licensees for our arms, AKA content, is expanding rapidly. This list shouldn’t be surprising. We sell to everyone Netflix, Amazon, Apple, HBO to name a few.

Jon mentioned our positioning with AVOD, SVOD, fast broadcast, et cetera. Our size, scope and independence allows us to work with everyone and we expect that

list to grow. If I could give one reason why we can compete and thrive, it would be our library, our crown jewel. Now let’s move on to the next slide number 8, which provides an overview of the key pieces of IP that make up our portfolio of

motion picture television and library content.

Obviously, some big franchises in here like the aforementioned Hunger Games and John Wick,

but also Twilight, Saw, Mad Men, Orange is the New Black and the Power Series. We never rest after a hit. We are always looking at new ways to exploit key franchises and keep the fan base engaged in new ways. You

may have seen that in the same year we had a successful John Wick 4 release from our motion picture team. We also released the Continental, a John Wick prequel television series, which was one of Peacock’s top originals in

2023. Besides theatrical revenue for these titles, we obviously have sequels, remakes, IP expansion through merchandise, location based theme parks and symbiotic alliances with companies like Blumhouse in the Horror Space.

Next on Slide 9, which covers some of Lionsgate’s film returns besides new content, we have key repeatable franchises with a risk mitigated model,

enabling us to produce compelling financial returns. We produce 10 plus wide releases theatrically a year, and historically, 74% of these titles are profitable, which we believe is well ahead of the industry average. As you can see, we produce and

distribute a great number of theatrical films every year. I’d be remiss if I didn’t mention the optionality this gives us to capture lightning in a bottle like we did with our biggest franchises over the last few years. Twilight,

Hunger Games, Now You See Me and John Wick. Additionally, we have a less understood but highly compelling business we call multiplatform. This is where we buy and distribute 30 to 40 low budget films while utilizing our scaled

theatrical home entertainment and library distribution infrastructure. Since fiscal 2020, 93% of our multiplatform film releases ended up being profitable to Lionsgate Studios, with above average returns.

So clearly, we have a movie business model that works well and provides a blend a balance between

profitability, growth and risk. The vast majority of these pictures come with worldwide rights in perpetuity. But how do we know that will continue? Let’s take a look at Slide 10, which discusses our pipeline. Of course, no studio can rest on

laurels and past successes. We are still going to be judged on our future releases and on this topic we really like how the pipeline for our motion picture and television group is shaping up over the next few years. As you’ll see, a lot of

compelling projects are in the slate. We’re very excited about our first John Wick spinoff, Ballerina later this calendar year. We have already dated the next Saw film, some other highly anticipated films in the next few years,

including Now You See Me 3, Highlander and the much-anticipated Michael Jackson biopic, just to name a few.

Turning to Slide 11, we take a

look at the television pipeline, a really strong lineup across streaming, particularly at Apple and Starz, as well as broadcast where the CBS comedy Ghosts has become a breakout hit. And the number one comedy on the network. The addition of

eOne provides two big franchises to our TV studio, including The Rookie, which is returning for its sixth season in 2024 on ABC and Yellowjackets, which is a hit show for Paramount Plus. You can read more detail about eOne on Slide 17

of the deck filed at the time of our transaction on December 22nd last year.

eOne is right in our wheelhouse. We paid around six times adjusted

post-synergy better for a bolt-on acquisition that we will leverage into our existing television production and library distribution infrastructure. Mythic Quest, a

co-production with Lionsgate Television, is a great example of why we invested in 3 Arts, the best-in-class management company

that takes us to Slide 12. Film Television 3 Arts serve as a three-legged stool, providing an enormous content annuity stream. 3 Arts is one of the industry’s premier talent management and production companies. Lionsgate first took a 51% stake

in 3 Arts back in 2018, and it turned out to be a terrific investment.

Earlier this week, we increased our stake significantly. The relationship between

Lionsgate Television 3 Arts since our 2018, investment has grown stronger over the years, with 3 Arts adjusted OIBDA increasing by 2X from fiscal 2019 to fiscal year 2023. With the strikes now behind us, we expect 3 Arts to continue to be a strong

contributor as we enter fiscal 2025 with some of their upcoming co-productions with Lionsgate, including Hunting Wives and Serpent Queen remain perfect examples of the strength of 3 Arts and the

Studio’s relationship.

The three legs of the stool are supported by our library foundation. Please turn to slide number 13 to dive deeper into our

library, which is growing nicely at 12.5% CAGR and approaching $900 million on the top line. Very high margin business and is one of the largest independent libraries in the world with over 20,000 titles. Our library has been a consistent

grower over the past several years, even growing through the pandemic. When Lionsgate Studio wasn’t releasing much new content.

Continuing on Slide

14, we think library has become more and more valuable to streamers over time, especially in a world where content spend on originals is being reassessed. The search phenomenon has proven to the market where we’ve always internally believed

that Lionsgate, the deep, high quality library content, can have superior unit economics to streamers compared to expensive originals. We are already seeing this trend positively affecting our library business. People always focus on the strategic

value of library, but the reality is its financial importance as the anchor to funding a great deal of our new content spend can’t be overstated. We’ve talked about organic growth, but we’ve had a solid M&A history as well over

the last 20 plus years.

Slide 15 overviews a quick history of successful M&A deals we’ve done related to the Studio. Most of the deals were

bolt-ons, but some, like Summit, were transformative. A great number were actually paid for with the acquisitions own money. And that segways us into Slide 16, which discusses our eOne asset, which we recently closed on last week. You will hear eOne

mentioned a bunch of times on this call and that’s because the opportunity fit exactly into what we do so well. Acquiring a solid foundation of hit television series combined with a top-notch reality

television business and of course, the library of 6,500 plus titles is great. But more importantly, we get to integrate the assets into our existing content creation and library distribution apparatus.

So when all is said and done, we’ll end up paying around six times adjusted OIBDA for the business,

which we find extremely attractive, especially when considering where our studio is being valued in this public offering. With this library and recent pick-ups on shows like Yellowjackets, The

Rookie and the Spencer Sisters, this deal should deliver steady revenue growth in OIBDA. We thrive on M&A plus organic growth.

Before I

hand it off to Jimmy, I wanted to just summarize again why we think Lionsgate Studios is uniquely positioned to create significant shareholder value over the next few years. Let’s turn to Slide 17, please. Our five core tenets each are immense

assets individually, and we’re worth a lot more together. The guiding principle and bedrock of the studio is to create high quality content that can be added to our library for long term monetization. It’s the gift that keeps on giving

while consumer tastes continue to shift. What hasn’t changed is consumer demand for quality, commercial content, and our track record as a key supplier of content to all the major players, regardless of platform, creates tailwinds for our

business long term.

This transaction, which we believe will set a mark for the valuation of Lionsgate Studios, also creates a path towards full

separation, which Jon discussed in his opening remarks. By staying independent and being agnostic to whom we license our content, we believe Lionsgate has substantial growth opportunities. And now, by establishing an opportunity for investors to

participate in our pure play studio equity, we believe Lionsgate’s best days remain ahead.

Jimmy will now take you through the transaction details,

summary, financials and outlook. Jimmy.

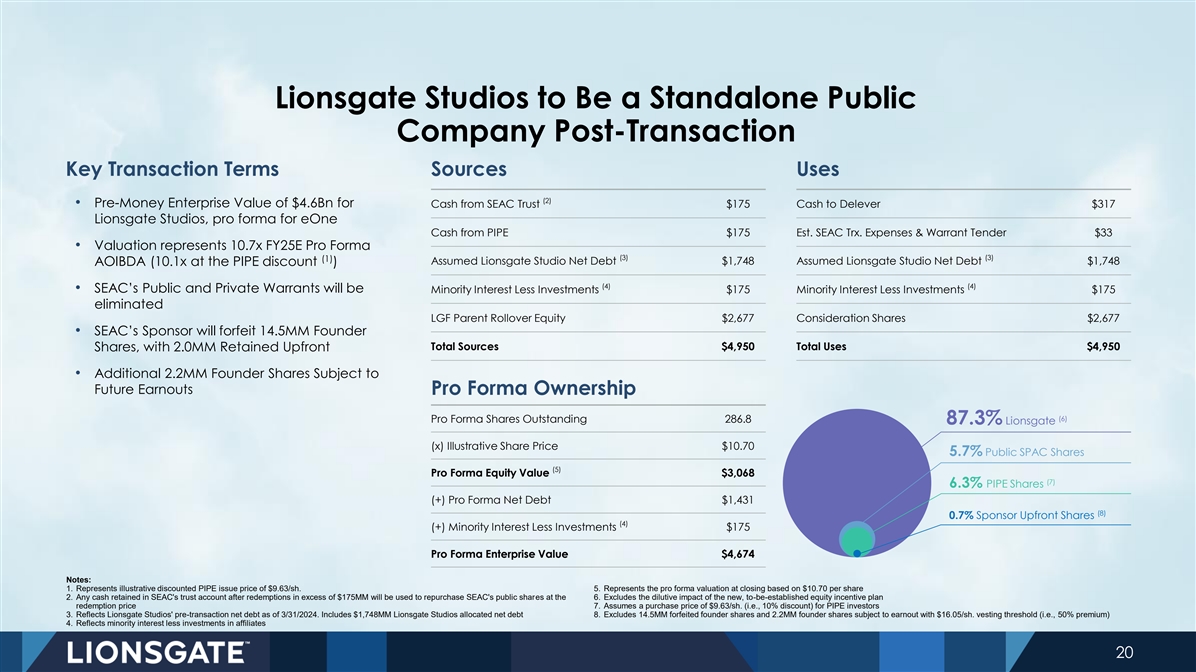

Jimmy Barge: Thanks, Michael, and good afternoon, everyone. Let’s start with slides 19 and 20, which

provides a simplified transaction structure overview and key transaction terms. As Jon noted, we’re excited to announce the combination of Lionsgate Studios, which consist of our motion picture, television production and library distribution

businesses with Screaming Eagle Acquisition Corp. at a pre-money enterprise value of $4.6 billion as summarized on Slide 19. Lionsgate Studios will raise $350 million of gross proceeds, including

175 million from marquee PIPE investors, with the remainder from cash held in Screaming Eagle. We will use the transaction proceeds to de-lever after taking into account this capital raise.

Our recently closed eOne acquisition and the incremental stake in 3 Arts that we recently purchased. Lionsgate Studios pro forma allocated net corporate debt

is anticipated to be approximately $1.4 billion at the close of the transaction. In exchange for contributing studio assets into Lionsgate Studios, Lions Gate Entertainment Corp., which I’ll referred to as Lions Gate Parent, will own

approximately 87% of Lionsgate Studios, while the remainder of Lionsgate Studios will be owned by PIPE and Screaming Eagle investors, along with its 87% stake in Lionsgate Studios. Lions Gate Parent will also own 100% of Starz when referring to the

pro forma ownership section of Slide 20. Please note this section is describing the Lionsgate Studio’s pro forma cap structure at the announced Screaming Eagle transaction price of $10.70 a share.

As you will see under key terms on Slide 20, we have structured this transaction with minimal founder shares, more specifically, unlike other SPACs in the

marketplace that include significant amounts of dilution. Screaming Eagle founders have relinquished the vast majority or 14.5 million of their 18.7 million shares of the 4.2 million remaining founder shares, 2.2 million will be

subject to an earnout and will only based upon Lionsgate Studios stock increasing by 50% to $16.05 per share. Thus, at close, the Screaming Eagle founders will own less than 1% of Lionsgate Studio shares.

Additionally, the founders have forfeited all of the private warrants they previously would have received as part of the transaction.

Finally, subject to the approval of Screaming Eagle public warrantholders, all public warrants will have been repurchased by the company by the time the

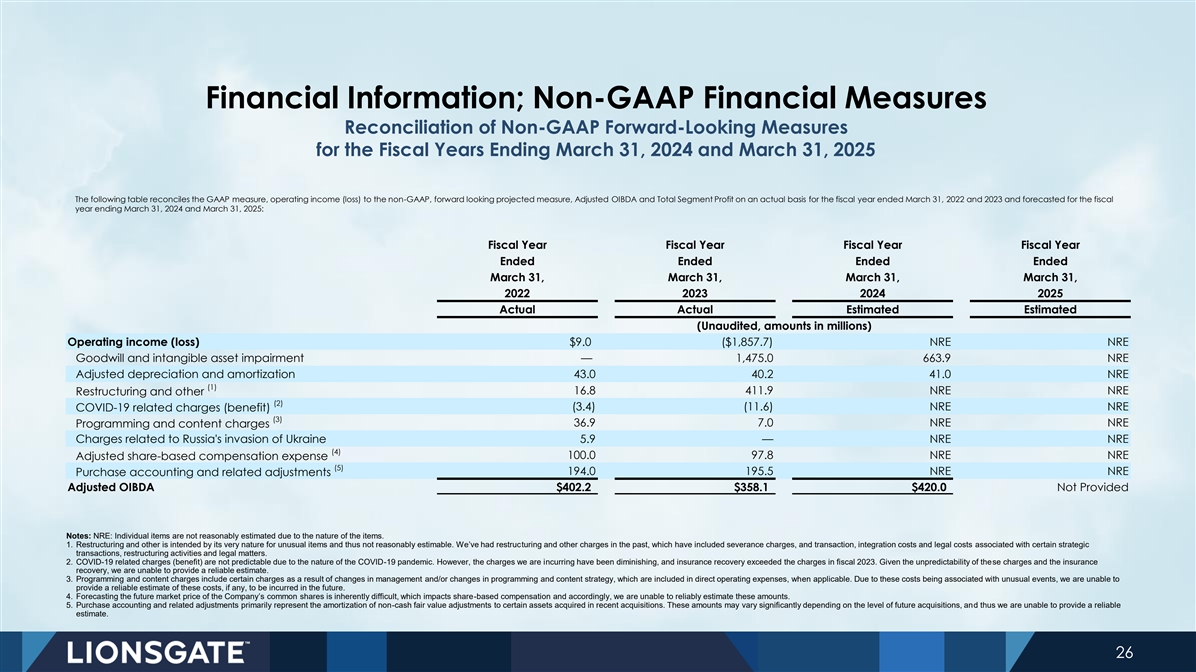

transaction closes. Let’s move to Slide 21 for the key components of our financial outlook. First, with respect to fiscal 2024, we are reiterating all prior components of our fiscal 2024 outlook for both segment related profit as well as

consolidated adjusted OIBDA. As you will see on Slide 21, we referenced a $320 million standalone studio adjusted OIBDA outlook for fiscal 2024, which is comfortably within our previously stated range of $300 to $350 million. Now, looking

at fiscal year 2025, we’re providing adjusted OIBDA outlook for Lionsgate Studios of $370 million, which excludes the impact of eOne. This implies over 15% year over year growth versus the $320 million we outlined in the presentation

slides.

Additionally, you will see in our presentation that we anticipate that eOne will achieve an annual run rate adjusted OIBDA contribution in fiscal

year 2025 of $60 million, including this run rate contribution from eOne. The $4.6 billion announced pre-money enterprise value for Lionsgate Studios implies a 10.7 times fiscal 2025 adjusted OIBDA

transaction multiple.

Before I close, I want to discuss the net debt allocations as laid out on Slide 22. As noted earlier, one of

the benefits of this transaction is that it results in over $300 million of deleveraging without impacting our existing corporate debt structure, including the availability of our $1.25 billion revolving credit facility.

Slide 22 provides a bridge to better understand how Lionsgate’s consolidated net debt of approximately $1.7 billion as of September 30, 2023

will progress by the time the transaction closes. Specifically, inclusive of our recent purchase of eOne, the incremental stake we took in 3 Arts and the use of cash related to the timing of Post-reit content spend Lionsgate’s consolidated net

debt at March 31, 2024, before the net proceeds of $317 million from the announced transaction is estimated to be approximately $2.4 billion.

The net debt after proceeds will approximate $2.1 billion, with $1.4 billion allocated to Lionsgate Studios being an intercompany debt agreement.

While the remaining $700 million of net debt is expected to be allocated to our Starz business. Inclusive of the 60 million dollars run rate of eOne adjusted OIBDA. This implies net leverage of 3.3 times our estimated studio adjusted OIBDA

for fiscal 2025.

To wrap up, we anticipate the transaction closing in the spring of 2024. There will be customary regulatory reviews of the transaction

with the SEC and Canadian authorities, the Screaming Eagle shareholders’ approval, but the proposed transaction does not require a shareholder vote among Lionsgate shareholders. Finally, as Jon noted in his prepared remarks, we remain committed

to a full separation of Lionsgate Studios and Starz.

Now I’d like to turn the call over to Nilay for Q&A.

Nilay Shah: Thanks, Jimmy. Operator, can we open up the line for questions, please?

Operator: We will now begin the question and answer session. At this time we will pause momentarily to assemble our roster. The first question is from

Steven Cahall with Wells Fargo. Please go ahead.

Question

Thanks. Jon, you said you had a number of options here and this was the best. So maybe for Jon and Michael, you’re marking the studios here at about 11

times EBITDA, your post-money net leverage, as Jimmy said, is three times. How did you think about balancing the available transactions in terms of any appetite for a higher valuation or a bigger capital raise versus the time to close or the

attractiveness of the time to close presented by the stack? So that’s the first one.

And then and then second, Michael, how do we think about the

process for collapsing the A’s and B’s? And specifically, can you talk about what percentage of A’s or B’s will need to vote for that to approve any exchange ratio? And I’ve got a quick follow up for Jimmy.

Answer

Thanks. Yeah, thanks, Steven. I’d say that

we found a price that we thought was reasonable for raising equity, but doesn’t really ultimately, of course, represent the full value of how we consider the the studio. But but we’re always happy when investors old and new come in and can

make some money with this. And I think the process proved to us that it was a fair price. It worked for both sides.

Answer

And I’ll take the closing of the stock. Ultimately, when you come up with a ratio for the A’s and the B’s given, you’re going to have to

get a shareholder vote for both the A’s and the B’s. And my sense is that will be imminent, but closer to separation.

Question

Thanks. And then a question just for Jimmy on the debt, as we think about where you were at the end of the last quarter and where you’re going to be pro

forma for the deal. Now we’ve got 3 Arts in there, eOne is in there. It looks like there’s been a couple hundred million of additional net debt if I bridge it, is that increasing cash content spend or anything in cash flow performance that

you can speak to in terms of that pro forma outlook for the debt? Thank you.

Answer

Yes, Steven, I mean, that’s our current forecast. And there is a bit of timing there. You saw, as you noted, we had really strong first half free cash

flow delivery. Some of that was timing. It was prestrike or during the strike.

And as we ramp up, as we noted on our last earnings call, we’re

ramping up production quickly as we emerge from the strike. So there would be anticipated more content spend in the second half of the year.

Question

Thanks.

Operator: The next question is from

Barton Crockett with Rosenblatt. Please go ahead.

Question

Okay, great. Thanks for taking the question. You know, you guys made the point with the announcement for the holidays, I guess, that the implied kind of equity

value for Starz is negative in this deal. And that just makes me kind of think ask questions about the split in terms of this, which is do you still think, given where the market is kind of valuing Starz, it makes sense to split. Or does that kind

of elevate in your minds maybe that there should be some other options for Starz, aside from the split, that should be more prominent in the thinking about this at this point.

Answer

Yeah. Thanks for the question, Barton. I think

the great thing about this transaction is we retain full optionality to treat Starz differently. Yes, clearly, we think Starz is way more valuable than we’re given, you know, a value for in the stock. It’s doing, what, a billion-four

revenue. It’s, you know, around $200 million of North American EBITDA. It’s cash flow positive. Obviously, we’re benefiting from the fact that we’re cleaning up the international channels that will be done last year in the

UK. That’ll be done in the next couple of months. So look, we believe that will be a, you know, great standalone channel. It’ll probably bulk up if we were to separate the business of could we sell it as well? Again, we retain full

optionality. So one way or the other someone is going to take advantage of the value that they’ve created at Starz.

Question

Okay. Thanks for that. And then if I could just ask one other question. Could you walk through what is kind of the drivers of the growth in studio EBITDA from

2025 versus 2024? You know, what’s kind of driving your outlook there?

Answer

Sure. Thanks, Barton. Yeah, look, we’re coming off of fiscal 2024 that we actually navigated very well, particularly through the strikes and while

there’s some carryover impact, we really feel good. We’re bouncing into 2024 with strength with strength in TV, 3 Arts in particular, right. Coming off a strike impacted period will be strong television production expect post-strike

episodic deliveries both new and returning series. We have Ghost Season 3 coming out. We have things like Mad Men rotating back into our licensing cycle. And on the motion picture side, we’ve got a very strong theatrical slate

Ballerina, Saw XI, Borderlands, The Crow, and then we have a carryover, nice carryover into home video and GST with respect to Hunger Games. So really feel good about how we’re projecting into fiscal 2025.

Question

Okay, great. Thank you.

Operator: The next question is

from David Joyce with Seaport Research Partners. Please go ahead.

Question

Thank you. Couple of questions. First is structural. The other is operational. Structurally, how should we think about the timing for a full separation given

that this deal with Screaming Eagle will be completed in spring? And then secondly, kind of extending the prior question on growth, what would be the broad strategy from here? Know every piece of content generates cash over a long period of time,

but that it diminished. Is it safe to keep layering on with more assets? But what are some other strategies to try to drive, you know, annuity revenue streams and anything else you can do with the IP, such as more attractions, theme parks and that

sort of thing? Just wondering what some of the growth strategies could be.

Answer

Yeah, thanks. I’m not sure I understood what you’re saying was you acquire businesses obviously, that fuels growth, particularly when we can do what

we’re doing with eOne, which is effectively buy something at a multiple probably half of our current multiple. And even less than that. And what we think ultimately are multiple is I’m not quite sure we can go back to that. On the full

separation, I think we are targeting calendar 2024 in terms of growth, you mentioned ancillary businesses. We have really started ramping up those businesses. I could say a lot of them, whether it’s theme parks, whether it’s our video-game

business. I announced a new John Wick AAA game recently and those businesses do take time. There’s lots of smaller pieces that add up. We’ve got 12 Broadway shows in development, a couple coming to fruition pretty quickly.

So, you know, I definitely see in the next year or two, those businesses contributing far more heavily to the business. But our core businesses are growing.

And I think that’s the point Jimmy was making. Our library keeps growing, our television keeps growing. 3 Arts is killing it. They they’ve doubled their EBITDA in the last five years that we’ve had them working together. We’ve

got a really diversified set of assets.

Our Debar-Mercury business is working well. I would actually say all of our businesses are working well and when

we can buy some of these, call it free radicals, as John Malone would say, and we can, you know, have them be extremely accretive, that continues to grow our business and take advantage and leverage our infrastructure, which is, you know, frankly,

world class.

Question

Great. Thank you very much.

Operator: The next question is from Thomas Yeh with Morgan Stanley. Please go ahead.

Question

Thanks so much. Yeah, just in light of the

recent eOne closure, can we get some color on what the integration process over the next year will look like? And maybe are there any structural reasons why the eOne margin profile can’t reach your existing TV segment over time? Maybe lay out

hitting the run rate, as you talked about, for exiting fiscal 2025, what that looks like over the course of the year would be helpful.

Answer

No, Thomas, thanks. We feel good about achieving that pro forma run rate, right? Post-synergies, as we put in here 60 million a meeting that achieving it

or exceeding it. And the cadence of that will come over the year as we go and integration is still early now, right? We’re just consummated. You know, just a few weeks ago, the transaction itself and we’re off to a very strong integration.

Expect revenue synergies, obviously some benefits on the cost side as well. And, you know, feel good about achieving that. And, you know, thanks. It just fits like a glove with our business, particularly on the TV side and the library folding in. So

more good things to come.

Answer

Yeah, I would say operationally, while we couldn’t operate that business, while we’re in final approval process, I would tell you, I think our staff

has done an amazing job of being prepared for, and I think you’ll see an announcement soon on how we’re approaching our nonfiction business and that integration of that business. I personally am going up to Canada next Monday to meet

everybody that I haven’t met yet and I will go in with a whole team up there. But we’re well along in the integration process and have seen no surprises except good ones so far.

Question

Great. That’s good to hear. And just on

top of that, in terms of the long-term margin potential of that business, is there an asset mix that structurally would make it look different than what you currently operate with? Or should I think about the opportunity being pretty good for you to

be able to bring that back to, you know, your historical track record of being able to deliver pretty healthy margins on the TV side?

Answer

Yeah, I think that’s right. I think that’s the right way to look at it. We’re getting, you know, both on the scripted side and the I will say

unscripted. There should be really nice accretion as we follow them together. Again, you’ll see that announcement. There are some benefits, I would say we probably expected, but there will be some benefits from the way they are positioned in

Canada. I think we’re getting benefits, particularly as we continue to expand our television business into some lower budgeted international productions. We’ve done quite a few of them this last year. So I think you’ll see some, you

know, accretive benefits there. But yeah, I think overall it will look pretty much like our television business.

Answer

And Thomas integrating the library and our library and titles and these additional territories as a significant benefit. Jim Packer and team are just beside

themselves waiting to get work with the one team to execute.

Question

Okay. Super helpful. If I could squeeze one last one in. Just in terms of following up on the commitment towards the full separation, should we think about the

original mechanics in terms of the plan that’s been studio out from Starz that still holds? Or is there any more complexity to contemplate given kind of the public equity that would be out there for studio?

Answer

No, that’s still that still holds this you

know, it lines up nicely with our overall plans was again it allowed us an opportunity to de-lever which is something we always wanted to do as part of the full separation. So but otherwise, you know, you see

we retained over 80% so we can execute a tax free shareholder spin of the studio.

Question

Thank you so much. Appreciate your time.

Answer

You’re welcome.

Operator: The next question is from

Alan Gould with Loop Capital. Please go ahead.

Question

Thanks for taking the question. I’ve got three here. First on eOne, can you tell us what the run rate revenue is on eOne and how much costs or any

synergies or part of that 60 million? Secondly, an easy one, Jimmy this SPAC. So will the S-4 present more detailed management projections are further out than what you’ve provided today. And third, on

the structural question, in total, you actually have the split who votes the 87% of the studio shares that will be owned by the Lionsgate Corporation, the shareholders or committee of the board has that work?

Answer

Yeah, from an operational perspective, and unless

there is a change of control transaction to the board. Jimmy. With regards to eOne revenue, you know, probably something like 600 million run rate on the revenue. But I think, you know, more importantly, just looking at ultimately what that

contribution is. So a lot of that will be impacted by timing of episodic deliveries. Of course, on the TV side, you know, we’ll follow the motion picture business really into our business. We’re already handling a release in common there

or through the king that’s coming out. So and then we’ll integrate libraries. I noted earlier on the S-4, you know, the projections you’ll see will be in line with obviously, but no more robust.

I wouldn’t expect than what we’ve already provided in the roadshow deck and discussed today in my remarks.

Question

Thank you.

Operator: The next question is from Matthew

Harrigan with Benchmark. Please go ahead.

Question

Oh, thank you. Very elegant, seeing them on a very long, messy plot. So congratulations. I was going to ask you about the tax considerations on Starz, but in

the sense that was already asked, if you look at the issues with the box office the last couple of years, you’ve clearly been positioned as a winner. And as Michael said, you’re kind of the benign arms dealer on the streaming side. But how

do position your business into the optical box office continues to decline on a global basis? And do you think some of your competitors who are maybe too streaming oriented will kind of reassess, you know, the balancing and the positioning that

they’ve done because you’re clearly, clearly a winner, right now. But what happens with the process that continues the way it’s been the last the last few years? Thank you.

Answer

Yeah, I’ll tell you, I think to start with,

your premise is a little bit off because you can’t talk about the film business as a box office business. Okay. The box office is the driver of the business, but I think I can’t speak for all of the studios. But I think if you asked folks

overall, you know, how they think about the business right now, I’m hearing really when people start putting together all of the revenue streams, I think it’s a pretty, pretty positive business, as you know. And so in terms of our segment

one business, and that’s our wide release business, we do it a little differently, as you well know, Matthew. And I think, you know, I like our profile. We probably take a little, you know, away from the super upside. But the way we pre-license are our movies to frankly a much larger group of international buyers and therefore go into the domestic release with a far lower gap or deficit.

I think to start with that in the world that we’re in right now, it’s a great model. And I would say, again, that when you look at the entire value

chain for Segment one movies, I would say, you know, particularly because we’ve all everyone is experimenting, but everyone is doing earlier windows in terms of pay per view, GST, pay television, et cetera. And again, obviously an earlier

window just is more economics than a revenue stream that comes in later. So. So I guess at the end of the day, the calculus as far as I’m concerned for what we call segment one movies, wide release movies is every bit as good, even if the

overall box office is a little bit less.

In terms of what we call segment two, our lower budgeted movies are multi-platform movies are direct to streamer

movies. As I think we’ve said on some calls before, we’re at about a 94%, 94% success rate. I would say our IRR in those is 30% to 40%. And that’s a business that is getting stronger and stronger, 30 movies, 40 movies a year.

It’s a great foundation, a great bedrock for our overall business. So I guess maybe I’m Chicken Little a little bit, but honestly, I like the business a lot. It’s a driver for library and repackaging our art, our library. I think

it’s a great business I’m not really concerned about. I’m bullish on it.

Question

That’s great. Thanks, Jon.

Operator: The next

question is from Jim Goss with Barrington Research. Please go ahead.

Question

Hi. I had a couple of questions. One, I was you were detailing your mix in terms of film versus television versus library as being fairly balanced. I’m

wondering if the ultimate mix objectives are to maintain that balance or build toward one area or another based on how you think the business is going. And with M&A, are you or are you are you tending to think of your growth and margin terms are

accretive M&A versus organic? And then finally, premium preference is sort of prominent. These days.

And I’m wondering if that causes you to

tilt your film production ambitions more toward bigger budgets with a perceived blockbuster potential? And that’s it.

Answer

Yeah. I’ll start with the last to work up. I would say I kind of answered, I think. But we like the mix of products that we have. And I would say at the

end of the day, we don’t concentrate on being in the blockbuster business. I would say, for example, we have Highlander coming down the pike, Chad Stahelski directing it. I’ve got very high hopes for that as a franchise, but I promise you

we won’t be spending $250 or $300 million on the first movie or frankly, on any of the movies. But I would consider that for us and Blockbuster, as we develop that, we’re developing at the same time, we’re developing a whole set

of characters and spinoff and television around it. So that to me is a blockbuster, but it’s not going to have crazy risk to it. And again, we will pre-sell pretty much guarantee 70%, 80% of the cost of

that movie.

And so we’re going to we’re going to stick with that model. In terms of M&A, I would say, versus organic growth, I mean, you

always want to have as much organic growth as you can. But because we’ve built this incredible infrastructure and frankly, I can handle you know, I can even handle with that infrastructure a significant amount of additional library product. I

would say M&A is always a faster way to growth, but you can’t ever forget organic growth and especially the creation of intellectual property, great intellectual property. That’s something we have to concentrate on all of the time. And

then I’m sorry, your question about mix of mix of product, I would say yes.

Answer

No, that’s not yeah, we don’t I mean, it’s not something you really aim at if you asked me, what would I really like to see? I’d like to

see the biggest revenue generator be the library. Obviously that that would be the best. But, you know, that’s probably not going to happen just because, you know, again, if you look at the mix right now, you’ve got film, television and

Starz even, you know, generating, I’d say, you know, sort of more current revenue. But at the end of the day, obviously, the key thing for us is building up that library. So the higher that that goes, the better I feel.

Answer

In the library as you know, Jim just naturally

grows as the products flow through in the production. I mean, as Michael noted, you know, we’re putting like 450 titles a year in library just through TV and motion picture. And of course, the eOne will nicely supplement our TV business.

Question

All right, thanks, guys. Appreciate it.

Operator: This concludes our question and answer session. I would like to turn the conference back

over to Nilay Shah for any closing remarks.

Nilay Shah: Thanks, everyone. Please refer to the Press Releases and Events tab under the Investor

Relations section of the company’s website for a discussion of certain non-GAAP forward looking measures discussed on this call today. Thank you.

Operator: The conference has now concluded. Thank you for attending today’s presentation. You may now disconnect.

Investor Presentation

[End of Communication]

Additional Information and Where to Find It

In

connection with the proposed transactions, SEAC II Corp. (“New SEAC”), a subsidiary of Screaming Eagle Acquisition Corp. (“SEAC”) intends to file with the SEC a registration statement on Form

S-4, which will include a preliminary proxy statement of SEAC and a preliminary prospectus of New SEAC, and after the registration statement is declared effective, SEAC will mail the definitive proxy

statement/prospectus relating to the proposed transactions to SEAC’s shareholders and public warrant holders as of the respective record dates to be established for voting at the SEAC shareholders meeting and the SEAC public warrant holders

meeting. The registration statement, including the proxy statement/prospectus contained therein, will contain important information about the proposed transactions and the other matters to be voted upon at SEAC shareholders meeting and the SEAC

public warrant holders meeting. This communication does not contain all the information that should be considered concerning the proposed transactions and other matters and is not intended to provide the basis for any investment decision or any

other decision in respect of such matters. SEAC, New SEAC and Lionsgate may also file other documents with the SEC regarding the proposed transactions. SEAC’s shareholders, public warrant holders and other interested persons are advised to

read, when available, the registration statement, including the preliminary proxy statement/prospectus contained therein, the amendments thereto and the definitive proxy statement/prospectus and other documents filed in connection with the proposed

transactions, as these materials will contain important information about SEAC, New SEAC, Lionsgate, the studio business and the proposed transactions. SEAC’s shareholders, public warrant holders and other interested persons will be able to

obtain copies of the Registration Statement, including the preliminary proxy statement/prospectus contained therein, the definitive proxy statement/prospectus and other documents filed or that will be filed with the SEC, free of charge, by SEAC, New

SEAC and Lionsgate through the website maintained by the SEC at www.sec.gov.

Participants in the Solicitation

SEAC, New SEAC, Lionsgate, LG Orion Holdings Inc. (“StudioCo”) and their respective directors and officers may be deemed participants in the

solicitation of proxies of SEAC shareholders and public warrant holders in connection with the proposed transactions. more detailed information regarding the directors and officers of SEAC, and a description of their interests in SEAC, is contained

in SEAC’s filings with the SEC, including its Annual Report on Form 10-K for the fiscal year ended December 31, 2022, which was filed with the SEC on March 1, 2023, and is available

free of charge at the SEC’s website at www.sec.gov. Information regarding the persons who may, under SEC rules, be deemed participants in the solicitation of proxies of SEAC’s shareholders and public warrant holders in connection with the

proposed transactions and other matters to be voted upon at the SEAC shareholders meeting and the SEAC public warrant holders meeting will be set forth in the registration statement for the proposed transactions when available.

Forward-Looking Statements

This communication includes

certain statements that may constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act, and Section 21E of the Exchange Act. Forward-looking statements include, but are not limited to,

statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions. The words “anticipate,” “believe,” “continue,” “could,”

“estimate,” “expect,” “intends,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “seek,” “should,”

“target,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements may include, for example,

statements about SEAC or Lionsgate’s ability to effectuate the proposed transactions discussed in this document; the benefits of the proposed transactions; the future financial performance of

the go-forward public company following the completion of the proposed transactions (“Pubco”) following the proposed transactions; changes in Lionsgate’s strategy, future operations,

financial position, estimated revenues and losses, projected costs, prospects, plans and objectives of management. These forward-looking statements are based on information available as of the date of this document, and current expectations,

forecasts and assumptions, and involve a number of judgments, risks and uncertainties. Accordingly, forward-looking statements should not be relied upon as representing SEAC, Lionsgate, StudioCo or New SEAC’s views as of any subsequent date,

and none

of SEAC, Lionsgate, StudioCo or New SEAC undertakes any obligation to update forward-looking statements to reflect events or circumstances after the date they were made, whether as a result of

new information, future events or otherwise, except as may be required under applicable securities laws. Neither Lionsgate, StudioCo, New SEAC nor SEAC gives any assurance that any of New SEAC, StudioCo, Pubco or SEAC will achieve its expectations.

You should not place undue reliance on these forward-looking statements. As a result of a number of known and unknown risks and uncertainties, Pubco’s actual results or performance may be materially different from those expressed or implied by

these forward-looking statements. Some factors that could cause actual results to differ include: (i) the timing to complete the proposed transactions by SEAC’s business combination deadline and the potential failure to obtain an extension

of the business combination deadline if sought by SEAC; (ii) the occurrence of any event, change or other circumstances that could give rise to the termination of the definitive agreements relating to the proposed transactions; (iii) the

outcome of any legal, regulatory or governmental proceedings that may be instituted against Pubco, SEAC, Lionsgate, StudioCo or New SEAC or any investigation or inquiry following announcement of the proposed transactions, including in connection

with the proposed transactions; (iv) the inability to complete the proposed transactions due to the failure to obtain approval of SEAC’s shareholders or public warrant holders; (v) Lionsgate’s and Pubco’s success in

retaining or recruiting, or changes required in, its officers, key employees or directors following the proposed transactions; (vi) the ability of the parties to obtain the listing of Pubco Common Shares on Nasdaq or another stock exchange upon

the Closing; (vii) the risk that the proposed transactions disrupts current plans and operations of Lionsgate; (viii) the ability to recognize the anticipated benefits of the proposed transactions; (ix) unexpected costs related to the

proposed transactions; (x) the amount of redemptions by SEAC’s public shareholders being greater than expected; (xi) the management and board composition of Pubco following completion of the proposed transactions; (xii) limited

liquidity and trading of Pubco’s securities following completion of the proposed transactions; (xiii) changes in domestic and foreign business, market, financial, political and legal conditions; (xiv) the possibility that Lionsgate,

StudioCo, Pubco, New SEAC or SEAC may be adversely affected by other economic, business, and/or competitive factors; (xv) operational risks; (xvi) litigation and regulatory enforcement risks, including the diversion of management time and

attention and the additional costs and demands on Lionsgate’s resources; (xvii) the risk that the consummation of the proposed transactions is substantially delayed or does not occur; and (xviii) other risks and uncertainties

indicated from time to time in the registration statement, including those under “Risk Factors” therein, and in the other filings of SEAC, Lionsgate, StudioCo, New SEAC and Pubco with the SEC.

No Offer or Solicitation

This communication relates

to a proposed transaction between Lionsgate and SEAC. This document does not constitute a solicitation of a proxy, consent or authorization with respect to any securities or in respect of the proposed transactions. This document does not constitute

an offer to sell or exchange, or the solicitation of an offer to buy or exchange, any securities, nor shall there be any offer, sale or exchange of securities in any state or jurisdiction in which such offer, solicitation, sale or exchange would be

unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offering of securities will be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act or an

exemption therefrom. No securities commission or securities regulatory authority in the United States or any other jurisdiction has in any way passed upon the merits of the transaction or the accuracy or adequacy of this communication.

Exhibit 99.2 Lionsgate Studios Conference Call Presentation January 4,

2024

Disclaimer Forward-looking statements and risk factors This presentation

(together with oral statements made in connection herewith, this “Presentation”) is provided for informational purposes only and has been prepared to with respect to a business combination involving LG Orion Holdings Inc. (“LG

Studio” or the “Company”), a wholly owned subsidiary of Lions Gate Entertainment Corp. (“Lionsgate”) created to hold the Studio Business of Lionsgate (“Lionsgate Studios”) and SEAC Acquisition Corp.

(“SEAC”) and related transactions (the “Proposed Business Combination”) and for no other purpose. All statements other than statements of historical facts contained in this Presentation are forward-looking statements. Forward

looking statements may generally be identified by the use of words such as “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,”

“expect,” “should,” “would,” “plan,” “project,” “forecast,” “predict,” “potential,” “seem,” “seek,” “future,”

“outlook,” “target” or other similar expressions that predict or indicate future events or trends or that are not statements of historical matters. These forward-looking statements include, but are not limited to, statements

regarding estimates and forecasts of financial and performance metrics and projections of market opportunity and m ark et share. These statements are based on management’s current estimations and analysis, are subject to various assumptions

that the parties believe are reasonable at this time, whether or not identified in this Presentation, reflect the current expectations Lionsgate’s management as of the date of this Presentation and are not predictions of actual performance.

These forward-looking statements are provided for illustrative purposes only and are not intended to serve as and must not be re lied on by any investor as, a guarantee, an assurance, a prediction or a definitive statement of fact or probability.

Actual events and circumstances are difficult or impossible to predict and may differ from assumptions and such differences may be material. Many actual events and circumstances are beyond the control of LG Studio, Lionsgate and SEAC. These

forward-looking statements are subject to a number of risks and uncertainties, including changes in domestic and foreign business, market, financial, political and legal conditions; the inability of the parties to successfully or timely consummate

the Proposed Business Combination, including the risk that any required regulatory approvals are not obtained, are delayed or are subject to unanticipated conditions that could adversely affect the combined company or the expected benefits of the

Proposed Business Combination or that the approval of the stockholders of SEAC is not obtained; failure to realize the anticipated benefits of the Proposed Business Combination; risks relating to the uncertainty of the projected financial

information with respect to Lionsgate’s Studio business; the effects of competition on Lionsgate’s Studio business; the amount of redemption requests made by SEAC’s public stockholders; the ability of SEAC or the combined company

to issue equity or equity linked securities in connection with the Proposed Business Combination or in the future; the risk of litigation and/or regulatory actions related to the Proposed Business Combination; diversion of management time from

ongoing business operations due to the Proposed Business Combination; the risk that the Proposed Business Combination could have an adverse effect on the ability of Lionsgate’s Studio business to retain customers and retain and hire key

personnel and maintain relationships with customers, suppliers, employees, stockholders and other business relationships; and those factors discussed under the heading “Risk Factors” in SEAC’s Annual Report on Form 10-K filed with

the SEC on March 1, 2023, SEAC’s Quarterly Report on Form 10-Q filed with the SEC on September 9, 2023, Lionsgate’s Annual Report on Form 10-K filed with the SEC on May 25, 2023, Lionsgate’s Quarterly Report on Form 10 Q filed with

the SEC on November 9, 2023, Lionsgate’s Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934 filed with the SEC on October 13, 2023, LG Studio’s registration statement on Form 10 filed with the SE C on July

12, 2023 and other periodic public filings of SEAC, LG Studio or Lionsgate filed, or to be filed, with the SEC, any provincial securities commissions or securities regulatory authorities in Canada, or on the SEDAR+ website at www.sedarplus.ca, as

applicable . You should also carefully consider the risks and uncertainties described in the “Risk Factors” section of the proxy statement/prospectus on Form S-4 (or other applicable SEC form) relating to the Proposed Business

Combination, which is expected to be filed with the SEC, and other documents filed from time to time with the SEC. These filings identify and address other important risks and uncertainties that could cause actual events and results to diverge

materially from those contained in the forward-looking statements in this presentation. If any of these risks materialize or SEAC’s, Lionsgate’s or LG Studio’s assumptions prove incorrect, actual results could differ materially

from the results implied by these forward-looking statements. There may be additional risks that neither SEAC, Lionsgate nor LG Studio presently know or that SEAC, Lionsgate and LG Studio currently believe are immaterial that could also cause actual

results to differ from those contained in the forward-looking statements. In addition, forward looking statements reflect Lionsgate’s expectations, plans or forecasts of future events and views as of the date of this Presentation. SEAC,

Lionsgate and LG Studio anticipate that subsequent events and developments will cause their assessments to change. It is not possible to predict all risks, nor assess the impact of all factors on LG Studio’s business or the extent to which any

factor, or combination of factors, may cause LG Studio’s actual results, performance or financial condition to be materially different from the expectations of future results, performance or financial condition. In addition, the analyses of

Lionsgate, LG Studio and SEAC contained herein are not, and do not purport to be, appraisals or the securities, assets or business of LG Studio, SEAC or any other entity. While SEAC, Lionsgate and LG Studio may elect to update these forward-looking

statements at some point in the future, SEAC, Lionsgate and LG Studio specifically disclaim any obligation to do so. These forward-looking statements should not be relied upon as representing SEAC’s, Lionsgate’s and LG Studio’s

assessments as of any date subsequent to the date of this Presentation. Accordingly, undue reliance should not be placed upon the forward-looking statements. Use of projections The projections, estimates and targets in this Presentation are forward

looking statements that are based on assumptions that are inherently subject to significant uncertainties and contingences, many of which are beyond Lionsgate’s, LG Studio’s and SEAC’s control. Lionsgate’s and SEAC’s

independent auditors did not audit, review, compile or perform any procedures with respect to such projections, estimates, or targets for the purpose of their inclusion in this Presentation, and accordingly, such auditors neither expressed an

opinion nor provided any other form of assurance with respect thereto for the purpose of this Presentation. While all protections, estimates, and targets are necessarily speculative, LG Studio and Lionsgate believe that the preparation of

prospective financial information involves increasingly higher levels of uncertainty the further out the projection, estimate, or target extends from the date of preparation. The assumptions and estimates underlying projected, expected, or targeted

results are inherently uncertain and are subject to a wide variety of risks and uncertainties, including but not limited to those mentioned in the immediately preceding paragraph, that could cause actual results to differ materially from those