true

2024

Q2

0001883835

0001883835

2024-01-01

2024-06-30

0001883835

2024-06-30

0001883835

2023-12-31

0001883835

2022-12-31

0001883835

2024-04-01

2024-06-30

0001883835

2023-04-01

2023-06-30

0001883835

2023-01-01

2023-06-30

0001883835

2023-01-01

2023-12-31

0001883835

2022-01-01

2022-12-31

0001883835

us-gaap:CommonStockMember

2023-12-31

0001883835

us-gaap:AdditionalPaidInCapitalMember

2023-12-31

0001883835

us-gaap:RetainedEarningsMember

2023-12-31

0001883835

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-12-31

0001883835

ESGH:TotalCompanysEquityMember

2023-12-31

0001883835

us-gaap:NoncontrollingInterestMember

2023-12-31

0001883835

us-gaap:CommonStockMember

2024-03-31

0001883835

us-gaap:AdditionalPaidInCapitalMember

2024-03-31

0001883835

us-gaap:RetainedEarningsMember

2024-03-31

0001883835

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2024-03-31

0001883835

ESGH:TotalCompanysEquityMember

2024-03-31

0001883835

us-gaap:NoncontrollingInterestMember

2024-03-31

0001883835

2024-03-31

0001883835

us-gaap:CommonStockMember

2022-12-31

0001883835

us-gaap:AdditionalPaidInCapitalMember

2022-12-31

0001883835

us-gaap:RetainedEarningsMember

2022-12-31

0001883835

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-12-31

0001883835

ESGH:TotalCompanysEquityMember

2022-12-31

0001883835

us-gaap:NoncontrollingInterestMember

2022-12-31

0001883835

us-gaap:CommonStockMember

2023-03-31

0001883835

us-gaap:AdditionalPaidInCapitalMember

2023-03-31

0001883835

us-gaap:RetainedEarningsMember

2023-03-31

0001883835

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-03-31

0001883835

ESGH:TotalCompanysEquityMember

2023-03-31

0001883835

us-gaap:NoncontrollingInterestMember

2023-03-31

0001883835

2023-03-31

0001883835

us-gaap:CommonStockMember

2021-12-31

0001883835

us-gaap:AdditionalPaidInCapitalMember

2021-12-31

0001883835

us-gaap:RetainedEarningsMember

2021-12-31

0001883835

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2021-12-31

0001883835

ESGH:TotalCompanysEquityMember

2021-12-31

0001883835

us-gaap:NoncontrollingInterestMember

2021-12-31

0001883835

2021-12-31

0001883835

us-gaap:CommonStockMember

2024-01-01

2024-03-31

0001883835

us-gaap:AdditionalPaidInCapitalMember

2024-01-01

2024-03-31

0001883835

us-gaap:RetainedEarningsMember

2024-01-01

2024-03-31

0001883835

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2024-01-01

2024-03-31

0001883835

ESGH:TotalCompanysEquityMember

2024-01-01

2024-03-31

0001883835

us-gaap:NoncontrollingInterestMember

2024-01-01

2024-03-31

0001883835

2024-01-01

2024-03-31

0001883835

us-gaap:CommonStockMember

2024-04-01

2024-06-30

0001883835

us-gaap:AdditionalPaidInCapitalMember

2024-04-01

2024-06-30

0001883835

us-gaap:RetainedEarningsMember

2024-04-01

2024-06-30

0001883835

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2024-04-01

2024-06-30

0001883835

ESGH:TotalCompanysEquityMember

2024-04-01

2024-06-30

0001883835

us-gaap:NoncontrollingInterestMember

2024-04-01

2024-06-30

0001883835

us-gaap:CommonStockMember

2023-01-01

2023-03-31

0001883835

us-gaap:AdditionalPaidInCapitalMember

2023-01-01

2023-03-31

0001883835

us-gaap:RetainedEarningsMember

2023-01-01

2023-03-31

0001883835

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-01-01

2023-03-31

0001883835

ESGH:TotalCompanysEquityMember

2023-01-01

2023-03-31

0001883835

us-gaap:NoncontrollingInterestMember

2023-01-01

2023-03-31

0001883835

2023-01-01

2023-03-31

0001883835

us-gaap:CommonStockMember

2023-04-01

2023-06-30

0001883835

us-gaap:AdditionalPaidInCapitalMember

2023-04-01

2023-06-30

0001883835

us-gaap:RetainedEarningsMember

2023-04-01

2023-06-30

0001883835

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-04-01

2023-06-30

0001883835

ESGH:TotalCompanysEquityMember

2023-04-01

2023-06-30

0001883835

us-gaap:NoncontrollingInterestMember

2023-04-01

2023-06-30

0001883835

us-gaap:CommonStockMember

2022-01-01

2022-12-31

0001883835

us-gaap:AdditionalPaidInCapitalMember

2022-01-01

2022-12-31

0001883835

us-gaap:RetainedEarningsMember

2022-01-01

2022-12-31

0001883835

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-01-01

2022-12-31

0001883835

ESGH:TotalCompanysEquityMember

2022-01-01

2022-12-31

0001883835

us-gaap:NoncontrollingInterestMember

2022-01-01

2022-12-31

0001883835

us-gaap:CommonStockMember

2023-01-01

2023-12-31

0001883835

us-gaap:AdditionalPaidInCapitalMember

2023-01-01

2023-12-31

0001883835

us-gaap:RetainedEarningsMember

2023-01-01

2023-12-31

0001883835

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-01-01

2023-12-31

0001883835

ESGH:TotalCompanysEquityMember

2023-01-01

2023-12-31

0001883835

us-gaap:NoncontrollingInterestMember

2023-01-01

2023-12-31

0001883835

us-gaap:CommonStockMember

2024-06-30

0001883835

us-gaap:AdditionalPaidInCapitalMember

2024-06-30

0001883835

us-gaap:RetainedEarningsMember

2024-06-30

0001883835

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2024-06-30

0001883835

ESGH:TotalCompanysEquityMember

2024-06-30

0001883835

us-gaap:NoncontrollingInterestMember

2024-06-30

0001883835

us-gaap:CommonStockMember

2023-06-30

0001883835

us-gaap:AdditionalPaidInCapitalMember

2023-06-30

0001883835

us-gaap:RetainedEarningsMember

2023-06-30

0001883835

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-06-30

0001883835

ESGH:TotalCompanysEquityMember

2023-06-30

0001883835

us-gaap:NoncontrollingInterestMember

2023-06-30

0001883835

2023-06-30

0001883835

ESGH:ESGMember

2023-01-16

0001883835

2023-09-01

2023-09-28

0001883835

ESGH:AUFPMember

2023-09-28

0001883835

ESGH:AUFPMember

ESGH:Mr.ZhiYangMember

2024-06-30

0001883835

ESGH:AUFPMember

ESGH:ZhihanMember

2024-06-30

0001883835

ESGH:AUFPMember

ESGH:Mr.ChrisAlonzoMember

2024-06-30

0001883835

ESGH:AUFPMember

2024-06-30

0001883835

ESGH:ESGMember

ESGH:ZhihanMember

2024-06-30

0001883835

ESGH:ESGMember

ESGH:Mr.ChristopherAlonzoMember

2024-06-30

0001883835

ESGH:AUFPMember

ESGH:Mr.ZhiYangMember

2023-12-31

0001883835

ESGH:AUFPMember

ESGH:ZhihanMember

2023-12-31

0001883835

ESGH:AUFPMember

ESGH:Mr.ChrisAlonzoMember

2023-12-31

0001883835

ESGH:AUFPMember

2023-12-31

0001883835

ESGH:ESGMember

ESGH:ZhihanMember

2023-12-31

0001883835

ESGH:ESGMember

ESGH:Mr.ChristopherAlonzoMember

2023-12-31

0001883835

ESGH:SubsidiariesInChinaMember

2024-06-30

0001883835

ESGH:AUFPMember

2024-06-30

0001883835

us-gaap:BuildingAndBuildingImprovementsMember

2024-06-30

0001883835

us-gaap:MachineryAndEquipmentMember

srt:MinimumMember

2024-06-30

0001883835

us-gaap:MachineryAndEquipmentMember

srt:MaximumMember

2024-06-30

0001883835

us-gaap:OfficeEquipmentMember

srt:MinimumMember

2024-06-30

0001883835

us-gaap:OfficeEquipmentMember

srt:MaximumMember

2024-06-30

0001883835

ESGH:LandPurchasedMember

2024-06-30

0001883835

us-gaap:UseRightsMember

2024-06-30

0001883835

us-gaap:PatentsMember

2024-06-30

0001883835

us-gaap:ComputerSoftwareIntangibleAssetMember

2024-06-30

0001883835

us-gaap:SalesRevenueNetMember

ESGH:DistributorOneMember

2024-04-01

2024-06-30

0001883835

us-gaap:SalesRevenueNetMember

ESGH:DistributorOneMember

2024-01-01

2024-06-30

0001883835

us-gaap:SalesRevenueNetMember

ESGH:DistributorTwoMember

2023-04-01

2023-06-30

0001883835

us-gaap:SalesRevenueNetMember

ESGH:DistributorTwoMember

2023-01-01

2023-06-30

0001883835

ESGH:AUMAndAUMTMember

2024-06-30

0001883835

ESGH:AUMAndAUMTMember

2024-06-30

0001883835

ESGH:AUMAndAUMTMember

2023-12-31

0001883835

ESGH:SubsidiariesInChinaMember

2023-12-31

0001883835

ESGH:AUFPMember

2023-12-31

0001883835

ESGH:AUFPMember

2022-12-31

0001883835

us-gaap:BuildingAndBuildingImprovementsMember

2023-12-31

0001883835

us-gaap:MachineryAndEquipmentMember

srt:MinimumMember

2023-12-31

0001883835

us-gaap:MachineryAndEquipmentMember

srt:MaximumMember

2023-12-31

0001883835

us-gaap:OfficeEquipmentMember

srt:MinimumMember

2023-12-31

0001883835

us-gaap:OfficeEquipmentMember

srt:MaximumMember

2023-12-31

0001883835

ESGH:LandPurchasedMember

2023-12-31

0001883835

us-gaap:UseRightsMember

2023-12-31

0001883835

us-gaap:PatentsMember

2023-12-31

0001883835

us-gaap:ComputerSoftwareIntangibleAssetMember

2023-12-31

0001883835

ESGH:AUMAndAUMTMember

2023-12-31

0001883835

ESGH:AUMAndAUMTMember

2022-12-31

0001883835

us-gaap:SalesRevenueNetMember

ESGH:DistributorOneMember

2023-01-01

2023-12-31

0001883835

us-gaap:SalesRevenueNetMember

ESGH:DistributorTwoMember

2023-01-01

2023-12-31

0001883835

ESGH:PeriodEndDateMember

2024-06-30

0001883835

ESGH:PeriodEndDateMember

2024-03-31

0001883835

ESGH:PeriodEndDateMember

2023-12-31

0001883835

ESGH:PeriodEndDateMember

2023-06-30

0001883835

ESGH:PeriodEndDateMember

2023-03-31

0001883835

ESGH:AverageUSDForTheReportingPeriodMember

2024-06-30

0001883835

ESGH:AverageUSDForTheReportingPeriodMember

2024-03-31

0001883835

ESGH:AverageUSDForTheReportingPeriodMember

2023-12-31

0001883835

ESGH:AverageUSDForTheReportingPeriodMember

2023-06-30

0001883835

ESGH:AverageUSDForTheReportingPeriodMember

2023-03-31

0001883835

ESGH:PeriodEndDateMember

2022-12-31

0001883835

ESGH:AverageUSDForTheReportingPeriodMember

2022-12-31

0001883835

ESGH:FunanAgriculturalRecliningInvestmentCo.LtdMember

2022-01-05

0001883835

ESGH:FunanAgriculturalRecliningInvestmentCo.LtdMember

2022-01-01

2022-01-05

0001883835

ESGH:MachineryEquipmentAndVehicleFleetMember

2024-06-30

0001883835

ESGH:MachineryEquipmentAndVehicleFleetMember

2023-12-31

0001883835

us-gaap:ConstructionInProgressMember

2024-06-30

0001883835

us-gaap:ConstructionInProgressMember

2023-12-31

0001883835

us-gaap:BuildingAndBuildingImprovementsMember

2022-12-31

0001883835

ESGH:MachineryEquipmentAndVehicleFleetMember

2022-12-31

0001883835

us-gaap:ConstructionInProgressMember

2022-12-31

0001883835

ESGH:LandUseRightMember

2024-06-30

0001883835

ESGH:LandUseRightMember

2023-12-31

0001883835

ESGH:LandUseRightMember

2022-12-31

0001883835

us-gaap:ComputerSoftwareIntangibleAssetMember

2022-12-31

0001883835

us-gaap:PatentsMember

2022-12-31

0001883835

ESGH:AgriculturalBankOfChinaFunanBranchMember

2024-06-30

0001883835

ESGH:AgriculturalBankOfChinaFunanBranchMember

2024-01-01

2024-06-30

0001883835

ESGH:AgriculturalBankOfChinaFunanBranchMember

2023-12-31

0001883835

ESGH:AgriculturalBankOfChinaFunanBranchMember

2023-01-01

2023-12-31

0001883835

ESGH:AnhuiFunanRuralCommercialBankMember

2024-06-30

0001883835

ESGH:AnhuiFunanRuralCommercialBankMember

2024-01-01

2024-06-30

0001883835

ESGH:AnhuiFunanRuralCommercialBankMember

2023-12-31

0001883835

ESGH:AnhuiFunanRuralCommercialBankMember

2023-01-01

2023-12-31

0001883835

ESGH:AnhuiFunanRuralCommercialBankOneMember

2024-06-30

0001883835

ESGH:AnhuiFunanRuralCommercialBankOneMember

2024-01-01

2024-06-30

0001883835

ESGH:AnhuiFunanRuralCommercialBankOneMember

2023-12-31

0001883835

ESGH:AnhuiFunanRuralCommercialBankOneMember

2023-01-01

2023-12-31

0001883835

ESGH:AnhuiFunanRuralCommercialBankTwoMember

2024-06-30

0001883835

ESGH:AnhuiFunanRuralCommercialBankTwoMember

2024-01-01

2024-06-30

0001883835

ESGH:AnhuiFunanRuralCommercialBankTwoMember

2023-12-31

0001883835

ESGH:AnhuiFunanRuralCommercialBankTwoMember

2023-01-01

2023-12-31

0001883835

ESGH:IndustrialAndCommercialBankOfChinaFunanMember

2024-06-30

0001883835

ESGH:IndustrialAndCommercialBankOfChinaFunanMember

2024-01-01

2024-06-30

0001883835

ESGH:IndustrialAndCommercialBankOfChinaFunanMember

2023-01-01

2023-12-31

0001883835

ESGH:IndustrialAndCommercialBankOfChinaFunanOneMember

2024-06-30

0001883835

ESGH:IndustrialAndCommercialBankOfChinaFunanOneMember

2024-01-01

2024-06-30

0001883835

ESGH:BankOfChinaFunanBranchMember

2024-06-30

0001883835

ESGH:BankOfChinaFunanBranchMember

2024-01-01

2024-06-30

0001883835

ESGH:BankOfChinaFunanBranchMember

2023-12-31

0001883835

ESGH:BankOfChinaFunanBranchMember

2023-01-01

2023-12-31

0001883835

ESGH:AgriculturalBankOfChinaFunanBranchMember

2022-12-31

0001883835

ESGH:AgriculturalBankOfChinaFunanBranchMember

2022-01-01

2022-12-31

0001883835

ESGH:AnhuiFunanRuralCommercialBankMember

2022-12-31

0001883835

ESGH:AnhuiFunanRuralCommercialBankMember

2022-01-01

2022-12-31

0001883835

ESGH:AnhuiFunanRuralCommercialBankOneMember

2022-12-31

0001883835

ESGH:AnhuiFunanRuralCommercialBankOneMember

2022-01-01

2022-12-31

0001883835

ESGH:AnhuiFunanRuralCommercialBankTwoMember

2022-12-31

0001883835

ESGH:AnhuiFunanRuralCommercialBankTwoMember

2022-01-01

2022-12-31

0001883835

ESGH:FunanYinghuaiRuralCommercialBankMember

2023-12-31

0001883835

ESGH:FunanYinghuaiRuralCommercialBankMember

2022-12-31

0001883835

ESGH:FunanYinghuaiRuralCommercialBankMember

2022-01-01

2022-12-31

0001883835

ESGH:IndustrialAndCommercialBankOfChinaFunanMember

2023-12-31

0001883835

ESGH:IndustrialAndCommercialBankOfChinaFunanMember

2022-12-31

0001883835

ESGH:BankOfChinaFunanBranchMember

2022-12-31

0001883835

ESGH:BankOfChinaFunanBranchMember

2022-01-01

2022-12-31

0001883835

ESGH:FunanAgriculturalInvestmentCo.LtdMember

2024-06-30

0001883835

ESGH:FunanAgriculturalInvestmentCo.LtdMember

2023-12-31

0001883835

ESGH:FunanSmallBusinessFinancingServiceCenterMember

2024-06-30

0001883835

ESGH:FunanSmallBusinessFinancingServiceCenterMember

2023-12-31

0001883835

ESGH:FunanZhihuaMushroomCoLtdMember

2021-01-01

2021-12-31

0001883835

ESGH:AUFPMember

2022-01-05

0001883835

ESGH:ZhihuaMember

2021-09-03

0001883835

ESGH:ZhihuaMember

2021-09-01

2021-09-03

0001883835

ESGH:AUFPMember

2022-11-01

2022-11-10

0001883835

ESGH:AUFPMember

2022-12-01

2022-12-02

0001883835

ESGH:GovernmentGrantsMember

2024-01-01

2024-06-30

0001883835

ESGH:GovernmentGrantsMember

2023-01-01

2023-06-30

0001883835

ESGH:AssetBasedGrantsMember

2024-01-01

2024-06-30

0001883835

ESGH:AssetBasedGrantsMember

2023-01-01

2023-06-30

0001883835

ESGH:IncomeBasedGrantsMember

2024-01-01

2024-06-30

0001883835

ESGH:IncomeBasedGrantsMember

2023-01-01

2023-06-30

0001883835

ESGH:GovernmentGrantsMember

2023-01-01

2023-12-31

0001883835

ESGH:GovernmentGrantsMember

2022-01-01

2022-12-31

0001883835

ESGH:AssetBasedGrantsMember

2023-01-01

2023-12-31

0001883835

ESGH:IncomeBasedGrantsMember

2023-01-01

2023-12-31

0001883835

ESGH:AssetBasedGrantsMember

2022-01-01

2022-12-31

0001883835

ESGH:IncomeBasedGrantsMember

2022-01-01

2022-12-31

0001883835

country:US

2023-12-31

0001883835

country:US

2022-12-31

0001883835

country:CN

2023-12-31

0001883835

country:CN

2022-12-31

0001883835

ESGH:MrZhiYangMember

2022-10-22

0001883835

ESGH:MrZhiYangMember

2022-10-01

2022-10-22

0001883835

ESGH:HanliangShaoMember

2021-08-01

2021-08-06

0001883835

2024-07-01

2024-07-31

0001883835

ESGH:MrZhiYangMember

2022-12-01

2022-12-31

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

xbrli:pure

iso4217:CNY

ESGH:Integer

As filed with the Securities and Exchange Commission

on October 7, 2024

File No. 333-281681

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1/A

Amendment No. 2

REGISTRATION STATEMENT UNDER THE SECURITIES ACT

OF 1933

ESG INC.

| Nevada |

|

2836 |

|

87-1918342 |

|

(State or jurisdiction of

Incorporation or organization) |

|

(Primary Standard Industrial

Classification Code) |

|

(I.R.S. Employer

Identification No.) |

523 School House Road

Kennett Square, PA 19348

267-467-5871

(Address, including zip code, and telephone number,

including area code, of registrant’s principle executive offices)

Registered Agents, Inc.

401 Ryland Street, Suite 200A

Reno, NV, 89502

(Name, address, including zip code, and telephone

number, including area code, of agent for service)

Approximate date of commencement of proposed sale

to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this

Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box:

☐

If this Form is filed to register additional securities

for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration

statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed

pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of

the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed

pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of

the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant

is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company.

See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company”

and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer |

☐ |

Accelerated filer |

☐ |

| Non-accelerated filer |

☒ |

Smaller reporting company |

☒ |

| |

|

Emerging growth company |

☒ |

If an emerging growth company, indicate by check

mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting

standards provided pursuant to Section 7(a)(2)(B) of the Securities Act.

PRELIMINARY PROSPECTUS

ESG INC.

5,000,000 Shares of Common Stock Offered by

the Company

$5.00 per share

This is a public offering of our common stock,

par value $0.001 per share. We are selling 5,000,000 shares of common stock in ESG Inc. (“ESG”), a Nevada corporation. ESG

Inc.’s common stock is quoted on the OTC Markets Pink Market Tier under the ticker symbol “ESGH.”

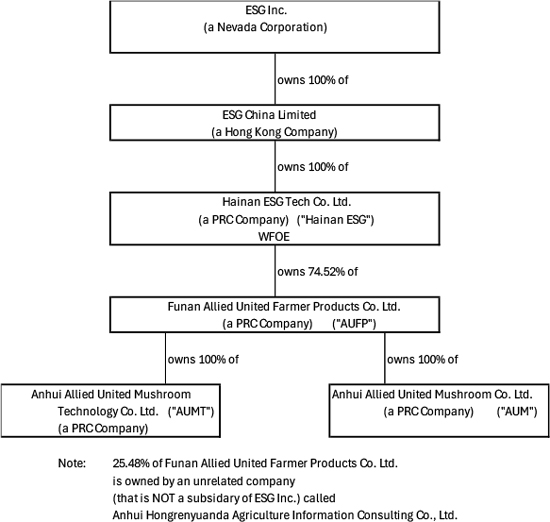

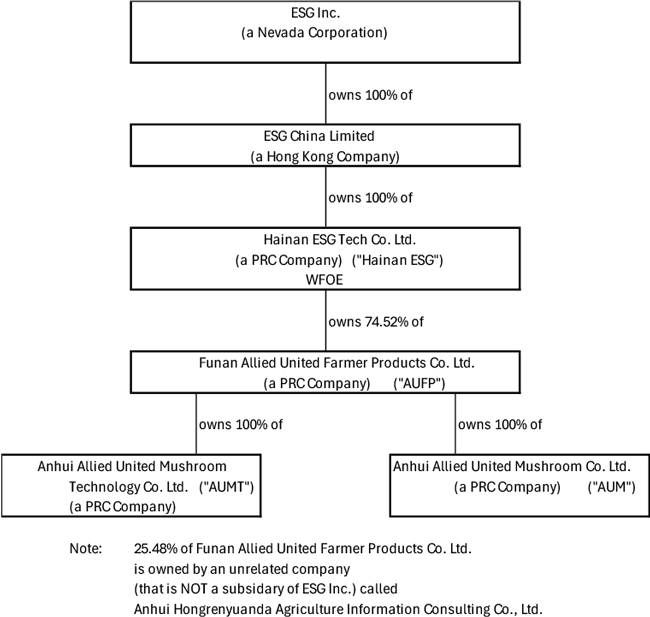

ESG Inc. is a domestic US corporation, formed

in Nevada, and it functions as a US holding company that operates its businesses through Chinese operating subsidiaries that are located

in the PRC. The Company’s Chinese operating subsidiaries are Funan Allied United Farmer Products Co., Ltd. (“AUFP”),

which owns Anhui Allied United Mushroom Technology Co., Ltd. (“AUMT”) and Anhui Allied United Mushroom Co., Ltd. (“AUM”).

No shares of stock in our Chinese operating

subsidiaries are offered for sale.

This offering will terminate on the date which

is 270 days from the effective date of this prospectus.

We currently expect the public offering price

of the shares we are offering to be $5.00 per share of our common stock.

The offering price of the shares has been determined

arbitrarily by us. The price does not bear any relationship to our assets, book value, earnings, or other established criteria for valuing

a company. In determining the number of shares to be offered and the offering price, we took into consideration our capital structure

and the amount of money we would need to implement our business plans. Accordingly, the offering price should not be considered an indication

of the actual value of our securities.

Investing in our common stock involves a high

degree of risk. See “Risk Factors” on Pages 13 through 35 for certain risks you should consider before purchasing any shares

in this offering. This prospectus is not an offer to sell these securities and it is not the solicitation of an offer to buy these

securities in any state where the offer or sale is not permitted.

Risks Associated with Doing Business in

China

Although ESG Inc. is a Nevada corporation,

and none of our officers and directors reside in China, the majority of our operations are conducted through subsidiaries that are based

in China. This corporate structure exposes the Company and its investors to certain legal and operational risks associated with being

based in or having the majority of the Company’s operations in China.

There are significant regulatory, liquidity,

and enforcement risks arising from our corporate structure and having the majority of the Company’s operations in China. For example,

there are significant risks arising from the legal system in China, including risks and uncertainties regarding the enforcement of laws

and that rules and regulations in China can change quickly with little advance notice. There is also the risk that the Chinese government

may intervene or influence our operations at any time, or may exert more control over offerings conducted overseas and/or foreign investment

in China-based issuers, which could result in a material change in our operations and/or the value of the securities we are registering

for sale.

Any actions by the Chinese government to

exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers could significantly

limit or completely hinder our ability to offer or continue to offer securities to investors and could cause the value of such securities

to significantly decline or become worthless.

See “Risks Related to Doing Business

in China” on Pages 16-23 under the “Risk Factors” section for specific risks associated with doing business in China.

There is no underwriter for this offering.

The offering is being conducted on a self-underwritten, best efforts basis, which means our management will attempt to sell the shares

being offered hereby on behalf of the Company. This offering will terminate on the date which is 270 days from the effective date

of this prospectus.

Completion of this offering is not subject to

us raising a minimum offering amount. We do not have an arrangement to place the proceeds from this offering in an escrow, trust or similar

account. Any funds raised from the offering will be immediately available to us for our immediate use.

Any purchaser of common stock in the offering

may be the only purchaser, given the lack of a minimum offering amount.

We are an “emerging growth company”

as defined in the Jumpstart Our Business Startups Act.

Neither the Securities and Exchange Commission

nor any state securities commission has approved or disapproved these securities, or determined if this prospectus is truthful or complete.

Any representation to the contrary is a criminal offense.

As disclosed on Page 24 herein, our Common

Stock is not traded on any exchange, either in the United States or on any foreign exchange Instead, our Common Stock trades on the over-the-counter

market (“OTC”), which may deprive stockholders of the full value of their shares. Our Common Stock is quoted on OTC Pink

Market Tier of OTCMarkets.com, under the ticker symbol “ESGH”. Therefore, our Common Stock is expected to have fewer market

makers, lower trading volumes, and larger spreads between bid and asked prices than securities listed on an exchange such as the New

York Stock Exchange or the NASDAQ Stock Market. These factors may result in higher price volatility and less market liquidity for our

Common Stock.

As disclosed on Page 9 and Page 26 herein,

our CEO and Director, Mr. Zhi Yang, beneficially owns and controls 83.53% of the Company’s Common Stock. Therefore, the interests

of our officers and directors may conflict with our outside stockholders, who may be unable to influence management and exercise control

over our business.

On May 8, 2024, Mr. Zhi Yang, the Company's founder

and CEO transferred 14,000,000 shares of our common stock held in his name to DCG China Limited, ("DCG") a company

owned by his mother, Xiayun Zhou. As a director in DCG, Mr. Yang has voting control over DCG and is considered the beneficial owner of

DCG, and therefore no change in control occurred. Prior to the transfer, DCG owned 7,632,800 shares of common stock, and now owns a total

of 21,632,800, representing 83.53% of the issued and outstanding shares of common stock. As a result, Mr. Yang may be able to elect or

defeat the election of our directors, amend or prevent amendment to our certificates of incorporation or bylaws, effect or prevent a

merger, sale of assets or other corporate transaction, and control the outcome of any other matter submitted to the shareholders for

vote. Accordingly, our outside stockholders may be unable to influence management and exercise control over our business.

Holding Foreign Companies Accountable Act ("HFCAA")

As disclosed on Pages 12 and 23 herein, on

December 18, 2020, the Holding Foreign Companies Accountable Act ("HFCAA") became law. Among other things, the statute

requires the SEC to identify public companies that have retained a registered public accounting firm to issue an audit report where the

firm has a branch or office that: (1) is located in a foreign jurisdiction, and (2) the Public Company Accounting Oversight Board (“PCAOB”)

has determined that it is unable to inspect or investigate completely because of a position taken by an authority in the foreign jurisdiction.

Under the HFCAA, the PCAOB has the responsibility

for determining that it is unable to inspect or investigate completely a registered public accounting firm or a branch or office of such

a firm because of a position taken by an authority in a foreign jurisdiction.

The SEC may suspend trading of securities in

companies if the PCAOB is unable to inspect an auditor’s records for those foreign companies. However, our Auditor, QI CPA, LLC,

an independent registered public accounting firm headquartered in the United States, is not included in the determinations made by the

PCAOB on December 16, 2021 in the Accelerating Holding Foreign Companies Accountable Act.

Our auditor is subject to PCAOB inspections

and has been inspected by the PCAOB on a regular basis. Therefore, although we operate in China, the Accelerating Holding Foreign Companies

Accountable Act and related regulations do not apply to our auditor, and trading in our securities will not be affected. If we subsequently

change auditors, we will choose another auditor headquartered in the United States.

How Cash Is Transferred Between ESG Inc. and

Its Subsidiaries

As further detailed on Page 7 herein, the

Company will settle amounts owed under the WFOE structure by transferring dividends, or distributions between the holding company and

its subsidiaries, or to investors, which have not yet occurred. We intend to rely primarily on dividends paid by the WFOE for our cash

needs, including the funds necessary to pay dividends and other cash distributions, if any, to our shareholders, to service any debt

we may incur and to pay our operating expenses. The Company has made no such distributions to date nor has it received any distributions

from the WFOE to date, and the Company has no current cash management policies in place. The Company will look to implement one in the

near future.

ESG entered into a Consulting Agreement with AUFP

on December 30, 2023 to provide mushroom spawn purchasing related services in the United States to AUFP, for a monthly fee of $20,000.

AUFP paid ESG Inc. $60,000 on January 18, 2024 for the first quarter, $60,000 on May 10, 2024 for the second quarter and $60,000 on September

2, 2024 for the third quarter, for a total of $180,000. The Consulting Agreement is attached as an exhibit. All these related party transactions

have been eliminated in the preparation of quarterly consolidated financial statements. Transferring cash between subsidiaries in China

occurred when AUMT sold Phase III button mushroom compost to AUM at the market price in 2022 and 2023 and at cost in 2024. The revenue

earned by AUMT when selling to AUM at market price totaled $3,604,169, in 2023, and,$3,814,879 in 2022. Separately, revenue earned by

AUMT when selling to AUM at cost was $1,519,838 for the six months ended June 30 2024. All the transactions have been eliminated in the

preparation of consolidated financial statements.

The Company has no plans to distribute earnings

or dividends and no distributions have been made to date between ESG Inc. and its subsidiaries, or investors.

The Company does not plan to use this offering

prospectus before the effective date.

Proceeds to Company in Offering

| | |

Number of Shares | | |

Offering Price (1) | | |

Underwriting Discounts & Commissions | | |

Gross Proceeds | |

| Per Share | |

| | | |

| | | |

| | | |

| | |

| 25% of Offering Sold | |

| 1,250,000 | | |

$ | 5.00 | | |

$ | 0 | | |

$ | 6,250,000 | |

| 50% of Offering sold | |

| 2,500,000 | | |

$ | 5.00 | | |

$ | 0 | | |

$ | 12,500,000 | |

| 75% of Offering Sold | |

| 3,750,000 | | |

$ | 5.00 | | |

$ | 0 | | |

$ | 18,750,000 | |

| Maximum Offering sold | |

| 5,000,000 | | |

$ | 5.00 | | |

$ | 0 | | |

$ | 25,000,000 | |

| (1) | Assuming

a public offering price of $5.00 per share, as set forth on the cover page of this prospectus. |

TABLE OF CONTENTS

ABOUT THIS PROSPECTUS

In making your investment

decision, you should only rely on the information contained in this prospectus. We have not authorized anyone to provide you with any

other or different information. If anyone provides you with information that is different from, or inconsistent with, the information

in this prospectus, you should not rely on it. We believe the information in this prospectus is materially complete and correct as of

the date on the front cover. We cannot, however, guarantee that the information will remain correct after that date. For that reason,

you should assume that the information in this prospectus is accurate only as of the date on the front cover and that it may not still

be accurate on a later date. This document may only be used where it is legal to sell these securities. The information contained in this

prospectus is current only as of its date, regardless of the time of delivery of this prospectus or of any sales of our shares of common

stock.

You should not interpret

the contents of this prospectus to be legal, business, investment or tax advice. You should consult with your own advisors for that type

of advice and consult with them about the legal, tax, business, financial and other issues that you should consider before investing in

our common stock.

This prospectus does not

offer to sell, or ask for offers to buy, any shares of our common stock in any state or other jurisdiction in which such offer or solicitation

would be unlawful or where the person making the offer is not qualified to do so.

No action is being taken

in any jurisdictions outside the United States to permit a public offering of our common stock or possession or distribution of this prospectus

in those jurisdictions. Persons who come into possession of this prospectus in jurisdictions outside the United States are required to

inform themselves about, and to observe, any restrictions that apply in those jurisdictions to this offering or the distribution of this

prospectus. In this prospectus, unless the context otherwise denotes, references to “we,” “us,” “our,”

“ESG” and the “Company” refer to ESG INC.

SUMMARY

The following

summary highlights material information in this prospectus. It may not contain all the information that is important to you. For additional

information, you should read this entire prospectus carefully, including “Risk Factors” the consolidated financial statements

and the notes to the consolidated financial statements.

Risks Associated with Doing Business in

China

Although ESG Inc. is a Nevada corporation,

and none of our officers and directors reside in China, the majority of our operations are conducted through subsidiaries that are based

in China. This corporate structure exposes the Company and its investors to certain legal and operational risks associated with being

based in or having the majority of the Company’s operations in China.

There are significant regulatory, liquidity,

and enforcement risks arising from our corporate structure and having the majority of the Company’s operations in China. For example,

there are significant risks arising from the legal system in China, including risks and uncertainties regarding the enforcement of laws

and that rules and regulations in China can change quickly with little advance notice. There is also the risk that the Chinese government

may intervene or influence our operations at any time, or may exert more control over offerings conducted overseas and/or foreign investment

in China-based issuers, which could result in a material change in our operations and/or the value of the securities we are registering

for sale.

Any actions by the Chinese government to

exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers could significantly

limit or completely hinder our ability to offer or continue to offer securities to investors and could cause the value of such securities

to significantly decline or become worthless.

See “Risks Related to Doing Business

in China” on Pages 16-23 under the “Risk Factors” section for specific risks associated with doing business in China.

Organizational History

ESG Inc. was incorporated

in July 2021 as a Nevada holding corporation and is headquartered at Kennett Square, PA and develops and operates sustainable plant-based

ingredients and food production and distribution with the substantial experience of its management team, including experience and relationships

in the industry of mushroom, agriculture and food in the world and the capital markets in the States.

Company Overview

We were incorporated under the name Plasma Innovative

Inc. (“Plasma”) on July 22, 2021 an emerging cold plasma application company. We intended to use our proprietary, cold

plasma technology to treat crops and plant seeds for agriculture. However, we have decided that it is in the best interest of our shareholders

to cease operations in the plasma application in the agriculture sector.

On November 6, 2023, Plasma Innovative Inc. entered

into a share exchange agreement (the “Share Exchange Agreement”) with ESG Inc. (“ESGI”), a Nevada corporation,

and the shareholders of ESGI (the “ESGI Shareholders”), whereby One Hundred Percent (100%) of the ownership interest of ESGI

was exchanged for 10,432,800 shares of common stock of Plasma issued to the ESGI Shareholders. The transaction has been accounted

for as a recapitalization of the Company, whereby ESGI is the accounting acquirer.

Immediately after completion of such share exchange, the Company has

65,000,000 authorized shares of common stock and a total of 25,899,468 issued and outstanding shares of common stock.

On September 28, 2023, ESGI entered into a share

exchange agreement with Funan Allied United Farmer Products Co., Ltd., a China corporation (“AUFP”), the shareholders of AUFP,

(each a “Shareholder,” and collectively, the “Shareholders”), and Hainan ESG Technology Co., Ltd., a China corporation

(“Hainan ESG”). Pursuant to such agreement, the Shareholders exchanged their equity of AUFP to Hainan ESG for shares of common

stock of ESGI, and ESGI has agreed to offer the ESGI shares. Following this transaction, AUFP became a 74.52% subsidiary of ESGI through

Hainan ESG.

Neither the Company nor ESGI are Chinese operating

companies. They are Nevada holding companies that operate business through Funan Allied United Farmer Products Co., Ltd., which owns Anhui

Allied United Mushroom Technology Co., Ltd. and Anhui Allied United Mushroom Co., Ltd., all of whom are Chinese operating companies.

On November 22, 2023, Plasma Innovative Inc. filed

Articles of Merger with the State of Nevada to merge ESGI into Plasma Innovative Inc. Plasma was the surviving entity with the name changed

into ESG Inc..

Effective February 23, 2024 the Company’s

name was changed from Plasma Innovative Inc. to ESG Inc., and its trading symbol was changed from PMIN to ESGH upon the approval from

FINRA.

The Company exercises control over the operations

of its subsidiaries. On February 17, 2023, the China Securities Regulatory Commission, or CSRC, issued the Trial Administrative Measures

of Overseas Securities Offering and Listing by Domestic Companies, or the Trial Measures, which became effective on March 31, 2023. Pursuant

to the Trial Measures, domestic companies that seek to offer or list securities overseas, both directly and indirectly, should fulfill

the filing procedure and report relevant information to the CSRC. We have not sought CSRC approval. Instead, we have relied on the legal

opinion attached hereto as Exhibit 99.1.

Our subsidiaries are formed and operating in

the People’s Republic of China (together, the “Material PRC Company”) and have been duly established. Each subsidiary

is validly existing as a company under the laws of the People’s Republic of China (“PRC Laws”) and has received all

authorizations required by the People’s Republic of China (the “Governmental Authorizations”) for its establishment

to the extent such Governmental Authorizations are required under applicable PRC Laws, and its business license is in full force and

effect. The Material PRC Company has the capacity and authority to own assets, to conduct business, and to sue and be sued in its own

name under PRC Laws. The articles of association, business license and other constitutional documents (if any) of the Material PRC Company

complies with the requirements of applicable PRC Laws and is in full force and effect. The Material PRC Company has not taken any corporate

action, nor has any legal proceedings commenced against it, for its liquidation, winding up, dissolution, or bankruptcy, for the appointment

of a liquidation committee, team of receivers or similar officers in respect of its assets or for any adverse suspension, withdrawal,

revocation or cancellation of its business license.

All of the equity interests of the Material PRC

Company are owned by ESG, through ESG China Limited, a Hong Kong company, and Hainan ESG Technology Co., Ltd, a PRC company, and we believe

the Material PRC Company has obtained all necessary Governmental Authorizations. The equity interests of the Material PRC Company are

owned by ESG, through its subsidiaries, free and clear of any pledge or other encumbrance under PRC Laws, and there are no outstanding

rights, warrants or options to acquire, or instruments convertible into or exchangeable for, any equity interest in the Material PRC Company

under PRC Laws.

All of our operations are conducted by

our subsidiaries and through our wholly-foreign-owned entity (“WFOE”) based in China currently which involves unique

risks to investors.

The legal and operational risks associated with

being based in or having the majority of the Company’s operations in China could result in a material change in the value of the

securities we are registering for sale or could significantly limit or completely hinder our ability to offer or continue to offer securities

to investors and cause the value of such securities to significantly decline or be worthless. Please see the Risk Factor titled “We

are faced with risks and uncertainties as a foreign enterprise under PRC laws”.

ESG the Driving Force behind the Company

ESG’s core business philosophy is to develop

and operate sustainable and technology-driving food businesses consistent with the principles of Environmental, Sustainable and Governance

investing.

An explanation of the three domains of Environmental,

Sustainable and corporate Governance -- is critical to understanding ESG’s development of its own business.

Environmental and Sustainable criteria include

technology and equipment application, energy use, waste, pollution, natural resource conservation, and treatment of animals and natural

resources and help us avoid a company that might pose a greater financial risk due to their environmental or other practices. The United

Nations projects that the world’s population is to reach 8.5 billion by 2030, 9.7 billion by 2050 and exceed 11 billion in 2100.

Food production needs to meet the projected demands in the coming years. Thus, food production should be technology-driven, environmentally

friendly, sustainable and not have a negative impact on the ecosystem and natural resources. Thus the “E and S” in ESG is

the first keen focus in developing and operating our business.

Corporate Governance deals with a

company’s top-down leadership and how it governs itself in an ethical and transparent manner devoid of conflicts of interest

and focuses on executive pay, audits, internal controls, and shareholder rights. We see an ever-increasing consumer and investor

demand for sustainable food production and distribution. We believe that many consumers will expect that food is produced under

stringent scrutiny for food safety and that ethical policies underlie every part of the process. We believe they will be willing to

pay a premium for food sourced through such channels. In addition, we expect governments everywhere will promulgate and enforce

stricter food safety regulations, which should eliminate a large number of food producers who will be unable to comply with these

respective regulations. These market conditions will require food companies to embrace new means of production and technology. We

believe this will lead to consolidation in various segments of the food industry, in which only forward-thinking participants like

ESG will survive and prosper.

Our Operating Subsidiary Companies

ESG is a holding company engaged in sustainable

food production and distribution directly or indirectly through our subsidiaries and currently owns operating entities in China. Our

operating subsidiaries are involved in direct mushroom composting, growing, food production, distribution as well as import and export

of food. We believe that the growing global demand for sustainable high-quality food presents a unique opportunity for companies engaged

in this critical area that is being paid increasing attention by global investors.

Funan Allied United Farmer Product Co., Ltd. (“AUFP”)

was created in 2017 in China by US mushroom industry participants with the support of strategic investors to revolutionize China’s

mushroom industry and create enhanced standards for food safety, sustainability, greenness, and resulting high-quality food products to

serve Chinese consumers and regional Asian export markets. AUFP engages in the research and development, composting, cultivation, processing,

packaging, and distribution of high-quality white button mushrooms from Fuyang, China. As a bio-sustainable and resources-recyclable company,

with wheat straw and animal manure as the major raw materials, kinds of agricultural waste, AUFP is dedicated to building Fuyang into

the hub to supply high-quality mushroom, compost and organic fertilizer in Asia with the support of industrial experts and capital.

Currently, AUFP owns approximately 56 acres of

industrial land use rights and built bunkers, tunnels and growing facilities, totaling approximately 300,000 square feet, with fresh white

button mushrooms capacity of 7300 tons and production capacity to 90,000 tons of Phase IIII compost, of which two-thirds are planned to

be sold to third party’s farms.

As an AUFP’s subsidiary, Anhui Allied United

Mushroom Technology Co., Ltd. (“AUMT”) operates a Phase III compost manufacturing facility to distribute to its own and third-party

growing facilities in China and east and southeast Asia while Anhui Allied United Mushroom Co. Ltd. (“AUM”), an AUFP subsidiary,

is a company engaged in growing, packing and distributing fresh white button mushrooms in China.

AUFP received the highest quality certification

“Green Food” in China. Along with its subsidiaries, AUFP recorded a consolidated revenue of USD 7.45 million and USD 7.25

million for the years ended December 31, 2023 and 2022, respectively.

Anhui Allied United Mushroom Technology Co., Ltd.

Anhui Allied United Mushroom Technology Co., Ltd.

(“AUMT”) was created in China in March 2018, to manufacture white button mushroom compost.

White button mushroom compost is a unique living

organism. It varies according to the environment where it is produced. Making mushroom compost is a complex process that AUMT has been

perfecting. AUMT uses the art of the state phase III composting process to make compost under the supervision of a team of specialists,

taking raw materials from the local area, for our own farms and other mushrooms growers.

Phase III composting process

is composed of:

Phase I: Bales of straw are

mixed with animal manure, water and gypsum. When mixed, the material is filled into large aerated concrete vessels, called bunkers. During

this phase the compost reaches temperatures of 80 degrees Celsius. After 7–13 days the Phase I process is completed, ready for the

Phase II process to begin.

Phase II: The material is

removed from the bunkers and filled into closed tunnels, where we monitor and control a series of temperature changes – the most

important of which is pasteurization. Pasteurization helps remove any unwanted organisms from the compost. The next and most important

stage of Phase II is the conditioning of the compost. This means that microbes convert ammonia and amines into protein. Phase II takes

approximately 5–6 days. The climate controlled “tunnel” heats the compost to 58 degrees Celsius for pasteurization and

then conditions it at 48 degrees Celsius.

Phase III: Once the Phase

II process is completed, the compost is cooled and removed from the Phase 2 tunnels. Mushroom spawn is added and the compost is then refilled

into Phase III tunnels. Spawn is usually made with rye or millet grain that has been sterilized and inoculated with mushroom tissue (mycelium).

This Phase III incubation process takes 15-17 days. During this time mycelium grows throughout the substrate. After the 15-17 days

incubation period, the Phase III compost is loaded into specially designed trucks for transport to the growing facility.

Currently AUMT operates 9 bunkers, 31

tunnels and related auxiliary facilities and equipment with the capacity of 90,000 tons annually of Phase III compost to supply.

Anhui Allied United Mushroom Co., Ltd.

Anhui Allied United Mushroom Co., Ltd. (“AUM”)

was created in China in April 2018, to grow fresh white button mushroom and provide white button mushroom growing management services.

AUM produces high quality fresh white button mushrooms.

The growing process is composed of the following

steps:

As the mushroom compost is

filled into the growing rooms, a layer of peat is applied to the surface of the Phase III compost. The layer is called the casing layer

and is essential for the formation of the mushrooms. Over a 3-4 days period, the mushroom tissue grows throughout the compost and up through

the casing layer.

The environment is then altered

to simulate an autumn day, which promotes the formation of mushrooms. As a result, tiny mushroom heads (pins) begin to appear. During

the next two weeks the levels of moisture, temperature, humidity, carbon dioxide and air movement are carefully monitored.

The pins eventually grow into

mushrooms. The mushrooms are picked by hand to maintain the highest possible quality. All our mushrooms are cooled quickly after harvesting

and are packed and transported in refrigerated trucks to wholesale markets or supermarkets.

Currently, AUM owns approximately 335,000 square

feet of growing area, with annual production of fresh white button mushroom of approximately 20,000,000 LBS.

Market Overview

Health Diet Trend

We believe that people are searching for vegan

and plant-based options for every aspect of their lifestyle. Mushrooms are a nutritious vegetarian delicacy and contain many vitamins

and minerals but are low on sugar and fat. We believe that they are becoming a preferable and quality ingredient source for plant-based

food. As an innovative food company with the whole production chain of mushrooms, we are committed to innovating and providing sustainable

mushroom-based food and its ingredients.

Mushrooms are popular in most of the developed

countries and are becoming accepted in many developing countries. The market for mushrooms is growing rapidly because of their rich nutritional

value and special taste aroma, and flavor. The global plant-based food market is expected to reach 77.8 billion U.S. dollars in 2025.

The forecast projects that by 2030 the market will have more than doubled. (https://www.statista.com/statistics/1280394/global-plant-based-food-market-value/).

Quality Phase III Compost and Strong Demand

We believe that the key factor for the successful

growing of white button mushrooms is composting. Composting is a delicate and difficult business, especially in large-scale and commercial

indoor growing. ESG believes it is positioning itself as the compost provider in the Asian Pacific area with its management expertise

and experience in composting and advantages of being near a raw material supply.

Our Competitive Strengths

Experienced Management

ESG’s management is composed of professionals

in mushroom composting, growing, food processing and marketing, and the food industry, as well as in capital markets and public companies.

We have experienced experts in white button mushroom production and, especially, composting, on our management team. Experienced and senior

experts are the most important asset to ESG. ESG is designing and executing a comprehensive training system to continue to build up the

management team for our operations and the provisions of management service.

Focusing Key Stages of Food Production

ESG is focusing on the composting business and

food processing business, especially mushroom related, which is two ends of the most value added.

ESG is focusing on research and development in

connection with the improvement of mushroom composting production and of the production of mushroom based food and its ingredients. We

concentrate ESG’s capital and efforts on key stages.

Production Location in the raw material base

A location near the supply of excellent

raw materials such as wheat straw and animal manure are very important in order to control the cost of production and the quality of mushrooms.

ESG’s current and planned production facilities are located in excellent places of raw materials to be collected such as Funan in

China.

Intellectual Property

ESG has 1 invention Patent, 14 Utility Model Patents, registered and

17 Utility Model Patents with pending effectiveness.

Regulatory Matters

Regulatory Permission

As substantially all of our operations are currently

conducted by our PRC Subsidiaries in China, we are subject to the associated legal and operational risks, including risks related to the

legal, political and economic policies of the Chinese government, the relations between China and the United States, or Chinese or United

States regulations, which risks could result in a material change in our operations and/or cause the value of our ordinary shares to significantly

decline or become worthless, and affect our ability to offer or continue to offer securities to investors. Recently, the PRC government

initiated a series of regulatory actions and made a number of public statements on the regulation of business operations in China with

little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based

companies listed overseas, and adopting new measures to extend the scope of cybersecurity reviews.

On July 6, 2021, the relevant PRC government authorities

made public the Opinions on Strictly Cracking Down Illegal Securities Activities, which provided that the administration and supervision

of overseas-listed China-based companies will be strengthened, and the special provisions of the State Council on overseas issuance and

listing of shares by such companies will be revised, clarifying the responsibilities of domestic industry competent authorities and regulatory

authorities. However, the Opinions on Strictly Cracking Down Illegal Securities Activities were only issued recently, leaving uncertainties

regarding the interpretation and implementation of these opinions. It is possible that any new rules or regulations may impose additional

requirements on us.

The Regulations on Mergers and Acquisitions of

Domestic Companies by Foreign Investors, or the M&A Rules, adopted by six PRC regulatory agencies in 2006 and amended in 2009, requires

an overseas special purpose vehicle formed for listing purposes through acquisitions of PRC domestic companies and controlled by PRC companies

or individuals to obtain the approval of the China Securities Regulatory Commission, or the CSRC, prior to the listing and trading of

such special purpose vehicle’s securities on an overseas stock exchange.

On December 28, 2021, the Cyberspace Administration

of China (the “CAC”) jointly with the relevant authorities formally published Measures for Cybersecurity Review (2021) which

took effect on February 15, 2022 and replace the former Measures for Cybersecurity Review (2020). Measures for Cybersecurity Review (2021)

stipulates that operators of critical information infrastructure purchasing network products and services, and online platform operator

(together with the operators of critical information infrastructure, the “Operators”) carrying out data processing activities

that affect or may affect national security, shall conduct a cybersecurity review, any online platform operator who controls more than

one million users’ personal information must go through a cybersecurity review by the cybersecurity review office if it seeks to

be listed in a foreign country.

According to the Notice by the General Office

of the State Council of Comprehensively Implementing the List-based Management of Administrative Licensing Items (No. 2 [2022] of the

General Office of the State Council) and its attachment, the List of Administrative Licensing Items Set by Laws, Administrative Regulations,

and Decisions of the State Council (2022 Edition), as of the date hereof, our PRC subsidiaries has received from PRC authorities all requisite

licenses, permissions or approvals needed to engage in the businesses currently conducted in China. As of the date hereof, neither we

nor our PRC Subsidiaries (i) are required to obtain permissions from any PRC authorities to operate or issue our ordinary shares to foreign

investors, (ii) are subject to permission requirements from the CSRC, the CAC or any other entity that is required to approve our PRC

subsidiaries’ operations, or (iii) have received or were denied such permissions by any PRC authorities.

The only permission required for operations is

the business license of the PRC subsidiaries. The business license in PRC is a permit issued by Market Supervision and Administration

that allows the company to conduct specific business within the government’s geographical jurisdiction. As of the date hereof, our

PRC subsidiaries have received from PRC authorities all requisite licenses, permissions or approvals needed to engage in the businesses

currently conducted in China, and no permission or approval has been denied. At present, we do not believe our operations require any

other approvals and or permissions of Chinese authorities.

If we have inadvertently concluded that additional

permissions or approvals are not required, or if applicable laws, regulations or interpretations change, and we are required to obtain

such permissions or approvals from the CSRC in the future and were denied permission from Chinese authorities to list or become quoted

on U.S. exchanges and/or quotation services, (or if we were granted permission and then failed to maintain permission) we will not be

able to continue to be quoted or listed on U.S. exchanges, which would materially affect the interests of the investors, including the

risk that investors could not never sell their Common Stock in the Company, which would render their investment worthless.

It is uncertain when and whether the Company will

be required to obtain permission from the PRC government to list or become quoted on U.S. exchanges in the future, and even if such permission

is obtained, whether it will be denied or rescinded. Although the Company is currently not required to obtain permission from any of

the PRC central or local government and has not received any denial to list or become quoted on the U.S. exchange, our operations could

be adversely affected, directly or indirectly, by existing or future laws and regulations relating to its business or industry; if we

inadvertently conclude that such approvals are not required when they are, or applicable laws, regulations, or interpretations change

and we are required to obtain approval in the future.

On December 24, 2021, the China Securities Regulatory

Commission, or the CSRC, issued Provisions of the State Council on the Administration of Overseas Securities Offering and Listing by Domestic

Companies (Draft for Comments) (the “Administration Provisions”), and the Administrative Measures for the Filing of Overseas

Securities Offering and Listing by Domestic Companies (the “Measures”), which were open for public comments by January 23,

2022. The Administration Provisions and Measures for overseas listings lay out specific requirements for filing documents and include

unified regulation management, strengthening regulatory coordination, and cross-border regulatory cooperation. Domestic companies seeking

to list abroad must carry out relevant security screening procedures if their businesses involve supervisions such as foreign investment

security and cyber security reviews. Companies endangering national security are among those off-limits for overseas listings. We believe

the Company is not affected by this based upon the legal opinion attached hereto as Exhibit 99.1.

On February 17, 2023, with the approval of the

State Council, the CSRC released the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies (the

“Trial Measures”) and five supporting guidelines, which came into effect on March 31, 2023. According to the Trial Measures,

among other requirements, (1) domestic companies that seek to offer or list securities overseas, both directly and indirectly, should

fulfill the filing procedures with the CSRC; if a domestic company fails to complete the filing procedures, such domestic company may

be subject to administrative penalties; and (2) where a domestic company seeks to indirectly offer and list securities in an overseas

market, the issuer shall designate a major domestic operating entity responsible for all filing procedures with the CSRC, and such filings

shall be submitted to the CSRC within three business days after the submission of the overseas offering and listing application. On the

same day, the CSRC also held a press conference for the release of the Trial Measures and issued the Notice on Administration for the

Filing of Overseas Offering and Listing by Domestic Companies, which clarifies that (1) on or prior to the effective date of the Trial

Measures, domestic companies that have already submitted valid applications for overseas offering and listing but have not obtained approval

from overseas regulatory authorities or stock exchanges may reasonably arrange the timing for submitting their filing applications with

the CSRC, and must complete the filing before the completion of their overseas offering and listing; (2) a six-month transition period

will be granted to domestic companies which, prior to the effective date of the Trial Measures, have already obtained the approval from

overseas regulatory authorities or stock exchanges, but have not completed the indirect overseas listing; if domestic companies fail to

complete the overseas listing within such six-month transition period, they shall file with the CSRC according to the requirements; and

(3) the CSRC will solicit opinions from relevant regulatory authorities and complete the filing of the overseas listing of companies with

contractual arrangements which duly meet the compliance requirements, and support the development and growth of these companies.

With respect to the domestic company, non-compliance

with the Trial Measures or an overseas listing completed in breach of it may result in a warning or a fine ranging from RMB 1 million

to RMB10 million. Furthermore, the directly responsible executives and other directly responsible personnel of the domestic company may

be warned or fined between RMB 500,000 and RMB 5 million and the controlling shareholder, actual controllers, and other legally appointed

persons of the domestic company may be warned, or fined between RMB 1 million and RMB 10 million. If, during the filing process, the domestic

company conceals important factors or the content is materially false, and securities are not issued, they are subject to a fine of RMB1

million to RMB10 million. With respect to the directly responsible executives and other directly responsible personnel of the domestic

company, they are subject to a warning and fine between RMB 500,000 and RMB 5 million, and with respect to the controlling shareholder,

actual controllers, and other legally appointed persons of the domestic company, they are subject to a warning and fine between RMB 1

million and RMB 10 million.

The Trial Measures have come into effect. After

March 31, 2023, any failure or perceived failure by the domestic company or PRC subsidiaries to comply with the above confidentiality

and archives administration requirements under the Trial Measures and other PRC laws and regulations may result in that the relevant entities

would be held legally liable by competent authorities and referred to the judicial organization to be investigated for criminal liability

if suspected of committing a crime.

According to a translated copy of the current

and effective regulations promulgated by the China Securities Regulatory Commission, that is, the “Trial Administrative Measures

of Overseas Securities Offering and Listing by Domestic Companies” Article 2 states, “Direct overseas offering and listing

by domestic companies refers to such overseas offering and listing by joint-stock company incorporated domestically. Indirect overseas

offering and listing by domestic companies refers to such overseas offering and listing by a company in the name of an overseas incorporated

entity, whereas the company’s major business operations are located domestically, and such offering and listing is based on the

underlying equity, assets, earnings or other similar rights of a domestic company”. Article 16 states, “Subsequent securities

offerings of an issuer in the same overseas market where it has previously offered and listed securities shall be filed with the CSRC

within 3 working days after the offering is completed.

According to a translated copy of the current

and effective regulations promulgated by the China Securities Regulatory Commission, that is, the “Regulations on Strengthening

the Confidentiality and Archives Management Work Related to the Overseas Issuance and Listing of Securities” Article 3 states, “A

domestic company that plans to, either directly or through its overseas listed entity, publicly disclose or provide to relevant entities

or individuals including securities companies, securities service providers, and overseas regulators, documents and materials that contain

state secrets or government work secrets, shall first obtain approval from competent authorities according to law, and file with the secrecy

administrative department at the same level. Where there is ambiguity or dispute over the identification of a state secret, a request

shall be submitted to the competent secrecy administrative department for determination; where there is ambiguity or dispute over the

identification of a government work secret, a request shall be submitted to the competent government authority for determination.”

Further, Article 4 states that, “A domestic company that plans to, either directly or through its overseas listed entity, publicly

disclose or provide to relevant entities or individuals including securities companies, securities service providers, and overseas regulators,

other documents and materials that, if divulged, will jeopardize national security or public interest, shall strictly fulfill relevant

procedures stipulated by applicable national regulations.” Accordingly, as the Company does not believe its operations fall into

the above legal provisions, the Company does not believe that it is required to seek authorizations from Chinese authorities.

On December 28, 2021, the Cyberspace Administration

of China (the “CAC”) jointly with the relevant authorities formally published Measures for Cybersecurity Review (2021) which

took effect on February 15, 2022 and replace the former Measures for Cybersecurity Review (2020). Measures for Cybersecurity Review (2021)

stipulates that operators of critical information infrastructure purchasing network products and services, and online platform operator

(together with the operators of critical information infrastructure, the “Operators”) carrying out data processing activities

that affect or may affect national security, shall conduct a cybersecurity review, any online platform operator who controls more than

one million users’ personal information must go through a cybersecurity review by the cybersecurity review office if it seeks to

be listed in a foreign country.

At present, we do not believe our operations require

the approval and or permission of Chinese authorities, based upon the legal opinion attached hereto as Exhibit 99.1. This is because the

Company’s primary business is food supply, which we were informed by counsel does not require the approval and permission of the

Chinese government. Please see related legal opinion attached hereto as Exhibit 99.1. The “Special Management Measures for Foreign

Investment Access (Negative List) (2021 Edition)” and “Market Access Negative List (2022 Edition)” issued by the Chinese

government do not include the industry and business the Company is involved in. The Company will settle amounts owed under the WFOE structure

by transferring dividends, or distributions between the holding company and its subsidiaries, or to investors, which have not yet occurred.

We intend to rely primarily on dividends paid by the WFOE for our cash needs, including the funds necessary to pay dividends and other

cash distributions, if any, to our shareholders, to service any debt we may incur and to pay our operating expenses. The Company has made

no such distributions to date nor has it received any distributions from the WFOE to date, and the Company has no current cash management

policies in place. The Company will look to implement one in the near future. The PRC government also imposes controls on the conversion

of RMB into foreign currencies and the remittance of currencies out of the PRC. Therefore, our WFOE may experience difficulties in completing

the administrative procedures necessary to pay distributions from its profits, if any. Furthermore, if our WFOE incurs debt on its own

in the future, the instruments governing the debt may restrict their ability to pay distributions or make other payments. If the Company

or our subsidiaries are unable to receive all of the revenues from our operations, we may be unable to pay dividends on our Shares.

Cash dividends, if any, on the Company’s

Shares will be paid in U.S. dollars. If the Company is considered a PRC tax resident enterprise for tax purposes, any dividends paid

to our overseas shareholders may be regarded as China-sourced income and as a result may be subject to PRC withholding tax at a rate

of up to 10.0%. The Company has no plans to distribute earnings or dividends and no distributions of earnings or dividends have made

to date between ESG Inc. and its subsidiaries or investors.

There are no legal, or governmental proceedings,

regulatory investigations or other governmental decisions, rulings, orders, or actions before any Governmental Agencies in progress or

pending in the PRC to which the Company or the Material PRC Company is a party or to which any assets of the Material PRC Company is a

subject.

All dividends declared and payable upon the equity

interests in the WFOE may be converted into foreign currency and freely transferred out of the PRC free of any deductions in the PRC,

provided that (i) the declaration and payment of such dividends complies with applicable PRC Laws and the constitutional documents of

the WFOE, and (ii) the remittance of such dividends out of the PRC complies with the procedures required by the relevant PRC Laws relating

to foreign exchange administration.

We face uncertainties with respect to indirect

transfers of equity interests in PRC resident enterprises by their non-PRC holding companies.

Adverse changes in economic and political policies

of the PRC government could have a material and adverse effect on overall economic growth in China, which could materially and adversely

affect our business. General macroeconomic conditions may materially and adversely affect our business, prospects, results of operations

and financial position. The PRC government’s control over foreign currency conversion may adversely affect our business and results

of operations and our ability to remit dividends.

There is no tax or duty payable by or on behalf

of the Material PRC Company under applicable PRC Laws in connection with the creation, allotment and issuance of Common Shares, provided

that each person taking the aforementioned actions is not subject to PRC tax by reason of citizenship, permanent establishment, residence

or otherwise subject to PRC tax imposed on or measured by net income or net profits.

There are no reporting obligations to any Governmental

Agency under PRC Laws on those holders of Common Shares who are not deemed to be PRC residents as defined under applicable PRC Laws, to

the extent that no reporting obligation is triggered by the purchase or holding of Common Shares under the PRC anti-monopoly laws, rules

and regulations.

We currently intend to retain all available funds

and future earnings, if any, for the operation and expansion of our business and do not anticipate declaring or paying any dividends in

the foreseeable future. Any future determination related to our dividend policy will be made at the discretion of our board of directors

after considering our financial condition, results of operations, capital requirements, contractual requirements, business prospects and

other factors the board of directors deem relevant, and subject to the restrictions contained in any future financing instruments.

All of our business operations are currently conducted

in China. Accordingly, our business, financial condition, results of operations and prospects are affected significantly by economic,

political and legal developments in China. Although the PRC economy has been transitioning from a planned economy to a more market-oriented

economy since the late 1970s, the PRC government continues to exercise significant control over China’s economic growth through

direct allocation of resources, monetary and tax policies, and a host of other government policies such as those that encourage or restrict