false

--12-31

2024

Q3

0001439264

0001439264

2024-01-01

2024-09-30

0001439264

2024-10-25

0001439264

2024-09-30

0001439264

2023-12-31

0001439264

us-gaap:PreferredStockMember

2024-09-30

0001439264

us-gaap:PreferredStockMember

2023-12-31

0001439264

us-gaap:SeriesAPreferredStockMember

2024-09-30

0001439264

us-gaap:SeriesAPreferredStockMember

2023-12-31

0001439264

us-gaap:SeriesBPreferredStockMember

2024-09-30

0001439264

us-gaap:SeriesBPreferredStockMember

2023-12-31

0001439264

us-gaap:SeriesCPreferredStockMember

2024-09-30

0001439264

us-gaap:SeriesCPreferredStockMember

2023-12-31

0001439264

2024-07-01

2024-09-30

0001439264

2023-07-01

2023-09-30

0001439264

2023-01-01

2023-09-30

0001439264

us-gaap:PreferredStockMember

2023-12-31

0001439264

us-gaap:CommonStockMember

2023-12-31

0001439264

us-gaap:AdditionalPaidInCapitalMember

2023-12-31

0001439264

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-12-31

0001439264

us-gaap:RetainedEarningsMember

2023-12-31

0001439264

us-gaap:PreferredStockMember

2024-03-31

0001439264

us-gaap:CommonStockMember

2024-03-31

0001439264

us-gaap:AdditionalPaidInCapitalMember

2024-03-31

0001439264

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2024-03-31

0001439264

us-gaap:RetainedEarningsMember

2024-03-31

0001439264

2024-03-31

0001439264

us-gaap:PreferredStockMember

2024-06-30

0001439264

us-gaap:CommonStockMember

2024-06-30

0001439264

us-gaap:AdditionalPaidInCapitalMember

2024-06-30

0001439264

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2024-06-30

0001439264

us-gaap:RetainedEarningsMember

2024-06-30

0001439264

2024-06-30

0001439264

us-gaap:PreferredStockMember

2022-12-31

0001439264

us-gaap:CommonStockMember

2022-12-31

0001439264

us-gaap:AdditionalPaidInCapitalMember

2022-12-31

0001439264

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-12-31

0001439264

us-gaap:RetainedEarningsMember

2022-12-31

0001439264

2022-12-31

0001439264

us-gaap:PreferredStockMember

2023-03-31

0001439264

us-gaap:CommonStockMember

2023-03-31

0001439264

us-gaap:AdditionalPaidInCapitalMember

2023-03-31

0001439264

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-03-31

0001439264

us-gaap:RetainedEarningsMember

2023-03-31

0001439264

2023-03-31

0001439264

us-gaap:PreferredStockMember

2023-06-30

0001439264

us-gaap:CommonStockMember

2023-06-30

0001439264

us-gaap:AdditionalPaidInCapitalMember

2023-06-30

0001439264

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-06-30

0001439264

us-gaap:RetainedEarningsMember

2023-06-30

0001439264

2023-06-30

0001439264

us-gaap:PreferredStockMember

2024-01-01

2024-03-31

0001439264

us-gaap:CommonStockMember

2024-01-01

2024-03-31

0001439264

us-gaap:AdditionalPaidInCapitalMember

2024-01-01

2024-03-31

0001439264

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2024-01-01

2024-03-31

0001439264

us-gaap:RetainedEarningsMember

2024-01-01

2024-03-31

0001439264

2024-01-01

2024-03-31

0001439264

us-gaap:PreferredStockMember

2024-04-01

2024-06-30

0001439264

us-gaap:CommonStockMember

2024-04-01

2024-06-30

0001439264

us-gaap:AdditionalPaidInCapitalMember

2024-04-01

2024-06-30

0001439264

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2024-04-01

2024-06-30

0001439264

us-gaap:RetainedEarningsMember

2024-04-01

2024-06-30

0001439264

2024-04-01

2024-06-30

0001439264

us-gaap:PreferredStockMember

2024-07-01

2024-09-30

0001439264

us-gaap:CommonStockMember

2024-07-01

2024-09-30

0001439264

us-gaap:AdditionalPaidInCapitalMember

2024-07-01

2024-09-30

0001439264

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2024-07-01

2024-09-30

0001439264

us-gaap:RetainedEarningsMember

2024-07-01

2024-09-30

0001439264

us-gaap:PreferredStockMember

2023-01-01

2023-03-31

0001439264

us-gaap:CommonStockMember

2023-01-01

2023-03-31

0001439264

us-gaap:AdditionalPaidInCapitalMember

2023-01-01

2023-03-31

0001439264

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-01-01

2023-03-31

0001439264

us-gaap:RetainedEarningsMember

2023-01-01

2023-03-31

0001439264

2023-01-01

2023-03-31

0001439264

us-gaap:PreferredStockMember

2023-04-01

2023-06-30

0001439264

us-gaap:CommonStockMember

2023-04-01

2023-06-30

0001439264

us-gaap:AdditionalPaidInCapitalMember

2023-04-01

2023-06-30

0001439264

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-04-01

2023-06-30

0001439264

us-gaap:RetainedEarningsMember

2023-04-01

2023-06-30

0001439264

2023-04-01

2023-06-30

0001439264

us-gaap:PreferredStockMember

2023-07-01

2023-09-30

0001439264

us-gaap:CommonStockMember

2023-07-01

2023-09-30

0001439264

us-gaap:AdditionalPaidInCapitalMember

2023-07-01

2023-09-30

0001439264

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-07-01

2023-09-30

0001439264

us-gaap:RetainedEarningsMember

2023-07-01

2023-09-30

0001439264

us-gaap:PreferredStockMember

2024-09-30

0001439264

us-gaap:CommonStockMember

2024-09-30

0001439264

us-gaap:AdditionalPaidInCapitalMember

2024-09-30

0001439264

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2024-09-30

0001439264

us-gaap:RetainedEarningsMember

2024-09-30

0001439264

us-gaap:PreferredStockMember

2023-09-30

0001439264

us-gaap:CommonStockMember

2023-09-30

0001439264

us-gaap:AdditionalPaidInCapitalMember

2023-09-30

0001439264

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-09-30

0001439264

us-gaap:RetainedEarningsMember

2023-09-30

0001439264

2023-09-30

0001439264

MVNC:ShareExchangeAgreementMember

MVNC:UWMCMember

2024-08-14

2024-08-15

0001439264

MVNC:ShareExchangeAgreementMember

MVNC:UWMCMember

2024-08-15

0001439264

MVNC:UnitedWarehouseManagementCorpMember

2024-01-01

2024-09-30

0001439264

MVNC:UnitedWarehouseManagementCorpMember

2024-09-30

0001439264

MVNC:KSKLogisticsLimitedMember

2024-01-01

2024-09-30

0001439264

MVNC:KSKLogisticsLimitedMember

2024-09-30

0001439264

MVNC:ProposeEnterpriseLimitedMember

2024-01-01

2024-09-30

0001439264

MVNC:ProposeEnterpriseLimitedMember

2024-09-30

0001439264

MVNC:UnitedWarehouseManagementLimitedMember

2024-01-01

2024-09-30

0001439264

MVNC:UnitedWarehouseManagementLimitedMember

2024-09-30

0001439264

MVNC:WarehouseFacilitiesMember

2024-01-01

2024-09-30

0001439264

us-gaap:EquipmentMember

2024-01-01

2024-09-30

0001439264

MVNC:MotorVehicleMember

2024-01-01

2024-09-30

0001439264

MVNC:PeriodEndMember

country:HK

2024-09-30

0001439264

MVNC:PeriodEndMember

country:HK

2023-09-30

0001439264

MVNC:PeriodAverageMember

country:HK

2024-09-30

0001439264

MVNC:PeriodAverageMember

country:HK

2023-09-30

0001439264

MVNC:FinancialConsultingIncomeMember

us-gaap:TransferredAtPointInTimeMember

2024-07-01

2024-09-30

0001439264

MVNC:FinancialConsultingIncomeMember

us-gaap:TransferredAtPointInTimeMember

2023-07-01

2023-09-30

0001439264

MVNC:FinancialConsultingIncomeMember

us-gaap:TransferredAtPointInTimeMember

2024-01-01

2024-09-30

0001439264

MVNC:FinancialConsultingIncomeMember

us-gaap:TransferredAtPointInTimeMember

2023-01-01

2023-09-30

0001439264

MVNC:LogisticServiceIncomeMember

us-gaap:TransferredAtPointInTimeMember

2024-07-01

2024-09-30

0001439264

MVNC:LogisticServiceIncomeMember

us-gaap:TransferredAtPointInTimeMember

2023-07-01

2023-09-30

0001439264

MVNC:LogisticServiceIncomeMember

us-gaap:TransferredAtPointInTimeMember

2024-01-01

2024-09-30

0001439264

MVNC:LogisticServiceIncomeMember

us-gaap:TransferredAtPointInTimeMember

2023-01-01

2023-09-30

0001439264

MVNC:WarehousingServiceIncomeMember

us-gaap:TransferredOverTimeMember

2024-07-01

2024-09-30

0001439264

MVNC:WarehousingServiceIncomeMember

us-gaap:TransferredOverTimeMember

2023-07-01

2023-09-30

0001439264

MVNC:WarehousingServiceIncomeMember

us-gaap:TransferredOverTimeMember

2024-01-01

2024-09-30

0001439264

MVNC:WarehousingServiceIncomeMember

us-gaap:TransferredOverTimeMember

2023-01-01

2023-09-30

0001439264

MVNC:WarehouseFacilitiesMember

2024-09-30

0001439264

srt:MinimumMember

2024-09-30

0001439264

srt:MaximumMember

2024-09-30

0001439264

us-gaap:DomesticCountryMember

2024-01-01

2024-09-30

0001439264

us-gaap:DomesticCountryMember

2023-01-01

2023-09-30

0001439264

us-gaap:ForeignCountryMember

country:VG

2024-01-01

2024-09-30

0001439264

us-gaap:ForeignCountryMember

country:VG

2023-01-01

2023-09-30

0001439264

us-gaap:ForeignCountryMember

country:HK

2024-01-01

2024-09-30

0001439264

us-gaap:ForeignCountryMember

country:HK

2023-01-01

2023-09-30

0001439264

country:HK

2024-01-01

2024-09-30

0001439264

country:HK

2023-01-01

2023-09-30

0001439264

MVNC:USTaxRegimeMember

2024-09-30

0001439264

MVNC:USTaxRegimeMember

2023-12-31

0001439264

MVNC:BritishVirginIslandsRegimeMember

2024-09-30

0001439264

MVNC:BritishVirginIslandsRegimeMember

2023-12-31

0001439264

MVNC:HongKongTaxRegimeMember

2024-09-30

0001439264

MVNC:HongKongTaxRegimeMember

2023-12-31

0001439264

MVNC:MajorCustomersMember

2024-01-01

2024-09-30

0001439264

MVNC:MajorVendorsMember

2024-01-01

2024-09-30

0001439264

MVNC:CustomerAMember

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2024-01-01

2024-09-30

0001439264

MVNC:CustomerAMember

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2024-09-30

0001439264

MVNC:CustomerBMember

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2024-01-01

2024-09-30

0001439264

MVNC:CustomerBMember

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2024-09-30

0001439264

MVNC:CustomerCMember

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2023-01-01

2023-09-30

0001439264

MVNC:CustomerCMember

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2023-09-30

0001439264

MVNC:CustomerDMember

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2023-01-01

2023-09-30

0001439264

MVNC:CustomerDMember

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2023-09-30

0001439264

MVNC:CustomerEMember

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2023-01-01

2023-09-30

0001439264

MVNC:CustomerEMember

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2023-09-30

0001439264

MVNC:CustomerAMember

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2024-07-01

2024-09-30

0001439264

MVNC:CustomerBMember

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2024-07-01

2024-09-30

0001439264

MVNC:CustomerBMember

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2023-07-01

2023-09-30

0001439264

MVNC:CustomerBMember

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2023-09-30

0001439264

MVNC:CustomerCMember

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2023-07-01

2023-09-30

0001439264

MVNC:CustomerDMember

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2023-07-01

2023-09-30

0001439264

MVNC:CustomerFMember

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2023-07-01

2023-09-30

0001439264

MVNC:CustomerFMember

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

2023-09-30

0001439264

MVNC:VendorDMember

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

2024-01-01

2024-09-30

0001439264

MVNC:VendorDMember

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

2024-09-30

0001439264

MVNC:VendorEMember

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

2024-01-01

2024-09-30

0001439264

MVNC:VendorEMember

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

2024-09-30

0001439264

MVNC:VendorAMember

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

2023-01-01

2023-09-30

0001439264

MVNC:VendorAMember

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

2023-09-30

0001439264

MVNC:VendorBMember

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

2023-01-01

2023-09-30

0001439264

MVNC:VendorBMember

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

2023-09-30

0001439264

MVNC:VendorCMember

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

2023-01-01

2023-09-30

0001439264

MVNC:VendorCMember

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

2023-09-30

0001439264

MVNC:VendorFMember

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

2024-07-01

2024-09-30

0001439264

MVNC:VendorFMember

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

2024-09-30

0001439264

MVNC:VendorDMember

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

2024-07-01

2024-09-30

0001439264

MVNC:VendorEMember

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

2024-07-01

2024-09-30

0001439264

MVNC:VendorEMember

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

2023-07-01

2023-09-30

0001439264

MVNC:VendorEMember

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

2023-09-30

0001439264

MVNC:VendorAMember

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

2023-07-01

2023-09-30

0001439264

MVNC:VendorCMember

us-gaap:CostOfGoodsTotalMember

us-gaap:SupplierConcentrationRiskMember

2023-07-01

2023-09-30

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

xbrli:pure

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

☒ QUARTERLY REPORT PURSUANT TO SECTION 13

OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2024

or

☐ TRANSITION REPORT UNDER SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from

to

Commission File Number 000-53612

MARVION INC.

(Exact name of registrant as specified in its charter)

| Nevada |

|

26-2723015 |

(State or other jurisdiction of

incorporation or organization) |

|

(IRS Employer

Identification No.) |

|

Room 1401, 14/F, Phase 1, Austin Tower

22-26 Austin Avenue, Jordan

Kowloon

Hong Kong

|

|

0000 |

| (Address of principal executive offices) |

|

(Zip Code) |

+ 852-21114437

(Registrant’s telephone number, including

area code)

Securities registered pursuant to Section 12(b)

of the Act:

| Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

| N/A |

|

N/A |

|

N/A |

Indicate by check mark whether

the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such

filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether

the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T

(§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit

such files).☒ Yes ☐ No

Indicate by check mark whether

the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging

growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting

company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer |

☐ |

Accelerated filer |

☐ |

| Non-accelerated filer |

☒ |

Smaller reporting company |

☒ |

| |

|

Emerging growth company |

☐ |

If an emerging growth company,

indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial

accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether

the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) ☐ Yes ☒ No

As of October 25, 2024, the

Company had outstanding 308,958,835 shares of common stock.

MARVION INC.

QUARTERLY REPORT

FOR THE QUARTER ENDED SEPTEMBER 30, 2024

TABLE OF CONTENTS

INTRODUCTORY COMMENTS

We are not a Hong Kong operating

company but a Nevada holding company with operations conducted through our wholly owned subsidiaries based in Hong Kong and Singapore.

Our investors hold shares of common stock in Marvion Inc., the Nevada holding company. This structure presents unique risks as our investors

may never directly hold equity interests in our Hong Kong subsidiary and will be dependent upon contributions from our subsidiaries to

finance our cash flow needs. Our ability to obtain contributions from our subsidiaries are significantly affected by regulations promulgated

by Hong Kong and Singaporean authorities. Any change in the interpretation of existing rules and regulations or the promulgation of new

rules and regulations may materially affect our operations and or the value of our securities, including causing the value of our securities

to significantly decline or become worthless. For a detailed description of the risks facing the Company associated with our structure,

please refer to “Risk Factors – Risks Relating to Doing Business in Hong Kong.” set forth in the Company’s

Annual Report on Form 10-K filed with the U.S. Securities and Exchange Commission (the “SEC”) on April 16, 2024 (the “Annual

Report”).

Marvion Inc. and our Hong

Kong subsidiaries are not required to obtain permission or approval from the China Securities Regulatory Commission, or CSRC, the Cybersecurity

Administration Committee, or CAC, or any other Chinese authorities to operate our business or to issue securities to foreign investors.

However, in light of the recent statements and regulatory actions by the People’s Republic of China (“the PRC”) government,

such as those related to Hong Kong’s national security, the promulgation of regulations prohibiting foreign ownership of Chinese

companies operating in certain industries, which are constantly evolving, and anti-monopoly concerns, we may be subject to the risks of

uncertainty of any future actions of the PRC government in this regard including the risk that we inadvertently conclude that such approvals

are not required, that applicable laws, regulations or interpretations change such that we are required to obtain approvals in the future,

or that the PRC government could disallow our holding company structure, which would likely result in a material change in our operations,

including our ability to continue our existing holding company structure, carry on our current business, accept foreign investments, and

offer or continue to offer securities to our investors. These adverse actions could cause the value of our common stock to significantly

decline or become worthless. We may also be subject to penalties and sanctions imposed by the PRC regulatory agencies, including the CSRC,

if we fail to comply with such rules and regulations, which would likely adversely affect the ability of the Company’s securities

to continue to trade on the Over-the-Counter Bulletin Board, which would likely cause the value of our securities to significantly decline

or become worthless.

There are prominent legal

and operational risks associated with our operations being in Hong Kong. For example, as a U.S.-listed Hong Kong public company,

we may face heightened scrutiny, criticism and negative publicity, which could result in a material change in our operations and the value

of our common stock. It could also significantly limit or completely hinder our ability to offer or continue to offer securities to investors

and cause the value of such securities to significantly decline or be worthless. We are subject to risks arising from the legal system

in China where there are risks and uncertainties regarding the enforcement of laws including where the Chinese government can change the

rules and regulations in China and Hong Kong, including the enforcement and interpretation thereof, at any time with little to no advance

notice and can intervene at any time with little to no advance notice. Changes in Chinese internal regulatory mandates, such as the M&A

rules, Anti-Monopoly Law, and Data Security Law, may target the Company’s corporate structure and impact our ability to conduct

business in Hong Kong, accept foreign investments, or list on an U.S. or other foreign exchange. By way of example, the PRC government

initiated a series of regulatory actions and statements to regulate business operations in China with little advance notice, including

cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas using variable

interest entity structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly

enforcement. In April 2020, the Cyberspace Administration of China and certain other PRC regulatory authorities promulgated the Cybersecurity

Review Measures, which became effective in June 2020. Pursuant to the Cybersecurity Review Measures, operators of critical information

infrastructure must pass a cybersecurity review when purchasing network products and services which do or may affect national security.

On July 10, 2021, the Cyberspace Administration of China issued a revised draft of the Measures for Cybersecurity Review for public comments

(“Draft Measures”), which required that, in addition to “operator of critical information infrastructure,” any

“data processor” carrying out data processing activities that affect or may affect national security should also be subject

to cybersecurity review, and further elaborated the factors to be considered when assessing the national security risks of the relevant

activities, including, among others, (i) the risk of core data, important data or a large amount of personal information being stolen,

leaked, destroyed, and illegally used or exited the country; and (ii) the risk of critical information infrastructure, core data, important

data or a large amount of personal information being affected, controlled, or maliciously used by foreign governments after listing abroad.

The Cyberspace Administration of China has said that under the proposed rules companies holding data on more than 1,000,000 users must

now apply for cybersecurity approval when seeking listings in other nations because of the risk that such data and personal information

could be “affected, controlled, and maliciously exploited by foreign governments,” The cybersecurity review will also investigate

the potential national security risks from overseas IPOs. On January 4, 2022, the CAC, in conjunction with 12 other government departments,

issued the New Measures for Cybersecurity Review (the “New Measures”). The New Measures amends the Draft Measures released

on July 10, 2021 and became effective on February 15, 2022.

The business of our subsidiaries

are not subject to cybersecurity review with the Cyberspace Administration of China, given that: (i) we do not have one million individual

online users of our products and services in Hong Kong; (ii) we do not possess a large amount of personal information in our business

operations. In addition, we are not subject to merger control review by China’s anti-monopoly enforcement agency due to the level

of our revenues which provided from us and audited by our auditor and the fact that we currently do not expect to propose or implement

any acquisition of control of, or decisive influence over, any company with revenues within China of more than Renminbi (“RMB”)

400 million. Currently, these statements and regulatory actions have had no impact on our daily business operations, the ability to accept

foreign investments and list our securities on an U.S. or other foreign exchange. However, since these statements and regulatory actions

are new, it is highly uncertain how soon legislative or administrative regulation making bodies will respond and what existing or new

laws or regulations or detailed implementations and interpretations will be modified or promulgated, if any, and the potential impact

such modified or new laws and regulations will have on our daily business operation, the ability to accept foreign investments and list

our securities on an U.S. or other foreign exchange. For a detailed description of the risks the Company is facing and the offering associated

with our operations in Hong Kong, please refer to “Risk Factors – Risks Relating to Doing Business in Hong Kong.”

set forth in the Annual Report.

The recent joint

statement by the SEC and Public Company Accounting Oversight Board (“PCAOB”), and the Holding Foreign Companies

Accountable Act (“HFCAA”) all call for additional and more stringent criteria to be applied to emerging market companies

upon assessing the qualification of their auditors, especially the non-U.S. auditors who are not inspected by the PCAOB. Trading in

our securities may be prohibited under the HFCAA if the PCAOB determines that it cannot inspect or investigate completely our

auditor, and that as a result, an exchange may determine to delist our securities. On June 22, 2021, the U.S. Senate passed the

Accelerating Holding Foreign Companies Accountable Act which would reduce the number of consecutive non-inspection years required

for triggering the prohibitions under the HFCAA from three years to two thus reducing the time before our securities may be

prohibited from trading or being delisted. On December 2, 2021, the U.S. Securities and Exchange Commission adopted rules to

implement the HFCAA. Pursuant to the HFCAA, the PCAOB issued its report notifying the Commission that it is unable to inspect or

investigate completely accounting firms headquartered in mainland China or Hong Kong due to positions taken by authorities in

mainland China and Hong Kong. Our auditor is based in Kuala Lumpur, Malaysia and is subject to PCAOB’s inspection. It is not

subject to the determinations announced by the PCAOB on December 16, 2021. However, in the event the Malaysian authorities

subsequently take a position disallowing the PCAOB to inspect our auditor, then we would need to change our auditor to avoid having

our securities delisted. Furthermore, due to the recent developments in connection with the implementation of the HFCAA, we cannot

assure you whether the SEC or other regulatory authorities would apply additional and more stringent criteria to us after

considering the effectiveness of our auditor’s audit procedures and quality control procedures, adequacy of personnel and

training, or sufficiency of resources, geographic reach or experience as it relates to the audit of our financial statements. The

requirement in the HFCAA that the PCAOB be permitted to inspect the issuer’s public accounting firm within two or three years,

may result in the delisting of our securities from applicable trading markets in the U.S, in the future if the PCAOB is unable to

inspect our accounting firm at such future time. Please see “Risk Factors- The Holding Foreign Companies Accountable Act

requires the Public Company Accounting Oversight Board (PCAOB) to be permitted to inspect the issuer’s public accounting firm

within three years. This three-year period will be shortened to two years if the Accelerating Holding Foreign Companies Accountable

Act is enacted. There are uncertainties under the PRC Securities Law relating to the procedures and requisite timing for the U.S.

securities regulatory agencies to conduct investigations and collect evidence within the territory of the PRC. If the U.S.

securities regulatory agencies are unable to conduct such investigations, they may suspend or de-register our registration with the

SEC and delist our securities from applicable trading market within the US.” set forth in the Annual Report.

In addition to the foregoing

risks, we face various legal and operational risks and uncertainties arising from doing business in Hong Kong as summarized below and

in “Risk Factors — Risks Relating to Doing Business in Hong Kong.” set forth in the Annual Report.

| |

· |

Adverse changes in economic and political policies of the PRC government could have a material and adverse effect on overall economic growth in China and Hong Kong, which could materially and adversely affect our business. Please see “Risk Factors-We face the risk that changes in the policies of the PRC government could have a significant impact upon the business we may be able to conduct in Hong Kong and the profitability of such business.” and “Substantial uncertainties and restrictions with respect to the political and economic policies of the PRC government and PRC laws and regulations could have a significant impact upon the business that we may be able to conduct in the PRC and accordingly on the results of our operations and financial condition.” set forth in the Annual Report. |

| |

· |

We are a holding company with operations conducted through our wholly owned subsidiaries based in Hong Kong and Singapore. This structure presents unique risks as our investors may never directly hold equity interests in our Hong Kong and Singapore subsidiaries and will be dependent upon contributions from our subsidiaries to finance our cash flow needs. Any limitation on the ability of our subsidiaries to make payments to us could have a material adverse effect on our ability to conduct business. We do not anticipate paying dividends in the foreseeable future; you should not buy our stock if you expect dividends. Please see “Risk Factors- Because our holding company structure creates restrictions on the payment of dividends or other cash payments, our ability to pay dividends or make other payments is limited.” set forth in the Annual Report. |

| |

|

|

| |

· |

There is a possibility that the PRC could prevent our cash maintained in Hong Kong from leaving or the PRC could restrict the deployment of the cash into our business or for the payment of dividends. We rely on dividends from our Hong Kong subsidiary for our cash and financing requirements, such as the funds necessary to service any debt we may incur. Any such controls or restrictions may adversely affect our ability to finance our cash requirements, service debt or make dividend or other distributions to our shareholders. Please see “Risk Factors - Our Hong Kong subsidiary may be subject to restrictions on paying dividends or making other payments to us, which may restrict its ability to satisfy liquidity requirements, conduct business and pay dividends to holders of our common stock.”; “Risk Factors - PRC regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion may delay or prevent us from using the proceeds we receive from offshore financing activities to make loans to or make additional capital contributions to our Hong Kong subsidiaries, which could materially and adversely affect our liquidity and our ability to fund and expand business.”; “Risk Factors - Because our holding company structure creates restrictions on the payment of dividends or other cash payments, our ability to pay dividends or make other payments is limited.” and “Transfers of Cash to and from our Subsidiaries” set forth in the Annual Report. |

| |

|

|

| |

· |

PRC regulation of loans to and direct investments in PRC entities by offshore holding companies may delay or prevent us from using the proceeds of this offering to make loans or additional capital contributions to our operating subsidiaries in Hong Kong. Substantial uncertainties exist with respect to the interpretation of the PRC Foreign Investment Law and how it may impact the viability of our current corporate structure, corporate governance and business operations. Please see “Risk Factors- PRC regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion may delay or prevent us from using the proceeds we receive from offshore financing activities to make loans to or make additional capital contributions to our Hong Kong subsidiaries, which could materially and adversely affect our liquidity and our ability to fund and expand business.” set forth in the Annual Report. |

| |

|

|

| |

· |

In light of China’s extension of its authority into Hong Kong, the Chinese government can change Hong Kong’s rules and regulations at any time with little or no advance notice, and can intervene and influence our operations and business activities in Hong Kong. We are currently not required to obtain approval from Chinese authorities to list on U.S. exchanges. However, if our subsidiaries or the holding company were required to obtain approval in the future, or we erroneously conclude that approvals were not required, or we were denied permission from Chinese authorities to operate or to list on U.S. exchanges, we will not be able to continue listing on a U.S. exchange and the value of our common stock would likely significantly decline or become worthless, which would materially affect the interest of the investors. There is a risk that the Chinese government may intervene or influence our operations at any time, or may exert more control over offerings conducted overseas and/or foreign investment in Hong Kong-based issuers, which could result in a material change in our operations and/or the value of our securities. Further, any actions by the Chinese government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers would likely significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless. Please see “Risk Factors-We face the risk that changes in the policies of the PRC government could have a significant impact upon the business we may be able to conduct in the Hong Kong and the profitability of such business.” and “Substantial uncertainties and restrictions with respect to the political and economic policies of the PRC government and PRC laws and regulations could have a significant impact upon the business that we may be able to conduct in the PRC and accordingly on the results of our operations and financial condition.” and “The Chinese government exerts substantial influence over the manner in which we must conduct our business activities. We are currently not required to obtain approval from Chinese authorities to list on U.S. exchanges. However, to the extent that the Chinese government exerts more control over offerings conducted overseas and/or foreign investment in China-based issuers over time and if our PRC subsidiaries or the holding company were required to obtain approval in the future and were denied permission from Chinese authorities to list on U.S. exchanges, we will not be able to continue listing on U.S. exchange and the value of our common stock may significantly decline or become worthless, which would materially affect the interest of the investors.” set forth in the Annual Report. |

| |

· |

Governmental control of currency conversion may limit our ability to utilize our revenues effectively and affect the value of your investment. |

| |

|

|

| |

· |

We may become subject to a variety of laws and regulations in the PRC regarding privacy, data security, cybersecurity, and data protection. We may be liable for improper use or appropriation of personal information provided by our customers. Please see “Risk Factors- The Chinese government exerts substantial influence over the manner in which we must conduct our business activities. We are currently not required to obtain approval from Chinese authorities to list on U.S exchanges. However, to the extent that the Chinese government exerts more control over offerings conducted overseas and/or foreign investment in China-based issuers over time and if our PRC subsidiaries or the holding company were required to obtain approval in the future and were denied permission from Chinese authorities to list on U.S. exchanges, we will not be able to continue listing on U.S. exchange and the value of our common stock may significantly decline or become worthless, which would materially affect the interest of the investors.” set forth in the Annual Report. |

| |

|

|

| |

· |

Under the Enterprise Income Tax Law of the PRC (“EIT Law”), we may be classified as a “Resident Enterprise” of China. Such classification will likely result in unfavorable tax consequences to us and our non-PRC shareholders. Please see “Risk Factors- Our global income may be subject to PRC taxes under the PRC Enterprise Income Tax Law, which could have a material adverse effect on our results of operations.” set forth in the Annual Report. |

| |

|

|

| |

· |

Failure to comply with PRC regulations relating to the establishment of offshore special purpose companies by PRC residents may subject our PRC resident Shareholders to personal liability, may limit our ability to acquire Hong Kong and PRC companies or to inject capital into our Hong Kong subsidiary, may limit the ability of our Hong Kong subsidiaries to distribute profits to us or may otherwise materially and adversely affect us. |

| |

|

|

| |

· |

You may be subject to PRC income tax on dividends from us or on any gain realized on the transfer of shares of our common stock. Please see “Risk Factors- Dividends payable to our foreign investors and gains on the sale of our shares of common stock by our foreign investors may become subject to tax by the PRC.” set forth in the Annual Report. |

| |

|

|

| |

· |

We face uncertainties with respect to indirect transfers of equity interests in PRC resident enterprises by their non-PRC holding companies. Please see “Risk Factors- We and our shareholders face uncertainties with respect to indirect transfers of equity interests in PRC resident enterprises by their non-PRC holding companies.” set forth in the Annual Report. |

| |

|

|

| |

· |

We are organized under the laws of the State of Nevada as a holding company that conducts its business through a number of subsidiaries organized under the laws of foreign jurisdictions such as Hong Kong, Singapore and the British Virgin Islands. This may have an adverse impact on the ability of U.S. investors to enforce a judgment obtained in U.S. Courts against these entities, bring actions in Hong Kong against us or our management or to effect service of process on the officers and directors managing the foreign subsidiaries. Please see “Risk Factors- Substantially all of our assets and a majority of our officers and directors are located in Hong Kong. The balance of our directors and officers are located in Singapore. As a result, it may be difficult for stockholders to enforce any judgment obtained in the United States against us, our officers or directors, which may limit the remedies otherwise available to our stockholders.” set forth in the Annual Report. |

| |

|

|

| |

· |

U.S. regulatory bodies may be limited in their ability to conduct investigations or inspections of our operations in China. |

| |

|

|

| |

· |

There are significant uncertainties under the EIT Law relating to the withholding tax liabilities of our PRC subsidiary, and dividends payable by our PRC subsidiary to our offshore subsidiaries may not qualify to enjoy certain treaty benefits. Please see “Risk Factors- Our global income may be subject to PRC taxes under the PRC Enterprise Income Tax Law, which could have a material adverse effect on our results of operations.” set forth in the Annual Report. |

References in this registration statement to

the “Company,” “MVNC,” “we,” “us” and “our” refer to Marvion Inc., a Nevada

company and all of its subsidiaries on a consolidated basis. Where reference to a specific entity is required, the name of such specific

entity will be referenced.

Transfers of Cash to and from Our Subsidiaries

Marvion Inc. is a Nevada

holding company with no operations of its own. We conduct our operations in Hong Kong primarily through our subsidiaries in Hong Kong

and Singapore. We may rely on dividends or other transfers of cash or assets to be made by our Hong Kong and Singapore subsidiaries to

fund our cash and financing requirements, including the funds necessary to pay dividends and other cash distributions to our shareholders,

to service any debt we may incur and to pay our operating expenses. If our Hong Kong and Singapore subsidiaries incur debt on their own

behalf in the future, the instruments governing the debt may restrict their ability to pay dividends or make other distributions to us.

To date, our subsidiaries have not made any transfers, dividends or distributions of cash flows or other assets to Marvion Inc. and Marvion

Inc. has not made any transfers, dividends or distributions of cash flows or other assets to our subsidiaries.

Marvion Inc. is permitted

under the Nevada laws to provide funding to and receive funding from our subsidiaries in Hong Kong and Singapore through loans or capital

contributions without restrictions on the amount of the funds, subject to satisfaction of applicable government registration, approval

and filing requirements. Our Hong Kong subsidiaries, Marvion (Hong Kong) Limited, Marvion Studios Limited (“MSL”) (Formerly

known as Typerwise Limited) and Marvel Multi-dimensions Limited (“MMDL”), and our Singapore subsidiary Marvion Private Limited,

are also permitted under the laws of Hong Kong and Singapore to provide and receive funding to and from Marvion Inc. through dividend

distribution without restrictions on the amount of the funds. As of the date of this report, there has been no dividends or distributions

among the holding company or the subsidiaries nor do we expect such dividends or distributions to occur in the foreseeable future among

the holding company and its subsidiaries.

We currently intend to retain

all available funds and future earnings, if any, for the operation and expansion of our business and do not anticipate declaring or paying

any dividends in the foreseeable future. Any future determination related to our dividend policy will be made at the discretion of our

board of directors after considering our financial condition, results of operations, capital requirements, contractual requirements, business

prospects and other factors the board of directors deems relevant, and subject to the restrictions contained in any future financing instruments.

Subject to the Nevada Revised

Statutes and our bylaws, our board of directors may authorize and declare a dividend to shareholders at such time and of such an amount

as they think fit if they are satisfied, on reasonable grounds, that immediately following the dividend the value of our assets will exceed

our liabilities and we will be able to pay our debts as they become due. There is no further Nevada statutory restriction on the amount

of funds which may be distributed by us by dividend.

Under the current practice

of the Inland Revenue Department of Hong Kong, no tax is payable in Hong Kong in respect of dividends paid by us. The laws and regulations

of the PRC do not currently have any material impact on transfer of cash from Marvion Inc. to our Hong Kong subsidiaries or from our Hong

Kong subsidiaries to Marvion Inc. There are no restrictions or limitation under the laws of Hong Kong imposed on the conversion of Hong

Kong dollar (“HKD”) into foreign currencies and the remittance of currencies out of Hong Kong or across borders and to U.S.

investors.

There is a possibility that

the PRC could prevent our cash maintained in Hong Kong from leaving or the PRC could restrict the deployment of the cash into our business

or for the payment of dividends. Any such controls or restrictions may adversely affect our ability to finance our cash requirements,

service debt or make dividend or other distributions to our shareholders. Please see “Risk Factors - Our Hong Kong subsidiary

may be subject to restrictions on paying dividends or making other payments to us, which may restrict its ability to satisfy liquidity

requirements, conduct business and pay dividends to holders of our common stock.”; “Risk Factors - PRC regulation of loans

to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion may delay or prevent

us from using the proceeds we receive from offshore financing activities to make loans to or make additional capital contributions to

our Hong Kong subsidiaries, which could materially and adversely affect our liquidity and our ability to fund and expand business.”;

“Risk Factors - Because our holding company structure creates restrictions on the payment of dividends or other cash payments, our

ability to pay dividends or make other payments is limited.”

Current PRC regulations permit

PRC subsidiaries to pay dividends to Hong Kong subsidiaries only out of their accumulated profits, if any, determined in accordance with

Chinese accounting standards and regulations. In addition, each of our subsidiaries in China is required to set aside at least 10% of

its after-tax profits each year, if any, to fund a statutory reserve until such reserve reaches 50% of its registered capital. Each of

such entity in China is also required to further set aside a portion of its after-tax profits to fund the employee welfare fund, although

the amount to be set aside, if any, is determined at the discretion of its board of directors. Although the statutory reserves can be

used, among other ways, to increase the registered capital and eliminate future losses in excess of retained earnings of the respective

companies, the reserve funds are not distributable as cash dividends except in the event of liquidation. As of the date of this report,

we do not have any PRC subsidiaries.

The PRC government imposes

controls on the conversion of RMB into foreign currencies and the remittance of currencies out of the PRC. Therefore, we may experience

difficulties in completing the administrative procedures necessary to obtain and remit foreign currency to finance our cash requirements,

service debt or make dividend or other distributions to our shareholders. Furthermore, if our subsidiaries in the PRC incur debt on their

own in the future, the instruments governing the debt may restrict their ability to pay dividends or make other payments. If we or our

subsidiaries are unable to receive all of the revenues from our operations, we may be unable to pay dividends on our common stock.

Cash dividends, if any, on

our common stock will be paid in U.S. dollars. If we are considered a PRC tax resident enterprise for tax purposes, any dividends we pay

to our overseas shareholders may be regarded as China-sourced income and as a result may be subject to PRC withholding tax at a rate of

up to 10.0%.

In order for us to pay dividends

to our shareholders, we will rely on payments made from our Hong Kong and Singapore subsidiaries to Marvion Inc. If in the future we have

PRC subsidiaries, certain payments from such PRC subsidiaries to Hong Kong subsidiaries will be subject to PRC taxes, including business

taxes and VAT. As of the date of this report, we do not have any PRC subsidiaries and our Hong Kong and Singapore subsidiaries have not

made any transfers, dividends or distributions nor do we expect to make such transfers, dividends or distributions in the foreseeable

future.

Pursuant to the Arrangement

between Mainland China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and Tax Evasion on Income,

or the Double Tax Avoidance Arrangement, the 10% withholding tax rate may be lowered to 5% if a Hong Kong resident enterprise owns no

less than 25% of a PRC entity. However, the 5% withholding tax rate does not automatically apply and certain requirements must be satisfied,

including, without limitation, that (a) the Hong Kong entity must be the beneficial owner of the relevant dividends; and (b) the Hong

Kong entity must directly hold no less than 25% share ownership in the PRC entity during the 12 consecutive months preceding its receipt

of the dividends. In current practice, a Hong Kong entity must obtain a tax resident certificate from the Hong Kong tax authority to apply

for the 5% lower PRC withholding tax rate. As the Hong Kong tax authority will issue such a tax resident certificate on a case-by-case

basis, we cannot assure you that we will be able to obtain the tax resident certificate from the relevant Hong Kong tax authority and

enjoy the preferential withholding tax rate of 5% under the Double Taxation Arrangement with respect to dividends to be paid by a PRC

subsidiary to its immediate holding company. As of the date of this report, we do not have a PRC subsidiary. In the event that we acquire

or form a PRC subsidiary in the future and such PRC subsidiary desires to declare and pay dividends to our Hong Kong subsidiary, our Hong

Kong subsidiary will be required to apply for the tax resident certificate from the relevant Hong Kong tax authority. In such event, we

plan to inform the investors through SEC filings, such as a current report on Form 8-K, prior to such actions. See “Risk Factors

– Risks Relating to Doing Business in Hong Kong.” set forth in the Annual Report.

CAUTIONARY NOTE CONCERNING FORWARD-LOOKING STATEMENTS

This Quarterly Report on

Form 10-Q includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended,

and Section 21E of the Securities Exchange Act of 1934, as amended that are not historical facts, and involve risks and uncertainties

that could cause actual results to differ materially from those expected and projected. All statements, other than statements of historical

facts, included in this Quarterly Report on Form 10-Q including, without limitation, statements in the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” regarding the Company’s market projections, financial position,

business strategy and the plans and objectives of management for future operations, events or developments which the Company expects or

anticipates will or may occur in the future, including such things as future capital expenditures (including the amount and nature thereof);

expansion and growth of the Company’s business and operations; and other such matters are forward-looking statements. These statements

are based on certain assumptions and analyses made by the Company in light of its experience and its perception of historical trends,

current conditions and expected future developments, as well as other factors it believes are appropriate under the circumstances. However,

whether actual results or developments will conform with the Company’s expectations and predictions is subject to a number of risks

and uncertainties, including general economic, market and business conditions; the business opportunities (or lack thereof) that may be

presented to and pursued by the Company; changes in laws or regulation; and other factors, most of which are beyond the control of the

Company.

These forward-looking statements

can be identified by the use of predictive, future-tense or forward-looking terminology, such as “believes,” “anticipates,”

“expects,” “estimates,” “plans,” “may,” “will,” or similar terms. These statements

appear in a number of places in this filing and include statements regarding the intent, belief or current expectations of the Company,

and its directors or its officers with respect to, among other things: (i) trends affecting the Company’s financial condition or

results of operations for its limited history; (ii) the Company’s business and growth strategies; and (iii) the Company’s

financing plans. Investors are cautioned that any such forward-looking statements are not guarantees of future performance and involve

significant risks and uncertainties, and that actual results may differ materially from those projected in the forward-looking statements

as a result of various factors. Such factors that could adversely affect actual results and performance include, but are not limited to,

the Company’s limited operating history, potential fluctuations in quarterly operating results and expenses, government regulation,

technological change and competition. For information identifying important factors that could cause actual results to differ materially

from those anticipated in the forward-looking statements, please refer to the Risk Factors section of the Company’s Annual Report.

Consequently, all of the

forward-looking statements made in this Quarterly Report on Form 10-Q are qualified by these cautionary statements and there can be no

assurance that the actual results or developments anticipated by the Company will be realized or, even if substantially realized, that

they will have the expected consequence to or effects on the Company or its business or operations. The Company assumes no obligations

to update any such forward-looking statements.

PART I - FINANCIAL INFORMATION

Item 1. Financial Statements

MARVION INC. AND SUBSIDIARIES

UNAUDITED CONDENSED CONSOLIDATED BALANCE SHEETS

(Currency expressed in United States Dollars

(“US$”), except for number of shares)

| | |

| | |

| |

| | |

September 30, 2024 | | |

December

31, 2023 | |

| | |

| | |

(Restated) | |

| ASSETS | |

| | | |

| | |

| Current assets: | |

| | | |

| | |

| Account receivables | |

$ | 210,761 | | |

$ | 74,263 | |

| Cash and cash equivalents | |

| 159,992 | | |

| 120,319 | |

| Prepaid expenses and other current

assets | |

| 17,125 | | |

| 1,537 | |

| Total current assets | |

| 387,878 | | |

| 196,119 | |

| | |

| | | |

| | |

| Non-current assets: | |

| | | |

| | |

| Construction in progress | |

| 1,293,375 | | |

| 886,896 | |

| Property and equipment, net | |

| 752,400 | | |

| 764,371 | |

| Right-of-use assets, net | |

| 1,274,043 | | |

| 1,357,270 | |

| Total non-current assets | |

| 3,319,818 | | |

| 3,008,537 | |

| | |

| | | |

| | |

| TOTAL ASSETS | |

$ | 3,707,696 | | |

$ | 3,204,656 | |

| | |

| | | |

| | |

| LIABILITIES AND SHAREHOLDERS’ DEFICIT | |

| | | |

| | |

| Current liabilities: | |

| | | |

| | |

| Account payables | |

$ | 3,218 | | |

$ | 57,243 | |

| Accrued liabilities and other payables | |

| 770,093 | | |

| 120,779 | |

| Amounts due to directors | |

| 1,651,554 | | |

| 1,020,409 | |

| Construction payable | |

| 378,379 | | |

| 639,751 | |

| Convertible note payable | |

| 170,000 | | |

| – | |

| Promissory notes | |

| 5,500,000 | | |

| – | |

| Lease liabilities | |

| 96,409 | | |

| 88,816 | |

| Promissory note payable | |

| 16 | | |

| – | |

| Tax payable | |

| 53,745 | | |

| 17,420 | |

| Total current liabilities | |

| 8,623,414 | | |

| 1,944,418 | |

| | |

| | | |

| | |

| Non-current liabilities: | |

| | | |

| | |

| Lease liabilities | |

| 1,278,876 | | |

| 1,345,094 | |

| TOTAL LIABILITIES | |

| 9,902,290 | | |

| 3,289,512 | |

| | |

| | | |

| | |

| Commitments and contingencies | |

| – | | |

| – | |

| | |

| | | |

| | |

| Shareholders’ deficit: | |

| | | |

| | |

| Preferred stock, par value $0.0001, 30,000,000,000

shares authorized, 18,999,999 and 18,999,999 shares undesignated as of September 30, 2024 and December 31, 2023, respectively | |

| – | | |

| – | |

| Preferred stock, Series A, par value $0.0001, 10,000,000

shares designated, 10,000,000 and 0 shares issued and outstanding as of September 30, 2024 and December 31, 2023, respectively | |

| 1,000 | | |

| – | |

| Preferred stock, Series B, par value $0.0001, 1,000,000

shares designated, 366,346 and 0 shares issued and outstanding as of September 30, 2024 and December 31, 2023, respectively | |

| 37 | | |

| – | |

| Preferred stock, Series C, par value $0.001, 1 share

designated, 1 and 0 share issued and outstanding as of September 30, 2024 and December 31, 2023, respectively | |

| 1 | | |

| – | |

| Common stock, par value $0.0001, 270,000,000,000

shares authorized, 308,958,835 and 148,148,150 shares issued and outstanding as of September 30, 2024 and December 31, 2023, respectively | |

| 30,897 | | |

| 14,815 | |

| Additional paid-in capital | |

| – | | |

| – | |

| Accumulated other comprehensive income | |

| 921 | | |

| 61 | |

| Accumulated losses | |

| (6,227,450 | ) | |

| (99,732 | ) |

| Total shareholders’ deficit | |

| (6,194,594 | ) | |

| (84,856 | ) |

| TOTAL LIABILITIES AND SHAREHOLDERS’

DEFICIT | |

$ | 3,707,696 | | |

$ | 3,204,656 | |

See Accompanying Notes

to Unaudited Condensed Consolidated Financial Statements.

MARVION INC. AND SUBSIDIARIES

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS

OF OPERATIONS AND

COMPREHENSIVE (LOSS) INCOME

(Currency expressed in United States Dollars

(“US$”), except for number of shares)

| | |

| | |

| | |

| | |

| |

| | |

For the Three Months Ended September 30, | | |

For the Nine Months Ended September 30, | |

| | |

2024 | | |

2023 | | |

2024 | | |

2023 | |

| | |

| | |

| | |

| | |

| |

| Revenues | |

$ | 390,275 | | |

$ | 212,502 | | |

$ | 1,019,593 | | |

$ | 406,607 | |

| Cost of revenues | |

| (193,891 | ) | |

| (88,893 | ) | |

| (517,252 | ) | |

| (181,675 | ) |

| Gross profit | |

| 196,384 | | |

| 123,609 | | |

| 502,341 | | |

| 224,932 | |

| | |

| | | |

| | | |

| | | |

| | |

| Operating expenses: | |

| | | |

| | | |

| | | |

| | |

| General and administrative expenses | |

| (573,438 | ) | |

| (57,737 | ) | |

| (732,377 | ) | |

| (144,610 | ) |

| Total operating expenses | |

| (573,438 | ) | |

| (57,737 | ) | |

| (732,377 | ) | |

| (144,610 | ) |

| (Loss) income from operations | |

| (377,054 | ) | |

| 65,872 | | |

| (230,036 | ) | |

| 80,322 | |

| | |

| | | |

| | | |

| | | |

| | |

| Other income: | |

| | | |

| | | |

| | | |

| | |

| Interest income | |

| 612 | | |

| 108 | | |

| 1,597 | | |

| 420 | |

| Total other income | |

| 612 | | |

| 108 | | |

| 1,597 | | |

| 420 | |

| Income tax expense | |

| (2,531 | ) | |

| (19,887 | ) | |

| (36,045 | ) | |

| (19,887 | ) |

| Net (loss) income | |

| (378,973 | ) | |

| 46,093 | | |

| (264,484 | ) | |

| 60,855 | |

| | |

| | | |

| | | |

| | | |

| | |

| Other comprehensive income: | |

| | | |

| | | |

| | | |

| | |

| Foreign currency adjustment (loss) gain | |

| 705 | | |

| (37 | ) | |

| 860 | | |

| 321 | |

| Comprehensive (loss) income | |

$ | (378,268 | ) | |

$ | 46,056 | | |

$ | (263,624 | ) | |

$ | 61,176 | |

| | |

| | | |

| | | |

| | | |

| | |

| Net (loss) income per share: | |

| | | |

| | | |

| | | |

| | |

| Basic (1) | |

$ | (0.00 | ) | |

$ | 0.00 | | |

$ | (0.00 | ) | |

$ | 0.00 | |

| Diluted (1) | |

$ | (0.00 | ) | |

$ | 0.00 | | |

$ | (0.00 | ) | |

$ | 0.00 | |

| | |

| | | |

| | | |

| | | |

| | |

| Weighted average common shares outstanding: | |

| | | |

| | | |

| | | |

| | |

| Basic # | |

| 167,498,301 | | |

| 148,148,150 | | |

| 152,650,588 | | |

| 148,148,150 | |

| Diluted # | |

| 167,498,301 | | |

| 148,148,150 | | |

| 152,650,588 | | |

| 148,148,150 | |

See Accompanying Notes to Unaudited Condensed

Consolidated Financial Statements.

MARVION INC. AND SUBSIDIARIES

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS

OF CHANGES IN SHAREHOLDERS’ DEFICIT

(Currency expressed in United States Dollars

(“US$”), except for number of shares)

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| | |

Preferred stock | |

Common stock | |

Additional | |

Accumulated

other

comprehensive | |

(Accumulated

deficit) | |

Total

shareholders’ |

| | |

No. of

shares | |

Amount | |

No. of

shares | |

Amount | |

paid-in

capital | |

income

(loss) | |

Retained

earnings | |

(deficit)

equity |

| | |

| |

| |

| |

| |

| |

| |

| |

|

| For the Three and Nine Months Ended September 30, 2024 |

| Balance as of January 1, 2024 (restated) | |

| – | | |

$ | – | | |

| 148,148,150 | | |

$ | 14,815 | | |

$ | – | | |

$ | 61 | | |

$ | (99,732 | ) | |

$ | (84,856 | ) |

| Foreign translation adjustment | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| 159 | | |

| – | | |

| 159 | |

| Net income for the period | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| 43,715 | | |

| 43,715 | |

| Balance as of March 31, 2024 | |

| – | | |

| – | | |

| 148,148,150 | | |

| 14,815 | | |

| – | | |

| 220 | | |

| (56,017 | ) | |

| (40,982 | ) |

| Foreign translation adjustment | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| (4 | ) | |

| – | | |

| (4 | ) |

| Net income for the period | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| 70,774 | | |

| 70,774 | |

| Balance as of June 30, 2024 | |

| – | | |

| – | | |

| 148,148,150 | | |

| 14,815 | | |

| – | | |

| 216 | | |

| 14,757 | | |

| 29,788 | |

| Share issued for acquisition of legal acquirer | |

| 10,366,346 | | |

| 1,038 | | |

| 160,810,685 | | |

| 16,082 | | |

| 41,639,772 | | |

| – | | |

| (47,503,006 | ) | |

| (5,846,114 | ) |

| Recapitalization of legal acquirer | |

| – | | |

| – | | |

| – | | |

| – | | |

| (41,639,772 | ) | |

| – | | |

| 41,639,772 | | |

| – | |

| Foreign translation adjustment | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| 705 | | |

| – | | |

| 705 | |

| Net loss for the period | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| (378,973 | ) | |

| (378,973 | ) |

| Balance as of September 30, 2024 | |

| 10,366,346 | | |

$ | 1,038 | | |

| 308,958,835 | | |

$ | 30,897 | | |

$ | – | | |

$ | 921 | | |

$ | (6,227,450 | ) | |

$ | (6,194,594 | ) |

| For the Three and Nine Months Ended September 30, 2023 |

| Balance as of January 1, 2023 (restated) | |

| – | | |

$ | – | | |

| 148,148,150 | | |

$ | 14,815 | | |

$ | – | | |

$ | 31 | | |

$ | (109,076 | ) | |

$ | (94,230 | ) |

| Foreign translation adjustment | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| 509 | | |

| – | | |

| 509 | |

| Net income for the period | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| 8,994 | | |

| 8,994 | |

| Balance as of March 31, 2023 | |

| – | | |

| – | | |

| 148,148,150 | | |

| 14,815 | | |

| – | | |

| 540 | | |

| (100,082 | ) | |

| (84,727 | ) |

| Foreign translation adjustment | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| (151 | ) | |

| – | | |

| (151 | ) |

| Net income for the period | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| 5,768 | | |

| 5,768 | |

| Balance as of June 30, 2023 | |

| – | | |

| – | | |

| 148,148,150 | | |

| 14,815 | | |

| – | | |

| 389 | | |

| (94,314 | ) | |

| (79,110 | ) |

| Foreign translation adjustment | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| (37 | ) | |

| – | | |

| (37 | ) |

| Net income for the period | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| – | | |

| 46,093 | | |

| 46,093 | |

| Balance as of September 30, 2023 | |

| – | | |

$ | – | | |

| 148,148,150 | | |

$ | 14,815 | | |

$ | – | | |

$ | 352 | | |

$ | (48,221 | ) | |

$ | (33,054 | ) |

See Accompanying Notes to Unaudited Condensed

Consolidated Financial Statements.

MARVION INC. AND SUBSIDIARIES

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS

OF CASH FLOWS

(Currency expressed in United States Dollars

(“US$”))

| | |

| |

|

| | |

For the Nine Months Ended September 30, |

| | |

2024 | |

2023 |

| Cash flows from operating activities: | |

| | | |

| | |

| Net (loss) income | |

$ | (264,484 | ) | |

$ | 60,855 | |

| Adjustments to reconcile net (loss) income to net cash (used in) provided by operating activities: | |

| | | |

| | |

| Depreciation of property and equipment | |

| 55,658 | | |

| 5,442 | |

| Amortization of right-of use assets | |

| 89,408 | | |

| 28,426 | |

| Interest expenses on lease liabilities | |

| 60,648 | | |

| 887 | |

| | |

| | | |

| | |

| Change in operating assets and liabilities: | |

| | | |

| | |

| Account receivables | |

| (136,498 | ) | |

| (100,150 | ) |

| Account payables | |

| (54,025 | ) | |

| 27,245 | |

| Construction payable | |

| (261,372 | ) | |

| – | |

| Prepaid expenses and other current assets | |

| (13,597 | ) | |

| (1,532 | ) |

| Accrued liabilities and other payable | |

| 471,225 | | |

| 5,894 | |

| Operating lease liabilities | |

| (125,961 | ) | |

| (3,064 | ) |

| Income tax payable | |

| 36,045 | | |

| 19,887 | |

| Net cash (used in) provided by operating activities | |

| (142,953 | ) | |

| 43,890 | |

| | |

| | | |

| | |

| Cash flows from investing activities: | |

| | | |

| | |

| Purchase of property and equipment | |

| (446,497 | ) | |

| (675,299 | ) |

| Net cash used in investing activities | |

| (446,497 | ) | |

| (675,299 | ) |

| | |

| | | |

| | |

| Cash flows from financing activities: | |

| | | |

| | |

| Advance from a director | |

| 631,145 | | |

| 609,824 | |

| Net cash provided by financing activities | |

| 631,145 | | |

| 609,824 | |

| | |

| | | |

| | |

| Effect of exchange rate on cash and cash equivalents | |

| (2,022 | ) | |

| 323 | |

| Net change in cash and cash equivalents | |

| 39,673 | | |

| (21,262 | ) |

| Cash and cash equivalents at beginning of the period | |

| 120,319 | | |

| 52,633 | |

| Cash and cash equivalents at end of the period | |

$ | 159,992 | | |

$ | 31,371 | |

| | |

| | | |

| | |

| Supplemental disclosure of cash flow information: | |

| | | |

| | |

| Cash paid for income taxes | |

$ | – | | |

$ | – | |

| Cash paid for interest | |

$ | – | | |

$ | – | |

| | |

| | | |

| | |

| Non-cash investing and financing activities: | |

| | | |

| | |

| Issuance of promissory notes for earnout liabilities through Share Exchange Transaction | |

$ | 5,500,000 | | |

$ | – | |

See Accompanying Notes to Unaudited Condensed

Consolidated Financial Statements.

MARVION INC. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL

STATEMENTS

FOR THE THREE AND NINE MONTHS ENDED SEPTEMBER

30, 2024

1. BASIS

OF PRESENTATION

These accompanying unaudited

condensed consolidated financial statements have been prepared in accordance with generally accepted accounting principles in the United

States of America (“US GAAP”) for interim financial information pursuant to the rules and regulations of the Securities and

Exchange Commission (the “SEC”). Accordingly, they do not include all of the information and footnotes required by U.S. GAAP

for complete financial statements. In the opinion of management, all adjustments (consisting of normal recurring accruals) considered

necessary to make the financial statements not misleading have been included. Operating results for the period ended September 30, 2024

are not necessarily indicative of the results that may be expected for the fiscal year ending December 31, 2024. The information included

in this Quarterly Report on Form 10-Q should be read in conjunction with Management’s Discussion and Analysis, and the financial

statements and notes thereto included in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2023, filed

with the SEC on April 16, 2024.

2. ORGANIZATION

AND BUSINESS BACKGROUND

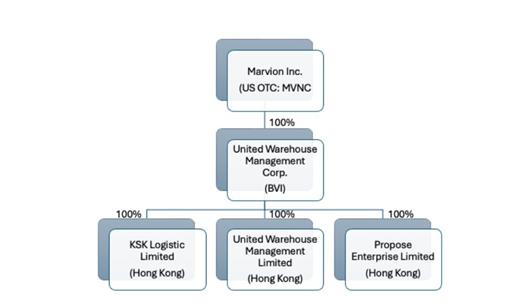

Marvion Inc. was incorporated

in the State of Nevada on March 6, 2008. The Company and its subsidiaries are hereinafter referred to as (the “Company”).

On August 15, 2024, the Company

and United Warehouse Management Corp., a British Virgin Island corporation (“UWMC”) and eleven shareholders of UWMC entered

into a Share Exchange Agreement (the “SEA”) pursuant to which the shareholders of UWMC agreed to transfer to the Company 4,000

shares of UWMC, constituting all of the issued and outstanding securities of UWMC, in exchange for 148,148,150 shares of common stock

of the Company, par value $0.0001 per share (the “share exchange transaction”).

In connection with the share

exchange transaction, all prior officers and directors of the Company resigned and new officers and directors were appointed as officers

and directors of the Company. Such share exchange transaction has been accounted for as a reverse merger and recapitalization of the Company,

whereby UWMC is deemed to be the accounting acquirer (legal acquiree) and the Company to be the accounting acquiree (legal acquirer).

Accordingly, the consolidated assets, liabilities and results of operations of the Company will become the historical financial statements

of UWMC, and the Company’s assets, liabilities and results of operations will be consolidated with UWMC beginning on the date of

the share exchange transaction. No goodwill is recognized in this transaction. The historical financial statements prior to the share

exchange transaction are those of the accounting acquirer (UWMC). Historical stockholders’ equity of the accounting acquirer prior

to the reverse merger are retroactively restated (a recapitalization) for the equivalent number of shares received in the merger. Operations