As filed with the Securities and Exchange Commission on February 12, 2016

Registration No. 333-209119

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

______________

AMENDMENT NO. 1 TO

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

AEOLUS PHARMACEUTICALS, INC.

(Exact Name of Issuer in Its Charter)

|

Delaware

|

2834

|

56-1953785

|

|

(State or Other Jurisdiction of

Incorporation or Organization)

|

(Primary Standard Industrial

Classification Number)

|

(I.R.S. Employer

Identification No.)

|

Aeolus Pharmaceuticals, Inc.

26361 Crown Valley Parkway, Suite 150

Mission Viejo, California 92691

(949) 481-9825

(Address, including zip code, and telephone number,

including area code, of registrant's principal executive offices)

______________

John McManus

President and Chief Executive Officer

Aeolus Pharmaceuticals, Inc.

26361 Crown Valley Parkway, Suite 150

Mission Viejo, California 92691

(949) 481-9825

(Name, address, including zip code, and telephone number,

including area code, of agent for service)

______________

Copies of all communications to:

|

Brian J. Lynch

Drinker Biddle & Reath LLP

One Logan Square, Suite 2000

Philadelphia, Pennsylvania 19103-6996

(215) 988-1119

|

______________

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

|

☐

|

Accelerated filer

|

☐

|

| |

|

|

|

|

Non-accelerated filer

|

☐ (Do not check if a smaller

reporting company)

|

Smaller reporting company

|

☒

|

______________

CALCULATION OF REGISTRATION FEE

|

Title of Each

Class of Securities

to be Registered

|

|

Amount to be

Registered(1)

|

|

|

Proposed

Maximum

Offering Price

Per Security

|

|

|

Proposed

Maximum

Aggregate

Offering Price

|

|

|

Amount of

Registration Fee

|

|

|

Common stock, par value $0.01 per share

|

|

|

15,629,676

|

|

|

$

|

0.22

|

(2)

|

|

$

|

3,438,528.72

|

|

|

$

|

346.26

|

|

|

Common stock, $0.01 par value per share, issuable upon the exercise of warrants

|

|

|

37,298,249

|

|

|

$

|

0.22

|

(3)

|

|

$

|

8,205,614.78

|

|

|

$

|

826.31

|

|

|

Common stock, $0.01 par value per share, issuable upon the conversion of Series C Convertible Preferred Stock

|

|

|

20,454,546

|

|

|

$

|

[ ]

|

(4)

|

|

$

|

4,500,000

|

|

|

$

|

453.15

|

|

|

Common stock, $0.01 par value per share, issuable upon the exercise of warrants

|

|

|

50,000

|

|

|

$

|

0.26

|

(3)

|

|

$

|

13,000

|

|

|

$

|

1.31

|

|

|

Total:

|

|

|

73,432,471

|

|

|

|

|

|

|

$

|

16,157,143.50

|

|

|

$

|

1,627.03

|

(5) |

(1) In accordance with Rule 416 under the Securities Act, the registrant is also registering hereunder an indeterminate number of shares that may be issued and resold resulting from stock splits, stock dividends or similar transactions.

(2) Estimated solely for purposes of calculating the registration fee in accordance with Rule 457(c) under the Securities Act, using the average of the high and low prices as reported on the OTC Bulletin Board on February 2, 2016.

(3) Estimated solely for purposes of calculating the registration fee in accordance with Rule 457(g) under the Securities Act, the proposed maximum offering price per share is based on the exercise price of the warrants.

(4) Estimated solely for purposes of calculating the registration fee in accordance with Rule 457(i) under the Securities Act, the proposed maximum offering price per share is based on the equivalent purchase price per share of common stock underlying the Series C Convertible Preferred Stock.

(5) Previously paid.

______________________

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell the securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to completion, dated February 12, 2016

PRELIMINARY PROSPECTUS

73,432,471

Common Stock

This prospectus relates to the offer and sale from time to time by the selling stockholders identified in this prospectus of up to 73,432,471 shares of our common stock, par value $0.01 per share. These shares include (i) 15,629,676 shares of common stock issued and outstanding, (ii) 20,454,546 shares of common stock issuable upon conversion of Series C Convertible Preferred Stock and (iii) 37,298,249 shares of common stock issuable upon exercise of warrants, all of which were issued in connection with a private placement which closed in December of 2015. This prospectus also relates to 50,000 shares of our common stock issuable upon the exercise of warrants that we issued in 2014. The shares of common stock and warrants were issued in transactions made in reliance on Section 4(a)(2) of the Securities Act of 1933, as amended, which we refer to as the Securities Act, and Rule 506 promulgated thereunder. For additional information regarding the private placements, please see "Description of the Shares included in this Prospectus" beginning on page 8 of this prospectus.

We are not selling any common stock under this prospectus and will not receive any of the proceeds from the sale of shares by the selling stockholders; however, we will receive the proceeds of any cash exercise of the warrants.

The selling stockholders may sell the shares from time to time at the market price quoted on the OTC Bulletin Board (or any stock exchange on which our common stock may be listed in the future) at the time of offer and sale, or at prices related to such prevailing market prices, in negotiated transactions or in a combination of such methods of sale directly or through brokers. See "Plan of Distribution" beginning on page 109 for additional information on how the selling stockholders may conduct sales of their shares of common stock.

In addition to the shares that may be offered under this prospectus, we also have registered shares for sale by certain other selling stockholders, who may offer and sell up to 117,512,184 shares under a separate prospectus. See "Risk Factors – Risks Related to Owning Our Stock; Substantial blocks of our total outstanding common stock may be sold into the market through existing registration statements already on file with the SEC. If there are substantial sales of shares of our common stock, the price of our common stock could decline"

Other than underwriting discounts and commissions, and transfer taxes, if any, we have agreed to bear certain expenses incurred in connection with the registration and sale of the common stock offered by the selling stockholders.

Our common stock is quoted on the OTC Bulletin Board under the symbol "AOLS." On February 2, 2016, the closing price of our common stock was $0.20 per share.

Investing in our common stock involves a high degree of risk. See "Risk Factors" beginning on page 8 for certain risks you should consider before purchasing any shares.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved these securities, or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

______________

The date of this prospectus is February 12, 2016

TABLE OF CONTENTS

| |

|

| |

Page

|

| |

|

|

Prospectus Summary

|

1

|

| |

|

|

Risk Factors

|

8

|

| |

|

|

Special Note Regarding Forward-Looking Statements

|

27

|

| |

|

|

Description of the Shares Included in this Prospectus

|

28

|

| |

|

|

Use of Proceeds

|

30

|

| |

|

|

Determination of Offering Price

|

31

|

| |

|

|

Market Information / Price Range Of Common Stock / Dividends

|

32

|

| |

|

|

Management's Discussion and Analysis of Financial Condition and Results of Operations

|

34

|

| |

|

|

Business

|

42

|

| |

|

|

Management

|

80

|

| |

|

|

Compensation of Directors

|

84

|

| |

|

|

Executive Compensation

|

86

|

| |

|

|

Certain Relationships and Related Party Transactions

|

90

|

| |

|

|

Security Ownership of Certain Beneficial Owners and Management

|

92

|

| |

|

|

Selling Stockholders

|

95

|

| |

|

|

Description of Capital Stock

|

105

|

| |

|

|

Plan of Distribution

|

110

|

| |

|

|

Legal Matters

|

112

|

| |

|

|

Experts

|

112

|

| |

|

|

Additional Information

|

112

|

| |

|

|

Incorporation of Certain Information by Reference

|

113

|

| |

|

|

Index to Financial Statements

|

F-1

|

You should only rely on the information contained in this prospectus. We have not, and the selling stockholders have not, authorized anyone to provide you with additional information or information different from that contained in this prospectus. We are not making an offer to sell these securities in any jurisdiction where an offer or sale is not permitted. You should assume that the information appearing in this prospectus is accurate as of the date on the front cover of this prospectus only, regardless of the time of delivery of this prospectus or of any sale of our securities. Our business, prospects, financial condition and results of operations may have changed since that date.

This document may only be used where it is legal to sell these securities. Certain jurisdictions may restrict the distribution of these documents and the offering of these securities. We require persons receiving these documents to inform themselves about, and to observe any, such restrictions. We have not taken any action that would permit an offering of these securities or the distribution of these documents in any jurisdiction that requires such action.

_________________________________

We own or have rights to trademarks or trade names that we use in conjunction with the operation of our business. Each trademark, trade name or service mark of any other company appearing in this prospectus belongs to its holder. Use or display by us of other parties' trademarks, trade names or service marks is not intended to and does not imply a relationship with, or endorsement or sponsorship by us of, the trademark, trade name or service mark owner

_________________________________

Industry and Market Data

Unless otherwise indicated, the market data and certain other statistical information used throughout this prospectus are based on independent industry publications, government publications, reports by market research firms or other published independent sources. Although we believe these third-party sources are reliable, we have not independently verified the information. Except as otherwise noted, none of the sources cited in this prospectus has consented to the inclusion of any data from its reports, nor have we sought their consent. In addition, some data are based on our good faith estimates. Such estimates are derived from publicly available information released by independent industry analysts and third-party sources, as well as our own management's experience in the industry, and are based on assumptions made by us based on such data and our knowledge of such industry and markets, which we believe to be reasonable. However, except as otherwise noted, none of our estimates have been verified by any independent source. Our estimates and assumptions involve risks and uncertainties and are subject to change based on various factors, including those discussed in the "Risk Factors" section of this prospectus and the other information contained herein. These and other factors could cause our actual results to differ materially from those expressed in the estimates and assumptions.

PROSPECTUS SUMMARY

This summary highlights certain information contained elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our common stock. You should carefully read the entire prospectus, including ''Risk Factors'' and our financial statements and related notes before you decide whether to invest in our common stock. Investing in our common stock involves risks. See ''Risk Factors'' beginning on page 3. All dollar amounts referred to in this prospectus are in U.S. dollars unless otherwise indicated. Any discrepancies in the tables included herein between the amounts listed and the totals thereof are due to rounding.

Unless otherwise indicated or unless the context otherwise requires, all references in this document to "we," "us," "our," the "Company" and similar expressions are references to Aeolus Pharmaceuticals, Inc.

Our Company and Business

We are a Southern California-based biopharmaceutical company leveraging significant U.S. Government funding to develop a platform of novel compounds for use in biodefense, fibrosis, oncology, infectious disease and diseases of the central nervous system. The platform consists of approximately 180 compounds licensed from the University of Colorado ("UC") Duke University ("Duke") and National Jewish Health ("NJH").

Our lead compound, AEOL 10150 ("10150"), is being developed under contract with the Biomedical Advanced Research and Development Authority ("BARDA" and the "BARDA Contract"), a division of the U.S. Department of Health and Human Services ("HHS"), as a medical countermeasure ("MCM") against the pulmonary sub-syndrome of acute radiation syndrome ("Pulmonary Acute Radiation Syndrome" or "Lung-ARS") and the delayed effects of acute radiation exposure ("DEARE"). Lung-ARS is caused by acute exposure to high levels of radiation due to a nuclear detonation or radiological event.

We are also developing 10150 for the treatment of lung fibrosis, including idiopathic pulmonary fibrosis ("IPF") and other fibrotic diseases. This new development program was created based upon the data generated from animal studies in Lung-ARS and chemical gas exposure under the BARDA Contract and National Institutes of Health ("NIH") grants. On March 17, 2015, we announced that 10150 was granted Orphan Drug Designation for IPF by the U.S. Food and Drug Administration ("FDA"). The Company plans to initiate a Phase 1 safety study in patients with IPF in 2016. After we have completed safety studies, we plan to initiate efficacy studies in patients with IPF. AEOL 10150 has previously been tested in two Phase I human clinical trials with no drug-related serious adverse events reported.

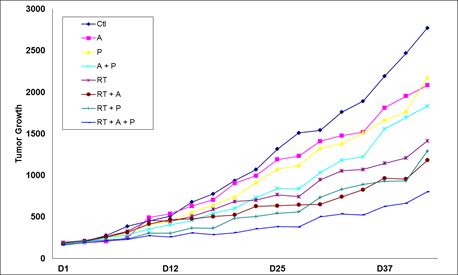

We are also developing 10150 for use in combination with radiation therapy for cancer as a treatment to reduce side effects caused by radiation toxicity and improve local tumor control. Pre-clinical studies at Duke, the University of Maryland and Loma Linda University have demonstrated that 10150 protects healthy, normal tissue, while not interfering with the benefit of radiation therapy or chemotherapy in prostate and lung cancer. Additional studies have demonstrated that 10150 enhances the anti-tumor activity of chemotherapy and radiation. A significant portion of the development work funded by the BARDA contract is applicable to the development program for radiation oncology, including safety, toxicology, pharmacokinetics and Chemistry, Manufacturing and Controls ("CMC"). After we have completed safety studies, we plan to initiate studies to demonstrate efficacy in protecting against the toxic side effects related to radiation therapy.

We are also developing 10150 as a MCM for exposure to chemical vesicants (e.g., chlorine gas, sulfur mustard gas and phosgene gas) and nerve agents (e.g., sarin gas and soman gas) with grant money from the NIH Countermeasures Against Chemical Threats ("NIH-CounterACT") program. 10150 has consistently demonstrated safety and efficacy in animal studies of chemical gas exposure and nerve gas exposure.

The Company is developing a second compound, AEOL 11114B ("11114"), as a treatment for Parkinson's disease. Research funded by the Michael J Fox Foundation for Parkinson's disease ("MJFF") demonstrated the neuro-protective activity of 11114 in mouse and rat models of Parkinson's disease. The compounds were invented by Aeolus in collaboration with Brian J. Day, PhD at National Jewish Health and Manisha Patel, PhD at the University of Colorado, Anschutz Medical Campus, Department of Pharmaceutical Sciences in collaboration with the Company. We have obtained worldwide, exclusive licenses to develop the compounds from NJH and the UC. We plan to complete the remaining work to file an Investigational New Drug ("IND") application with the FDA by 2017.

In April 2015, we announced the discovery of a new compound, AEOL 20415 ("20415"), which has demonstrated anti-inflammatory and anti-infective properties, and could be effective in treating cystic fibrosis and combatting anti-biotic resistant bacteria. The compound was developed under collaboration between Brian J. Day, PhD at National Jewish Health in Denver, Colorado and Aeolus Pharmaceuticals. We have obtained a worldwide, exclusive license to develop the rights to the compound from NJH. We plan to complete the remaining work to file an Investigational New Drug ("IND") application with the FDA by 2017.

Finally, we have a pipeline of approximately 180 additional compounds. We expect that the development of additional compounds in our portfolio is dependent on our finding non-dilutive capital sources to fund such pipeline opportunities.

Recent Developments

On December 10, 2015, we entered into securities purchase agreements with certain accredited investors to sell and issue (i) an aggregate of 10,215,275 common units issued at a purchase price of $0.22 per unit, and (ii) 4,500 preferred stock units issued to Biotechnology Value Fund, L.P. and certain other affiliates of BVF Partners, L.P., for an aggregate purchase price of $4.5 million, resulting in aggregate gross proceeds to the Company of approximately $6.75 million (the "2015 Securities Placement"). Each common unit consisted of one share of the Company's common stock and a five year warrant to purchase one share of the Company's common stock, subject to adjustment. The preferred stock units collectively consisted of (i) 4,500 shares of our Series C Convertible Preferred Stock (the "Series C Preferred Stock") that are collectively convertible into an aggregate of 20,454,546 shares of the Company's common stock and (ii) warrants to purchase an aggregate of 20,454,546 shares of our common stock, in each case subject to adjustment. Each of the foregoing warrants has an initial exercise price of $0.22 per share.

On September 29, 2015, the Company received funding in the form of convertible promissory notes (the "BVF Notes") from Biotechnology Value Fund, L.P. and certain other affiliates of BVF Partners, L.P. The BVF Notes (i) had an aggregate principal balance of $1,000,000, (ii) accrued interest at a rate of 6% per annum, (iii) had a scheduled maturity date of September 28, 2016 and (iv) were subject to automatic conversion into Company equity securities, provided a qualified financing of not less than $4 million occurred. Following the completion of the 2015 Securities Placement, the principal and accrued interest amounts under the BVF Notes were converted into 5,414,402 shares of our common stock and warrants to purchase an additional 5,414,402 shares of our common stock at an exercise price per share of $0.22 subject to adjustment (the "BVF Convert"). As a result, the BVF Notes are no longer outstanding as of the date of this prospectus.

Strategy

Our strategy is pursue the development of our promising platform of anti-fibrotic, anti-inflammatory, anti-infective and anti-oxidant compounds that address important unmet medical indications of clinical and national strategic importance. Our objective is to use non-dilutive capital whenever possible.

To date, we, and/or our research collaborators, have been awarded more than $149 million in non-dilutive U.S. government funding in the form of grants and contracts from federal agencies, such as BARDA, NIH-NIAID and NIH-CounterACT. Additional research has been conducted on our compounds with funding from private foundations, such as the MJFF and Citizens United for Research in Epilepsy ("CURE").

The expected benefit of this strategy is threefold. First, safety, toxicology, pharmacokinetic and CMC work funded by the government and foundations is applicable to our traditional commercial development programs. As an example, significant work funded under the BARDA contract for Lung-ARS has generated data that can be used to support our New Drug Applications ("NDA") for pulmonary fibrosis and/or radiation therapy for cancer.

Second, cost-plus development contracts, like our contract with BARDA, include funds for overhead and profit. These overhead and profit streams have significantly reduced our cash burn rate, which reduces our need to raise capital and incur dilution.

Third, some government contracts, such as the Lung ARS contract with BARDA are designed to lead to the acquisition of the product under development by the US Government for use as a MCM in the Strategic National Stockpile ("SNS" or the "Stockpile"). Government procurement could result in significant revenue to the Company, which could be used to further the development of the product in other indications or for the development of other promising products. Procurements may be made if either the drug meets the requirements for approval by the U.S. Food and Drug Administration (the "FDA") under the "Animal Rule" or prior to Animal Rule approval following the filing of a pre-Emergency Use Authorization ("EUA") application. Most of BARDA's procurements to date have been following the filing of a pre-EUA application.

The amount of any potential procurement is undisclosed by BARDA at this time and is unknown to us. Based on publicly available information, as well as other procurements made by the agency after pre-EUA applications, we believe the agency may purchase sufficient courses of therapy to treat a minimum of one hundred thousand people, with options to purchase an additional two hundred thousand courses of treatment. If purchases of such volumes occurred, the revenue to the Company could provide funding to advance numerous clinical studies, including potentially large Phase III programs in lung fibrosis and radiation therapy for cancer. This funding could allow us to fund studies with less dependence on collaborative partnering arrangements and future equity offerings, which is consistent with our strategy to deploy non-dilutive capital wherever possible to develop our compounds for unmet medical indications and thereby generate value for our stockholders. In addition, purchases of such volumes of drug could make the Company profitable.

Business Overview

We are developing a platform of compounds with anti-fibrotic, anti-inflammatory, anti-infective and anti-oxidant activity based on technology discovered and researched at Duke University, the University of Colorado and National Jewish Health, developed by Drs. Irwin Fridovich, Brian Day and others. Dr. Day is our Chief Scientific Officer.

Our lead compound, 10150, is a metalloporphyrin specifically designed to neutralize reactive oxygen and nitrogen species. The neutralization of these species reduces oxidative stress, inflammation, and subsequent tissue damage-signaling cascades resulting from radiation or chemical exposure. We are developing 10150 as a MCM for national defense and for use in oncology and treating lung fibrosis.

Our most extensive development program to date is the advanced development of 10150 for Lung-ARS and DEARE. On February 11, 2011, we signed a cost-plus contract with BARDA for the development of 10150 as a MCM against Lung-ARS. BARDA is the government agency responsible for the advanced development and purchase of medical countermeasures for chemical, biological, radiological and nuclear threats. The contract contemplates the advanced development of 10150 through approval by the FDA under 21 CFR Part 314 Subpart I and Part 601 Subpart H (the "Animal Rule.") The Animal Rule allows for approval of drugs using only animal studies when human clinical trials cannot be conducted ethically. The ultimate goal of the BARDA Contract is to complete all of the work necessary to obtain FDA approval for 10150 as a MCM for Lung-ARS. In addition, the BARDA Contract is designed to generate the data that would allow for acquisition of the drug by BARDA prior to FDA approval under a pre-Emergency Use Authorization.

Pursuant to the BARDA Contract we were awarded approximately $10.4 million for the base period of the contract. On April 16, 2012, we announced that BARDA had exercised two options under the BARDA Contract worth approximately $9.1 million. On September 17, 2013, we announced that BARDA had exercised $6.0 million in additional contract options. On May 07, 2014, we announced that BARDA had exercised a Contract Modification worth approximately $1.8 million. The Contract Modification allowed Aeolus to reconcile actual costs incurred with billings under the original provisional indirect billing rate. It established a new provisional indirect billing rate and placed a cap on the current and future provisional indirect billing rates. On June 26, 2015, we announced that BARDA had exercised $3.0 million in additional contract options under its advanced research and development contract for AEOL 10150. The June option exercise brings the total contract value exercised as of September 30, 2015 to approximately $30.3 million. We may receive up to an additional $88.1 million in options exercisable over the remainder of the BARDA Contract. Options are exercised based on the progress of the development program, including the completion of clinical trials or manufacturing tasks under previously exercised options.

The final goal of the contract is to achieve FDA approval for 10150 and the development of commercial manufacturing capability. In order to achieve these goals, we believe it will be necessary to exercise the majority of the options in the contract. We also believe that BARDA is likely to continue to exercise options as long as 10150 continues to demonstrate efficacy and safety in animal testing for Lung-ARS. In the event we begin sales to the U.S. government following the filing of a pre-EUA application, we believe that BARDA is likely to exercise the majority of the remaining options under the contract. One of the requirements of an EUA is that the development program continue towards the goal of FDA approval. If all of the options are exercised by BARDA, the total value of the contract would be approximately $118.4 million.

There are no existing treatments for Lung-ARS or DEARE and we are not aware of any compounds in development that have shown efficacy in increasing survival when administered after exposure to radiation. 10150 has demonstrated efficacy in two animal models (mouse and non-human primate) when administered after exposure to radiation. The U.S. government's planning scenario for a radiation incident is a 10 kiloton detonation of a nuclear device in a major American city. It is estimated that several hundred thousand civilians would be exposed to high doses of radiation in this scenario.

The BARDA contract is also designed to complete the work necessary for 10150 to be purchased for the US Strategic National Stockpile (the "SNS"). BARDA currently acquires drugs for the SNS through a Special Reserve Fund (the "SRF") created under Project BioShield and reauthorized under the Pandemic All-Hazards Preparedness Reauthorization Act of 2013. Although the final goal of the contract is full FDA approval under the Animal Rule, BARDA may purchase product prior to FDA approval following the filing of a pre-EUA application. BARDA has made numerous acquisitions of compounds that were not approved by the FDA, but were the subject of a pre-EUA filing. Procurements from BARDA following a pre-EUA application could result in a significant increase in revenues for Aeolus and potential profitability.

In August 2014, we filed an Investigational New Drug ("IND") application with the Division of Medical Imaging Products of the U.S. Food & Drug Administration ("FDA") for 10150 as a treatment for Lung-ARS. On September 4, 2014, the Company announced positive results from a study in non-human primates exposed to lethal radiation and treated with 10150. The study demonstrated that administration of 10150 24 hours after exposure to lethal radiation impacted survival at six months post-exposure as follows: survival in the 60 day treatment group was 50%, compared to 25% survival in the radiation only untreated control group. The data from this study, combined with development work completed in manufacturing and human safety data, will form the basis for a pre-EUA application. On September 22, 2014, we received a letter from the FDA placing our proposed Phase I study in healthy normal volunteers for 10150 as a treatment for Lung-ARS on clinical hold. (See - "Future Development Plans" and "Risk Factors – Risks Related to Our Business; Our commercialization efforts may be adversely impacted by an FDA clinical hold on our Phase I clinical trial in Lung-ARS.") The FDA provided the Company with specific concerns that need to be addressed in order to allow for the initiation of studies in healthy normal volunteers. In consultation with BARDA, the Company has submitted a mitigation strategy to the FDA for their review and feedback. The Company filed a complete response to the FDA's question in January 2016 and expects the FDA to review and respond to that submission within 30 days.

We also benefit from research funded by grants from the NIH CounterACT program for the development of 10150 as a MCM for the effects of nerve gas (e.g., sarin and soman) and chemical vesicant gasses (e.g., mustard gas, phosgene gas and chlorine gas) exposure. Funding for this indication is provided directly to the research institution and does not flow through our financial statements. Continued funding is generally dependent on continuing evidence of efficacy in animal trials. In October 2011, we announced that National Jewish Health was awarded a $12.5 million grant from NIH CounterACT to continue the development of 10150 as a MCM against chlorine gas exposure. Also included in the grant is support for research in looking at tissue plasminogen activator ("TPA") and Silabilin, which are not Aeolus assets, as MCMs against sulfur mustard gas exposure. The ultimate objective of the sulfur mustard and chlorine gas work at National Jewish Health will be to complete all work necessary to initiate pivotal efficacy studies in animals for both indications. This would include: running efficacy studies in the rat model for higher doses of sulfur mustard and chlorine gas; establishing endpoints, optimal dosing and duration of treatment for pivotal efficacy studies; and characterizing the natural history from sulfur mustard and chlorine gas damage.

We are also funded by grant money from the NIH CounterACT program and the National Institute of Neurological Disorders and Stroke ("NINDS") for the development of 10150 as a MCM for the effects of nerve gas (e.g., sarin and soman) exposure. NIH-CounterACT awarded a contract on September 24, 2011 worth approximately $735,000, to the University of Colorado to develop 10150 as a MCM against nerve agents. Work performed with this initial funding has demonstrated that 10150 significantly improved survival when administered with current treatment in a pilocarpine model for nerve gas exposure. In September 2013, we announced that Dr. Manisha Patel at the University of Colorado had been awarded a $4.3 million grant from NINDS to further develop as a MCM for exposure to sarin gas and other nerve agents.

Substantially all of the past costs for the Lung-ARS program have been funded by the BARDA Contract. To date, the chlorine, phosgene, mustard gas and nerve agent programs have been funded by NIH-CounterACT and NINDS through programs at National Jewish Health, the University of Colorado, and the United States Army Medical Research Institute for Chemical Defense ("USAMRICD").

We are also developing 10150 for the treatment of lung fibrosis, including idiopathic pulmonary fibrosis ("IPF") and other fibrotic diseases. This new development program was created based upon the data generated from animal studies in Lung-ARS and chemical gas exposure under the BARDA Contract and NIH grants. On March 17, 2015, we announced that 10150 was granted Orphan Drug Designation for IPF by the U.S Food and Drug Administration ("FDA"). The Company plans to initiate a Phase 1 safety study in patients with IPF in 2016. After we have completed safety studies, we plan to initiate efficacy studies in patients with IPF. We expect a portion of the net proceeds from the 2015 Securities Placement will be used to fund a portion of the future costs of work associated with IPF and other fibrotic diseases.

We are also developing 10150 for use in combination with radiation therapy for cancer as a treatment to reduce side effects caused by radiation toxicity and to improve local tumor control. Pre-clinical studies at Duke University and Loma Linda University have demonstrated that 10150 does not interfere with the benefit of radiation therapy or chemotherapy in prostate and lung cancer. Additional studies have shown that 10150 enhances the anti-tumor activity of radiation and chemotherapy. A significant portion of the development work funded by the BARDA contract is applicable to the development program for radiation oncology, including safety, toxicology, pharmacokinetics and Chemistry, Manufacturing and Controls ("CMC"). After we have completed safety studies, we plan to initiate studies to demonstrate efficacy in ameliorating the toxic side effects related to radiation therapy and, potentially, enhancing tumor control. We expect a portion of the net proceeds from the 2015 Securities Placement will be used to fund a portion of the future costs of work related to radiation therapy opportunities.

10150 has been tested in two human Phase I safety studies where it was well-tolerated and no adverse events were observed. Efficacy has been demonstrated in animal models for Lung-ARS, chlorine gas exposure, phosgene gas exposure, sulfur mustard gas exposure (lungs and skin) and nerve gas exposure. In both mouse and non-human primate ("NHP") studies for Lung-ARS, 10150 treated groups showed significantly reduced weight loss, inflammation, oxidative stress, lung damage, and most importantly, mortality. Therapeutic efficacy has been demonstrated when 10150 is administered 24 hours after exposure to radiation, a requirement for consideration as a radiation MCM for the SNS.

Following the events at the Fukushima nuclear plant in Japan in 2011, we performed radiation exposure studies in mice at the request of Japanese researchers to determine how the administration of AEOL 10150 would impact the use of leukocyte growth factors ("LGF") used to treat the hematopoietic or bone marrow syndrome of ARS ("H-ARS"). Data showed that 10150 does not interfere with the efficacy of LGF (in this case Amgen's Neupogen®). Additionally, the study demonstrated that administration of Neupogen®, the current standard of care for H-ARS, increased damage to the lungs. When 10150 was administered with Neupogen® this damage was significantly reduced. We believe that this finding may have important implications for the potential procurement of 10150 for the SNS. In September 2013, BARDA announced that it had entered into a procurement and inventory management agreement with Amgen to provide Neupogen® for the SNS. On March 30, 2015, the FDA approved Neupogen® for the treatment of H-ARS.

We have an active Investigational New Drug Application ("IND") on file with the FDA for AEOL 10150 as a potential treatment for amyotrophic lateral sclerosis ("ALS"). At this time, we do not have any plans to continue development of 10150 for ALS.

We have already completed two Phase I safety studies in 50 humans (39 receiving drug and 13 control) demonstrating that 10150 is safe and well tolerated. CMC work has been completed, pilot lots have been prepared and production is being scaled up under the BARDA Contract.

The Company is developing a second compound, AEOL 11114 ("11114"), as a treatment for Parkinson's disease. Research funded by the Michael J Fox Foundation for Parkinson's disease ("MJFF") demonstrated the neuro-protective activity of 11114 in mouse and rat models of Parkinson's disease. The compounds were invented by Aeolus in collaboration with Brian J. Day, PhD at National Jewish Health and Manisha Patel, PhD at the University of Colorado, Anschutz Medical Campus, Department of Pharmaceutical Sciences in collaboration with the Company. We have obtained worldwide, exclusive licenses to develop the compounds from NJH and the UC. We plan to complete the remaining work to file an Investigational New Drug ("IND") application with the FDA by 2017.

In April 2015, we announced the discovery of a new compound, AEOL 20415 ("20415"), that has demonstrated anti-inflammatory and anti-infective properties, and could be effective in treating cystic fibrosis and combatting anti-biotic resistant bacteria. The compound was developed under a collaboration between Brian J. Day, PhD at National Jewish Health in Denver, Colorado and Aeolus Pharmaceuticals. We have obtained a worldwide, exclusive license to develop the rights to the compound from NJH. We plan to complete the remaining work to file an Investigational New Drug ("IND") application with the FDA by 2017.

Risks Associated with Our Business

Our business is subject to numerous risks. Please see the "Risk Factors" section beginning on page 8 of this prospectus.

Corporate Information

We were incorporated in the State of Delaware in 1994. Our common stock trades on the OTC Bulletin Board under the symbol "AOLS." Our principal executive offices are located at 26361 Crown Valley Parkway, Suite 150, Mission Viejo, California 92691, and our phone number at that address is (949) 481-9825. Our website address is www.aeoluspharma.com. However, the information in, or that can be accessed through, our web site is not part of the registration statement of which this prospectus forms a part. We also make available free of charge through our website our most recent annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to those reports, as soon as reasonably practicable after such material is electronically filed with or furnished to the Securities and Exchange Commission, which we refer to as the SEC.

THE OFFERING

|

Common stock offered by us

|

None

|

|

Common stock offered by selling stockholders

|

73,432,471, including (i) 15,629,676 shares of common stock issued and outstanding as of the date of this prospectus, (ii) 20,454,456 shares of common stock issuable upon conversion of Series C Convertible Preferred Stock (the "Conversion Shares") and (iii) 37,298,249 shares of common stock issuable upon the exercise of warrants (the "Warrant Shares").

|

|

Charter Amendment

|

In order to facilitate the potential future issuance of Conversion Shares and Warrant Shares, the Company expects to complete a Charter Amendment (defined below) on or about March 10, 2016. As used in this prospectus, "Charter Amendment" means an amendment to the Company's Certificate of Incorporation to increase the authorized number of shares of common stock available for issuance by the Company or to effect a reverse common stock split without altering the number of shares of common stock previously authorized.

|

| |

|

|

Factors affecting the issuance of Conversion Shares and Warrant Shares

|

The Company is not obligated to issue Conversion Shares or Warrant Shares (i) if the holder, including its affiliates, would thereby beneficially own in excess of 9.99% of the Company's common stock and (ii) in no case prior to March 10, 2016.

|

|

OTC Bulletin Board Symbol

|

"AOLS"

|

|

Proceeds to us

|

We will not receive any proceeds from the sale of the shares of common stock covered by this prospectus. However, we will receive the proceeds of any cash exercise of the warrants.

|

|

Risk factors

|

Investing in our common stock involves certain risks. You should read "Risk Factors" beginning on page 8 for a discussion of factors that you should consider carefully before deciding whether to purchase shares of our common stock.

|

RISK FACTORS

You should carefully consider the following information about risks described below, together with the other information contained in this prospectus and in our other filings with the SEC, before you decide to buy or maintain an investment in our common stock. We believe the risks described below are the risks that are material to us as of the date of this prospectus. If any of the following risks actually occur, our business, financial condition, results of operations and future growth prospects would likely be materially and adversely affected. In these circumstances, the market price of our common stock could decline, and you may lose all or part of your investment.

Risks Related to Our Business

We have operated at a loss and will likely continue to operate at a loss for the foreseeable future.

We have incurred significant historical losses and had an accumulated deficit of approximately $186,630,000 as of September 30, 2015. While the vast majority of this accumulated deficit relates to development programs that were abandoned before 2014 (our "Discontinued Development Programs"), our current development programs (primarily 10150, and to a lesser extent 11114 and 20415) continue to generate losses. During the years ended September 30, 2015 and 2014, we incurred losses of $2,628,000 and $80,000, respectively. Our operating losses have been due primarily to our expenditures for research and development on our drug candidates and for general and administrative expenses and our lack of significant, or sufficient, revenues to offset all of the expenditures. We are likely to continue to incur operating losses until such time, if ever, that we generate significant recurring revenues from product sales, whether to the U.S. government for the Strategic National Stockpile or to the general healthcare community for commercial indications, like oncology, epilepsy or Parkinson's Disease. We anticipate it will take a minimum of two years (and possibly longer) for us to generate recurring revenues. We expect that it will take at least that long before the development of any of our licensed, or other current potential, products is completed, marketing approvals are obtained from the FDA and commercial sales of any of these products can begin, or that we might receive a procurement from the U.S. Government following a pre-Emergency Use Authorization application or Animal Rule Approval.

We may need substantial additional funding to continue our operations and may be unable to raise capital when needed, or at all, which would force us to delay, curtail or eliminate our clinical programs and our product development programs.

We may need to raise substantial additional capital to fund human clinical trials and continue our research and development, unless and until we receive a procurement of sufficient size from the U.S. Government for the Strategic National Stockpile. In addition, we may need to raise substantial additional capital to enforce our proprietary rights, defend, in litigation or otherwise, any claims that we infringe third party patents or other intellectual property rights; and commercialize, for non-government related indications, any of our products that may be approved by the FDA or any international regulatory authority.

As of December 31, 2015, we had cash of approximately $5,444,000. As of December 31, 2015, our monthly cash requirements to operate our business that are not reimbursed under the BARDA Contract are approximately $204,000. To the extent we do not have sufficient cash to fund our working capital requirements; we may not be able to pay our payables timely, which may cause vendors to cease providing services to us.

In order to fund on-going operating cash requirements, or to accelerate or expand our oncology and other programs we will need to raise significant additional funds. We are continuously considering strategic and financial options available to us, including public or private equity offerings, debt financings or collaboration arrangements. If we raise additional funds by issuing securities, our stockholders will experience dilution of their ownership interest. Debt financings, if available, may involve restrictive covenants and require significant interest payments. If we do not receive additional financing to fund our operations not reimbursed under the BARDA Contract, or if BARDA does not exercise any additional options under the BARDA Contract, and we are unable to raise sufficient capital for operations, we would have to discontinue some or all of our activities, merge with or sell, lease or license some or all of our assets to another company, or cease operations entirely, and our stockholders might lose all or part of their investments.

In addition, if our non-biodefense, commercial development program shows scientific progress, we will need significant additional funds to move therapies through the preclinical stages of development and clinical trials. If we are unable to raise the amount of capital necessary, or do not receive a sufficient procurement from the U.S. Government for the Strategic National Stockpile, to complete development and reach commercialization of any of our catalytic antioxidant products, we will need to delay or cease development of one or more of these products or partner with another company for the development and commercialization of these products.

We have a history of operating losses and expect to continue to incur substantial losses and may never become profitable.

We have no products approved for commercialization in the United States or abroad. Our drug candidates are still being developed, and all but 10150 are still in early stages of development. Our drug candidates will require significant additional development, clinical trials, regulatory clearances or approvals by the FDA and additional investment before they can be commercialized in the United States.

Our likelihood of achieving profitability will depend on numerous factors, including success in:

• developing our existing drug candidates and developing and testing new drug candidates;

• protecting our intellectual property;

• establishing our competitive position;

• achieving third-party collaborations;

• receiving regulatory approvals;

• manufacturing and marketing products; and

• receiving government funding and identifying new government funding opportunities.

Many of these factors will depend on circumstances beyond our control. We may not achieve sufficient revenues for profitability. Even if we do achieve profitability, we may not be able to sustain or increase profitability on a quarterly or annual basis in the future. If revenues grow more slowly than we anticipate, or if operating expenses exceed our expectations or cannot be adjusted accordingly, then our business, results of operations, financial condition and cash flows will be materially and adversely affected.

As of September 30, 2015, we had an accumulated deficit of $186,630,000 from our research, development and other activities, the vast majority of which is related to Discontinued Development Programs. We have not generated material revenues from product sales and do not expect to generate product revenues sufficient to support us for at least several more years. As a result, we may not be successful in obtaining sufficient financing on commercially reasonable terms, or at all. Our requirements for additional capital may be substantial and will be dependent on many factors, including the success of our research and development efforts, our ability to commercialize and market products, our ability to successfully pursue our licensing and collaboration strategy, the receipt of government funding, competing technological developments, costs associated with the protection of our intellectual property and any future change in our business strategy.

Our research and development ("R&D") activities are at an early stage and therefore might never result in viable products.

Our catalytic antioxidant program is in the early stages of development, involves unproven technology, requires significant further R&D and regulatory approvals and is subject to the risks of failure inherent in the development of products or therapeutic procedures based on innovative technologies. These risks include the possibilities that:

|

• |

any or all of these proposed products or procedures are found to be unsafe or ineffective or otherwise fail to receive necessary regulatory approvals; |

|

• |

the proposed products or procedures are not economical to market or do not achieve broad market acceptance; |

|

• |

third parties hold proprietary rights that preclude us from marketing the proposed products or procedures; and |

|

• |

third parties market a superior or equivalent product. |

Further, the timeframe for commercialization of any product is long and uncertain because of the extended testing and regulatory review process required before marketing approval can be obtained. We may not be able to successfully develop or market any of our proposed products or procedures. If we are not able to successfully market any product, our business will suffer.

Our commercialization efforts may be adversely impacted by an FDA clinical hold on our Phase I clinical trial in Lung-ARS.

In September of 2014, the Company received notice from the FDA that our IND for 10150 for Lung ARS has been placed on a clinical hold following their review of our data. A clinical hold is an order that the FDA issues to a trial sponsor to suspend all ongoing clinical trials and delay all proposed trials. With this clinical hold, any patients in an ongoing clinical trial cannot receive treatment with 10150. Therefore, initiation of this Phase I clinical trial will be delayed indefinitely and may not occur at all. In particular, until the FDA lifts the clinical hold, or partially lifts the full clinical hold, we will be unable to submit any new clinical trial protocols to the FDA under our IND for 10150 for Lung ARS. If the FDA does not lift the full clinical hold, we may be unable to pursue the development of 10150 for Lung ARS.

The FDA provided the Company with specific concerns that need to be addressed in order to allow for the initiation of studies in healthy normal volunteers. In consultation with BARDA, the Company submitted a mitigation strategy to the FDA for their review and requested a meeting with the FDA to discuss and receive feedback. On March 12, 2015, the Company met with the FDA and received feedback and further guidance on the requirements for release of the clinical hold. In its written and verbal comments to the Company, the FDA requested that the Company provide an explanation for positive results seen in the Ames Assay testing of AEOL 10150, and indicated that if the Company could produce data to explain why results in four in-vivo gentox studies have been negative, but that results in the Ames were positive, the FDA would release the clinical hold. A complete response to the FDA's question was filed in January 2016 and we expect a response within 30 days. There can be no assurance, however, that the FDA will release the clinical hold.

Our ability to advance our commercialization objectives may be limited by limitation on our access to capital, the absence of any current ability to manufacture our drug candidates on a commercial scale and the absence of any internal marketing capabilities and external marketing arrangements.

In light of the limited number of employees we currently have, our limited resources, and the early stage of our commercial development efforts, our future success may be limited. In addition, there are significant uncertainties as to our ability to access potential sources of capital, and we may not be able to enter into industry partner collaborations that would provide us with liquidity sources on terms acceptable to us, or at all. These uncertainties may be due to a variety of factors, including evolving or adverse conditions in the pharmaceutical industry or in the economy in general or based on the prospects of our commercial programs. Even if we are successful in obtaining collaboration for our commercial programs, we may have to relinquish rights to technologies, product candidates or markets that we might otherwise develop ourselves. These same risks apply to any attempt to out-license our compounds. Moreover, even if our commercialization efforts advance, we currently do not have the capability to manufacture any of our drug candidates on a commercial scale and our ability to develop this capability will be limited since it will be resource intensive and costly. Finally, our product candidates are being developed for large therapeutic markets. We believe these markets are best approached by partnering with established biotechnology or pharmaceutical companies that have broad sales and marketing capabilities. We are pursuing marketing collaborations of this type as part of our search for development partners. However, we may not be able to enter into any marketing arrangements for any of our products on satisfactory terms or at all.

If our products are not successfully developed and eventually approved by the FDA, we may be forced to reduce or terminate our operations.

All of our drug candidates are at various stages of development and must be approved by the FDA or similar foreign governmental agencies before they can be marketed. The process for obtaining FDA and foreign regulatory approval is both time-consuming and costly, with no certainty of a successful outcome. This process typically requires extensive preclinical and clinical testing, which may take longer or cost more than we anticipate, and may prove unsuccessful due to numerous factors. Drug candidates that may appear to be promising at early stages of development may not successfully reach the market for a number of reasons. The results of preclinical and initial clinical testing of these drug candidates may not necessarily indicate the results that will be obtained from later or more extensive testing. A number of companies in the pharmaceutical and biotechnology industries have suffered significant setbacks in advanced clinical trials, even after obtaining promising results in earlier trials.

Numerous factors could affect the timing, cost or outcome of our drug development efforts, including the following:

• difficulty in securing research laboratories to conduct research activities;

• difficulty in securing centers to conduct trials;

• difficulty in enrolling patients in conformity with required protocols or projected timelines;

• unexpected adverse reactions by patients in trials;

• difficulty in obtaining clinical supplies of the product;

|

• |

changes in the FDA's or other regulatory body's requirements for our testing during the course of that testing; |

• inability to generate statistically significant data confirming the efficacy of the product being tested;

• modification of the drug during testing; and

• reallocation of our limited financial and other resources to other clinical programs.

It is possible that none of the products we develop will obtain the regulatory approvals necessary for us to begin commercializing them. The time required to obtain FDA and other approvals is unpredictable but often can take years following the commencement of clinical trials, depending upon the nature of the drug candidate. Any analysis we perform on data from clinical activities is subject to confirmation and interpretation by regulatory authorities, which could delay, limit or prevent regulatory approval. Any delay or failure in obtaining required approvals could have a material adverse effect on our ability to generate revenues from the particular drug candidate and we may not have the financial resources to continue to develop our drug candidates and, as a result, may have to terminate our operations.

If we do not reach the market with our products before our competitors offer products for the same or similar uses, or if we are not effective in marketing our products, our revenues from product sales, if any, will be reduced.

We face intense competition in our development activities. Many of our competitors are fully integrated pharmaceutical companies, biotechnology companies or more established bioterrorism product companies, which have substantially greater financial, technical, sales and marketing and human resources than we do. These companies might succeed in obtaining regulatory approval for competitive products more rapidly than we can for our products. In addition, competitors might develop technologies and products that are less expensive and perceived to be safer or more effective than those being developed by us, which could impair our product development and render our technology obsolete.

We are and expect to remain dependent upon collaborations with third parties for the development of new products, and adverse events involving these collaborations could prevent us from developing and commercializing our drug candidates and achieving profitability.

We currently license from third parties, and do not own, rights under patents and certain related intellectual property for the development of our drug candidates. In addition, we expect to enter into agreements with third parties to license rights to our drug candidates. We might not be able to enter into or maintain these agreements on terms favorable to us, if at all. Further, if any of our current licenses were to expire or terminate, our business, prospects, financial condition and results of operations could be materially and adversely affected.

Our research and development activities rely on technology licensed from third parties, and termination of any of those licenses would result in loss of significant rights to develop and market our products, which would impair our business, prospects, financial condition and results of operations.

We have exclusive worldwide rights to our antioxidant small molecule technology through license agreements with Duke and the NJH. Each license generally may be terminated by the licensor if we fail to perform our obligations under the agreement, including obligations to develop the compounds and technologies under license. If terminated, we would lose the right to develop the products, which could adversely affect our business, prospects, financial condition and results of operations. The license agreements also generally require us to meet specified milestones or show reasonable diligence in development of the technology. If disputes arise over the definition of these requirements or whether we have satisfied the requirements in a timely manner, or if any other obligations in the license agreements are disputed by the other party, the other party could terminate the agreement, and we could lose our rights to develop the licensed technology.

If new technology is developed from these licenses, we may be required to negotiate certain key financial and other terms, such as royalty payments, for the licensing of this future technology with these research institutions, and it might not be possible to obtain any such license on terms that are satisfactory to us, or at all.

We now rely, and will continue to rely, heavily on third parties for product and clinical development, manufacturing, marketing and distribution of our products.

We currently depend heavily and will depend heavily in the future on third parties for support in product development, clinical development, manufacturing, marketing and distribution of our products. The termination of some or all of our existing collaborative arrangements, or our inability to establish and maintain collaborative arrangements, could have a material adverse effect on our ability to continue or complete clinical development of our products.

We rely on contract clinical research organizations ("CROs") for various aspects of our clinical development activities including clinical trial monitoring, data collection and data management. As a result, we have had and continue to have less control over the conduct of clinical trials, the timing and completion of the trials, the required reporting of adverse events and the management of data developed through the trial than would be the case if we were relying entirely upon our own staff. Although we rely on CROs to conduct our clinical trials, we are responsible for confirming that each of our clinical trials is conducted in accordance with the investigational plan and protocol. Moreover, the FDA and foreign regulatory agencies require us to comply with GCPs for conducting, recording and reporting the results of clinical trials to assure that the data and results are credible and accurate and that the trial participants are adequately protected. Our reliance on third parties does not relieve us of these responsibilities and requirements.

The third parties on which we rely may have staffing difficulties, may undergo changes in priorities or may become financially distressed, adversely affecting their willingness or ability to conduct our trials. We may experience unexpected cost increases that are beyond our control. Any failure of such CROs to successfully accomplish clinical trial monitoring, data collection and data management and the other services they provide for us in a timely manner and in compliance with regulatory requirements could have a material adverse effect on our ability to complete clinical development of our products and obtain regulatory approval. Problems with the timeliness or quality of the work of a CRO may lead us to seek to terminate the relationship and use an alternate service provider. However, making such changes may be costly and would likely delay our trials, and contractual restrictions may make such a change difficult or impossible. Additionally, it may be difficult to find a replacement organization that can conduct our trials in an acceptable manner and at an acceptable cost.

If BARDA opts not to exercise its options under the BARDA Contract, we would be dependent upon grants from NIH for continued development of 10150 for Lung-ARS, or we would need to curtail our development program in this area significantly and we may be placed at a competitive disadvantage in addressing this market opportunity.

During the fiscal years ended September 30, 2015 and 2014, we received 100% of our revenues from our agreement with BARDA, for the development of 10150 as a MCM against Lung-ARS. These revenues have funded some of our personnel and other R&D costs and expenses. Pursuant to the BARDA Contract, we received approximately $10.4 million under the base period of the contract from February 2011 to April 2012. On April 9, 2012, we announced that BARDA had issued a Notice of Intent to Exercise two options valued at $9.1 million. On April 16, 2012, BARDA exercised the two options. On September 17, 2013, we announced that BARDA had exercised $6.0 million in additional contract options. On May 5, 2014, we announced that BARDA had exercised $1.8 million in additional contract options. On June 26, 2015, we announced that BARDA had exercised $3.0 million in additional contract options, bringing the total value to date to approximately $30.3 million. We may receive up to an additional $88.1 million in options exercisable over the remaining years of the contract. If all of the options are exercised by BARDA, the total value of the contract would be approximately $118.4 million.

Under the terms of the BARDA Contract, BARDA may elect not to exercise some or all of the additional options. Because a significant portion of our current revenues are generated from the BARDA Contract, if BARDA does not exercise its options under the BARDA Contract, our ability to develop 10150 as an MCM for Lung-ARS could be negatively impacted, which could harm our competitive position and materially and adversely affect our business, financial condition and results of operations. In general, we believe that future exercise of options under the contract will depend on successful completion of tasks under exercised options and continued demonstration of efficacy.

Necessary reliance on the "Animal Rule" in conducting trials is time-consuming and expensive.

To obtain FDA approval for our drug candidate for a bioterrorism indication under current FDA regulations, we are required to utilize animal model studies for efficacy and provide animal and human safety data under the "Animal Rule." For many of the biological and chemical threats, animal models are not yet available, and as such we are developing, or will have to develop, appropriate animal models, which is a time-consuming and expensive research effort. Further, we may not be able to sufficiently demonstrate the animal correlation to the satisfaction of the FDA, as these corollaries are difficult to establish and are often unclear. The FDA may decide that our data are insufficient for approval and require additional preclinical, clinical or other studies, refuse to approve our products, or place restrictions on our ability to commercialize those products. Further, other countries do not, at this time, have established criteria for review and approval of these types of products outside their normal review process; i.e., there is no "Animal Rule" equivalent, and consequently we may not be able to make a submission for marketing approval in foreign countries based on such animal data.

Additionally, few facilities in the U.S. and internationally have the capability to test animals with radiation, nerve agents, or other lethal biotoxins or chemical agents or otherwise assist us in qualifying the requisite animal models. We have to compete with other biodefense companies for access to this limited pool of highly specialized resources. We therefore may not be able to secure contracts to conduct the testing in a predictable timeframe, cost-effectively or at all.

Even if we succeed in commercializing our drug candidates, we may not become profitable and manufacturing problems or side effects discovered at later stages can further increase costs of commercialization.

Any drugs resulting from our research and development efforts may not become commercially available. Even if we succeed in developing and commercializing our drug candidates, we may never generate sufficient or sustainable revenues to enable us to be profitable. Even if effective, a product that reaches the market may be subject to additional clinical trials, changes to or re-approvals of our manufacturing facilities or a change in labeling if we or others identify side effects or manufacturing problems after a product is on the market. This could harm sales of the affected products and could increase the cost and expenses of commercializing and marketing them. It could also lead to the suspension or revocation of regulatory approval for the products.

We and our contract manufacturing organizations ("CMOs") will also be required to comply with the applicable FDA current good manufacturing practice ("cGMP") regulations. These regulations include requirements relating to quality control and quality assurance as well as the corresponding maintenance of records and documentation. Manufacturing facilities are subject to inspection by the FDA. These facilities must be approved to supply licensed products to the commercial marketplace. We and our contract manufacturers may not be able to comply with the applicable cGMP requirements and other FDA regulatory requirements. Should we or our contract manufacturers fail to comply, we could be subject to fines or other sanctions or could be prohibited from marketing any products we develop.

Political or social factors may delay or impair our ability to market our products and our business may be materially adversely affected.

Products developed to treat diseases caused by, or to combat the threat of, bioterrorism will be subject to changing political and social environments. The political and social responses to bioterrorism have been unpredictable. Political or social pressures may delay or cause resistance to bringing our products to market or limit pricing of our products, which would harm our business. Changes to favorable laws, such as Project BioShield, could have a material adverse effect on our business, prospects, financial condition and results of operations.

Legislation limiting or restricting liability for medical products used to fight bioterrorism is new, and we cannot be certain that any such protection will apply to our products or if applied what the scope of any such coverage will be.

The U.S. Public Readiness Act was signed into law in December 2005 (the "Public Readiness Act") and creates general immunity for manufacturers of countermeasures, including security countermeasures (as defined in Section 319F-2(c)(1)(B) of the Public Readiness Act), when the U.S. Secretary of Health and Human Services issues a declaration for their manufacture, administration or use. The declaration is meant to provide general immunity from all claims under state or federal law for loss arising out of the administration or use of a covered countermeasure. Manufacturers are excluded from this protection in cases of willful misconduct. The Secretary of Health and Human Services may not make declarations that would cover any of our other drug candidates or the U.S. Congress may not act in the future to reduce coverage under the Public Readiness Act or it may repeal it altogether.

Upon a declaration by the Secretary of Health and Human Services, a compensation fund would be created to provide "timely, uniform and adequate compensation to eligible individuals for covered injuries directly caused by the administration or use of a covered countermeasure." The "covered injuries" to which the program applies are defined as serious physical injuries or death. Individuals are permitted to bring a willful misconduct action against a manufacturer only after they have exhausted their remedies under the compensation program. A willful misconduct action could be brought against us if an individual(s) has exhausted his or her remedies under the compensation program, which could thereby expose us to liability. Furthermore, the Secretary of Health and Human Services may not issue a declaration under the Public Readiness Act to establish a compensation fund. We may also become subject to standard product liability suits and other third party claims if products we develop which fall outside of the Public Readiness Act cause injury or if treated individuals subsequently become infected or otherwise suffer adverse effects from such products.

Healthcare reform measures and other statutory or regulatory changes could adversely affect our business.

The pharmaceutical and biotechnology industries are subject to extensive regulation, and from time to time legislative bodies and governmental agencies consider changes to such regulations that could have significant impact on industry participants. For example, in light of certain highly-publicized safety issues regarding certain drugs that had received marketing approval, the U.S. Congress is considering various proposals regarding drug safety, including some which would require additional safety studies and monitoring and could make drug development more costly. We are unable to predict what additional legislation or regulation, if any, relating to safety or other aspects of drug development may be enacted in the future or what effect such legislation or regulation would have on our business.

The business and financial condition of pharmaceutical and biotechnology companies are also affected by the efforts of governments, third-party payors and others to contain or reduce the costs of healthcare to consumers. In the United States and various foreign jurisdictions there have been, and we expect that there will continue to be, a number of legislative and regulatory proposals aimed at changing the healthcare system, such as the Affordable Care Act and proposals relating to the reimportation of drugs into the U.S. from other countries (where they are then sold at a lower price) and government control of prescription drug pricing. The roll-out, pendency or approval of such proposals could affect our commercialization efforts and result in a decrease in our share price or limit our ability to raise capital or to obtain strategic collaborations or licenses.

We will need to enter into collaborative arrangements for the manufacturing and marketing of our drug candidates, or we will have to develop the expertise, obtain the additional capital and invest the resources to perform those functions internally.

We do not have the staff or facilities to manufacture or market any of the drug candidates being developed in our catalytic antioxidant program. As a result, we will need to enter into collaborative arrangements to commercialize, manufacture and market products that we expect to emerge from our catalytic antioxidant program, or develop the expertise within Aeolus. We might not be successful in entering into such third party arrangements on terms acceptable to us, if at all. If we are unable to obtain or retain third-party manufacturing or marketing on acceptable terms, we may be delayed in our ability to commercialize products, which could have a material adverse effect on our business, prospects, financial condition and results of operations. Substantial additional funds and personnel would be required if we needed to establish our own manufacturing or marketing operations. We may not be able to obtain adequate funding or establish these capabilities in a cost-effective or timely manner, which could have a material adverse effect on our business, prospects, financial condition and results of operations.

A failure to obtain or maintain patent and other intellectual property rights would allow others to develop and sell products similar to ours, which could impair our business, prospects, financial condition and results of operations.