As filed with the U.S. Securities and Exchange

Commission on October 24, 2023

Registration No. [ ]

U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-14

REGISTRATION STATEMENT UNDER THE SECURITIES

ACT OF 1933

| |

Pre-Effective Amendment No. |

¨ |

| |

|

|

| |

Post-Effective Amendment No. |

¨ |

| |

(Check appropriate box or boxes) |

|

abrdn Income Credit Strategies Fund

(Exact Name of Registrant as Specified in Charter)

1900 Market Street, Suite 200

Philadelphia, PA 19103

(Address of Principal Executive Offices)

215-405-5700

(Registrant’s Telephone Number, Including

Area Code)

Lucia Sitar, Esq.

c/o abrdn Inc.

1900 Market Street, Suite 200

Philadelphia, PA 19103

215-405-5700

(Name and Address of Agent for Service)

Copies to:

Thomas C. Bogle, Esq.

William J. Bielefeld, Esq.

Dechert LLP

1900 K Street, NW

Washington, DC 20006

Approximate date of proposed public offering:

As soon as practicable after the effective date of this Registration Statement.

The Registrant hereby amends this registration

statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which

specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the

Securities Act of 1933 or until this registration statement shall become effective on such date as the Securities and Exchange Commission,

acting pursuant to said Section 8(a), may determine.

FIRST TRUST HIGH INCOME LONG/SHORT FUND

FIRST TRUST/ABRDN GLOBAL OPPORTUNITY INCOME

FUND

120 East Liberty Drive, Suite 400

Wheaton, IL 60187

(630) 765-8000

IMPORTANT SHAREHOLDER INFORMATION

We

are pleased to enclose a notice, combined proxy statement/prospectus (the “Proxy Statement/Prospectus”), and proxy card(s) for

special meetings of shareholders relating to each of First Trust High Income Long/Short Fund (“FSD”) and First Trust/abrdn

Global Opportunity Income Fund (“FAM”), each a Massachusetts business trust (each, an “Acquired Fund” and collectively,

the “Acquired Funds”). The special meetings (with any postponements or adjournments, each a “Special Meeting”

and, collectively, the “Special Meetings”) of shareholders of each Acquired Fund are scheduled to be held at

the offices of the Acquired Fund’s investment adviser, First Trust Advisors L.P., located at 120 East Liberty Drive, Suite 400,

Wheaton, Illinois 60187, on [ ], 2024, at [ ] Central Time for FSD and at [ ] Central Time for FAM. At the Special Meeting, shareholders

will be asked to consider and, to vote on the approval of a proposed Agreement and Plan of Reorganization (each, a “Reorganization

Agreement” and, collectively, the “Reorganization Agreements”) for each Acquired Fund, which contemplates the reorganization

of the Acquired Fund with and into abrdn Income Credit Strategies Fund (the “Acquiring Fund”), a Delaware statutory trust

(each, a “Reorganization” and collectively, the “Reorganizations”). The Acquiring Fund as it would exist after

the Reorganizations is referred to as the “Combined Fund.” Each Reorganization is not contingent on the approval or consummation

of the other Reorganization.

After

careful consideration, the Board of Trustees of FSD and the Board of Trustees of FAM believe that each Reorganization, as applicable,

is in the best interests of FSD and FAM shareholders and therefore recommends that you vote “FOR” the respective proposal.

The Acquired Funds and the Acquiring Fund are managed by different investment advisers. Each Reorganization is anticipated

to provide shareholders of FSD and FAM, among other things, with exposure to a similar investment objective, principal investment strategies

and principal risks, with some differences as discussed in the enclosed Proxy Statement/Prospectus and access to the Acquiring Fund’s

investment adviser’s and its affiliates’ asset management business, including its commitment to the closed-end fund business,

and its investment management experience.

It is expected that shareholders of each Acquired

Fund will not recognize any gain or loss for federal income tax purposes as a result of the exchange of their shares in the applicable

Acquired Fund for shares of the Acquiring Fund in connection with the applicable Reorganization (except with respect to cash received

in lieu of fractional shares of the Acquiring Fund). The Reorganization proposals are described in more detail, and a comparison of the

strategies, expenses and certain other features of each Acquired Fund and the Acquiring Fund is included, in the enclosed Proxy Statement/Prospectus.

We encourage you to review this information carefully.

As

a shareholder of record as of the close of business on October 23, 2023, the record date, you are entitled to notice of, and to

vote at, the Special Meeting, therefore we are asking that you please take the time to cast your vote prior to the [ ], 2024 Special

Meeting. If you do not vote, you may receive a phone call from the Acquired Fund’s proxy solicitor, EQ Fund Solutions, LLC.

We appreciate your participation in this important Special Meeting.

Sincerely,

James A. Bowen

Chairman of the Board of Trustees, First Trust High Income Long/Short

Fund and First Trust/abrdn Global Opportunity Income Fund

It

is important that your shares be represented at the Special Meeting. In order to avoid

delay and to ensure that your shares are represented, please vote as promptly as possible. You may vote easily and quickly by mail, by

telephone or via the Internet. You may also vote in person by attending the Special Meeting (subject to certain requirements). To vote

by mail, please complete and mail your proxy card in the enclosed envelope. To vote by telephone or via the Internet, please follow the

instructions on the proxy card. If you need any assistance or have any questions regarding a proposal or how to vote your shares, please

call the Acquired Funds’ proxy solicitor, EQ Fund Solutions, LLC, at [ ] weekdays from 9:00 a.m. to 10:00 p.m. Eastern

Time.

FIRST TRUST HIGH INCOME LONG/SHORT FUND

FIRST TRUST/ABRDN GLOBAL OPPORTUNITY INCOME

FUND

120 East Liberty Drive, Suite 400

Wheaton, IL 60187

(630) 765-8000

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD [ ], 2024

Notice is hereby given that special meetings

of shareholders (with any postponements or adjournments, each a “Special Meeting” and, collectively, the “Special Meetings”)

of each of First Trust High Income Long/Short Fund (“FSD”) and First Trust/abrdn Global Opportunity Income Fund (“FAM”),

each a Massachusetts business trust, (each an “Acquired Fund” and, collectively, the “Acquired Funds”), are scheduled

to be held at the offices of the Acquired Fund’s investment adviser, First Trust Advisors, L.P., located at 120 East Liberty Drive,

Suite 400, Wheaton, Illinois 60187, on [ ], 2024, at [ ] Central Time for FSD and at [ ] Central Time for FAM. At the Special

Meeting, shareholders will be asked to consider and to vote on the below proposals (each a “Proposal” and, collectively,

the “Proposals”).

For shareholders of FSD:

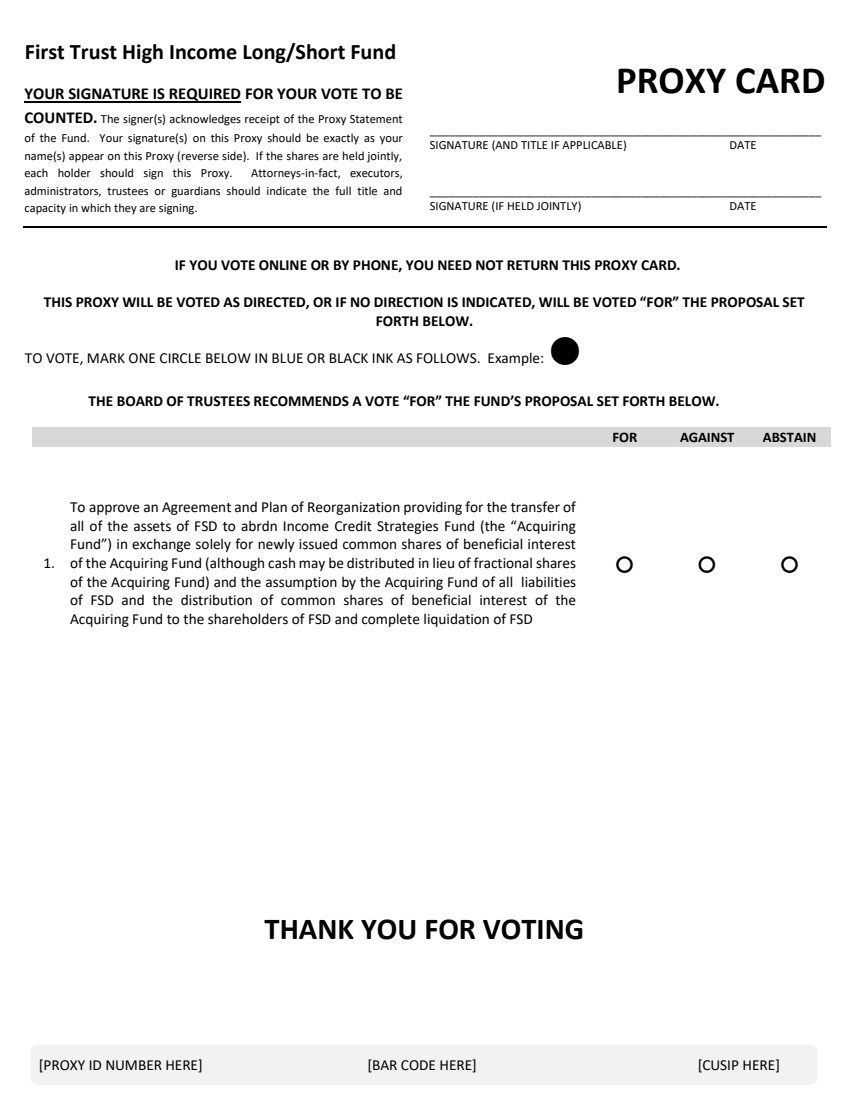

To approve an Agreement and Plan of Reorganization

providing for the transfer of all of the assets of FSD to abrdn Income Credit Strategies Fund (the “Acquiring Fund”) in exchange

solely for newly issued common shares of beneficial interest of the Acquiring Fund (although cash may be distributed in lieu of fractional

shares of the Acquiring Fund) and the assumption by the Acquiring Fund of all liabilities of FSD and the distribution of common shares

of beneficial interest of the Acquiring Fund to the shareholders of FSD and complete liquidation of FSD (the “FSD Reorganization”)

For shareholders of FAM:

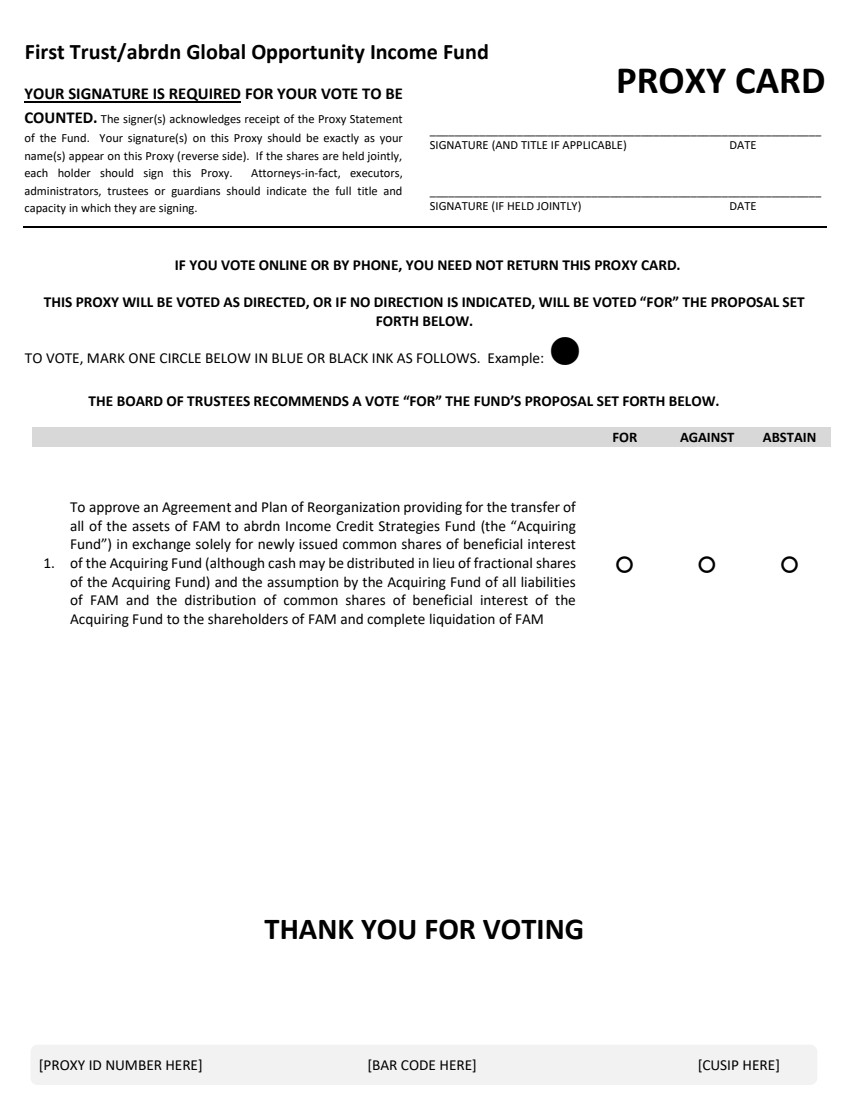

To approve an Agreement and Plan of Reorganization

providing for the transfer of all of the assets of FAM to abrdn Income Credit Strategies Fund (the “Acquiring Fund”) in exchange

solely for newly issued common shares of beneficial interest of the Acquiring Fund (although cash may be distributed in lieu of fractional

shares of the Acquiring Fund) and the assumption by the Acquiring Fund of all liabilities of FAM and the distribution of common shares

of beneficial interest of the Acquiring Fund to the shareholders of FAM and complete liquidation of FAM (the “FAM Reorganization”)

Shareholders will also be asked to transact such

other business as may properly come before the applicable Special Meeting.

Shareholders of record as of the close of business

on October 23, 2023, the record date (the “Record Date”), are entitled to notice of, and to vote at, the Special Meeting.

Each Reorganization is intended to be treated

as a tax-free reorganization for US federal income tax purposes.

Each Reorganization is not contingent on the approval or consummation

of the other Reorganization.

Whether

or not you are planning to attend the Special Meeting, please vote prior to [11:59pm] ET on [ ],

2024. Voting is quick and easy. Voting by proxy will not prevent you from voting your shares at the Special Meeting. You may revoke

your proxy at any time before the Special Meeting by (i) written notice delivered to the Secretary of the respective Acquired Fund

prior to the exercise of the proxy; (ii) execution of a subsequent proxy; or (iii) attending and voting at the Special Meeting.

If you hold shares through a broker, bank or other nominee, you must follow the instructions you receive from your nominee in order to

revoke your voting instructions.

Please contact EQ Fund Solutions, LLC at [ ]

with any questions regarding access to the Special Meeting, and an EQ representative will contact you to answer your questions. Whether

or not you plan to participate in the Special Meeting, we urge you to vote and submit your vote in advance of the Special Meeting.

By order of the Board of Trustees of FSD and the Board of Trustees

of FAM,

W. Scott Jardine

Secretary, First Trust High Income Long/Short Fund and First Trust/abrdn

Global Opportunity Income Fund

Important Notice Regarding Internet Availability

of Proxy Materials for the Special Meeting to be Held on [ ], 2024:

The Proxy Statement/Prospectus, the Notice of

the Special Meeting, any accompanying materials and any amendments or supplements to the foregoing materials that are required to be

furnished to shareholders are available to you on the Internet at [ ].

It

is important that your shares be represented at the Special Meeting. In order to avoid delay and to ensure that your shares are represented,

please vote as promptly as possible. You may vote easily and quickly by mail, by telephone or via the Internet. You may also vote in

person by attending the Special Meeting (subject to certain requirements). To vote by mail, please complete and mail your proxy card

in the enclosed envelope. To vote by telephone or via the Internet, please follow the instructions on the proxy card. If you need any

assistance or have any questions regarding a Proposal or how to vote your shares, please call the Acquired Funds’ proxy solicitor,

EQ Fund Solutions, LLC, at [ ] weekdays from 9:00 a.m. to 10:00 p.m. Eastern Time.

QUESTIONS & ANSWERS

The following is a summary of more complete information

appearing later in the attached combined proxy statement/prospectus (the “Proxy Statement/Prospectus”) or incorporated by

reference into the Proxy Statement/Prospectus. You should carefully read the entire Proxy Statement/Prospectus, including the Agreements

and Plans of Reorganization (each, a “Reorganization Agreement” and, collectively, the “Reorganization Agreements”),

forms of which are attached as Appendix A thereto, because it contains details that are not in the Questions & Answers.

| Q: |

Why is a shareholder meeting being held?

|

| A: |

The

shareholders of First Trust High Income Long/Short Fund (“FSD”) and First Trust/abrdn Global Opportunity Income Fund

(“FAM”), each a Massachusetts business trust (each an “Acquired Fund” and, collectively, the “Acquired

Funds”), are being asked to approve a Reorganization Agreement providing for the transfer of all of the assets of each Acquired

Fund to abrdn Income Credit Strategies Fund (the “Acquiring Fund”) in exchange solely for newly issued common shares

of beneficial interest of the Acquiring Fund (although cash may be distributed in lieu of fractional shares of the Acquiring Fund)and

the assumption by the Acquiring Fund of all liabilities of each Acquired Fund and the distribution of common shares of beneficial

interest of the Acquiring Fund to the shareholders of each Acquired Fund and complete liquidation of each Acquired Fund (each a “Reorganization”

and, collectively, the “Reorganizations”). It is currently expected that the Reorganizations will occur in the first

quarter of 2024.

As summarized below and described more fully

in the Proxy Statement/Prospectus, each Acquired Fund and the Acquiring Fund (each, a “Fund” and, collectively, the “Funds”)

are closed-end management investment companies with similar investment objectives, principal investment strategies and principal

risks, with some substantial differences. Please see below and “Comparison of the Funds” in the Proxy Statement/Prospectus

for additional information. The Acquiring Fund would be the accounting and performance survivor of each Reorganization. The Acquiring

Fund as it would exist after each Reorganization is referred to as the “Combined Fund.”

At a separate meeting, the shareholders of

the Acquiring Fund are being asked to approve the issuance of additional common shares of beneficial interest of the Acquiring Fund

that would be issued to the Acquired Fund shareholders in connection with the Reorganizations. |

| Q: |

Why are the Reorganizations being proposed?

|

| A: |

On October 23, 2023, First Trust Advisors

L.P. (“First Trust”), abrdn Inc. and, for the purposes specified therein, abrdn plc., entered into a separate agreement

(the “Purchase Agreement”) pursuant to which abrdn Inc. will acquire certain assets related to First Trust’s business

of providing investment management services with respect to the assets of each Acquired Fund and certain other registered investment

companies (the “Business”) if the Reorganizations are approved, and upon satisfaction or waiver of certain other conditions.

More specifically, under the Purchase Agreement, First Trust has agreed to transfer to abrdn Inc., for a cash payment at the closing

of the Asset Transfer (as defined below) and subject to certain exceptions, (i) all right, title and interest of First Trust

in and to the books and records relating to the Business of the Acquired Fund; and (ii) the goodwill of the Business (the “Asset

Transfer”).

The Funds are not a party to the Purchase

Agreement; however, the completion of the Asset Transfer is subject to certain conditions, including shareholder approval of each

Reorganization described in the Proxy Statement/Prospectus for such Fund’s Reorganization to proceed. Therefore, if the respective

shareholders do not approve the Reorganizations or if the other conditions in the Purchase Agreement are not satisfied or waived,

then the Asset Transfer may not be completed, and the Purchase Agreement may be terminated.

|

| Q: |

Why are the Reorganizations being recommended

by the Board of Trustees of FSD and the Board of Trustees of FAM?

|

| A: |

The Board of Trustees of FSD and the Board

of Trustees of FAM (each an “Acquired Fund Board” and, collectively, the “Acquired Fund Boards”) have determined

that the Reorganizations are in the best interests of the shareholders of the respective Acquired Funds. In reaching its decision

to approve the respective Reorganization, each Acquired Fund Board considered alternatives to the Reorganizations, including continuing

to operate the Acquired Fund as a separate fund, and determined to recommend that shareholders approve the respective Reorganization.

|

| |

Please see “Background and Reasons for the Proposed Reorganization” in the Proxy Statement/Prospectus

for additional information on each Acquired Fund Board’s considerations relating to each Reorganization. |

| Q: |

What happens if a Proposal is not approved

by the shareholders?

|

| A: |

Completion of each Reorganization requires

both the approval of the Reorganization Agreement by the respective Acquired Fund shareholders and approval of the issuance of Acquiring

Fund common shares by the Acquiring Fund shareholders. However, each Reorganization is not contingent on the approval or consummation

of the other Reorganization (i.e., a Reorganization of one of the Acquired Funds, if approved by that Acquired Fund’s shareholders,

may still proceed if the other Reorganization is not approved by the other Acquired Fund’s shareholders). If the applicable

Reorganization Agreement or the issuance of Acquiring Fund common shares is not approved by shareholders of the applicable Fund,

then the Acquired Fund will continue to operate as a separate fund in the manner in which it is currently managed.

|

| Q: |

How will the fees and expenses of the

Combined Fund compare to those of each Acquired Fund? |

| |

|

A: |

The contractual advisory fee of FSD is

1.00% of the average daily value of FSD’s Managed Assets, and the contractual advisory fee of the FAM is 1.00% of the average

daily value of FAM’s Managed Assets. For FAM, the term Managed Assets, for purposes of the advisory fee, means the total

asset value of FAM minus the sum of FAM’s liabilities other than the principal amount of borrowings, if any. For FSD, the

term Managed Assets, for purposes of the advisory fee, means the average daily gross asset value of FSD (which includes the principal

amount of any borrowings) minus the sum of FSD’s liabilities. The Acquired Funds and Acquiring Fund each currently use

leverage.

The contractual advisory fee of the Acquiring

Fund and the Combined Fund is 1.25% of the Fund’s average daily Managed Assets. For the Acquiring Fund and the Combined Fund, the

term Managed Assets means the total assets of the Acquiring Fund (including any assets attributable to money borrowed for investment

purposes, including proceeds from (and assets subject to) reverse repurchase agreements, any credit facility and any issuance of preferred

shares or notes) minus the sum of the Acquiring Fund’s accrued liabilities (other than Acquiring Fund liabilities incurred for

the purpose of leverage).

The net total annual operating expense ratios,

excluding interest expense, of the Acquired Funds and the Acquiring Fund, and, following the consummation of one or both Reorganizations,

the net total annual operating expense ratio, excluding interest expense, of the Combined Fund is expected to be as follows: |

| |

Current Expense

Ratio of FSD* | |

Current Expense

Ratio of FAM* | |

Current Expense

Ratio of the

Acquiring

Fund** | |

Pro Forma

Combined Fund

(FSD into

Acquiring Fund

only)** | |

Pro Forma

Combined Fund

(FAM into

Acquiring Fund

only)** | |

Pro Forma

Combined Fund

(FSD and FAM

into Acquiring

Fund)** | |

| |

| 1.16 | % |

1.91 | % |

1.99 | % |

1.99 | % |

1.99 | % |

1.99 | % |

| |

*As of the Acquired Fund’s most recent

semi-annual period end (April 30, 2023 for FSD and June 30, 2023 for FAM), based on average daily net assets. |

| |

|

| |

**Information for the Acquiring Fund and Combined Fund

is as of the six months ended April 30, 2023. The Acquiring Fund’s assets have been restated to reflect the net assets as of

April 30, 2023 (rather than average net assets over the six months ended April 30, 2023) in order to provide more accurate expense

ratios due to a significant increase in Fund assets that occurred on March 10, 2023 as the result of a reorganization of another

closed-end management investment company registered under the 1940 Act with and into the Acquiring Fund. The estimated total annual

operating expense ratio of the Acquiring Fund and the Combined Fund is net of fee waivers and, therefore, reflects the application

of the operating expense limitation described below. |

| |

|

| |

Pro forma combined fees and expenses are estimated in good

faith and are hypothetical. There can be no assurance that future expenses will not increase or that any estimated expense savings

will be realized. |

| |

Following the consummation of the Reorganization,

the total annual operating expense ratio of the Combined Fund is expected to be higher than the current total annual operating expense

ratio of each Acquired Fund. The Acquiring Fund has consistently traded at a tighter discount/premium over near and longer-term periods

than each Acquired Fund and has a higher distribution rate and yield. Morningstar reports that as of September 29, 2023, the 12-month

average discount of the Acquiring Fund was 0.21% as compared to the discount of the FSD of 9.85% and FAM of 10.73% over the same

period. |

| |

|

| |

abrdn Investments Limited (“aIL”), the investment

adviser of the Acquiring Fund, has contractually agreed to limit total “Other Expenses” of the Acquiring Fund (excluding

any interest, taxes, brokerage fees, short sale dividend and interest expenses and non-routine expenses) as a percentage of net assets

attributable to common shares of the Acquiring Fund to 0.25% per annum of the Acquiring Fund’s average daily net assets until

March 7, 2024 and then 0.35% per annum of the Acquiring Fund’s average daily net assets until October 31, 2024. aIL has contractually

agreed to limit total “Other Expenses” of the Combined Fund (excluding any interest, taxes, brokerage fees, short sale

dividend and interest expenses and non-routine expenses) as a percentage of net assets attributable to common shares of the Combined

Fund to 0.25% per annum of the Combined Fund’s average daily net assets for twelve months following the closing of the Reorganization

and then 0.35% until June 30, 2025. This contractual limitation may not be terminated before twelve months following the closing

of the Reorganization or June 30, 2025, whichever is later, without the approval of the Acquiring Fund’s or Combined Fund’s,

as applicable, trustees who are not “interested persons” of the Acquiring Fund or Combined Fund, as applicable (as defined

in the Investment Company Act of 1940, as amended (the “1940 Act”)). |

| |

|

| |

The Acquiring Fund or Combined Fund, as applicable, may

repay any such reimbursement from aIL, within three years of the reimbursement, provided that the following requirements are met:

the reimbursements do not cause the Acquiring Fund or Combined Fund, as applicable, to exceed the lesser of the applicable expense

limitation in the contract at the time the fees were limited or expenses are paid or the applicable expense limitation in effect

at the time the expenses are being recouped by aIL. |

| |

|

| |

Please see “Fees and Expenses” and “Management

of the Funds” in the Proxy Statement/Prospectus for additional information. |

| Q: |

How different are the Funds? |

| A: |

As

summarized below and set forth more fully in the Proxy Statement/Prospectus, there are substantial differences between each Acquired

Fund and the Acquiring Fund. In particular, they have different investment advisers. First Trust is the investment manager of each

Acquired Fund. MacKay Shields LLC (“MacKay”) is the sub-adviser of FSD and abrdn Inc. is the sub-adviser of FAM.

aIL is the investment adviser of the Acquiring Fund and abrdn Inc. is the investment sub-adviser of the Acquiring Fund.

Each Fund is a closed-end management investment

company registered under the 1940 Act. FSD and FAM are Massachusetts business trusts and diversified closed-end management investment

companies. The Acquiring Fund is a Delaware statutory trust and a diversified closed-end management investment company. Each Fund’s

common shares are listed on the New York Stock Exchange.

The

Acquiring Fund and FAM have investment objectives that are materially the same. FSD’s primary investment objective is

to provide current income, with a secondary objective of capital appreciation. Each of FAM’s and the Acquiring Fund’s

primary investment objective is to is to seek a high level of current income with a secondary objective of capital appreciation.

The Funds’ investment strategies are similar in that they invest in high-yield fixed income securities. However, in seeking

to achieve their respective investment objectives, there are some substantial differences in the investment strategies and risks

of each Fund. The Acquiring Fund and FSD each may invest in high-yield securities without limitation (although FSD generally limits

its investment in certain high-yield securities to no more than 5% above the index which it tracks) while FAM may only invest up

to 60% of its Managed Assets in such securities.

FSD seeks to achieve its investment objectives

by investing, under normal market conditions, a majority of its assets in a diversified portfolio of U.S. and foreign (including

emerging markets) high-yield corporate fixed-income securities of varying maturities that are rated below investment grade at the

time of purchase. As part of its investment strategy, FSD maintains both long and short positions in securities under normal market

conditions. The Fund’s long positions, either directly or through derivatives, may total up to 130% of the Fund’s managed

assets.

|

| | The

Fund’s short positions, either directly or through derivatives, may total up to 30%

of the Fund’s managed assets. The Fund’s use of derivatives, other than for hedging

purposes, will not exceed 30% of the Fund’s managed assets.

FSD

may invest up to 5% of its Managed Assets (defined below) in common stocks, including those

of foreign issuers. FSD may invest up to 20% of its Managed Assets in securities that, at

the time of investment, are illiquid. FSD may also invest, without limit, in securities that

are unregistered (but are eligible for purchase and sale by certain qualified institutional

buyers) or are held by control persons of the issuer and securities that are subject to contractual

restrictions on their resale (“restricted securities”). However, restricted securities

determined to be illiquid are subject to the limitations set forth above.

FAM seeks to achieve its investment objectives

by investing, under normal circumstances, substantially all of its Managed Assets (defined below) in a diversified portfolio of fixed-income

securities, including government and corporate bonds, of U.S. and non-U.S. issuers. FAM’s investment team believes that a portfolio

containing investment grade securities that invests across many national markets has the opportunity to achieve returns in excess

of a portfolio that invests in a single domestic bond market, as the global fixed-income marketplace is generally less efficient

than domestic markets. Under normal market conditions, FAM invests in securities of issuers in at least three countries (in addition

to the United States), however, securities of issuers in a single country will not exceed 30% of the FAM’s Managed Assets.

The Fund invests at least 60% of its Managed Assets in securities issued by government, government-related and supranational issuers

(“government debt”). At least 25% of the Fund’s Managed Assets will be invested in U.S. dollar-denominated securities

or non-U.S. dollar-denominated securities that have been fully hedged into U.S. dollars. FAM may also invest up to 10% of its Managed

Assets in forward foreign currency exchange contracts for hedging and investment purposes. FAM places thresholds of the proportion

of its Managed Assets that may be invested in corporate debt obligations, below investment grade securities, asset-backed securities,

credit-linked notes, illiquid securities, and forward foreign exchange contracts (both deliverable and non-deliverable).

For purposes of FAM’s investment strategies,

“Managed Assets” means the total asset value of FAM minus the sum of FAM’s liabilities other than the principal

amount of borrowings, if any. For purposes of FSD’s investment strategies, “Managed Assets” means the average daily

gross asset value of FSD (which includes the principal amount of any borrowings), minus the sum of FSD’s liabilities.

The Acquiring Fund is a high yield debt fund

that is permitted to invest in a variety of US and foreign-issued debt instruments, and may utilize derivatives and hedging techniques,

to achieve its investment objectives. The Acquiring Fund generally invests in corporate bonds and is permitted to invest in senior

loans and in second lien or other subordinated loans or debt instruments, including non-stressed and stressed credit obligations,

and related derivatives. The Acquiring Fund seeks to capitalize on market inefficiencies and to reallocate the portfolio of the Acquiring

Fund to opportunistically emphasize those investments, categories of investments and geographic exposures believed to be best suited

to the current investment and interest rate environment and market outlook. There is no minimum or maximum limit on the amount of

the Acquiring Fund’s assets that may be invested in non-U.S. credit obligations generally or in emerging market credit obligations

specifically.

The Acquiring Fund is permitted to use derivative

instruments to manage currency risk, credit risk, and interest rate risk and to replicate, or use as a substitute for, physical securities.

As of the Acquiring Fund’s most recent annual report to shareholders, the Acquiring Fund used derivatives to hedge foreign

currency exposure.

The Acquiring Fund and the Acquired Funds

may use leverage to the extent permitted by the 1940 Act. Currently, the 1940 Act and the rules and regulations thereunder generally

limit the extent to which a Fund may utilize borrowings, together with any other senior securities representing indebtedness, to

33 and 1/3% of the Fund’s total assets (including the assets subject to, and obtained with, the proceeds of such leverage)

at the time utilized (less the Fund’s liabilities and indebtedness not represented by senior securities). In addition, the

1940 Act limits the extent to which the Fund may issue preferred shares plus senior securities representing indebtedness to 50% of

the Fund’s total assets (less the Fund’s liabilities and indebtedness not represented by senior securities). As of September 29,

2023, FSD and FAM had 26.0% and 20.3% aggregate leverage from borrowings as a percentage of each Acquired Fund’s total assets,

respectively. As of September 29, 2023, the Acquiring Fund had 29.1% aggregate leverage from the issuance of preferred shares

and borrowings as a percentage of its total assets. The Combined Fund anticipates that it will use leverage similarly to the Acquiring

Fund. |

| |

The Acquiring Fund offers preferred shares. The preferred shares of the Acquiring Fund are senior to the Acquiring

Fund’s common shares, such that holders of preferred shares have priority over the distribution of the Acquiring Fund’s

assets, including dividends and liquidating distributions. Additionally, holders of the preferred shares, voting separately as a

class, have the right to elect two trustees of the Acquiring Fund.

Please see “Comparison of the Funds” in the Proxy Statement/Prospectus for additional information. |

| |

|

| Q: |

How will the Reorganizations be effected?

|

| A: |

Assuming

FSD and FAM shareholders approve the Reorganizations and the Acquiring Fund’s shareholders approve the issuance of Acquiring

Fund common shares, each Acquired Fund will transfer all of its assets to the Acquiring Fund in exchange for common shares of the

Acquiring Fund (although shareholders may receive cash for fractional shares of the Acquiring Fund), and the assumption by the Acquiring

Fund of all liabilities of each Acquired Fund. Following the Reorganizations, each Acquired Fund will be dissolved and terminated

in accordance with its Declaration of Trust, Amended and Restated By-Laws and the 1940 Act.

Following each Reorganization, you, as an

Acquired Fund shareholder, will become a shareholder of the Acquiring Fund. Holders of common shares of each Acquired Fund will receive

newly issued common shares of the Acquiring Fund, par value $0.001 per share, the aggregate net asset value (“NAV”) (not

the market value) of which will equal the aggregate NAV (not the market value) of the common shares of the respective Acquired Fund

you held immediately prior to the respective Reorganization (although shareholders may receive cash for fractional shares of the

Acquiring Fund).

Based

on each Fund’s NAV as of September 29, 2023, the exchange ratio at which common shares of FSD would have converted to

common shares of the Combined Fund is 1.8109 (assuming each Reorganization was consummated

following the market close on September 29, 2023) and

the exchange ratio at which common shares of FAM would have converted to common shares of the Combined Fund is 0.9511 (assuming

each Reorganization was consummated following the market close on September 29, 2023).

An FSD shareholder would have received 1.8109 shares of the Combined Fund for each FSD share held and an FAM shareholder would

have received 0.9511 shares of the Combined Fund for each FAM share held.

|

| Q: |

How will a Reorganization affect the value

of my investment?

|

| A: |

At the closing of each Reorganization, each

Agreement and Plan of Reorganization sets forth that the Acquired Fund assets will be valued in accordance with the Acquired Fund’s

valuation procedures as approved by the Board of Trustees of the Acquired Fund. Upon the consummation of the Reorganization, the

assets transferred to the Acquiring Fund will be valued pursuant to the Acquiring Fund’s valuation procedures as approved by

the Board of Trustees of the Acquiring Fund. The valuation procedures for the Acquired Funds, on the one hand, and the Acquiring

Fund, on the other hand, differ in certain respects.

For purposes of determining an Acquired Fund’s

net asset value, corporate, sovereign, government, foreign, mortgage backed, and capital preferred fixed income securities and senior

floating rate bank loans are priced at the mean of evaluated bid and asked prices provided by third-party pricing vendors on the

valuation date. In contrast, the Acquiring Fund values such securities at the bid price provided by third-party pricing vendors.

If a Reorganization is approved by shareholders

and assuming that FSD’s and FAM’s fixed income holdings are not sold in advance of the respective Reorganization, the

net asset value per share of the Acquiring Fund will be less than the net asset value per share of the respective Acquired Fund.

For example, if ACP’s valuation procedures were used to value FSD and FAM’s fixed income security holdings as of September 29,

2023, the value of the Combined Fund’s shares is estimated to be reduced by approximately $1,052,639 (0.13% of the Combined

Fund as of September 29, 2023) or $0.009 per share of the Combined Fund, assuming both Reorganizations are consummated. |

| Q: |

At what prices have common shares of each

Acquired Fund and common shares of the Acquiring Fund historically traded?

|

| A: |

Common shares of each Acquired Fund and the

Acquiring Fund have from time to time traded below their NAVs. As of September 29, 2023, FSD common shares were trading at a

12.56% discount to its NAV, FAM common shares were trading at a 11.49% discount to its NAV, and the Acquiring Fund common shares

were trading at a 0.44%premium to its NAV. There can be no assurance that, after the Reorganization, common shares of the Combined

Fund will trade at, above or below NAV. The market value of the common shares of the Combined Fund may be more or less than the

market value of the common shares of either the Acquiring Fund or each Acquired Fund prior to the Reorganization.

To the extent the respective Acquired Fund

is trading at a discount to its NAV and the Acquiring Fund is trading at a premium to its NAV at the time of the Reorganization,

Acquired Fund shareholders would have the potential for an economic benefit. There can be no assurance that, after the Reorganization,

common shares of the Combined Fund will trade at, above or below NAV. The market value of the common shares of the Combined Fund

may be less than the market value of the common shares of the Acquiring Fund prior to the Reorganization. Additionally, among other

potential consequences of the Reorganization, portfolio transitioning due to the Reorganization may result in capital gains or losses,

which may have federal income tax consequences for shareholders of the Acquired Funds and the Combined Fund.

Please see “Share Price Data”

in the Proxy Statement/Prospectus for additional information.

|

| Q: |

Will the Reorganizations impact Fund distributions

to shareholders?

|

| A: |

FSD currently pays a monthly distribution

of $0.105 per share; based on the market price and NAV as of September 29, 2023, FSD’s annualized distribution rate is

11.75% and 10.28%, respectively. FAM currently pays a monthly distribution of $0.060 per share; based on the market price and NAV as

of September 29, 2023, FAM’s annualized distribution rate is 12.63% and 11.18%, respectively. The Acquiring Fund currently

pays a monthly distribution of $0.100 per share; based on the market price and NAV as of September 29, 2023, the Acquiring Fund’s

annualized distribution rate is 17.6% and 17.7%, respectively. The Combined Fund expects to pay a monthly distribution of $0.100

per share and would have the same distribution yield as the Acquiring Fund.

Prior to the closing of the Reorganizations,

each Acquired Fund expects to declare a distribution to its shareholders that, together with all previous distributions, will have

the effect of distributing to its shareholders all of its investment company taxable income (computed without regard to the deduction

for dividends paid) and net realized capital gains, if any, through the date of the Reorganizations’ closing. All or a portion

of such distribution may be taxable to the Acquired Fund shareholders for US federal income tax purposes.

The Combined Fund intends to make its first

distribution to shareholders in the month immediately following the Reorganization. In addition, the Combined Fund expects to follow

the same frequency of payments as each Fund and to make monthly distributions to shareholders. |

| Q: |

Who will manage the Combined Fund’s

portfolio?

|

| A: |

The

Combined Fund will be advised by aIL, the Acquiring Fund’s current adviser, and sub-advised by abrdn Inc., the Acquiring Fund’s

current sub-adviser. Furthermore, the Acquiring Fund’s current portfolio management team will be primarily responsible for

the day-to-day management of the Combined Fund’s portfolio. |

| Q: |

Will there be any significant portfolio

transitioning in connection with the Reorganizations?

|

| A: |

Each Acquired Fund is required to pay back its outstanding leverage in connection with the closing

of the Reorganization. It is anticipated that approximately 26% of FSD’s holdings and 20% of FAM’s holdings will be sold

by each respective Acquired Fund before the closing of the Reorganizations in order to pay back each Acquired Fund’s outstanding

leverage. As a result of the disposition of securities, each Acquired Fund may hold more uninvested cash than normal and there may

be times when each Acquired Fund is not fully invested in accordance with its investment objective and strategies. This may impact

each Acquired Fund’s performance. As of September 21, 2023, the expected costs to de-lever FSD’s portfolio would

be approximately $405,000 (or 0.08% of FSD’s NAV as of September 21, 2023) or $0.012 per share. As of September 21,

2023, the expected costs to de-lever FAM’s portfolio would be approximately $33,000 (or 0.04% of FAM’s NAV as of September 21,

2023) or $0.003 per share. To the extent an Acquired Fund has holdings in France, Spain and/or Italy, such countries may impose an

additional foreign transfer tax on the transfer of such securities to the Acquiring Fund. These taxes are in addition to the transaction

costs disclosed above and would be borne by the applicable Acquired Fund. The foregoing estimates are subject to change depending

on the composition of each Acquired Fund’s portfolio and market circumstances at the time any sales are made. |

|

Following the Reorganization, the Combined

Fund expects to realign its portfolio in a manner consistent with its investment strategies and policies, which will be the same

as the Acquiring Fund’s strategies and policies. The Combined Fund may not be invested consistent with its investment strategies

or aIL’s investment approach while such realignment occurs. The realignment is anticipated to take approximately one week following

the closing of the Reorganization, based on current market conditions and assuming that the Acquired Funds’ holdings are the

same as of September 21, 2023. Sales and purchases of less liquid securities could take longer. Based on the FSD and FAM holdings

as of September 21, 2023, the Combined Fund expects to sell approximately 99% of FAM’s portfolio following the closing

of the Reorganization. The Combined Fund currently does not expect to sell any of FSD’s portfolio following the closing of

the Reorganization. To the extent there are any transaction costs (including brokerage commissions, transaction charges and related

fees) associated with the sales and purchases made in connection with the Reorganization, these will be borne by the Acquired Fund

with respect to the portfolio transitioning conducted before the Reorganizations and borne by the Combined Fund with respect to the

portfolio transitioning conducted after the Reorganizations. The portfolio transitioning pre- and post-Reorganizations may result

in capital gains or losses, which may have federal income tax consequences for shareholders of the Acquired Funds and the Combined

Fund.

|

| Q: |

Will I have to pay any sales load or commission

in connection with the respective Reorganization?

|

| A: |

No. You will pay no sales load or commission

in connection with the respective Reorganization.

|

| Q: |

Who will pay for the costs associated

with each Reorganization?

|

| A: |

aIL and its affiliates and First Trust and

its affiliates will bear certain expenses incurred in connection with each Reorganization, whether or not the Reorganization is consummated.

The expenses of the Reorganizations are estimated to be approximately $589,000 for FSD and approximately $453,000 for FAM. To the

extent there are any transaction costs (including brokerage commissions, transaction charges and related fees) associated with the

sales and purchases made in connection with the Reorganizations, these will be borne by the applicable Acquired Fund with respect

to the portfolio transitioning and de-levering conducted before the Reorganizations and borne by the Combined Fund with respect to

the portfolio transitioning conducted after the Reorganizations. In addition, to the extent an Acquired Fund has holdings in France,

Spain and/or Italy, such countries may impose an additional foreign transfer tax on the transfer of such securities to the Acquiring

Fund. These taxes are in addition to the transaction costs disclosed above and would be borne by the applicable Acquired Fund.

|

| Q: |

Are the Reorganizations expected to be

taxable to the respective shareholders of each Acquired Fund?

|

| A: |

It is expected that shareholders of each

Acquired Fund will not recognize any gain or loss for federal income tax purposes as a result of the exchange of their shares in

the Acquired Fund for shares of the Acquiring Fund pursuant to the Reorganization Agreement (except with respect to cash received

in lieu of fractional shares of the Acquiring Fund).

As a condition to each Acquired Fund’s

obligation to consummate the Reorganization, each Acquired Fund and the Acquiring Fund will receive an opinion from legal counsel

to the effect that, on the basis of the existing provisions of the Internal Revenue Code of 1986, as amended (the “Code”),

current administrative rules and court decisions, the transactions contemplated by the respective Reorganization Agreement constitute

a tax-free reorganization for federal income tax purposes (except with respect to cash received in lieu of fractional shares of the

Acquiring Fund). Despite this opinion, there can be no assurances that the US Internal Revenue Service will deem the exchanges to

be tax-free.

The portfolio transitioning discussed above

may result in capital gains or losses, which may have federal income tax consequences.

|

| |

The portfolio de-levering

discussed above may result in capital gains or losses, which may have federal income tax

consequences. For example, if the de-levering of FSD was completed on September 21,

2023, it is estimated that approximately $16,821,000, or $0.505 per share, in capital losses

would have resulted from the sale of portfolio securities ahead of the Reorganization. If

the de-levering of FAM was completed on September 21, 2023, it is estimated that approximately

$2,261,000, or $0.223 per share, in capital losses would have resulted from the sale of portfolio

securities ahead of the Reorganization.

The portfolio transitioning

after the Reorganization discussed above may result in capital gains or losses, which may

have federal income tax consequences. For example, if the Reorganization of FAM only was

completed on September 21, 2023, it is estimated that approximately $10,756,000, or $0.088

per share, in capital losses would have resulted from portfolio transitioning in the Combined

Fund following the Reorganization. No sales of portfolio securities are anticipated after

the Reorganization as it relates to the FSD Reorganization.

The actual tax consequences

as a result of portfolio repositioning after the closing of the Reorganizations are dependent

on the portfolio composition of each Acquired Fund at the time of closing and market conditions.

Any net capital gain resulting from the realignment coupled with the results of the Acquiring

Fund’s normal operations during the tax year following the close of the Reorganizations

would be distributed to the shareholder base of the Combined Fund post-Reorganization in

connection with the annual distribution requirements under US federal tax laws. |

| Q: |

How do the Acquired Fund Boards suggest

that I vote?

|

| A: |

The Acquired Fund Boards recommend that you

vote “FOR” the respective Proposal.

|

| Q: |

How do I vote my proxy? |

| |

|

| A: |

You may vote in any one of four ways: |

| · | by

mail, by sending the enclosed proxy card, signed and dated, in the enclosed envelope; |

| · | by

phone, by following the instructions set forth on your proxy card; |

| · | via

the Internet, by following the instructions set forth on your proxy card; or |

| · | in

person, by attending the Special Meeting. Please note that shareholders who intend

to attend the Special Meeting will need to provide valid identification and, if they hold

shares through a bank, broker or other nominee, satisfactory proof of ownership of shares,

such as a voting instruction form (or a copy thereof) or a letter from their bank, broker

or other nominee or broker’s statement indicating ownership as of October 23, 2023

(the record date), to be admitted to the Special Meeting. |

|

Broker-dealer firms holding shares in “street

name” for the benefit of their customers and clients may request voting instructions from such customers and clients. You are

encouraged to contact your broker-dealer and record your voting instructions. |

| |

|

| Q: |

Whom do I contact for further information?

|

| A: |

If you

need any assistance or have any questions regarding the Proposals or how to vote your shares, please call EQ Fund Solutions, LLC,

the Acquired Fund’s proxy solicitor, at [ ] weekdays from 9:00 a.m. to 10:00 p.m. Eastern Time. |

It

is important that your shares be represented at the Special Meeting. In order to avoid delay and to ensure that your shares

are represented, please vote as promptly as possible.

The information

in this Proxy Statement/Prospectus is not complete and may be changed. We may not sell these securities until the registration statement

filed with the Securities and Exchange Commission is effective. This Proxy Statement/Prospectus is not an offer to sell these securities

and it is not soliciting an offer to buy these securities in any state where the offer of sale is not permitted.

Subject to Completion

October 24, 2023

PROXY STATEMENT FOR

FIRST TRUST HIGH INCOME LONG/SHORT FUND

FIRST TRUST/ABRDN GLOBAL OPPORTUNITY INCOME

FUND

120 East Liberty Drive, Suite 400

Wheaton, IL 60187

(630) 765-8000

PROSPECTUS FOR

ABRDN INCOME CREDIT STRATEGIES FUND

1900 Market Street, Suite 200

Philadelphia, PA 19103

(215) 405-5700

[ ], 2023

This combined proxy statement/prospectus

(the “Proxy Statement/Prospectus”) is furnished to you as a common shareholder of each of or either of First Trust High

Income Long/Short Fund (“FSD”) and First Trust/abrdn Global Opportunity Income Fund (“FAM”), each a

Massachusetts business trust and closed-end management investment company registered under the Investment Company Act of 1940, as

amended (the “1940 Act”) (each, an “Acquired Fund” and, collectively, the “Acquired Funds”).

Special Meetings (with any postponements or adjournments, each a “Special Meeting” and, collectively, the “Special

Meetings”) of shareholders of each Acquired Fund are scheduled to be held at the offices of the Acquired Fund’s

investment adviser, First Trust Advisors L.P. (“First Trust”), located at 120 East Liberty Drive, Suite 400,

Wheaton, Illinois 60187, on [ ], 2024, at [ ] Central Time for FSD and at [ ] Central Time for FAM. At the Special Meeting,

shareholders will be asked to consider and to vote on the below proposals (each a “Proposal” and, collectively, the

“Proposals”). If you are unable to attend the Special Meeting, the Board of Trustees of FSD and the Board of Trustees of

FAM (each a “Board” and, collectively, the “Boards”) requests that you vote your shares by completing and

returning the enclosed proxy card or by recording your voting instructions by telephone or via the Internet. The approximate mailing

date of this Proxy Statement/Prospectus is [ ], 2023.

For shareholders of FSD:

To approve an Agreement and Plan of Reorganization

providing for the transfer of all of the assets of FSD to abrdn Income Credit Strategies Fund (the “Acquiring Fund”) in exchange

solely for newly issued common shares of beneficial interest of the Acquiring Fund (although cash may be distributed in lieu of fractional

shares of the Acquiring Fund) and the assumption by the Acquiring Fund of all liabilities of FSD and the distribution of common shares

of beneficial interest of the Acquiring Fund to the shareholders of FSD and complete liquidation of FSD (the “FSD Reorganization”)

For shareholders of FAM:

To approve an Agreement and Plan of Reorganization

providing for the transfer of all of the assets of FAM to abrdn Income Credit Strategies Fund (the “Acquiring Fund”) in exchange

solely for newly issued common shares of beneficial interest of the Acquiring Fund (although cash may be distributed in lieu of fractional

shares of the Acquiring Fund) and the assumption by the Acquiring Fund of all liabilities of FAM and the distribution of common shares

of beneficial interest of the Acquiring Fund to the shareholders of FAM and complete liquidation of FAM (the “FAM Reorganization”)

Shareholders of record as of the close of business

on October 23, 2023, the record date (the “Record Date”), are entitled

to notice of and to vote at the Special Meeting.

Shareholders of each Acquired Fund are being

asked to consider and vote on an Agreement and Plan of Reorganization (each a “Reorganization Agreement” and, collectively,

the “Reorganization Agreements”) pursuant to which each Reorganization would be accomplished. The aggregate NAV (not the

market value) of Acquiring Fund common shares received by the shareholders of each Acquired Fund in the Reorganization would equal the

aggregate NAV (not the market value) of the respective Acquired Fund common shares held immediately prior to the respective Reorganizations

(although shareholders may receive cash for fractional shares of the Acquiring Fund, which may be taxable). It is important to note that

the Reorganization of an Acquired Fund is not contingent on the approval of the other Acquired Fund’s shareholders (i.e., a Reorganization

of one of the Acquired Funds, if approved by that Acquired Fund’s shareholders, may still proceed if the other Reorganization is

not approved by the other Acquired Fund’s shareholders). The Acquiring Fund as it would exist after one or both Reorganizations

is referred to as the “Combined Fund.”

At the closing of each Reorganization, each Reorganization

Agreement sets forth that the Acquired Fund assets will be valued in accordance with the Acquired Fund’s valuation procedures as

approved by the Board of the Acquired Fund. Upon the consummation of the Reorganization, the assets transferred to the Acquiring Fund

will be valued pursuant to the Acquiring Fund’s valuation procedures as approved by the Board of Trustees of the Acquiring Fund.

The valuation procedures for the Acquired Funds, on the one hand, and the Acquiring Fund, on the other hand differ in certain respects.

For purposes of determining an Acquired Fund’s

net asset value, corporate, sovereign, government, foreign, mortgage backed, and capital preferred fixed income securities and senior

floating rate bank loans are priced at the mean of evaluated bid and asked prices provided by third-party pricing vendors on the valuation

date. In contrast, the Acquiring Fund values such securities at the bid price provided by third-party pricing vendors.

If a Reorganization is approved by shareholders

and assuming that FSD’s and FAM’s fixed income holdings are not sold in advance of the respective Reorganization, the net

asset value per share of the Acquiring Fund will be less than the net asset value per share of the respective Acquired Fund. For example,

if ACP’s valuation procedures were used to value FSD and FAM’s fixed income security holdings as of September 29, 2023,

the value of the Combined Fund’s shares is estimated to be reduced by approximately $1,052,639 (0.13% of the Combined Fund as of

September 29, 2023) or $0.009 per share of the Combined Fund, assuming both Reorganizations are consummated.

Separately, the shareholders of the Acquiring

Fund are being asked to approve the issuance of additional common shares of the Acquiring Fund in connection with the Reorganizations.

Completion of each Reorganization requires both the approval of the respective Acquired Fund shareholders of the respective Reorganization

Agreement and the Acquiring Fund shareholders of the issuance of Acquiring Fund common shares.

There are differences between each Acquired Fund

and the Acquiring Fund. In particular, they have different investment advisers. First Trust Advisors L.P. (previously defined as “First

Trust”) is the investment manager of each Acquired Fund. MacKay Shields LLC (“MacKay”) is the sub-adviser of FSD and

abrdn Inc. is the sub-adviser of FAM. aIL is the investment adviser of the Acquiring Fund and abrdn Inc. is the investment sub-adviser

of the Acquiring Fund. The Funds have similar investment objectives, principal investment strategies and principal risks, with some differences.

The Acquiring Fund and FAM have investment objectives that are materially the same. FSD’s primary investment objective is to provide

current income, with a secondary objective of capital appreciation. Each of FAM’s and the Acquiring Fund’s primary investment

objective is to is to seek a high level of current income with a secondary objective of capital appreciation.

The common shares of the Acquiring Fund are listed

on the New York Stock Exchange (the “NYSE”) under the ticker symbol “ACP” and will continue to be so listed following

the Reorganizations. The common shares of FSD are listed on the NYSE under the ticker symbol “FSD” and the common shares

of FAM are listed on the NYSE under the ticker symbol “FAM”. Common shares of each Acquired Fund would be delisted from the

NYSE following the Reorganization. Shareholder reports, proxy statements and other information concerning Funds can be inspected at the

NYSE.

The following documents have been filed with

the Securities and Exchange Commission (“SEC”):

| |

· |

the Statement of Additional Information,

dated [ ], 2023, relating to this Proxy Statement/Prospectus is incorporated

into this Proxy Statement/Prospectus by reference;

|

| |

· |

the

Semi-Annual Report to shareholders of FSD for the fiscal period ended April 30, 2023 (Investment Company Act File No. 811-22442;

Accession Number 0001445546-23-004198); |

| |

· |

the

Annual Report to shareholders of FSD for the fiscal period ended October 31, 2022

(Investment Company Act File No. 811-22442; Accession Number 0001445546-23-000101);

|

| |

· |

the

Semi-Annual Report to shareholders of FAM for the fiscal period ended June 30, 2023 (Investment Company Act File No. 811-21636;

Accession Number 0001445546-23-005506);

|

| |

· |

the

Annual Report to shareholders of FAM for the fiscal period ended December 31, 2022

(Investment Company Act File No. 811-21636; Accession Number 0001445546-23-001824);

|

| |

· |

the

Semi-Annual Report to shareholders of the Acquiring Fund for the fiscal period ended April 30,

2023 (Investment Company Act File No. 811-22485; Accession Number

0001104659-23-079589); and

|

| |

· |

the

Annual Report to shareholders of the Acquiring Fund for the fiscal period ended October 31,

2022 (Investment Company Act File No. 811-22485; Accession Number

0001104659-23-002299). |

Additionally, copies of the foregoing and any

more recent reports filed after the date hereof may be obtained without charge:

for the Acquiring Fund:

| By Phone: |

1-800-522-5465 |

| By Mail: |

abrdn Income Credit Strategies

Fund |

| |

c/o abrdn Inc.

1900 Market Street, Suite 200 |

| |

Philadelphia, PA 19103 |

| By

Internet: |

www.abrdnacp.com |

for FSD:

| By Phone: |

(630) 765-8000 |

| By Mail: |

First Trust High Income Long/Short

Fund |

| |

120 East Liberty Drive, Suite 400 |

| |

Wheaton, IL 60187 |

| By

Internet: |

www.ftportfolios.com |

for FAM:

| By Phone: |

(630) 765-8000 |

| By Mail: |

First Trust/abrdn Global Opportunity

Income Fund |

| |

120 East Liberty Drive, Suite 400 |

| |

Wheaton, IL 60187 |

| By

Internet: |

www.ftportfolios.com |

The Funds are subject to the informational requirements

of the Securities Exchange Act of 1934 (the “Exchange Act”), as amended, and, in accordance therewith, file reports, proxy

statements, proxy materials and other information with the SEC. You also may view or obtain the foregoing documents from the SEC:

| By e-mail: |

publicinfo@sec.gov

(duplicating fee required) |

| By Internet: |

www.sec.gov |

This Proxy Statement/Prospectus serves as a prospectus

of the Acquiring Fund. This Proxy Statement/Prospectus sets forth concisely the information that shareholders of the Acquired Funds should

know before voting on the Proposals. Please read it carefully and retain it for future reference. No person has been authorized to give

any information or make any representation not contained in this Proxy Statement/Prospectus and, if so given or made, such information

or representation must not be relied upon as having been authorized. This Proxy Statement/Prospectus does not constitute an offer to

sell or a solicitation of an offer to buy any securities in any jurisdiction in which, or to any person to whom, it is unlawful to make

such offer or solicitation.

THE SEC HAS NOT APPROVED OR DISAPPROVED THESE

SECURITIES OR PASSED UPON THE ADEQUACY OF THIS PROXY STATEMENT/PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

TABLE OF CONTENTS

| PROPOSALS |

6 |

| |

|

| COMPARISON

OF THE FUNDS |

16 |

| |

|

| MANAGEMENT

OF THE FUNDS |

53 |

| |

|

| AGREEMENT

BETWEEN First Trust Advisors L.P. AND ABRDN INC. |

57 |

| |

|

| NET

ASSET VALUE OF COMMON SHARES of the acquiring fund |

63 |

| |

|

| DIVIDEND

REINVESTMENT AND OPTIONAL CASH PURCHASE PLAN |

63 |

| |

|

| ANTI-TAKEOVER

AND CERTAIN PROVISIONS OF THE ACQUIRING FUND’S AGREEMENT AND DECLARATION OF TRUST AND BYLAWS |

65 |

| |

|

| APPRAISAL

RIGHTS |

66 |

| |

|

| FINANCIAL

HIGHLIGHTS |

66 |

| |

|

| INFORMATION

ABOUT THE REORGANIZATION |

70 |

| |

|

| TERMS

OF THE REORGANIZATION AGREEMENT |

70 |

| |

|

| MATERIAL

FEDERAL INCOME TAX CONSEQUENCES OF THE REORGANIZATIONS |

71 |

| |

|

| VOTING

INFORMATION AND REQUIREMENTS |

73 |

| |

|

| SHAREHOLDER

INFORMATION |

75 |

| |

|

| SHAREHOLDER

PROPOSALS |

76 |

| |

|

| SOLICITATION

OF PROXIES |

76 |

| |

|

| OTHER

BUSINESS |

76 |

| |

|

| APPENDIX

A: FORMS OF AGREEMENT AND PLAN OF REORGANIZATION |

A-1 |

PROPOSALS

For shareholders of FSD:

To approve an Agreement and Plan of

Reorganization providing for the transfer of all of the assets of FSD to abrdn Income Credit Strategies Fund (the “Acquiring Fund”)

in exchange solely for newly issued common shares of beneficial interest of the Acquiring Fund (although cash may be distributed in lieu

of fractional shares of the Acquiring Fund) and the assumption by the Acquiring Fund of all liabilities of FSD and the distribution of

common shares of beneficial interest of the Acquiring Fund to the shareholders of FSD and complete liquidation of FSD (the “FSD

Reorganization”)

For shareholders of FAM:

To approve an Agreement and Plan of

Reorganization providing for the transfer of all of the assets of FAM to abrdn Income Credit Strategies Fund (the “Acquiring Fund”)

in exchange solely for newly issued common shares of beneficial interest of the Acquiring Fund (although cash may be distributed in lieu

of fractional shares of the Acquiring Fund) and the assumption by the Acquiring Fund of all liabilities of FAM and the distribution of

common shares of beneficial interest of the Acquiring Fund to the shareholders of FAM and complete liquidation of FAM (the “FAM

Reorganization”)

Synopsis

The Board of each Acquired Fund, including trustees

who are not “interested persons” of each Acquired Fund (as defined in the 1940 Act) (the “Independent Trustees”),

have approved the respective Reorganization Agreement. The Acquiring Fund as it would exist after one or both Reorganizations is referred

to as the “Combined Fund.”

Subject to approval of the respective Reorganization

Agreements by the shareholders of the respective Acquired Funds and of the issuance of Acquiring Fund common shares by the shareholders

of the Acquiring Fund, the Reorganization Agreements provide for:

| · | the

transfer of all of the assets of each Acquired Fund to the Acquiring Fund, in exchange solely

for shares of the Acquiring Fund (although cash may be distributed in lieu of fractional

shares of the Acquiring Fund); |

| · | the

assumption by the Acquiring Fund of all liabilities of each Acquired Fund; |

| · | the

distribution of common shares of the Acquiring Fund to the shareholders of each Acquired

Fund; and |

| · | the

complete liquidation of each Acquired Fund. |

It is currently expected that each Reorganization

will occur in the first quarter of 2024.

The Reorganization of an Acquired Fund is not

contingent on the approval of the other Acquired Fund’s shareholders (i.e., a Reorganization of one of the Acquired Funds, if approved

by that Acquired Fund’s shareholders, may still proceed if the other Reorganization is not approved by the other Acquired Fund’s

shareholders).

At the closing of each Reorganization, each Reorganization

Agreement sets forth that the Acquired Fund assets will be valued in accordance with the Acquired Fund’s valuation procedures as

approved by the Board of the Acquired Fund. Upon the consummation of the Reorganization, the assets transferred to the Acquiring Fund

will be valued pursuant to the Acquiring Fund’s valuation procedures as approved by the Board of Trustees of the Acquiring Fund.

The valuation procedures for the Acquired Funds, on the one hand, and the Acquiring Fund, on the other hand, differ in certain respects.

For purposes of determining an Acquired Fund’s

net asset value, corporate, sovereign, government, foreign, mortgage backed, and capital preferred fixed income securities and senior

floating rate bank loans are priced at the mean of evaluated bid and asked prices provided by third-party pricing vendors on the valuation

date. In contrast, the Acquiring Fund values such securities at the bid price provided by third-party pricing vendors.

If a Reorganization is approved by shareholders

and assuming that FSD’s and FAM’s fixed income holdings are not sold in advance of the respective Reorganization, the net

asset value per share of the Acquiring Fund will be less than the net asset value per share of the respective Acquired Fund. For example,

if ACP’s valuation procedures were used to value FSD and FAM’s fixed income security holdings as of September 29, 2023,

the value of the Combined Fund’s shares is estimated to be reduced by approximately $1,052,639 (0.13% of the Combined Fund as of

September 29, 2023) or $0.009 per share of the Combined Fund, assuming both Reorganizations are consummated.

Each Acquired Fund is required to pay back its

outstanding leverage in connection with the closing of the Reorganization. It is anticipated that approximately 26% of FSD’s holdings

and approximately 20% of FAM’s holdings will be sold by such Acquired Fund before the closing of the Reorganization in order to

pay back each Acquired Fund’s outstanding leverage. This portfolio transition may take a significant amount of time and result

in the Acquired Fund holding large amounts of uninvested cash. As a result, there may be times when an Acquired Fund is not pursuing

its investment objective or is not being managed consistent with its investment strategies. This may impact each Acquired Fund’s

performance. Following the Reorganization, the Combined Fund expects to realign its portfolio in a manner consistent with its investment

strategies and policies, which will be the same as the Acquiring Fund’s strategies and policies. The Combined Fund may not be invested

consistent with its investment strategies or the adviser’s investment approach while such realignment occurs. The realignment is

anticipated to take approximately one week, based on current market conditions and assuming that the Acquired Funds’ holdings are

the same as of September 21, 2023. Sales and purchases of less liquid securities could take longer.

The portfolio de-levering discussed above may

result in capital gains or losses, which may have federal income tax consequences. For example, if the de-levering of FSD was completed

on September 21, 2023, it is estimated that approximately $16,821,000, or $0.505 per share, in capital losses would have resulted

from the sale of portfolio securities ahead of the Reorganization. If the de-levering of FAM was completed on September 21, 2023,

it is estimated that approximately $2,261,000, or $0.223 per share, in capital losses would have resulted from the sale of portfolio

securities ahead of the Reorganization.

Based on the FSD and FAM holdings as of September 21,

2023, the Combined Fund expects to sell approximately 99% of FAM’s portfolio following the closing of the Reorganization. The Combined

Fund currently does not expect to sell any of FSD’s portfolio following the closing of the Reorganization. To the extent there

are any transaction costs (including brokerage commissions, transaction charges and related fees) associated with the sales and purchases

made in connection with the Reorganizations, these will be borne by the Acquired Fund with respect to the portfolio transitioning conducted

before the Reorganizations and borne by the Combined Fund with respect to the portfolio transitioning conducted after the Reorganizations.

To the extent an Acquired Fund has holdings in France, Spain and/or Italy, such countries may impose an additional foreign transfer tax

on the transfer of such securities to the Acquiring Fund. These taxes are in addition to the transaction costs disclosed above and would

be borne by the applicable Acquired Fund.

The portfolio transitioning after the Reorganization

discussed above may result in capital gains or losses, which may have federal income tax consequences. For example, if the Reorganization

of FAM only was completed on September 21, 2023, it is estimated that approximately $10,756,000, or $0.088 per share, in capital losses

would have resulted from portfolio transitioning in the Combined Fund following the Reorganization. No sales of portfolio securities

are anticipated after the Reorganization as it relates to the FSD Reorganization. The actual tax consequences as a result of portfolio

repositioning after the closing of the Reorganizations are dependent on the portfolio composition of each Acquired Fund at the time of

closing and market conditions. Any net capital gain resulting from the realignment coupled with the results of the Acquiring Fund’s

normal operations during the tax year following the close of the Reorganizations would be distributed to the shareholder base of the

Combined Fund post-Reorganization in connection with the annual distribution requirements under US federal tax laws.

FSD seeks to achieve its investment objectives

by investing, under normal market conditions, a majority of its assets in a diversified portfolio of U.S. and foreign (including emerging

markets) high-yield corporate fixed-income securities of varying maturities that are rated below investment grade at the time of purchase.

As part of its investment strategy, FSD maintains both long and short positions in securities under normal market conditions. The Fund’s

long positions, either directly or through derivatives, may total up to 130% of the Fund’s managed assets. The Fund’s short

positions, either directly or through derivatives, may total up to 30% of the Fund’s managed assets. The Fund’s use of derivatives,

other than for hedging purposes, will not exceed 30% of the Fund’s managed assets.

FSD may invest up to 5% of its Managed Assets

(defined below) in common stocks, including those of foreign issuers. FSD may invest up to 20% of its Managed Assets in securities that,

at the time of investment, are illiquid. FSD may also invest, without limit, in securities that are unregistered (but are eligible for

purchase and sale by certain qualified institutional buyers) or are held by control persons of the issuer and securities that are subject

to contractual restrictions on their resale (“restricted securities”). However, restricted securities determined to be illiquid

are subject to the limitations set forth above.

FAM seeks to achieve its investment objectives

by investing, under normal circumstances, substantially all of its Managed Assets (defined below) in a diversified portfolio of fixed-income

securities, including government and corporate bonds, of U.S. and non-U.S. issuers. FAM’s investment team believes that a portfolio

containing investment grade securities that invests across many national markets has the opportunity to achieve returns in excess of

a portfolio that invests in a single domestic bond market, as the global fixed-income marketplace is generally less efficient than domestic

markets. Under normal market conditions, FAM invests in securities of issuers in at least three countries (in addition to the United

States), however, securities of issuers in a single country will not exceed 30% of the FAM’s Managed Assets. The Fund invests at

least 60% of its Managed Assets in securities issued by government, government-related and supranational issuers (“government debt”).

At least 25% of the Fund’s Managed Assets will be invested in U.S. dollar-denominated securities or non-U.S. dollar-denominated

securities that have been fully hedged into U.S. dollars. FAM may also invest up to 10% of its Managed Assets in forward foreign currency

exchange contracts for hedging and investment purposes. FAM places thresholds of the proportion of its Managed Assets that may be invested

in corporate debt obligations, below investment grade securities, asset-backed securities, credit-linked notes, illiquid securities,

and forward foreign exchange contracts (both deliverable and non-deliverable).

For purposes of FAM’s investment strategies,

“Managed Assets” means the total asset value of FAM minus the sum of FAM’s liabilities other than the principal amount

of borrowings, if any. For purposes of FSD’s investment strategies, “Managed Assets” means the average daily gross

asset value of FSD (which includes the principal amount of any borrowings), minus the sum of FSD’s liabilities.

The Acquiring Fund is a high yield debt fund

that is permitted to invest in a variety of US and foreign-issued debt instruments, and may utilize derivatives and hedging techniques,

to achieve its investment objectives. The Acquiring Fund generally invests in corporate bonds and is permitted to invest in senior loans

and in second lien or other subordinated loans or debt instruments, including non-stressed and stressed credit obligations, and related

derivatives. The Acquiring Fund seeks to capitalize on market inefficiencies and to reallocate the portfolio of the Acquiring Fund to

opportunistically emphasize those investments, categories of investments and geographic exposures believed to be best suited to the current