UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 13E-3

RULE 13e-3 TRANSACTION STATEMENT UNDER SECTION 13(e)

OF THE SECURITIES EXCHANGE ACT OF 1934

(AMENDMENT NO. 2)

ASTRA SPACE,

INC.

(Name of the Issuer)

Astra Space,

Inc.

Apogee Parent Inc.

Apogee Merger Sub Inc.

Chris C. Kemp

Chris C.

Kemp, Trustee of

the Chris Kemp Living

Trust dated February 10,

2021

Adam P. London

(Names of Persons Filing Statement)

Class A Common Stock, par value $0.0001 per share

(Title of Class of Securities)

04634X202

(CUSIP Number

of Class of Securities)

|

|

|

| Chris C. Kemp

Adam P. London Astra

Space, Inc. 1900 Skyhawk Street

Alameda, California (866)

278-7217 |

|

Chris C. Kemp

Adam P. London Apogee

Parent Inc. Apogee Merger Sub Inc.

1900 Skyhawk Street

Alameda, California (866)

278-7217 |

(Name, Address and Telephone Numbers of Person Authorized to Receive Notices and Communications on Behalf of

the Persons Filing Statement)

With copies to

|

|

|

|

|

| Lillian Kim

Stephen B. Amdur

Pillsbury Winthrop Shaw Pittman LLP

31 West 52nd Street New

York, New York (212) 858-1000 |

|

Katheryn A. Gettman

Kevin Roggow Cozen

O’Connor P.C. 33 South 6th Street, Suite 3800

Minneapolis, Minnesota

(612) 260-9000 |

|

Jenny Hochenberg

Boris Feldman Freshfields

Bruckhaus Deringer LLP 601 Lexington Ave

New York, New York (212) 277-4000 |

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED THIS

TRANSACTION, PASSED ON THE MERITS OR THE FAIRNESS OF THE TRANSACTION OR PASSED UPON THE ADEQUACY OR ACCURACY OF THE INFORMATION CONTAINED IN THIS DOCUMENT. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

This statement is filed in connection with (check the appropriate box):

|

|

|

|

|

| a. |

|

☒ |

|

The filing of solicitation materials or an information statement subject to Regulation 14A (§§ 240.14a-1 through 240.14b-2), Regulation

14C (§§ 240.14c-1 through 240.14c-101) or Rule 13e-3(c)

(§ 240.13e-3(c)) under the Securities Exchange Act of 1934 (the “Exchange Act”). |

|

|

|

| b. |

|

☐ |

|

The filing of a registration statement under the Securities Act of 1933. |

|

|

|

| c. |

|

☐ |

|

A tender offer. |

|

|

|

| d. |

|

☐ |

|

None of the above. |

Check the following box if the soliciting materials or information statement referred to in checking box (a) are

preliminary copies: ☒

Check the following box if the filing is a final amendment reporting the results of the transaction: ☐

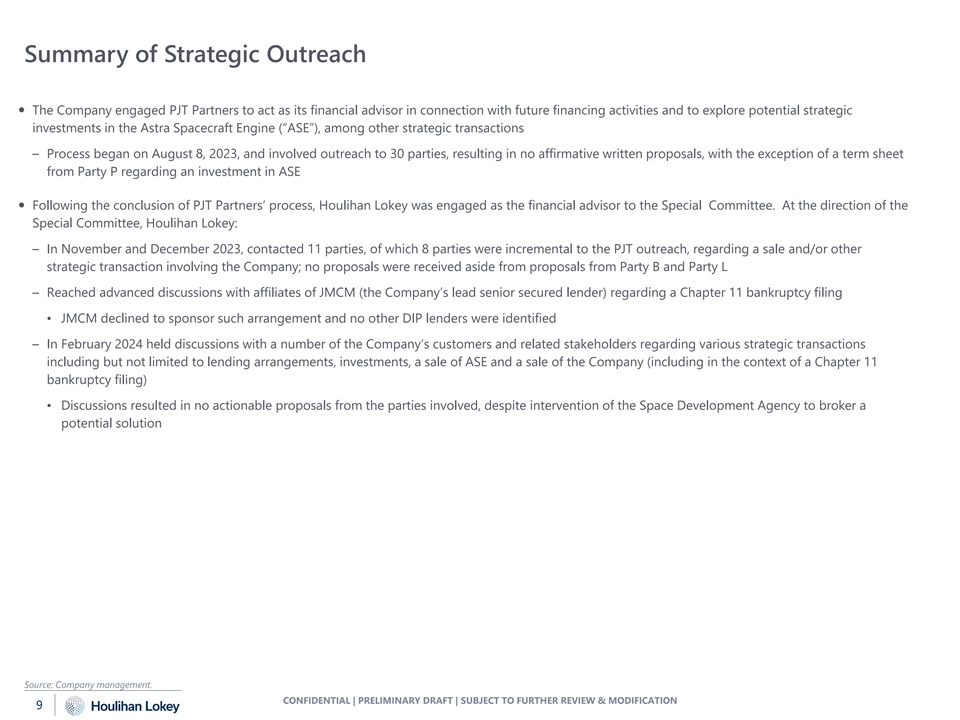

EXPLANATORY NOTE

This Amendment No. 2 to Rule 13e-3 Transaction Statement on Schedule 13E-3 (together with its exhibits, the “Transaction Statement”) amends

and restates the original Rule 13e-3 Transaction Statement on Schedule 13E-3 on April 8, 2024, as amended on May 8, 2024 (together with its exhibits, the “Original Transaction Statement”), specifically to (i) include additional disclosure

regarding the Kemp Trust pursuant to Item 3 of the Transaction Statement and (ii) include, as exhibit (c)(2), discussion materials prepared by PJT Partners LP and provided to the Board of Directors of Astra Space, Inc. and to include as exhibits

(c)(3) through (c)(7), unredacted discussion materials prepared by Houlihan Lokey Capital, Inc. and provided to the Special Committee of the Board of Directors of Astra Space, Inc. The discussion materials prepared by Houlihan Lokey Capital, Inc.,

dated December 19, 2023, filed as exhibit (c)(5), make mistaken reference to Pine Ridge in certain locations; all such references were intended to refer to JMCM Holdings LLC or an affiliate.

INTRODUCTION

This Transaction Statement is being filed with the Securities and Exchange Commission (the “SEC”) pursuant to Section 13(e) of the

Securities Exchange Act of 1934, as amended (the “Exchange Act”), by (a) Astra Space, Inc., a Delaware corporation (“Astra” or the “Company”), the issuer of the shares of Class A common

stock, par value $0.0001 per share (the “Class A Shares”), and Class B common stock, par value $0.0001 per share (the “Class B Shares” and, together with the Class A

Shares, the “Common Shares”), of Astra that are the subject of the Rule 13e-3 transaction; (b) Apogee Parent Inc., a Delaware corporation (“Parent”); (c) Apogee

Merger Sub Inc., a Delaware corporation (“Merger Sub”) (together with Parent and Merger Sub, the “Parent Entities”); (d) Chris C. Kemp (including the Kemp Trust), the Company’s chief executive officer, chairman

and a director; and (e) Adam P. London, the Company’s chief technology officer and a director. Collectively, the persons filing this Transaction Statement are referred to as the “filing persons.”

This Transaction Statement relates to the Agreement and Plan of Merger, dated March 7, 2024 (the “Merger Agreement”), by and among

Astra, Parent and Merger Sub. The Merger Agreement provides that Merger Sub will merge with and into Astra, with Astra continuing as the surviving corporation (the “Surviving Corporation”) and becoming a subsidiary of Parent (the

“Merger”). In connection with the Merger Agreement and pursuant to equity commitment letters with Parent and Merger Sub, dated March 7, 2024 (collectively, the “Equity Commitment Letters”), Chris Kemp, Adam

London, SherpaVentures Fund II, LP (“ACME Fund II”), Astera Institute, Eagle Creek Capital, LLC, JW 16 LLC, and RBH

Ventures Astra SPV, LLC (“RBH”, and collectively, the “Equity Commitment Parties” and each an “Equity Commitment Party”) have severally agreed

to provide equity financing to Parent in the amounts specified in their respective Equity Commitment Letters, for a total aggregate value of approximately $28.8 million, on the terms and subject to the conditions contained in the Equity

Commitment Letters. The Equity Commitment Parties’ commitments may be satisfied, in each of their sole discretion, by (i) a cash contribution to Parent, (ii) a contribution to Parent of Class A Shares held by such Equity

Commitment Party, or (iii) a combination of the foregoing. For purposes of determining the value of an Equity Commitment Party’s contribution pursuant to the foregoing clauses (ii) and (iii), each Class A Share contributed by an

Equity Commitment Party will be ascribed a value equal to the Merger Consideration (as defined in the Merger Agreement).

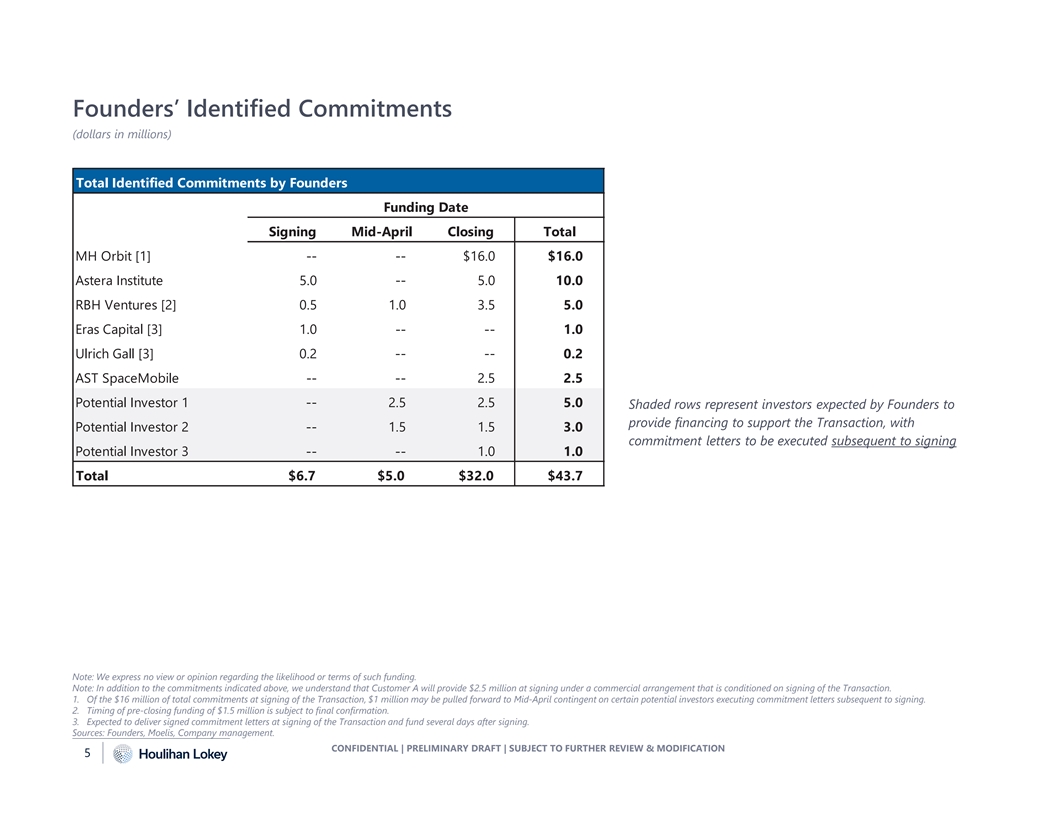

In addition, RBH has also agreed

in its Equity Commitment Letter to provide interim debt financing to the Company in the amount of $1.5 million, and MH Orbit, LLC (“MH Orbit”) may, pursuant to a debt commitment letter, dated March 7, 2024, provide debt

financing to the Company in the amount of $1.0 million, in each case, by no later than April 15, 2024, for the purposes of financing cash shortfalls at the Company during the period between the signing of the Merger Agreement and the

consummation of the Merger. On March 15, 2024, RBH purchased additional Company Convertible Notes and Company Warrants. As a result of these purchases, such interim debt financing commitment and equity commitment of RBH under its Equity

Commitment Letter was reduced by $991,000.00 and $1,044,658.75, respectively. On April 22, 2024, RBH purchased additional Company Convertible Notes, which purchase further reduced RBH’s interim debt financing commitment and equity commitment by

$400,000, respectively. MH Orbit has not made any additional purchases of Company Convertible Notes and Company Warrants as of the date hereof.

In

addition to the Equity Commitment Letters, pursuant to a debt commitment letter with Parent, dated March 6, 2024 (the “AST Debt Commitment Letter”), AST & Science, LLC (“AST”) has agreed to purchase

from Parent one or more notes in an aggregate principal amount of $2.5 million for a purchase price of 100% of the principal amount thereof, on the terms and subject to the conditions contained in the AST Debt Commitment Letter (including that

the Merger shall have closed substantially concurrent with such purchase).

Upon the consummation of the Merger, on the terms and subject to the

conditions set forth in the Merger Agreement, the following will occur: (i) each Class A Share and each Class B Share, that is owned by Astra as treasury shares and each Common Share that is owned by any direct or indirect wholly owned subsidiary of

Astra, or by Parent, Merger Sub, or any direct or indirect wholly owned subsidiary of Parent or Merger Sub, in each case, issued and outstanding immediately prior to the Effective Time, will automatically be canceled without payment of any

consideration therefor and cease to exist (the “Canceled Common Shares”); (ii) each Class A Share for which the holder thereof did not consent or vote in favor of the Merger Agreement and is entitled to and properly

demands appraisal pursuant to the DGCL, and does not withdraw or otherwise lose the right to appraisal pursuant to the DGCL (such Class A Shares, the “Dissenting Shares”) will automatically be cancelled; (iii) each (a) Class A Share

and (b) Class A Share subject to a restricted stock unit award held by an independent director of Astra that has fully vested as of the Effective Time, that is issued and outstanding immediately prior to the Effective Time and held by Parent or its

affiliates, including the Specified Stockholders (as defined below) and certain other holders of Class A Shares (the “Rollover Shares”), as of immediately prior to the Effective Time as a result of having been acquired by Parent or

its affiliates pursuant to a rollover agreement in a form mutually acceptable to Parent and the Company (each, a “Rollover Agreement”) or in connection with the funding of a capital commitment set forth in an Equity Commitment

Letter, will be canceled and cease to exist (the “Rollover”); provided that the Rollover will be permitted only if no Class B Shares are issued and outstanding; and (iv) each Class A Share that is issued and outstanding immediately

prior to the Effective Time (other than any Rollover Shares, Canceled Common Shares and Dissenting Shares), as of the Effective Time, will be converted into the right to receive an amount in cash equal to $0.50 per Class A Share, without interest.

Treatment of outstanding equity plan awards under Astra’s equity incentive plans and award agreements is described in greater detail in the Information Statement (defined below) under “The Merger Agreement—Consideration to be Received

in the Merger.” Further, following consummation of the Merger, the Class A Shares will cease to be listed on the Nasdaq Capital Market and registration of the Class A Shares under the Exchange Act will be terminated.

A special committee (the “Special Committee”) of the board of directors (the “Board”) of the Company consisting only of

independent and disinterested directors of the Company has unanimously determined that (i) the Merger Agreement and the transactions contemplated thereby (the “Transactions”), including the Merger, on the terms and subject to

the conditions set forth therein, are advisable, fair to and in the best interests of the Company and all of the holders of the issued and outstanding Common Shares, excluding Chris C. Kemp, the Kemp Trust and Dr. Adam P. London

(collectively, the “Specified Stockholders”) and their respective affiliates (excluding the Company and its subsidiaries) (the “Public Stockholders”) and (ii) recommended that the Board (a) approve the

Merger Agreement, the other transaction documents and the Transactions, including the Merger, including for purposes of Section 203 of the DGCL, and (b) recommend adoption and approval of the Merger Agreement and the Transactions, including the

Merger, to the Company’s stockholders. In addition, the Special Committee believes that the Merger is fair to the Company’s “unaffiliated security holders,” as such term is defined in Rule 13e-3 under the Exchange Act.

The Board (with Mr. Kemp, Dr. London and Scott Stanford, a director of the Company and an affiliate of ACME, LLC, abstaining from voting on the approval of

the Transactions, including the Merger), acting on the recommendation of the Special Committee (i) determined that the Merger Agreement and the Transactions, including the Merger, on the terms and subject to the conditions set forth therein,

are advisable, fair to and in the best interests of the Company and its stockholders, (ii) declared the Merger Agreement and the Transactions, including the Merger, advisable, (iii) approved the Merger Agreement, the execution and delivery

by the Company of the Merger Agreement, the performance by the Company of its covenants and agreements contained therein and the consummation of the Transactions, including the Merger, on the terms and subject to the conditions contained in the

Merger Agreement and (iv) resolved to recommend adoption and approval of the Merger Agreement and the Transactions, including the Merger, to the Company’s stockholders. In addition, the Board (excluding Mr. Kemp, Dr. London and

Mr. Stanford), on behalf of the Company, believes that the Merger is fair to the Company’s “unaffiliated security holders,” as such term is defined in Rule 13e-3 under the Exchange Act.

Concurrently with the filing of this Transaction Statement, Astra is filing a notice of written consent and

appraisal rights and information statement (the “Information Statement”) under Section 14(c) of the Exchange Act. A copy of the Information Statement is attached hereto as Exhibit (a)(1), and a copy of the Merger

Agreement is attached as Annex C to the Information Statement. In accordance with Section 228 and Section 251 of the DGCL, Astra’s Second Amended and Restated Certificate of Incorporation, dated June 30, 2021, as amended, and

Astra’s Amended and Restated Bylaws, dated June 30, 2021, the adoption of the Merger Agreement and the approval of the Merger and the other Transactions required the affirmative vote or written consent, by stockholders of Astra holding a

majority of the aggregate voting power of the outstanding Common Shares entitled to vote thereon, voting together as a single class (the “Required Stockholder Approval”). On March 7, 2024, Mr. Kemp and Dr. London, which on such

date beneficially owned a majority of the voting power of the issued and outstanding Common Shares, executed and delivered to the Company a written consent adopting the Merger Agreement and approving the Merger, (the “Written

Consent”), thereby providing the Required Stockholder Approval for the Merger.

Pursuant to General Instruction F to Schedule 13E-3, the information contained in the Information Statement, including all annexes thereto, is expressly incorporated herein by reference in its entirety, and responses to each item herein are qualified in their

entirety by the information contained in the Information Statement and the annexes thereto. The cross-references below are being supplied pursuant to General Instruction G to Schedule 13E-3 and show the

location in the Information Statement of the information required to be included in response to the items of Schedule 13E-3. As of the date hereof, the Information Statement is in preliminary form and is

subject to completion.

All information contained in this Transaction Statement concerning any of the filing persons has been provided by such filing

person and no filing person has produced any disclosure with respect to any other filing persons.

ITEM 1. SUMMARY TERM SHEET

The information set forth in the Information Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers about the

Merger”

ITEM 2. SUBJECT COMPANY INFORMATION

(a) Name and Address. The information set forth in the Information Statement under the following caption is

incorporated herein by reference:

“Summary — The

Parties to the Merger Agreement”

(b) Securities. The information set forth in the Information Statement under the following

captions is incorporated herein by reference:

“Summary”

“Questions and Answers about the Merger”

“Market

Information, Dividends and Certain Transactions in the Class A Shares”

(c) Trading Market and Price. The information set forth in the Information Statement under the

following caption is incorporated herein by reference:

“Market Information, Dividends and Certain Transactions in the Class A Shares”

(d) Dividends. The information set forth in the Information Statement under the following caption is incorporated herein by reference:

“Market Information, Dividends and Certain Transactions in the Class A Shares”

(e) Prior Public Offerings. The information set forth in the Information Statement under the following captions is incorporated herein by reference:

“Summary”

“The Special Factors –

Background of the Merger”

(f) Prior Stock Purchases. The information set forth in the Information Statement under the following caption is

incorporated herein by reference:

“Market Information, Dividends and Certain Transactions in the Class A Shares”

ITEM 3. IDENTITY AND BACKGROUND OF FILING PERSONS

(a)–(c) Name and Address; Business and Background of Entities; Business and Background of Natural Persons. The information set

forth in the Information Statement under the following captions is incorporated herein by reference:

“Summary”

“The Parties to the Merger Agreement”

“Directors,

Executive Officers and Controlling Persons of the Company”

“Where You Can Find More Information”

Additionally, with respect to the Kemp Trust, the name of the Kemp Trust is the Chris Kemp Living Trust dated February 10, 2021. The business address of the

Kemp Trust is 1900 Skyhawk Street, Alameda, CA, 94501. The telephone number of the Kemp Trust is (866) 278-7217. Mr. Kemp is the sole trustee and a beneficiary of the Kemp Trust. By virtue of this relationship, the Kemp Trust is an affiliate of the

Company, Parent, and Merger Sub. The Kemp Trust is primarily engaged in the business of investing in securities and is organized under the laws of the State of California, United States of America. During the last five years, the Kemp Trust has not

been convicted in a criminal proceeding (excluding traffic violations or similar misdemeanors) nor has it been party to a civil proceeding of a judicial or administrative body of competent jurisdiction and as a result of such proceeding was or is

subject to a judgment, decree or final order enjoining future violations of, or prohibiting or mandating activities subject to, federal or state securities laws or finding any violation with respect to such laws

ITEM 4. TERMS OF THE TRANSACTION

(a)(1)

Material Terms – Tender Offers. Not applicable.

(a)(2) Material Terms – Merger or Similar Transactions. The information set forth in

the Information Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers about the Merger”

“The

Special Factors – Background of the Merger”

“The Special Factors – Recommendation of the Special Committee; Reasons for the

Merger”

“The Special Factors – Recommendation of the Board; Reasons for the Merger”

“The Special Factors – Required Stockholder Approval for the Merger”

“The Special Factors – Opinion of Houlihan Lokey Capital, Inc. to the Special Committee”

“The Special Factors – Certain Company Financial Projections”

“The Special Factors – Position of the Company on the Fairness of the Merger”

“The Special Factors – Position of the Parent Entities in Connection with the Merger”

“The Special Factors – Purposes and Reasons of the Company in Connection with the Merger”

“The Special Factors – Purposes and Reasons of the Parent Entities in Connection with the Merger”

“The Special Factors – Interests of Our Directors and Executive Officers in the Merger”

“The Special Factors – Delisting and Deregistration of Class A Shares”

“The Special Factors – Material United States Federal Income Tax Consequences of the Merger”

“The Merger Agreement”

“Annex C: Agreement and

Plan of Merger”

“Annex D: Opinion of Houlihan Lokey Capital, Inc.”

(c) Different Terms. The information set forth in the Information Statement under the following

captions is incorporated herein by reference:

“Summary”

“Questions and Answers about the Merger”

“The

Special Factors – Interests of Our Directors and Executive Officers in the Merger”

“The Merger Agreement – Consideration to be

Received in the Merger”

(d) Appraisal Rights. The information set forth in the Information Statement under the following captions is

incorporated herein by reference:

“Summary – Appraisal Rights”

“Questions and Answers about the Merger”

“The

Merger Agreement – Dissenting Shares”

“Appraisal Rights”

“Annex F: Section 262 of the General Corporation Law of Delaware”

(e) Provisions for Unaffiliated Security Holders. The information set forth in the Information Statement under the following captions is incorporated

herein by reference:

“Provisions for Unaffiliated Stockholders”

(f) Eligibility for Listing or Trading. Not applicable.

ITEM 5. PAST CONTACTS, TRANSACTIONS, NEGOTIATIONS AND AGREEMENTS

(a) Transactions. The information set forth in the Information Statement under the following caption is incorporated herein by

reference:

“Market Information, Dividends and Certain Transactions in the Class A Shares”

(b)–(c) Significant Corporate Events; Negotiations or Contacts. The information set forth in the Information Statement under the following

captions is incorporated herein by reference:

“Summary”

“Questions and Answers about the Merger”

“The

Special Factors – Background of the Merger”

“The Special Factors – Recommendation of the Special Committee; Reasons for the

Merger”

“The Special Factors – Recommendation of the Board; Reasons for the Merger”

“The Special Factors – Required Stockholder Approval for the Merger”

“The Special Factors – Financing”

“The

Special Factors – Position of the Company on the Fairness of the Merger”

“The Special Factors – Position of the Parent Entities in

Connection with the Merger”

“The Special Factors – Purposes and Reasons of the Company in Connection with the Merger”

“The Special Factors – Purposes and Reasons of the Parent Entities in Connection with the Merger”

“The Special Factors – Interests of Our Directors and Executive Officers in the Merger”

“The Special Factors – Delisting and Deregistration of Class A Shares”

“The Special Factors – Fees and Expenses”

“The Merger Agreement – Form of Merger”

“The

Merger Agreement – Consummation and Effectiveness of the Merger”

“The Merger Agreement – Consideration to be Received in the

Merger”

“The Merger Agreement – Written Consent; Merger Sub Stockholder Consent”

“Market Information, Dividends and Certain Transactions in the Class A Shares”

“Annex C: Agreement and Plan of Merger”

(e)

Agreements Involving the Subject Company’s Securities. The information set forth in the Information Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers about the

Merger”

“The Special Factors – Background of the Merger”

“The Special Factors – Recommendation of the Special Committee; Reasons for the Merger”

“The Special Factors – Recommendation of the Board; Reasons for the Merger”

“The Special Factors – Required Stockholder Approval for the Merger”

“The Special Factors – Financing”

“The

Special Factors – Position of the Company on the Fairness of the Merger”

“The Special Factors – Position of the Parent Entities in

Connection with the Merger”

“The Special Factors – Purposes and Reasons of the Company in Connection with the Merger”

“The Special Factors – Purposes and Reasons of the Parent Entities in Connection with the Merger”

“The Special Factors – Interests of Our Directors and Executive Officers in the Merger”

“The Special Factors – Delisting and Deregistration of Class A Shares”

“The Special Factors – Fees and Expenses”

“The Merger Agreement – Form of Merger”

“The

Merger Agreement – Consummation and Effectiveness of the Merger”

“The Merger Agreement – Consideration to be Received in the

Merger”

“The Merger Agreement – Written Consent; Merger Sub Stockholder Consent”

“The Merger Agreement – Other Covenants and Agreements”

“Market Information, Dividends and Certain Transactions in the Class A Shares”

“Annex C: Agreement and Plan of Merger”

ITEM 6. PURPOSES OF THE TRANSACTION AND PLANS OR PROPOSALS

(b) Use of Securities Acquired. The information set forth in the Information Statement under the following captions is incorporated herein by

reference:

“Summary”

“Questions and Answers

about the Merger”

“The Special Factors – Delisting and Deregistration of Class A Shares”

“The Special Factors – Plans for the Company After the Merger”

“The Merger Agreement – Form of Merger”

“The

Merger Agreement – Consideration to be Received in the Merger”

(c)(1)–(8) Plans. The information set forth

in the Information Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers about the Merger”

“The

Special Factors – Background of the Merger”

“The Special Factors – Recommendation of the Special Committee; Reasons for the

Merger”

“The Special Factors – Recommendation of the Board; Reasons for the Merger”

“The Special Factors – Position of the Company on the Fairness of the Merger”

“The Special Factors – Position of the Parent Entities in Connection with the Merger”

“The Special Factors – Purposes and Reasons of the Company in Connection with the Merger”

“The Special Factors – Purposes and Reasons of the Parent Entities in Connection with the Merger”

“The Special Factors – Interests of Our Directors and Executive Officers in the Merger”

“The Special Factors – Other Arrangements”

“The Special Factors – Delisting and Deregistration of Class A Shares”

“The Special Factors – Plans for the Company After the Merger”

“The Special Factors – Fees and Expenses”

“The Merger Agreement”

“Annex C: Agreement and

Plan of Merger”

ITEM 7. PURPOSES, ALTERNATIVES, REASONS AND EFFECTS

(a) Purposes. The information set forth in the Information Statement under the following captions is incorporated herein by reference:

“Summary”

“The Special Factors – Background

of the Merger”

“The Special Factors – Recommendation of the Special Committee; Reasons for the Merger”

“The Special Factors – Recommendation of the Board; Reasons for the Merger”

“The Special Factors – Position of the Company on the Fairness of the Merger”

“The Special Factors – Position of the Parent Entities in Connection with the Merger”

“The Special Factors – Purposes and Reasons of the Company in Connection with the Merger”

“The Special Factors – Purposes and Reasons of the Parent Entities in Connection with the Merger”

“The Special Factors – Plans for the Company After the Merger”

(b) Alternatives. The information set forth in the Information Statement under the following captions is incorporated herein by reference:

“The Special Factors – Background of the Merger”

“The Special Factors – Recommendation of the Special Committee; Reasons for the Merger”

“The Special Factors – Recommendation of the Board; Reasons for the Merger”

“The Special Factors – Opinion of Houlihan Lokey Capital, Inc. to the Special Committee”

“The Special Factors – Purposes and Reasons of the Company in Connection with the Merger”

“The Special Factors – Alternatives to the Merger”

(c) Reasons. The information set forth in the Information Statement under the following captions is incorporated herein by reference:

“Summary”

“The Special Factors – Background

of the Merger”

“The Special Factors – Recommendation of the Special Committee; Reasons for the Merger”

“The Special Factors – Recommendation of the Board; Reasons for the Merger”

“The Special Factors – Position of the Company on the Fairness of the Merger”

“The Special Factors – Position of the Parent Entities in Connection with the Merger”

“The Special Factors – Purposes and Reasons of the Company in Connection with the Merger”

“The Special Factors – Purposes and Reasons of the Parent Entities in Connection with the Merger”

“The Special Factors – Alternatives to the Merger”

(d) Effects. The information set forth in the Information Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers about the

Merger”

“The Special Factors – Background of the Merger”

“The Special Factors – Recommendation of the Special Committee; Reasons for the Merger”

“The Special Factors – Recommendation of the Board; Reasons for the Merger”

“The Special Factors – Financing”

“The

Special Factors – Position of the Company on the Fairness of the Merger”

“The Special Factors – Purposes and Reasons of the Company in

Connection with the Merger”

“The Special Factors – Purposes and Reasons of the Parent Entities in Connection with the Merger”

“The Special Factors – Interests of Our Directors and Executive Officers in the Merger”

“The Special Factors – Delisting and Deregistration of Class A Shares”

“The Special Factors – Plans for the Company After the Merger”

“The Special Factors – Fees and Expenses”

“The Special Factors – Material United States Federal Income Tax Consequences of the Merger”

“The Merger Agreement – Form of Merger”

“The

Merger Agreement – Consummation and Effectiveness of the Merger”

“The Merger Agreement – Consideration to be Received in the

Merger”

“The Merger Agreement – Dissenting Shares”

“The Merger Agreement – Charter; Bylaws”

“The Merger Agreement – Indemnification and Insurance”

“Appraisal Rights”

“Annex C: Agreement and Plan

of Merger”

“Annex F: Section 262 of the Delaware General Corporation Law”

ITEM 8. FAIRNESS OF THE TRANSACTION

(a)–(b) Fairness; Factors Considered in Determining Fairness. The information set forth in the Information Statement under the following

captions is incorporated herein by reference:

“Summary”

“Questions and Answers about the Merger”

“The

Special Factors – Background of the Merger”

“The Special Factors – Recommendation of the Special Committee; Reasons for the

Merger”

“The Special Factors – Recommendation of the Board; Reasons for the Merger”

“The Special Factors – Opinion of Houlihan Lokey Capital, Inc. to the Special Committee”

“The Special Factors – Position of the Company on the Fairness of the Merger”

“The Special Factors – Position of the Parent Entities in Connection with the Merger”

“The Special Factors – Purposes and Reasons of the Company in Connection with the Merger”

“The Special Factors – Purposes and Reasons of the Parent Entities in Connection with the Merger”

“The Special Factors – Interests of Our Directors and Executive Officers in the Merger”

“Annex D: Opinion of Houlihan Lokey Capital, Inc.”

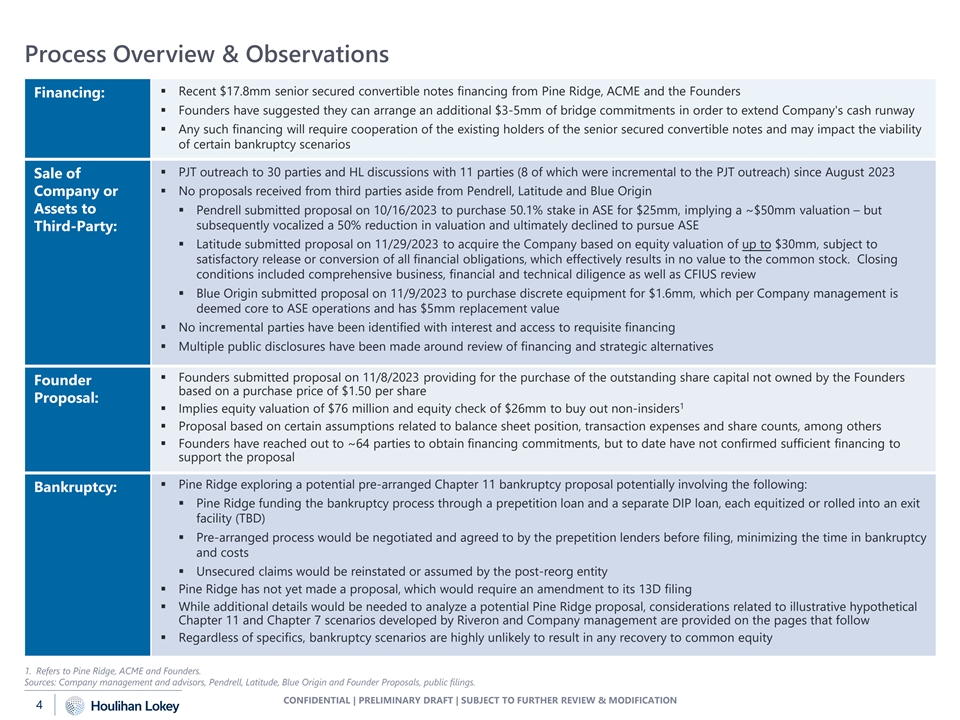

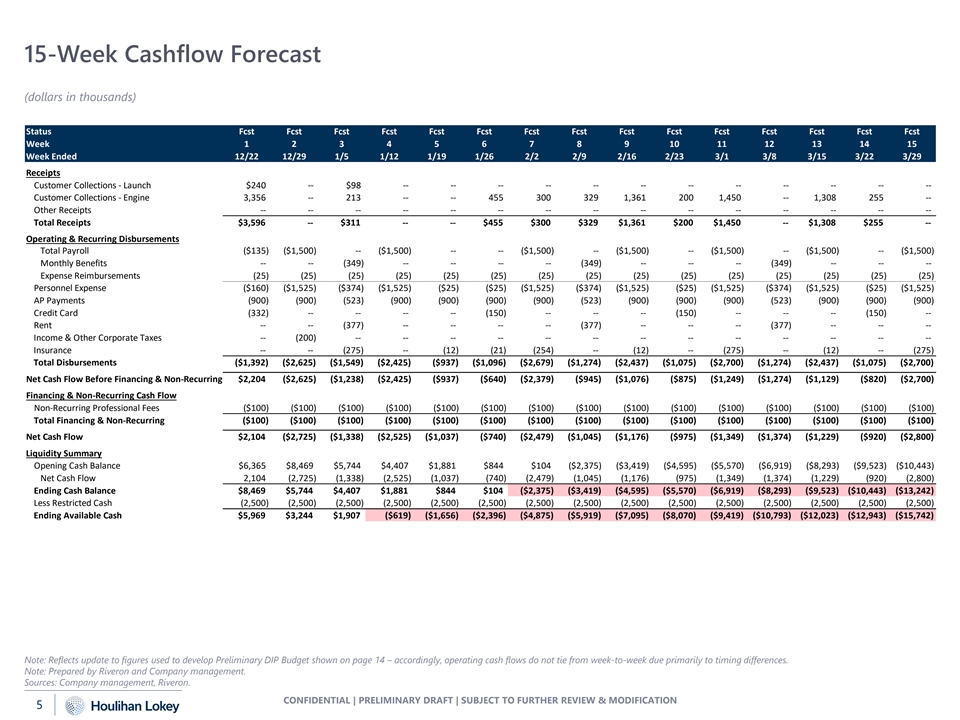

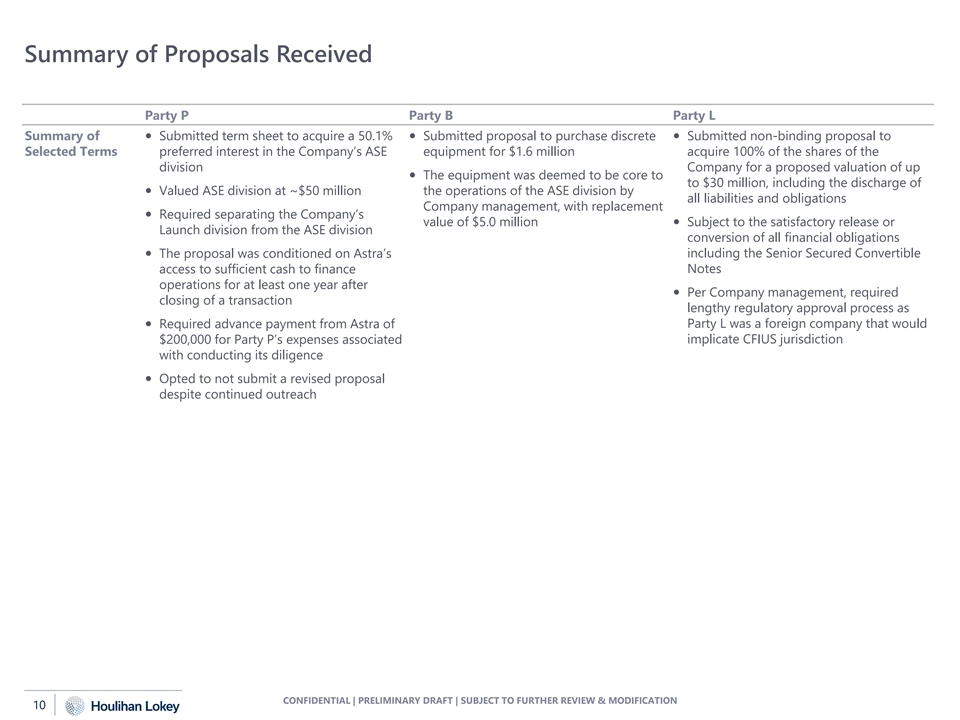

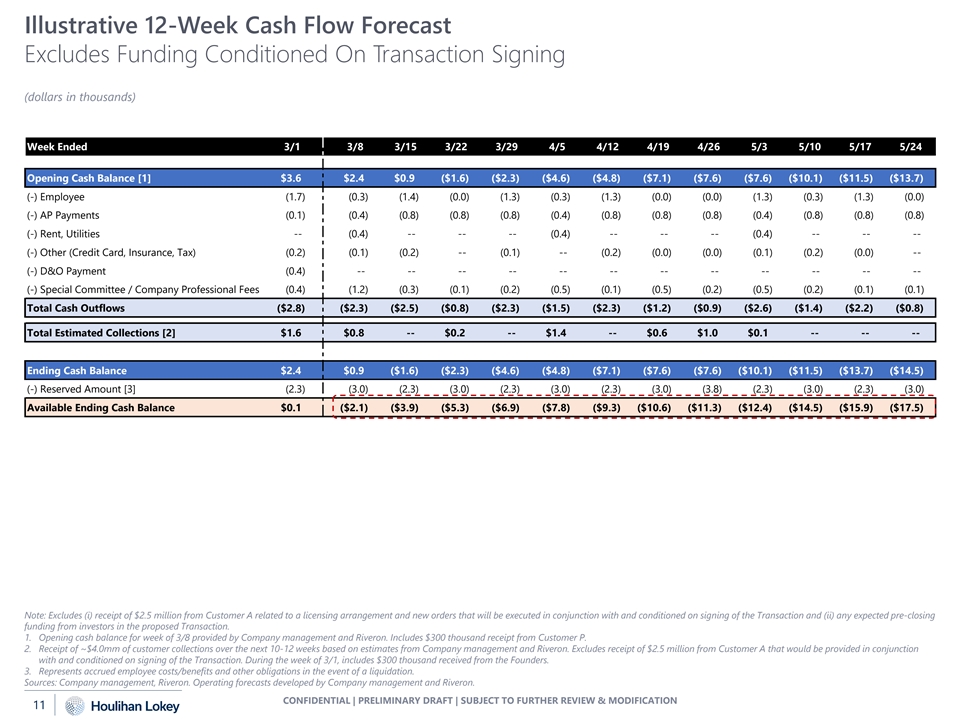

The confidential discussion materials prepared by Houlihan Lokey Capital, Inc. and provided to the Special Committee, dated November 16, 2023,

December 4, 2023, December 19, 2023, February 25, 2024, March 4, 2024 and March 5, 2024, are attached hereto as Exhibits (c)(3) through and including (c)(8).

(c) Approval of Security Holders. The information set forth in the Information Statement under the following captions is incorporated herein by

reference:

“Summary”

“Questions and Answers

about the Merger”

“The Special Factors – Background of the Merger”

“The Special Factors – Recommendation of the Special Committee; Reasons for the Merger”

“The Special Factors – Recommendation of the Board; Reasons for the Merger”

“The Special Factors – Required Stockholder Approval for the Merger”

“The Merger Agreement – Written Consent; Merger Sub Stockholder Consent”

“Annex C: Agreement and Plan of Merger”

(d)

Unaffiliated Representative. The Company did not retain an unaffiliated representative to act solely on behalf of the unaffiliated security holders for purposes of negotiating the transaction. The Special Committee, which consists

entirely of independent and disinterested directors, was formed for the purpose of exploring potential strategic alternatives including, without limitation, one or more potential financing transactions or a potential dissolution or winding up of the

Company and liquidation of our assets. The Special Committee retained (i) Freshfields Bruckhaus Deringer LLP as its legal advisor and (ii) Houlihan Lokey as its financial advisor, and Houlihan Lokey rendered an opinion to the Special Committee to

the effect that the Merger Consideration to be received by the Public Stockholders in the Merger, pursuant to the Merger Agreement, is fair to such stockholders, from a financial point of view. The Special Committee considered the Public

Stockholders to be situated substantially similarly to the Company’s “unaffiliated security holders,” as such term is defined in Rule 13e-3 under the Exchange Act, due to the fact that holders of Class A Shares who are officers or

directors of the Company, and who are included among the Public Stockholders but might be considered affiliates of the Company by virtue of such role, will receive the same per share Merger Consideration in respect of their Class A Shares as the

security holders unaffiliated with the Company will receive in respect of their Class A Shares.

(e) Approval of Directors. The

information set forth in the Information Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers about the Merger”

“The

Special Factors – Background of the Merger”

“The Special Factors – Recommendation of the Special Committee; Reasons for the

Merger”

“The Special Factors – Recommendation of the Board; Reasons for the Merger”

“The Special Factors – Position of the Company on the Fairness of the Merger”

“The Special Factors – Position of the Parent Entities in Connection with the Merger”

(f) Other Offers. The information set forth in the Information Statement under the following captions is incorporated by reference:

“Summary”

“The Special Factors – Background

of the Merger”

“The Special Factors – Recommendation of the Special Committee; Reasons for the Merger”

“The Special Factors – Recommendation of the Board; Reasons for the Merger”

“The Special Factors – Position of the Company on the Fairness of the Merger”

“The Special Factors – Position of the Parent Entities in Connection with the Merger”

“The Merger Agreement – No Solicitation; Superior Proposal and Adverse Recommendation Change”

ITEM 9. REPORTS, OPINIONS, APPRAISALS AND NEGOTIATIONS

(a)–(c) Report, Opinion or Appraisal; Preparer and Summary of the Report, Opinion or Appraisal; Availability of Documents. The information set

forth in the Information Statement under the following captions is incorporated herein by reference:

“Summary”

“The Special Factors – Background of the Merger”

“The Special Factors – Recommendation of the Special Committee; Reasons for the Merger”

“The Special Factors – Recommendation of the Board; Reasons for the Merger”

“The Special Factors – Opinion of Houlihan Lokey Capital, Inc. to the Special Committee”

“The Special Factors – Certain Company Financial Projections”

“The Special Factors – Position of the Company on the Fairness of the Merger”

“The Special Factors – Position of the Parent Entities in Connection with the Merger”

“Annex D: Opinion of Houlihan Lokey Capital, Inc.”

The discussion materials prepared by PJT Partners LP and provided to the Board, dated August 23, 2023 are attached hereto as Exhibit (c)(2).

The discussion materials prepared by Houlihan Lokey Capital, Inc. and provided to the Special Committee, dated November 16, 2023, December 4, 2023,

December 19, 2023, February 25, 2024, March 4, 2024 and March 5, 2024, are attached hereto as Exhibits (c)(3) through and including (c)(8).

The reports, opinions or appraisals referenced in this Item 9 are filed herewith or incorporated by reference herein and will be made available for inspection

and copying at the principal executive offices of Astra during its regular business hours by any interested holder of Common Stock or representative who has been designated in writing, and copies may be obtained by requesting them in writing from

Astra at the email address provided under the caption “Where You Can Find More Information” in the Information Statement, which is incorporated herein by reference.

ITEM 10. SOURCE AND AMOUNTS OF FUNDS OR OTHER CONSIDERATION

(a)–(b) Source of Funds; Conditions. The information set forth in the Information Statement under the following captions is incorporated

herein by reference:

“Summary”

“Questions

and Answers about the Merger”

“The Special Factors – Financing”

“The Special Factors – Position of the Parent Entities in Connection with the Merger”

“The Merger Agreement – Consummation and Effectiveness of the Merger”

“The Merger Agreement – Financing of the Merger”

“Annex C –Agreement and Plan of Merger”

(c)

Expenses. The information set forth in the Information Statement under the following caption is incorporated herein by reference:

“The

Special Factors – Fees and Expenses”

(d) Borrowed Funds. Not applicable.

ITEM 11. INTEREST IN SECURITIES OF THE SUBJECT COMPANY

(a) Securities Ownership. The information set forth in the Information Statement under the following caption is incorporated herein by reference:

“Directors, Executive Officers and Controlling Persons of the Company”

“Security Ownership of Certain Beneficial Owners and Management”

(b) Securities Transactions. The information set forth in the Information Statement under the

following captions is incorporated herein by reference:

“The Special Factors – Background of the Merger”

“The Special Factors – Financing”

“The

Special Factors – Interests of Our Directors and Executive Officers in the Merger”

“The Merger Agreement”

“Market Information, Dividends and Certain Transactions in the Class A Shares”

“Annex C: Agreement and Plan of Merger”

ITEM 12. THE SOLICITATION OR RECOMMENDATION

(d)

Intent to Tender or Vote in a Going-Private Transaction. Mr. Kemp and Dr. London have voted in favor of the Merger by written consent on March 7, 2024, which votes were sufficient to approve the Merger Agreement and the consummation of the

Merger on behalf of the Stockholders. No other vote is required. Certain Class A Shares held by Mr. Kemp and Dr. London may be sold to cover transaction expenses in connection with the Merger. Such Class A Shares would not be included in any

Rollover Agreements entered into by Mr. Kemp and Dr. London in favor of the Parent. To the Company’s knowledge, no other officer or director intends to sell any Class A Shares owned by him or her prior to the consummation of the Merger.

(e) Recommendations of Others. Not applicable.

ITEM 13. FINANCIAL STATEMENTS

(a)

Financial Statements. The (a) audited financial statements of the Company for the fiscal years ended December 31, 2023 and 2022 and the related notes thereto which were included in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2023, filed with the SEC on April 18, 2024, and (b) unaudited condensed consolidated financial statements of the Company for the quarterly period ended March 31, 2024

and the related notes thereto, which were included in the Company’s Quarterly Report on Form 10-Q filed with the SEC on May 29, 2024, are each incorporated by reference herein. The information set forth in the Information Statement under the

following caption is incorporated herein by reference:

“Market Information, Dividends and Certain Transactions in the Class A Shares”

“Where You Can Find More Information”

(b) Pro

Forma Information. Not applicable.

ITEM 14. PERSONS/ASSETS, RETAINED, EMPLOYED, COMPENSATED OR USED

(a) Solicitations or Recommendations. Not applicable.

(b) Employees and Corporate Assets. The information set forth in the Information Statement under the following captions is incorporated herein by

reference:

“Summary”

“Questions and Answers

about the Merger”

“The Special Factors – Background of the Merger”

“The Special Factors – Recommendation of the Special Committee; Reasons for the Merger”

“The Special Factors – Recommendation of the Board; Reasons for the Merger”

“The Special Factors – Opinion of Houlihan Lokey Capital, Inc. to the Special Committee”

“The Special Factors – Interests of Our Directors and Executive Officers in the Merger”

“The Special Factors – Special Committee Compensation”

“The Special Factors – Other Interests”

“The

Special Factors – Fees and Expenses”

ITEM 15. ADDITIONAL INFORMATION

(b) Golden Parachute Compensation. The information set forth in the Information Statement under the following caption is incorporated herein by

reference:

“The Special Factors – Interests of Our Directors and Executive Officers in the Merger”

“The Special Factors – Severance Entitlements”

(c) Other Material Information. The information set forth in the Information Statement, including all annexes thereto, is incorporated herein by

reference.

ITEM 16. EXHIBITS

|

|

|

| Exhibit

No. |

|

Description |

|

|

| (a)(1) |

|

Preliminary Information Statement of Astra Space, Inc. incorporated herein by reference to the Information

Statement. |

|

|

| (c)(1) |

|

Opinion of Houlihan Lokey Capital, Inc. to the Special Committee to the Special Committee

of the Board of Directors of Astra Space, Inc. dated March 5, 2024, incorporated herein by reference to Annex D to the Information Statement. |

|

|

| (c)(2)* |

|

Discussion materials prepared by PJT Partners LP., dated August 23, 2023, for the Board of Directors of Astra Space, Inc. |

|

|

| (c)(3)* |

|

Discussion materials prepared by Houlihan Lokey Capital, Inc., dated November 16, 2023, for the Special Committee of the Board of Directors of Astra Space, Inc. |

|

|

| (c)(4)* |

|

Discussion materials prepared by Houlihan Lokey Capital, Inc., dated December 4, 2023, for the Special Committee of the Board of Directors of Astra Space, Inc. |

|

|

| (c)(5)* |

|

Discussion materials prepared by Houlihan Lokey Capital, Inc., dated December 19, 2023, for the Special Committee of the Board of Directors of Astra Space, Inc. |

|

|

| (c)(6)* |

|

Discussion materials prepared by Houlihan Lokey Capital, Inc., dated February 25, 2024, for the Special Committee of the Board of Directors of Astra Space, Inc. |

|

|

| (c)(7)* |

|

Discussion materials prepared by Houlihan Lokey Capital, Inc., dated March 4, 2024, for the Special Committee of the Board of Directors of Astra Space, Inc. |

|

|

| (c)(8)* |

|

Discussion materials prepared by Houlihan Lokey Capital, Inc., dated March 5, 2024, for the Special Committee of the Board of Directors of Astra Space, Inc. |

|

|

| (d)(1) |

|

Agreement and Plan of Merger, dated as of March

7, 2024, by and among Astra Space, Inc., Apogee Parent Inc. and Apogee Merger Sub Inc. (incorporated by reference to Exhibit 2.1 of the Issuer’s Form 8-K filed with the Commission on March 12,

2024). |

|

|

| (d)(2) |

|

Limited Waiver and Consent to Senior Secured Convertible Notes and Common Stock Purchase Warrant and Reaffirmation of Transaction Documents,

dated as of March 7, 2024, by and among Astra Space, Inc., each of the subsidiaries of Astra Space, Inc. party thereto and each of the investors party thereto (incorporated by reference to Exhibit 10.1 of the Issuer’s Form 8-K filed with the Commission on March 12, 2024). |

|

|

| (d)(3) |

|

Interim Investors’ Agreement, dated as of March

7, 2024, by and among Apogee Parent Inc., Apogee Merger Sub Inc., Chris C. Kemp, Adam London, MH Orbit LLC, JMCM Holdings LLC, JW 16 LLC, SherpaVentures Fund II, LP, and the other parties appearing on the signature pages thereto (incorporated by reference

to Exhibit 99.13 of Adam London’s Schedule 13D/A filed on March 11, 2024). |

|

|

| (d)(4) |

|

Equity Commitment Letter by and between the Issuer and Chris C. Kemp, dated March

7, 2024 (incorporated by reference to Exhibit 99.14 of Chris C. Kemp’s Schedule 13D/A filed on March 11, 2024). |

|

|

| (d)(5) |

|

Equity Commitment Letter by and between the Issuer and Adam London, dated March

7, 2024 (incorporated by reference to Exhibit 99.10 of Adam London’s Schedule 13D/A filed on March 11, 2024). |

|

|

| (d)(6) |

|

Warrant Exchange Agreement, dated March

7, 2024 (incorporated by reference to Exhibit 99.11 of Adam London’s Schedule 13D/A filed on March 11, 2024). |

|

|

| (d)(7) |

|

Noteholder Conversion Agreement, dated March

7, 2024 (incorporated by reference to Exhibit 99.12 of Adam London’s Schedule 13D/A filed on March 11, 2024). |

|

|

| (d)(8) |

|

Form of 12% Senior Secured Convertible Note due 2025 (incorporated by reference to Exhibit 4.1 to the Issuer’s Form 8-K filed with the Commission on May 1, 2024). |

|

|

| (d)(9) |

|

Exclusivity Agreement (incorporated by reference to Exhibit 99.7 of Adam London’s Schedule 13D/A filed on February 26, 2024).

|

|

|

| (d)(10) |

|

Letter to the Special Committee of the Board of Directors of Astra Space, Inc., dated February

24, 2024 (incorporated by reference to Exhibit 99.8 of Adam London’s Schedule 13D/A filed on February 26, 2024). |

|

|

|

| (d)(11) |

|

Form of Warrant (incorporated by reference to Exhibit 4.2 to the Issuer’s Form 8-K filed with the

Commission on November 24, 2023). |

|

|

| (d)(12) |

|

Omnibus Amendment No. 3 Agreement dated as of November 21, 2023 (incorporated by reference to Exhibit 10.1 to the Issuer’s Form 8-K filed with the Commission on November 24, 2023). |

|

|

| (d)(13) |

|

Amendment to Securities Purchase Agreement, dated January 19, 2024, by and among Astra Space, Inc., each of the subsidiaries of Astra Space,

Inc. party thereto, the Investors and GLAS Americas LLC, which Securities Purchase Agreement was amended and restated as an exhibit to exhibit (d)(12) (incorporated by reference to Exhibit 10.1 of the Issuer’s current report on Form 8-K filed

with the Commission on January 25, 2024). |

|

|

| (d)(14) |

|

Agreement regarding Omnibus Amendment No. 3 Agreement, dated as of January 22, 2024, between Astra Space, Inc., its subsidiaries and the Investors

(incorporated by reference to Exhibit 10.29 of the Issuer’s annual report on Form 10-K filed with the Commission on April 18, 2024). |

|

|

| (d)(15) |

|

Amendment to Senior Secured Convertible Notes, dated as of January 31, 2024, by and among Astra Space, Inc. and the Holders (incorporated by

reference to Exhibit 10.1 of the Issuer’s current report on Form 8-K filed with the Commission on February 6, 2024). |

|

|

| (d)(16) |

|

Second Amendment to Securities Purchase Agreement and Second Amendment to Senior Secured Convertible Notes, dated February 26, 2024, by and among

Astra Space, Inc., each of the subsidiaries of Astra Space, Inc. party thereto, the Investors and GLAS Americas LLC (incorporated by reference to Exhibit 10.1 of the Issuer’s current report on Form 8-K filed with the Commission on March 1,

2024). |

|

|

| (d)(17) |

|

Third Amendment to Securities Purchase Agreement and Third Amendment to Senior Secured Convertible Notes, dated April 10, 2024, by and among

Astra Space, Inc., each of the subsidiaries of Astra Space, Inc. party thereto, the investors party thereto and GLAS Americas LLC (incorporated by reference to Exhibit 10.1 of the Issuer’s current report on Form 8-K filed with the Commission

on April 15, 2024). |

|

|

| (d)(18) |

|

Fourth Amendment to Senior Secured Convertible Notes, dated April 30, 2024, by and among Astra Space, Inc., its subsidiaries and the Holders

(incorporated by reference to Exhibit 10.1 of the Issuer’s current report on Form 8-K filed with the Commission on May 1, 2024). |

|

|

| (d)(19) |

|

Letter to the Special Committee of the Board of Directors of Astra Space, Inc., dated November

8, 2023 (incorporated by reference to Exhibit 99.3 of Adam London’s Schedule 13D/A filed on November 9, 2023). |

|

|

| (f)(1) |

|

Section

262 of the Delaware General Corporation Law, incorporated herein by reference to Annex F to the Information Statement. |

|

|

| 107** |

|

Filing Fee Table |

| ** |

Previously filed with the Schedule 13E-3 filed with the SEC on April 8, 2024 |

SIGNATURES

After due inquiry and to the best of each of the undersigned’s knowledge and belief, each of the undersigned certifies that the information set forth in

this statement is true, complete and correct.

Dated as of June 4, 2024.

|

| ASTRA SPACE, INC. |

|

| By: /s/ Axel Martinez |

| Name: Axel Martinez |

| Title: Chief Financial Officer |

|

| Apogee Parent Inc. |

|

| By: /s/ Chris C. Kemp |

| Name: Chris C. Kemp |

| Title: Chief Executive Officer |

|

| Apogee Merger Sub Inc. |

|

| By: /s/ Chris C. Kemp |

| Name: Chris C. Kemp |

| Title: Chief Executive Officer |

|

| Chris C. Kemp |

|

| By: /s/ Chris C. Kemp |

| Name: Chris C. Kemp |

|

| Chris C. Kemp, Trustee of the Chris Kemp Living Trust |

| dated February 10, 2021 |

|

| By: /s/ Chris C. Kemp |

| Name: Chris C. Kemp |

| Title: Trustee |

|

| Adam P. London |

|

| By: /s/ Adam P. London |

| Name: Adam P. London |

EXHIBIT (c)(2) August 23, 2023 Project Star DISCUSSION MATERIALS

CONFIDENTIAL

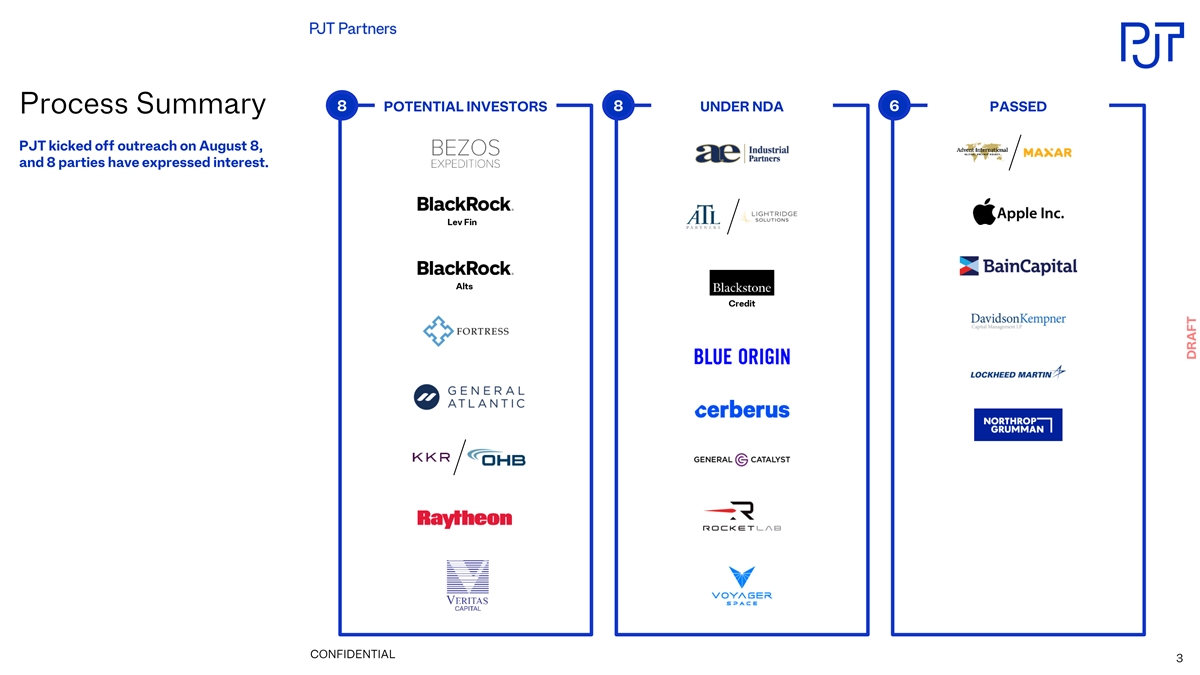

I. Investor Outreach Log CONFIDENTIAL 2

8 POTENTIAL INVESTORS 8 UNDER NDA 6 PASSED Process Summary PJT kicked off

outreach on August 8, and 8 parties have expressed interest. Lev Fin Alts Credit CONFIDENTIAL 3

II. Illustrative Strategic Alternatives for Astra CONFIDENTIAL

4

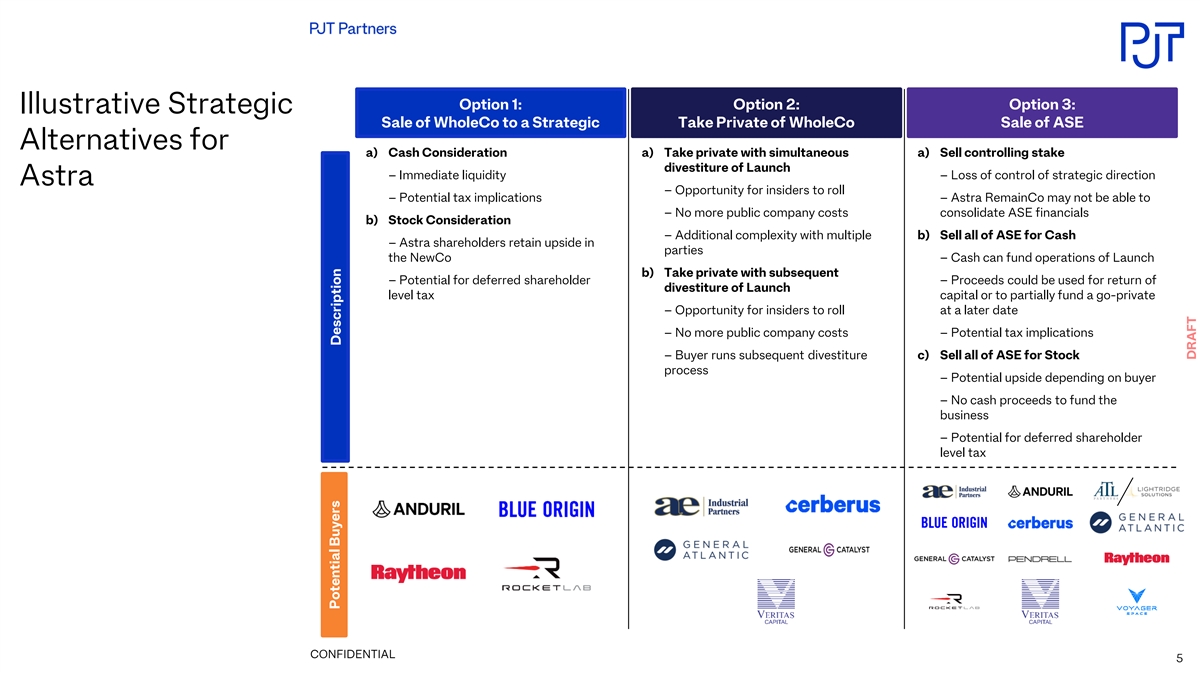

Option 1: Option 2: Option 3: Illustrative Strategic Sale of WholeCo to a

Strategic Take Private of WholeCo Sale of ASE Alternatives for a) Cash Consideration a) Take private with simultaneous a) Sell controlling stake divestiture of Launch – Immediate liquidity – Loss of control of strategic direction Astra

– Opportunity for insiders to roll – Potential tax implications – Astra RemainCo may not be able to – No more public company costs consolidate ASE financials b) Stock Consideration – Additional complexity with multiple

b) Sell all of ASE for Cash – Astra shareholders retain upside in parties the NewCo – Cash can fund operations of Launch b) Take private with subsequent – Potential for deferred shareholder – Proceeds could be used for return

of divestiture of Launch level tax capital or to partially fund a go-private – Opportunity for insiders to roll at a later date – No more public company costs – Potential tax implications – Buyer runs subsequent divestiture

c) Sell all of ASE for Stock process – Potential upside depending on buyer – No cash proceeds to fund the business – Potential for deferred shareholder level tax CONFIDENTIAL 5 Potential Buyers Description

This document contains highly confidential information and is solely for

obtained from third parties, including ratings from credit ratings agencies such informational purposes. You should not rely upon it or use it to form the as Standard & Poor’s. Reproduction and distribution of third party content in

Disclaimer definitive basis for any decision or action whatsoever, with respect to any any form is prohibited except with the prior written permission of the related proposed transaction or otherwise. You and your affiliates and agents must hold

third party. Third party content providers do not guarantee the accuracy, this document and any oral information provided in connection with this completeness, timeliness or availability of any information, including ratings, document, as well as

any information derived by you from the information and are not responsible for any errors or omissions (negligent or otherwise), contained herein, in strict confidence and may not communicate, reproduce or regardless of the cause, or for the

results obtained from the use of such disclose it to any other person, or refer to it publicly, in whole or in part at any content. THIRD PARTY CONTENT PROVIDERS GIVE NO EXPRESS OR time except with our prior written consent. If you are not the

intended recipient IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY of this document, please delete and destroy all copies immediately. WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE. THIRD PARTY CONTENT PROVIDERS

SHALL NOT BE This document is “as is” and is based, in part, on information obtained from LIABLE FOR ANY DIRECT, INDIRECT, INCIDENTAL, EXEMPLARY, other sources. We have assumed and relied upon the accuracy and COMPENSATORY, PUNITIVE,

SPECIAL OR CONSEQUENTIAL DAMAGES, completeness of such information for purposes of this document and have not COSTS, EXPENSES, LEGAL FEES, OR LOSSES (INCLUDING LOST INCOME independently verified any such information. Neither we nor any of our

affiliates OR PROFITS AND OPPORTUNITY COSTS OR LOSSES CAUSED BY or agents, makes any representation or warranty, express or implied, in relation NEGLIGENCE) IN CONNECTION WITH ANY USE OF THEIR CONTENT, to the accuracy or completeness of the

information contained in this document INCLUDING RATINGS. Credit ratings are statements of opinions and are not or any oral information provided in connection herewith, or any data it generates statements of fact or recommendations to purchase, hold

or sell securities. and expressly disclaim any and all liability (whether direct or indirect, in They do not address the suitability of securities or the suitability of securities for contract, tort or otherwise) in relation to any of such

information or any errors investment purposes, and should not be relied on as investment advice.” or omissions therein. Any views or terms contained herein are preliminary, and are based on financial, economic, market and other conditions

prevailing as of This document may include information from SNL Financial LC. Such the date of this document and are subject to change. We undertake no information is subject to the following: “CONTAINS COPYRIGHTED AND obligations or

responsibility to update any of the information contained in this TRADE SECRET MATERIAL DISTRIBUTED UNDER LICENSE FROM SNL. document. Past performance does not guarantee or predict future FOR RECIPIENT’S INTERNAL USE ONLY.” performance.

PJT Partners LP (“PJT Partners”) is a SEC registered broker-dealer and is a This document does not constitute an offer to sell or the solicitation of an offer member of FINRA and SIPC. PJT Partners is represented in the United to buy any

security, nor does it constitute an offer or commitment to lend, Kingdom by PJT Partners (UK) Limited. PJT Partners (UK) Limited is syndicate or arrange a financing, underwrite or purchase or act as an agent or authorised and regulated by the

Financial Conduct Authority (Ref No. 678983) advisor or in any other capacity with respect to any transaction, or commit and is a Company registered in England and Wales (No. 9424559). PJT capital, or to participate in any trading strategies, and

does not constitute legal, Partners is represented in Spain by PJT Partners Park Hill (Spain) A.V., S.A.U., a regulatory, accounting or tax advice to the recipient. This document does not firm authorized and regulated by the Comision Nacional del

Mercado de Valores constitute and should not be considered as any form of financial opinion or (“CNMV”). PJT Partners is represented in Hong Kong by PJT Partners (HK) recommendation by us or any of our affiliates. This document is not a

research Limited, authorised and regulated by the Securities and Futures Commission. In report nor should it be construed as such. connection with our capital raising services in Canada, PJT Partners relies on the international dealer exemption

pursuant to subsection 8.18(2) of National This document may include information from the S&P Capital IQ Platform Instrument 31-103 Registration Requirements. Please see Service. Such information is subject to the following: “Copyright

© 2023, S&P https://pjtpartners.com/regulatory-disclosure for more information. Capital IQ (and its affiliates, as applicable). This may contain information Copyright © 2023, PJT Partners LP (and its affiliates, as applicable).

CONFIDENTIAL 6

Exhibit (c)(3) November 2023 Project Star Buyer Outreach Update Strictly

Confidential. Not for Distribution.

Disclaimer ¡ This presentation, and any supplemental information

(written or oral) or other documents provided in connection therewith (collectively, the “materials”), are provided solely for the information of the Special Committee (the “Committee”) of the Board of Directors (the

“Board”) of Astra Space, Inc. (the “Company”) by Houlihan Lokey in connection with the Committee’s consideration of a potential transaction (the “Transaction”) involving the Company. This presentation is

incomplete without reference to, and should be considered in conjunction with, any supplemental information provided by and discussions with Houlihan Lokey in connection therewith. Any defined terms used herein shall have the meanings set forth

herein, even if such defined terms have been given different meanings elsewhere in the materials. ¡ The materials are for discussion purposes only. Houlihan Lokey expressly disclaims any and all liability, whether direct or indirect, in

contract or tort or otherwise, to any person in connection with the materials. The materials were prepared for specific persons familiar with the business and affairs of the Company for use in a specific context and were not prepared with a view to

public disclosure or to conform with any disclosure standards under any state, federal or international securities laws or other laws, rules or regulations, and none of the Committee, the Company or Houlihan Lokey takes any responsibility for the

use of the materials by persons other than the Committee. The materials are provided on a confidential basis solely for the information of the Committee and may not be disclosed, summarized, reproduced, disseminated or quoted or otherwise referred

to, in whole or in part, without Houlihan Lokey’s express prior written consent. ¡ Notwithstanding any other provision herein, the Company (and each employee, representative or other agent of the Company) may disclose to any and all

persons without limitation of any kind, the tax treatment and tax structure of any transaction and all materials of any kind (including opinions or other tax analyses, if any) that are provided to the Company relating to such tax treatment and

structure. However, any information relating to the tax treatment and tax structure shall remain confidential (and the foregoing sentence shall not apply) to the extent necessary to enable any person to comply with securities laws. For this purpose,

the tax treatment of a transaction is the purported or claimed U.S. income or franchise tax treatment of the transaction and the tax structure of a transaction is any fact that may be relevant to understanding the purported or claimed U.S. income or

franchise tax treatment of the transaction. If the Company plans to disclose information pursuant to the first sentence of this paragraph, the Company shall inform those to whom it discloses any such information that they may not rely upon such

information for any purpose without Houlihan Lokey’s prior written consent. Houlihan Lokey is not an expert on, and nothing contained in the materials should be construed as advice with regard to, legal, accounting, regulatory, insurance, tax

or other specialist matters. Houlihan Lokey’s role in reviewing any information was limited solely to performing such a review as it deemed necessary to support its own advice and analysis and was not on behalf of the Committee. ¡ The

materials necessarily are based on financial, economic, market and other conditions as in effect on, and the information available to Houlihan Lokey as of, the date of the materials. Although subsequent developments may affect the contents of the

materials, Houlihan Lokey has not undertaken, and is under no obligation, to update, revise or reaffirm the materials. The materials are not intended to provide the sole basis for evaluation of the Transaction and do not purport to contain all

information that may be required. The materials do not address the underlying business decision of the Company or any other party to proceed with or effect the Transaction, or the relative merits of the Transaction as compared to any alternative

business strategies or transactions that might be available for the Company or any other party. The materials do not constitute any opinion, nor do the materials constitute a recommendation to the Board, the Committee, the Company, any security

holder of the Company or any other party as to how to vote or act with respect to any matter relating to the Transaction or otherwise or whether to buy or sell any assets or securities of any company. Houlihan Lokey’s only opinion is the

opinion, if any, that is actually delivered to the Committee. In preparing the materials Houlihan Lokey has acted as an independent contractor and nothing in the materials is intended to create or shall be construed as creating a fiduciary or other

relationship between Houlihan Lokey and any party. The materials may not reflect information known to other professionals in other business areas of Houlihan Lokey and its affiliates. ¡ The preparation of the materials was a complex process

involving quantitative and qualitative judgments and determinations with respect to the financial, comparative and other analytic methods employed and the adaption and application of these methods to the unique facts and circumstances presented and,

therefore, is not readily susceptible to partial analysis or summary description. Furthermore, Houlihan Lokey did not attribute any particular weight to any analysis or factor considered by it, but rather made qualitative judgments as to the

significance and relevance of each analysis and factor. Each analytical technique has inherent strengths and weaknesses, and the nature of the available information may further affect the value of particular techniques. Accordingly, the analyses

contained in the materials must be considered as a whole. Selecting portions of the analyses, analytic methods and factors without considering all analyses and factors could create a misleading or incomplete view. The materials reflect judgments and

assumptions with regard to industry performance, general business, economic, regulatory, market and financial conditions and other matters, many of which are beyond the control of the participants in the Transaction. Any estimates of value contained

in the materials are not necessarily indicative of actual value or predictive of future results or values, which may be significantly more or less favorable. Any analyses relating to the value of assets, businesses or securities do not purport to be

appraisals or to reflect the prices at which any assets, businesses or securities may actually be sold. The materials do not constitute a valuation opinion or credit rating. The materials do not address the consideration to be paid or received in,

the terms of any arrangements, understandings, agreements or documents related to, or the form, structure or any other portion or aspect of, the Transaction or otherwise. Furthermore, the materials do not address the fairness of any portion or

aspect of the Transaction to any party. In preparing the materials, Houlihan Lokey has not conducted any physical inspection or independent appraisal or evaluation of any of the assets, properties or liabilities (contingent or otherwise) of the

Company or any other party and has no obligation to evaluate the solvency of the Company or any other party under any law. 2

Disclaimer (cont.) ¡ All budgets, projections, estimates, financial

analyses, reports and other information with respect to operations (including, without limitation, estimates of potential cost savings and synergies) reflected in the materials have been prepared by management of the relevant party or are derived

from such budgets, projections, estimates, financial analyses, reports and other information or from other sources, which involve numerous and significant subjective determinations made by management of the relevant party and/or which such

management has reviewed and found reasonable. The budgets, projections and estimates (including, without limitation, estimates of potential cost savings and synergies) contained in the materials may or may not be achieved and differences between

projected results and those actually achieved may be material. Houlihan Lokey has relied upon representations made by management of the Company and other participants in the Transaction that such budgets, projections and estimates have been

reasonably prepared in good faith on bases reflecting the best currently available estimates and judgments of such management (or, with respect to information obtained from public sources, represent reasonable estimates), and Houlihan Lokey

expresses no opinion with respect to such budgets, projections or estimates or the assumptions on which they are based. The scope of the financial analysis contained herein is based on discussions with the Company (including, without limitation,

regarding the methodologies to be utilized), and Houlihan Lokey does not make any representation, express or implied, as to the sufficiency or adequacy of such financial analysis or the scope thereof for any particular purpose. ¡ Houlihan Lokey

has assumed and relied upon the accuracy and completeness of the financial and other information provided to, discussed with or reviewed by it without (and without assuming responsibility for) independent verification of such information, makes no

representation or warranty (express or implied) in respect of the accuracy or completeness of such information and has further relied upon the assurances of the Company and other participants in the Transaction that they are not aware of any facts

or circumstances that would make such information inaccurate or misleading. In addition, Houlihan Lokey has relied upon and assumed, without independent verification, that there has been no change in the business, assets, liabilities, financial

condition, results of operations, cash flows or prospects of the Company or any other participant in the Transaction since the respective dates of the most recent financial statements and other information, financial or otherwise, provided to,

discussed with or reviewed by Houlihan Lokey that would be material to its analyses, and that the final forms of any draft documents reviewed by Houlihan Lokey will not differ in any material respect from such draft documents. ¡ The materials

are not an offer to sell or a solicitation of an indication of interest to purchase any security, option, commodity, future, loan or currency. The materials do not constitute a commitment by Houlihan Lokey or any of its affiliates to underwrite,

subscribe for or place any securities, to extend or arrange credit, or to provide any other services. In the ordinary course of business, certain of Houlihan Lokey’s affiliates and employees, as well as investment funds in which they may have

financial interests or with which they may co-invest, may acquire, hold or sell, long or short positions, or trade or otherwise effect transactions, in debt, equity, and other securities and financial instruments (including loans and other

obligations) of, or investments in, the Company, any Transaction counterparty, any other Transaction participant, any other financially interested party with respect to any transaction, other entities or parties that are mentioned in the materials,

or any of the foregoing entities’ or parties’ respective affiliates, subsidiaries, investment funds, portfolio companies and representatives (collectively, the “Interested Parties”), or any currency or commodity that may be

involved in the Transaction. Houlihan Lokey provides mergers and acquisitions, restructuring and other advisory and consulting services to clients, which may have in the past included, or may currently or in the future include, one or more

Interested Parties, for which services Houlihan Lokey has received, and may receive, compensation. Although Houlihan Lokey in the course of such activities and relationships or otherwise may have acquired, or may in the future acquire, information

about one or more Interested Parties or the Transaction, or that otherwise may be of interest to the Board, the Committee, or the Company, Houlihan Lokey shall have no obligation to, and may not be contractually permitted to, disclose such

information, or the fact that Houlihan Lokey is in possession of such information, to the Board, the Committee, or the Company or to use such information on behalf of the Board, the Committee, or the Company. Houlihan Lokey’s personnel may

make statements or provide advice that is contrary to information contained in the materials. 3

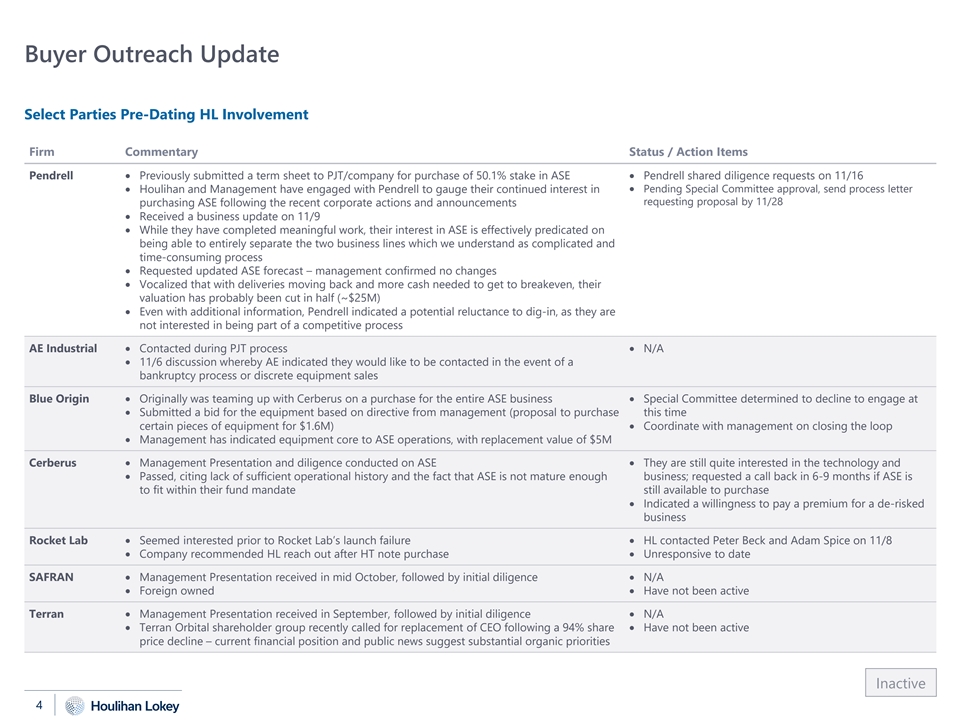

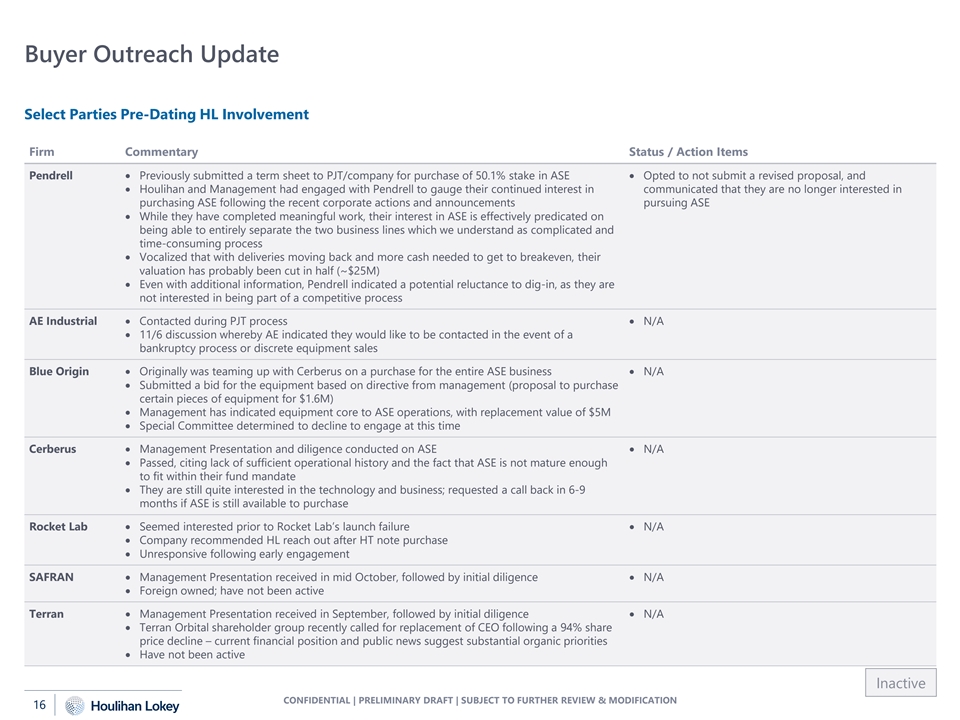

Buyer Outreach Update Select Parties Pre-Dating HL Involvement Firm

Commentary Status / Action Items Pendrell• Previously submitted a term sheet to PJT/company for purchase of 50.1% stake in ASE• Pendrell shared diligence requests on 11/16 • Pending Special Committee approval, send process letter

• Houlihan and Management have engaged with Pendrell to gauge their continued interest in requesting proposal by 11/28 purchasing ASE following the recent corporate actions and announcements • Received a business update on 11/9 •

While they have completed meaningful work, their interest in ASE is effectively predicated on being able to entirely separate the two business lines which we understand as complicated and time-consuming process • Requested updated ASE forecast

– management confirmed no changes • Vocalized that with deliveries moving back and more cash needed to get to breakeven, their valuation has probably been cut in half (~$25M) • Even with additional information, Pendrell indicated a

potential reluctance to dig-in, as they are not interested in being part of a competitive process AE Industrial • Contacted during PJT process• N/A • 11/6 discussion whereby AE indicated they would like to be contacted in the event

of a bankruptcy process or discrete equipment sales Blue Origin• Originally was teaming up with Cerberus on a purchase for the entire ASE business• Special Committee determined to decline to engage at • Submitted a bid for the

equipment based on directive from management (proposal to purchase this time certain pieces of equipment for $1.6M)• Coordinate with management on closing the loop • Management has indicated equipment core to ASE operations, with

replacement value of $5M Cerberus• Management Presentation and diligence conducted on ASE• They are still quite interested in the technology and • Passed, citing lack of sufficient operational history and the fact that ASE is not

mature enough business; requested a call back in 6-9 months if ASE is to fit within their fund mandate still available to purchase • Indicated a willingness to pay a premium for a de-risked business Rocket Lab• Seemed interested prior to

Rocket Lab’s launch failure• HL contacted Peter Beck and Adam Spice on 11/8 • Company recommended HL reach out after HT note purchase• Unresponsive to date SAFRAN• Management Presentation received in mid October,

followed by initial diligence• N/A • Foreign owned• Have not been active Terran• Management Presentation received in September, followed by initial diligence• N/A • Terran Orbital shareholder group recently called

for replacement of CEO following a 94% share • Have not been active price decline – current financial position and public news suggest substantial organic priorities Inactive 4

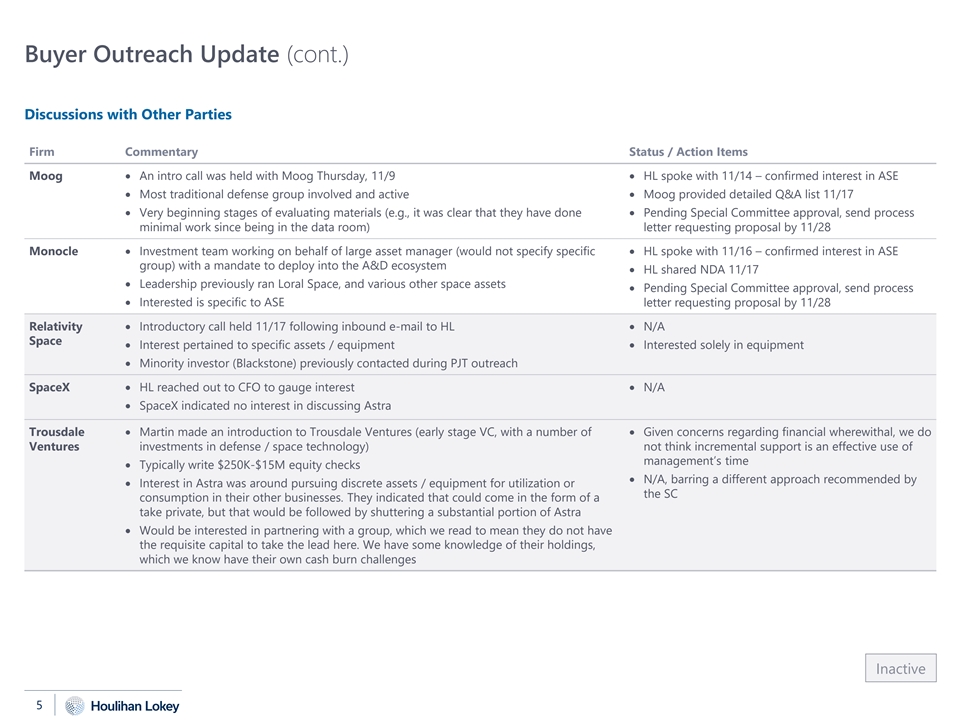

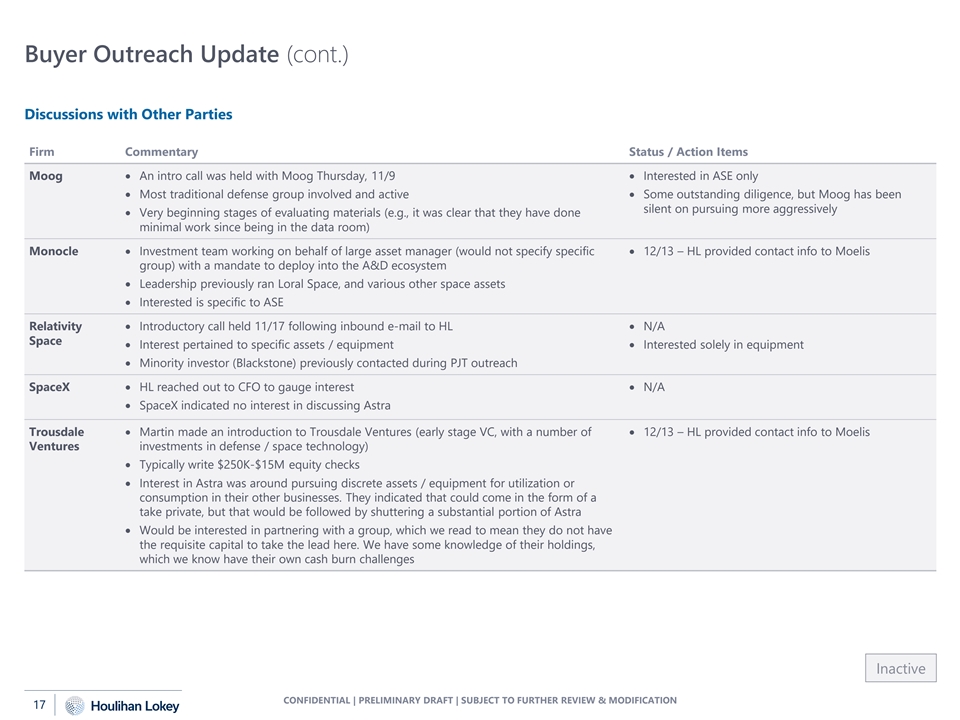

I Buyer Outreach Update (cont.) Discussions with Other Parties Firm

Commentary Status / Action Items Moog• An intro call was held with Moog Thursday, 11/9• HL spoke with 11/14 – confirmed interest in ASE • Most traditional defense group involved and active• Moog provided detailed

Q&A list 11/17 • Very beginning stages of evaluating materials (e.g., it was clear that they have done • Pending Special Committee approval, send process minimal work since being in the data room) letter requesting proposal by 11/28

Monocle • Investment team working on behalf of large asset manager (would not specify specific • HL spoke with 11/16 – confirmed interest in ASE group) with a mandate to deploy into the A&D ecosystem • HL shared NDA 11/17

• Leadership previously ran Loral Space, and various other space assets • Pending Special Committee approval, send process • Interested is specific to ASE letter requesting proposal by 11/28 Relativity • Introductory call

held 11/17 following inbound e-mail to HL• N/A Space • Interest pertained to specific assets / equipment• Interested solely in equipment • Minority investor (Blackstone) previously contacted during PJT outreach SpaceX•

HL reached out to CFO to gauge interest• N/A • SpaceX indicated no interest in discussing Astra Trousdale • Martin made an introduction to Trousdale Ventures (early stage VC, with a number of • Given concerns regarding

financial wherewithal, we do Ventures investments in defense / space technology) not think incremental support is an effective use of management’s time • Typically write $250K-$15M equity checks • N/A, barring a different approach

recommended by • Interest in Astra was around pursuing discrete assets / equipment for utilization or the SC consumption in their other businesses. They indicated that could come in the form of a take private, but that would be followed by

shuttering a substantial portion of Astra • Would be interested in partnering with a group, which we read to mean they do not have the requisite capital to take the lead here. We have some knowledge of their holdings, which we know have their

own cash burn challenges Inactive 5

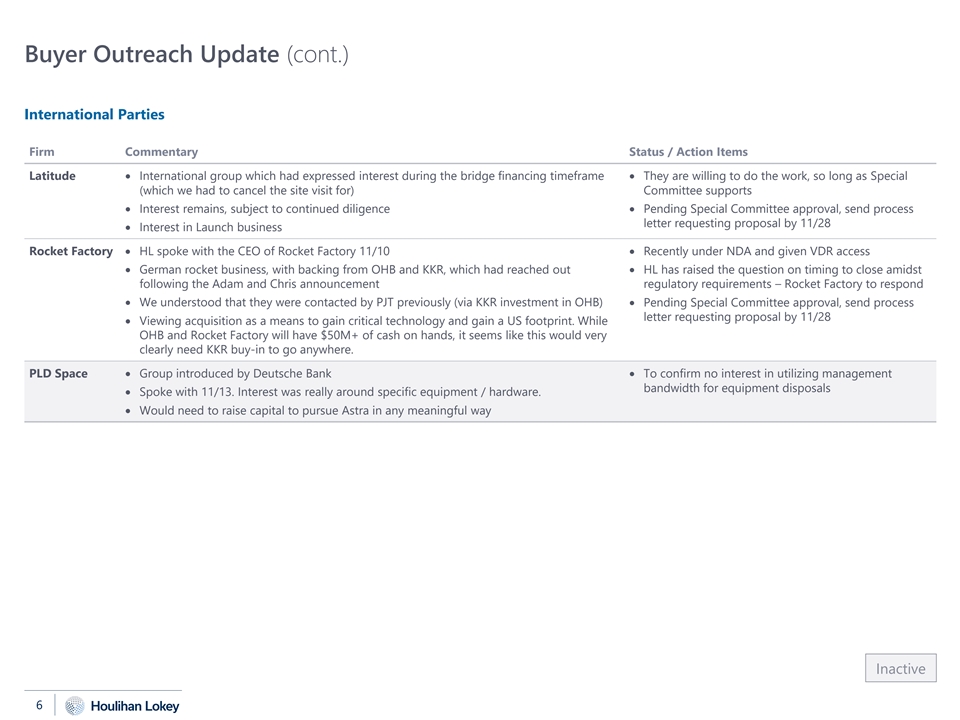

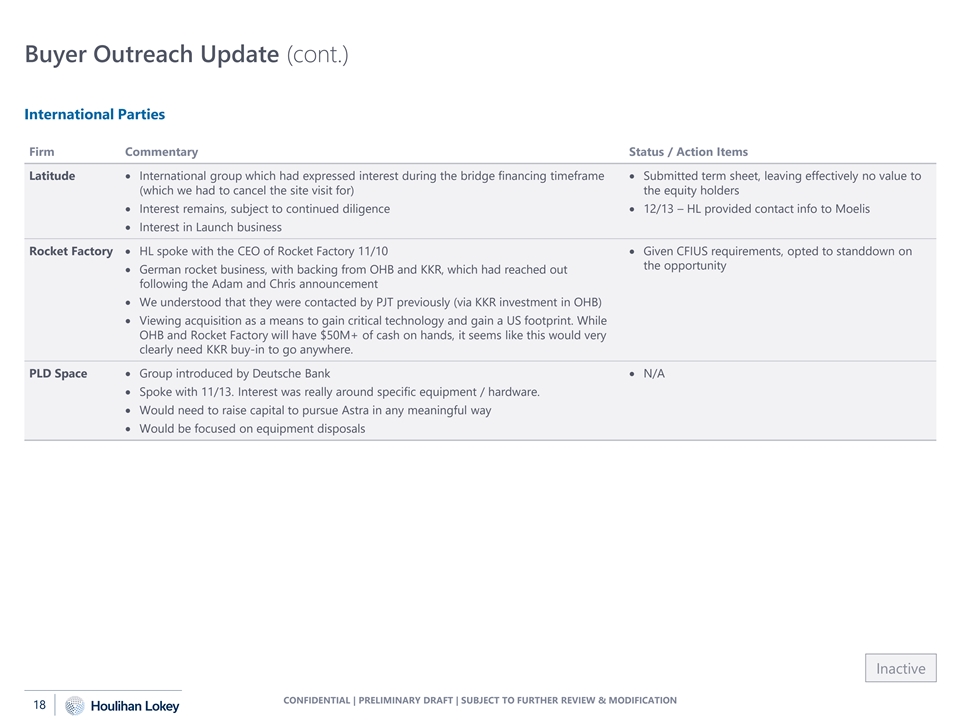

Buyer Outreach Update (cont.) International Parties Firm Commentary

Status / Action Items Latitude• International group which had expressed interest during the bridge financing timeframe• They are willing to do the work, so long as Special (which we had to cancel the site visit for) Committee supports

• Interest remains, subject to continued diligence• Pending Special Committee approval, send process letter requesting proposal by 11/28 • Interest in Launch business Rocket Factory • HL spoke with the CEO of Rocket Factory

11/10• Recently under NDA and given VDR access • German rocket business, with backing from OHB and KKR, which had reached out • HL has raised the question on timing to close amidst following the Adam and Chris announcement

regulatory requirements – Rocket Factory to respond • We understood that they were contacted by PJT previously (via KKR investment in OHB)• Pending Special Committee approval, send process letter requesting proposal by 11/28

• Viewing acquisition as a means to gain critical technology and gain a US footprint. While OHB and Rocket Factory will have $50M+ of cash on hands, it seems like this would very clearly need KKR buy-in to go anywhere. PLD Space• Group