UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-22455

Cohen & Steers Select Preferred and Income Fund, Inc.

(Exact name of Registrant as specified

in charter)

1166 Avenue of the Americas, 30th Floor, New York, NY 10036

(Address of principal executive

offices) (Zip code)

Dana A. DeVivo

Cohen & Steers Capital Management, Inc.

1166 Avenue of the Americas, 30th Floor

New York, New York 10036

(Name and address of agent for service)

Registrant’s telephone number, including area code: (212)

832-3232

Date of fiscal year

end: December 31

Date of reporting period: December 31,

2023

Item 1. Reports to Stockholders.

COHEN

& STEERS SELECT PREFERRED

AND INCOME FUND, INC.

To Our Shareholders:

We would like to share with you our report for the year ended December 31, 2023. The total returns for Cohen & Steers Select

Preferred and Income Fund, Inc. (the Fund) and its comparative benchmarks were:

|

|

|

|

|

|

|

|

|

| |

|

Six Months Ended

December 31, 2023 |

|

|

Year Ended

December 31, 2023 |

|

| Cohen & Steers Select Preferred and Income Fund at Net Asset Value(a) |

|

|

10.34 |

% |

|

|

7.99 |

% |

| Cohen & Steers Select Preferred and Income Fund at Market Value(a) |

|

|

8.40 |

% |

|

|

9.72 |

% |

| ICE BofA Fixed Rate Preferred Securities Index(b) |

|

|

5.36 |

% |

|

|

10.21 |

% |

| Blended

Benchmark(b) |

|

|

6.97 |

% |

|

|

8.21 |

% |

| Bloomberg U.S. Aggregate Bond

Index(b) |

|

|

3.37 |

% |

|

|

5.53 |

% |

The performance data quoted represent past performance. Past performance is no guarantee of

future results. The investment return and the principal value of an investment will fluctuate and shares, if sold, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted.

Performance results reflect the effects of leverage, resulting from borrowings under a credit agreement. Current total returns of the Fund can be obtained by visiting our website at cohenandsteers.com. The Fund’s returns assume the reinvestment

of all dividends and distributions at prices obtained under the Fund’s dividend reinvestment plan. Index performance does not reflect the deduction of any fees, taxes or expenses. An investor cannot invest directly in an index. Performance

figures for periods shorter than one year are not annualized.

Distribution Policy

Effective July 1, 2023, the Fund adopted a policy to make regular monthly distributions at a level rate (the Policy), which

replaced the Fund’s previous managed distribution policy (the Plan). The Fund expects that these distributions will continue to be declared and announced on a quarterly basis. As a result of the Policy, the Fund may pay distributions in excess

of its investment company taxable income and realized gains. This excess would be a return of capital distributed from the Fund’s assets. Distributions of capital decrease the Fund’s total assets and, therefore, could have the effect of

increasing the Fund’s expense ratio. In order to make these distributions, the Fund may have to sell portfolio securities at a less opportune time, which could have an adverse effect on the market price of the Fund’s shares. The Board may

amend or terminate the Policy, or re-adopt a managed distribution plan, at any time without prior notice to shareholders. In accordance with the Plan, the Fund distributed $0.135 per share on a monthly basis through June 30, 2023. Effective

July 1, 2023, in accordance with the Policy, the Fund distributed $0.126 per share on a monthly basis.

| (a) |

As a closed-end investment company, the price of the Fund’s exchange-traded shares will be set

by market forces and can deviate from the net asset value (NAV) per share of the Fund. |

| (b) |

For benchmark descriptions, see page 6. |

1

COHEN

& STEERS SELECT PREFERRED

AND INCOME FUND, INC.

Under the Plan, the Fund’s monthly

distributions could include long-term capital gains, short-term capital gains, net investment income and/or return of capital for federal income tax purposes. Return of capital includes distributions paid by the Fund in excess of its net investment

income and net realized capital gains and such excess is distributed from the Fund’s assets. A return of capital is not taxable; rather, it reduces a shareholder’s tax basis in his or her shares of the Fund. The amount of monthly

distributions may vary depending on a number of factors, including changes in portfolio and market conditions.

Market Review

The 12 months ended December 31, 2023 were mostly favorable for financial markets amid better-than-expected

economic resilience. Stocks and credit-sensitive fixed income assets had generally solid returns in this environment, while more rate-sensitive assets such as government bonds had relatively modest gains, hindered at times by volatility in interest

rates. Bond yields rose sharply through most of the period as the U.S. Federal Reserve and other central banks continued to raise interest rates in an effort to contain inflation. Yields declined late in the year as central banks highlighted

progress related to inflation targets, suggesting paths to begin lowering rates in 2024, even if the timing and magnitude of such cuts were unclear. The yield on the 10-year U.S. Treasury retreated to 3.9% by

year end, about where it stood at the start of 2023 after peaking near 5.0% in October.

In this environment, preferreds

had a gain as a group and outperformed Treasuries, but trailed more credit-sensitive high-yield debt.

Fund Performance

The Fund had a positive total return in the period but underperformed its blended benchmark on a net asset value

basis (the Fund outperformed the blended benchmark based on market price).

In the U.S., the sudden collapse of Silicon

Valley Bank, Signature Bank and First Republic Bank in early 2023 raised concerns about funding and contagion risk. In Europe, struggling Credit Suisse was acquired by rival UBS in March. Financial regulators took swift action to mitigate contagion

risk; the Fed and other central banks assured that funding would remain readily available in the global banking system.

Concerns around these events eased as the period progressed and fundamentals of the broader banking system remained healthy and

resilient. Industry data and individual company comments suggested that the well-publicized U.S. regional bank failures were idiosyncratic and not reflective of systemic risk. Credit Suisse, meanwhile, appeared to be an outlier among European banks.

Overall, the banking sector in the U.S. and Europe continued to generate solid profitability and strong capitalization.

Security selection in the banking sector detracted from relative performance. While security selection among non-U.S. banks was favorable (including a contribution from an underweight in issues of Credit Suisse), this was more than offset by security selection in U.S. banks, due in part to out-of-benchmark investments in issues from Silicon Valley Bank.

The insurance

sector performed well during the period. Property & casualty insurance companies experienced significant premium growth due to the recovering economy, while life insurers benefited from the declining impact of the Covid pandemic. The

Fund’s underweight in insurance hindered relative performance, although the effect was largely offset by favorable security selection in that sector.

2

COHEN

& STEERS SELECT PREFERRED

AND INCOME FUND, INC.

The pipeline sector had a solid absolute

return as company cash flows improved, supported by recovering demand and high crude oil and refined product prices. Utilities also outperformed. The Fund’s overweights and security selection in both sectors contributed to relative performance.

Impact of Leverage on Fund Performance

The Fund employs leverage as part of a yield-enhancement strategy. Leverage, which can increase total return in rising markets

(just as it can have the opposite effect in declining markets), contributed significantly to the Fund’s performance for the 12 months ended December 31, 2023.

Impact of Derivatives on Fund Performance

In connection with its use of leverage, the Fund pays interest on its borrowings based on a floating rate under the terms of its

credit agreement. To reduce the impact that an increase in interest rates could have on the performance of the Fund with respect to these borrowings, the Fund used interest rate swaps to exchange a portion of the floating rate for a fixed rate. The

Fund also used total return swaps with the intention of managing credit risk. The Fund’s use of interest rate swaps contributed to the Fund’s total return for the 12 months ended December 31, 2023, while the total return swaps

had essentially no effect.

The Fund used forward foreign currency exchange contracts for managing currency risk on

certain Fund positions denominated in foreign currencies. The currency forwards did not have a material effect on the Fund’s total return for the 12 months ended December 31, 2023.

Sincerely,

|

|

|

|

|

|

| WILLIAM F. SCAPELL

Portfolio Manager |

|

ELAINE ZAHARIS-NIKAS

Portfolio Manager |

|

|

| JERRY DOROST

Portfolio Manager |

3

COHEN

& STEERS SELECT PREFERRED

AND INCOME FUND, INC.

The views and opinions in the preceding

commentary are subject to change without notice and are as of the date of the report. There is no guarantee that any market forecast set forth in the commentary will be realized. This material represents an assessment of the market environment at a

specific point in time, should not be relied upon as investment advice and is not intended to predict or depict performance of any investment.

Visit Cohen & Steers online at cohenandsteers.com

For more information about the Cohen & Steers family of mutual funds, visit cohenandsteers.com. Here you will

find fund net asset values, fund fact sheets and portfolio highlights, as well as educational resources and timely market updates.

Our website also provides comprehensive information about Cohen & Steers, including our

most recent press releases, profiles of our senior investment professionals and their investment approach to each asset class. The Cohen & Steers family of mutual funds specializes in liquid real assets, including real estate securities, listed

infrastructure and natural resource equities, as well as preferred securities and other income solutions.

4

COHEN

& STEERS SELECT PREFERRED

AND INCOME FUND, INC.

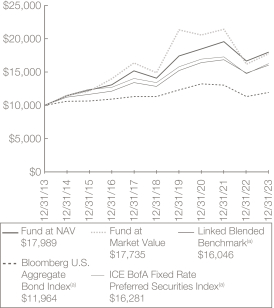

Performance Review (Unaudited)

Growth of a $10,000 Investment

Average Annual Total Returns—For Periods Ended December 31, 2023

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

1 Year |

|

|

5 Years |

|

|

10 Years |

|

|

Since Inception(b) |

|

|

Fund at NAV |

|

|

7.99 |

% |

|

|

5.00 |

% |

|

|

6.05 |

% |

|

|

7.49 |

% |

|

Fund at Market Value |

|

|

9.72 |

% |

|

|

3.53 |

% |

|

|

5.90 |

% |

|

|

6.51 |

% |

The performance data quoted represent past performance. Past performance is no guarantee of future results. The

investment return will vary and the principal value of an investment will fluctuate and shares, if sold, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance

results reflect the effect of leverage from utilization of borrowings under a credit agreement. Current total returns of the Fund can be obtained by visiting our website at cohenandsteers.com. The Fund’s returns assume the reinvestment of all

dividends and distributions at prices obtained under the Fund’s dividend reinvestment plan. The performance graph and table do not reflect the deduction of brokerage commissions or taxes that a shareholder would pay on Fund distributions or the

sale of Fund shares.

5

COHEN &

STEERS SELECT PREFERRED AND INCOME FUND, INC.

Performance Review (Unaudited)—(Continued)

| (a) |

The Linked Blended Benchmark is represented by the performance of the blended benchmark consisting

of 50% ICE BofA U.S. Capital Securities Index and 50% ICE BofA Fixed Rate Preferred Securities Index through December 31, 2016; the blended benchmark consisting of 60% ICE BofA U.S. IG Institutional Capital Securities Index, 30% ICE BofA Core

Fixed Rate Preferred Securities Index and 10% Bloomberg Developed Market USD Contingent Capital Index through December 31, 2018; and the blended benchmark consisting of 60% ICE BofA U.S. IG Institutional Capital Securities Index, 20% ICE BofA

Core Fixed Rate Preferred Securities Index and 20% Bloomberg Developed Market USD Contingent Capital Index through March 31, 2022; and the blended benchmark consisting of 55% ICE BofA U.S. IG Institutional Capital Securities Index, 20% ICE BofA Core

Fixed Rate Preferred Securities Index and 25% Bloomberg Developed Market USD Contingent Capital Index thereafter. |

| |

The ICE BofA U.S. Capital Securities Index is a subset of the ICE BofA U.S. Corporate Index

including securities with deferrable coupons. The ICE BofA Fixed Rate Preferred Securities Index tracks the performance of fixed-rate U.S. dollar-denominated preferred securities issued in the U.S. domestic market. The ICE BofA US IG Institutional

Capital Securities Index tracks the performance of US dollar denominated investment-grade hybrid capital corporate and preferred securities publicly issued in the US domestic market. The ICE BofA Core Fixed Rate Preferred Securities Index tracks the

performance of fixed-rate U.S. dollar denominated preferred securities issued in the U.S. domestic market, excluding $1,000 par securities. The Bloomberg Developed Market USD Contingent Capital Index includes hybrid capital securities in developed

markets with explicit equity conversion or write down loss absorption mechanisms that are based on an issuer’s regulatory capital ratio or other explicit solvency-based triggers. The Bloomberg US Aggregate Bond Index is a broad-market measure

of the U.S. dollar-denominated investment-grade fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, mortgage-backed securities, asset-backed securities, and commercial mortgage-backed

securities. Benchmark returns are shown for comparative purposes only and may not be representative of the Fund’s portfolio. |

| |

The comparative indexes are not adjusted to reflect expenses or other fees that the U.S. Securities

and Exchange Commission (SEC) requires to be reflected in the Fund’s performance. Index performance does not reflect the deduction of any fees, taxes or expenses. An investor cannot invest directly in an index. The Fund’s performance

assumes dividends and distributions are reinvested at prices obtained under the Fund’s dividend reinvestment plan. |

| (b) |

Commencement of investment operations is November 24, 2010. |

6

COHEN

& STEERS SELECT PREFERRED

AND INCOME FUND, INC.

Our Leverage Strategy

(Unaudited)

Our current leverage strategy utilizes borrowings up to the maximum

permitted by the Investment Company Act of 1940 to provide additional capital for the Fund, with an objective of increasing net income available for shareholders. As of December 31, 2023, leverage represented 35% of the Fund’s managed assets.

Through a combination of variable rate financing and interest rate swaps, the Fund has locked in

interest rates on a significant portion of this additional capital through 2027 (where we effectively reduce our variable rate obligation and lock in our fixed rate obligation over various terms). Locking in a significant portion of our leveraging

costs is designed to protect the dividend-paying ability of the Fund. The use of leverage increases the volatility of the Fund’s NAV in both up and down markets. However, we believe that locking in portions of the Fund’s leveraging costs

for the various terms partially protects the Fund’s expenses from an increase in short-term interest rates.

Leverage Facts(a)(b)

|

|

|

|

|

| Leverage (as a % of managed assets) |

|

|

35% |

|

| % Variable Rate Financing |

|

|

16% |

|

| Variable Rate |

|

|

6.2% |

|

| % Fixed Rate

Financing(c) |

|

|

84% |

|

| Weighted Average Rate on Fixed Financing |

|

|

1.6% |

|

| Weighted Average Term on Fixed Financing |

|

|

2.8 years |

|

The Fund seeks to enhance its dividend yield through leverage. The use of leverage

is a speculative technique and there are special risks and costs associated with leverage. The NAV of the Fund’s shares may be reduced by the issuance and ongoing costs of leverage. So long as the Fund is able to invest in securities that

produce an investment yield that is greater than the total cost of leverage, the leverage strategy will produce higher current net investment income for shareholders. On the other hand, to the extent that the total cost of leverage exceeds the

incremental income gained from employing such leverage, shareholders would realize lower net investment income. In addition to the impact on net income, the use of leverage will have an effect of magnifying capital appreciation or depreciation for

shareholders. Specifically, in an up market, leverage will typically generate greater capital appreciation than if the Fund were not employing leverage. Conversely, in down markets, the use of leverage will generally result in greater capital

depreciation than if the Fund had been unlevered. To the extent that the Fund is required or elects to reduce its leverage, the Fund may need to liquidate investments, including under adverse economic conditions which may result in capital losses

potentially reducing returns to shareholders. There can be no assurance that a leveraging strategy will be successful during any period in which it is employed.

| (a) |

Data as of December 31, 2023. Information is subject to change. |

| (b) |

See Note 7 in Notes to Financial Statements. |

| (c) |

Represents fixed payer interest rate swap contracts on variable rate borrowing.

|

7

COHEN

& STEERS SELECT PREFERRED

AND INCOME FUND, INC.

December 31, 2023

Top Ten Holdings(a)

(Unaudited)

|

|

|

|

|

|

|

|

|

| Security |

|

Value |

|

|

% of

Managed

Assets |

|

|

|

|

| Wells Fargo & Co., 3.90%, Series BB |

|

$ |

6,474,845 |

|

|

|

1.7 |

|

| BP Capital Markets PLC, 4.875% (United Kingdom) |

|

|

4,871,340 |

|

|

|

1.3 |

|

| Citigroup Capital III, 7.625%, due 12/1/36 |

|

|

4,235,818 |

|

|

|

1.1 |

|

| UBS Group AG, 9.25% (Switzerland) |

|

|

3,998,754 |

|

|

|

1.1 |

|

| Emera, Inc., 6.75%, due 6/15/76, Series 16-A

(Canada) |

|

|

3,893,542 |

|

|

|

1.1 |

|

| Sempra, 4.875% |

|

|

3,697,475 |

|

|

|

1.0 |

|

| Transcanada Trust, 5.875%, due 8/15/76, Series

16-A (Canada) |

|

|

3,655,580 |

|

|

|

1.0 |

|

| Toronto-Dominion Bank, 8.125%, due 10/31/82 (Canada) |

|

|

3,547,183 |

|

|

|

1.0 |

|

| Charles Schwab Corp., 4.00%, Series H |

|

|

3,504,395 |

|

|

|

0.9 |

|

| Banco Santander SA, 9.625% (Spain) |

|

|

3,504,000 |

|

|

|

0.9 |

|

| (a) |

Top ten holdings (excluding short-term investments and derivative instruments) are determined on

the basis of the value of individual securities held. The Fund may also hold positions in other securities issued by the companies listed above. See the Schedule of Investments for additional details on such other positions.

|

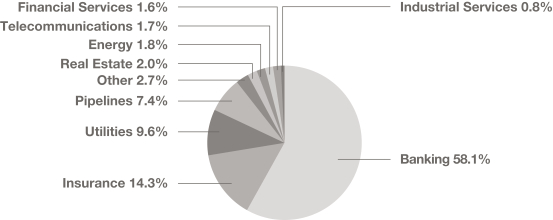

Sector Breakdown(b)

(Based on Managed Assets)

(Unaudited)

| (b) |

Excludes derivative instruments. |

8

COHEN

& STEERS SELECT PREFERRED

AND INCOME FUND, INC.

SCHEDULE OF INVESTMENTS

December 31, 2023

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

Shares |

|

|

Value |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| PREFERRED

SECURITIES—EXCHANGE-TRADED |

|

|

27.4% |

|

|

|

|

|

|

|

|

|

| BANKING |

|

|

10.2% |

|

|

|

|

|

|

|

|

|

| Bank of America Corp., 4.125%, Series PP(a)(b) |

|

|

|

63,685 |

|

|

$ |

1,171,804 |

|

| Bank of America Corp., 4.25%, Series QQ(a)(b) |

|

|

|

73,869 |

|

|

|

1,368,054 |

|

| Bank of America Corp., 4.375%, Series NN(a)(b) |

|

|

|

55,712 |

|

|

|

1,083,041 |

|

| Bank of America Corp., 4.75%, Series SS(a)(b) |

|

|

|

36,841 |

|

|

|

766,293 |

|

| Bank of America Corp., 5.00%, Series LL(a)(b) |

|

|

|

20,560 |

|

|

|

442,657 |

|

| Bank of America Corp., 5.375%, Series KK(a)(b) |

|

|

|

66,862 |

|

|

|

1,538,495 |

|

| Bank of America Corp., 5.875%, Series HH(a)(b) |

|

|

|

35,622 |

|

|

|

880,932 |

|

| Federal Agricultural Mortgage Corp., 4.875%, Series G(b) |

|

|

|

27,286 |

|

|

|

521,163 |

|

| JPMorgan Chase & Co., 4.20%, Series MM(a)(b) |

|

|

|

15,599 |

|

|

|

296,537 |

|

| JPMorgan Chase & Co., 4.55%, Series JJ(b) |

|

|

|

7,939 |

|

|

|

162,750 |

|

| JPMorgan Chase & Co., 4.75%, Series GG(a)(b) |

|

|

|

32,770 |

|

|

|

701,278 |

|

| JPMorgan Chase & Co., 5.75%, Series DD(a)(b) |

|

|

|

58,472 |

|

|

|

1,461,800 |

|

| Morgan Stanley, 4.25%, Series O(a)(b) |

|

|

|

71,416 |

|

|

|

1,361,903 |

|

| Morgan Stanley, 4.875%, Series L(a)(b) |

|

|

|

1,102 |

|

|

|

24,861 |

|

| Morgan Stanley, 5.85%, Series K(a)(b) |

|

|

|

35,712 |

|

|

|

864,945 |

|

| Morgan Stanley, 6.375%, Series I(a)(b) |

|

|

|

66,456 |

|

|

|

1,645,451 |

|

| Morgan Stanley, 6.50%, Series P(a)(b) |

|

|

|

28,701 |

|

|

|

751,105 |

|

| Regions Financial Corp., 5.70% to 5/15/29, Series C(a)(b)(c) |

|

|

|

30,119 |

|

|

|

641,836 |

|

| Texas Capital Bancshares, Inc., 5.75%, Series B(a)(b) |

|

|

|

8,443 |

|

|

|

155,773 |

|

| Truist Financial Corp., 4.75%, Series R(a)(b) |

|

|

|

16,854 |

|

|

|

339,102 |

|

| U.S. Bancorp, 4.00%, Series

M(a)(b) |

|

|

|

67,508 |

|

|

|

1,182,740 |

|

| U.S. Bancorp, 5.50%, Series

K(a)(b) |

|

|

|

32,953 |

|

|

|

764,839 |

|

| Wells Fargo & Co., 4.25%, Series DD(a)(b) |

|

|

|

71,807 |

|

|

|

1,276,728 |

|

| Wells Fargo & Co., 4.375%, Series CC(a)(b) |

|

|

|

89,764 |

|

|

|

1,653,453 |

|

| Wells Fargo & Co., 4.70%, Series AA(a)(b) |

|

|

|

62,001 |

|

|

|

1,243,120 |

|

| Wells Fargo & Co., 4.75%, Series Z(a)(b) |

|

|

|

82,253 |

|

|

|

1,639,302 |

|

| Wells Fargo & Co., 5.625%, Series Y(a)(b) |

|

|

|

37,197 |

|

|

|

890,124 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

24,830,086 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| CONSUMER DISCRETIONARY

PRODUCTS |

|

|

0.1% |

|

|

|

|

|

|

|

|

|

| Ford Motor Co., 6.50%, due 8/15/62(a) |

|

|

|

11,605 |

|

|

|

269,817 |

|

|

|

|

|

|

|

|

|

|

|

| CONSUMER STAPLE PRODUCTS |

|

|

0.1% |

|

|

|

|

|

|

|

|

|

| CHS, Inc., 6.75% to 9/30/24, Series 3(b)(c) |

|

|

|

13,581 |

|

|

|

334,500 |

|

|

|

|

|

|

|

|

|

|

|

| FINANCIAL SERVICES |

|

|

0.7% |

|

|

|

|

|

|

|

|

|

| Apollo Global Management, Inc., 7.625% to 9/15/28, due 9/15/53(a)(c) |

|

|

|

61,512 |

|

|

|

1,689,735 |

|

| Carlyle Finance LLC, 4.625%, due 5/15/61(a) |

|

|

|

1,919 |

|

|

|

39,512 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1,729,247 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| INDUSTRIAL SERVICES |

|

|

1.2% |

|

|

|

|

|

|

|

|

|

| WESCO International, Inc., 10.625% to 6/22/25, Series A(b)(c) |

|

|

|

108,966 |

|

|

|

2,878,882 |

|

|

|

|

|

|

|

|

|

|

|

See accompanying notes to financial statements.

9

COHEN

& STEERS SELECT PREFERRED

AND INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2023

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

Shares |

|

|

Value |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| INSURANCE |

|

|

7.1% |

|

|

|

|

|

|

|

|

|

| AEGON Funding Co. LLC, 5.10%, due 12/15/49 (Netherlands)(a) |

|

|

|

48,152 |

|

|

$

|

1,046,825 |

|

| Allstate Corp., 7.375%, Series J(a)(b) |

|

|

|

23,761 |

|

|

|

641,547 |

|

| Arch Capital Group Ltd., 4.55%, Series G(a)(b) |

|

|

|

64,738 |

|

|

|

1,288,934 |

|

| Arch Capital Group Ltd., 5.45%, Series F(a)(b) |

|

|

|

34,097 |

|

|

|

812,191 |

|

| Athene Holding Ltd., 4.875%, Series D(a)(b) |

|

|

|

70,627 |

|

|

|

1,257,161 |

|

| Athene Holding Ltd., 5.625%, Series B(a)(b) |

|

|

|

1,266 |

|

|

|

27,054 |

|

| Athene Holding Ltd., 6.35% to 6/30/29, Series A(a)(b)(c) |

|

|

|

27,898 |

|

|

|

627,147 |

|

| Athene Holding Ltd., 6.375% to 6/30/25, Series C(a)(b)(c) |

|

|

|

13,765 |

|

|

|

333,388 |

|

| Athene Holding Ltd., 7.75% to 12/30/27, Series E(a)(b)(c) |

|

|

|

49,803 |

|

|

|

1,262,008 |

|

| Axis Capital Holdings Ltd., 5.50%, Series E(a)(b) |

|

|

|

34,884 |

|

|

|

729,424 |

|

| Brighthouse Financial, Inc., 5.375%, Series C(a)(b) |

|

|

|

37,973 |

|

|

|

699,842 |

|

| Enstar Group Ltd., 7.00% to 9/1/28, Series D(a)(b)(c) |

|

|

|

54,631 |

|

|

|

1,370,146 |

|

| Equitable Holdings, Inc., 4.30%, Series C(a)(b) |

|

|

|

10,139 |

|

|

|

167,902 |

|

| Equitable Holdings, Inc., 5.25%, Series A(a)(b) |

|

|

|

47,313 |

|

|

|

1,008,713 |

|

| F&G Annuities & Life, Inc., 7.95%, due

12/15/53(a) |

|

|

|

50,511 |

|

|

|

1,303,689 |

|

| Lincoln National Corp., 9.00%, Series D(a)(b) |

|

|

|

30,282 |

|

|

|

826,396 |

|

| MetLife, Inc., 4.75%, Series F(a)(b) |

|

|

|

11,301 |

|

|

|

230,540 |

|

| MetLife, Inc., 5.625%, Series E(a)(b) |

|

|

|

65,302 |

|

|

|

1,586,186 |

|

| Prudential Financial, Inc., 5.95%, due 9/1/62(a) |

|

|

|

10,620 |

|

|

|

269,960 |

|

| Reinsurance Group of America, Inc., 7.125% to 10/15/27,

due 10/15/52(a)(c) |

|

|

|

22,716 |

|

|

|

592,433 |

|

| RenaissanceRe Holdings Ltd., 4.20%, Series G

(Bermuda)(b) |

|

|

|

36,402 |

|

|

|

626,842 |

|

| W R Berkley Corp., 4.125%, due 3/30/61(a) |

|

|

|

31,995 |

|

|

|

645,659 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

17,353,987 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| PIPELINES |

|

|

1.1% |

|

|

|

|

|

|

|

|

|

| Energy Transfer LP, 7.60% to 5/15/24, Series E(a)(b)(c) |

|

|

|

64,669 |

|

|

|

1,603,791 |

|

| Energy Transfer LP, 10.364% to 1/29/24, Series D(a)(b)(c) |

|

|

|

33,672 |

|

|

|

851,902 |

|

| TC Energy Corp., 3.351% to 11/30/25, Series 11 (Canada)(a)(b)(c) |

|

|

|

26,957 |

|

|

|

332,016 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2,787,709 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| REAL ESTATE |

|

|

1.8% |

|

|

|

|

|

|

|

|

|

| Brookfield Property Partners LP, 5.75%, due , Series A(a)(b) |

|

|

|

36,050 |

|

|

|

414,215 |

|

| Brookfield Property Partners LP, 6.50%, Series A-1(b) |

|

|

|

13,444 |

|

|

|

173,696 |

|

| Public Storage, 4.10%, Series S(a)(b) |

|

|

|

30,000 |

|

|

|

554,700 |

|

| Public Storage, 4.70%, Series J(a)(b) |

|

|

|

38,024 |

|

|

|

813,333 |

|

| Public Storage, 4.75%, Series K(a)(b) |

|

|

|

42,122 |

|

|

|

907,308 |

|

| Regency Centers Corp., 5.875%, Series B(b) |

|

|

|

60,000 |

|

|

|

1,410,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4,273,252 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

See accompanying notes to financial statements.

10

COHEN

& STEERS SELECT PREFERRED

AND INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2023

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

Shares |

|

|

Value |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| TELECOMMUNICATIONS |

|

|

1.8% |

|

|

|

|

|

|

|

|

|

| AT&T, Inc., 4.75%, Series C(a)(b) |

|

|

|

48,527 |

|

|

$

|

957,438 |

|

| AT&T, Inc., 5.00%, Series A(a)(b) |

|

|

|

47,603 |

|

|

|

999,187 |

|

| AT&T, Inc., Senior Debt, 5.35%, due 11/1/66(a) |

|

|

|

41,684 |

|

|

|

977,490 |

|

| AT&T, Inc., 5.625%, due 8/1/67(a) |

|

|

|

24,500 |

|

|

|

607,600 |

|

| Telephone & Data Systems, Inc., 6.00%, Series VV(a)(b) |

|

|

|

192 |

|

|

|

2,949 |

|

| U.S. Cellular Corp., Senior Debt, 5.50%, due 3/1/70(a) |

|

|

|

16,414 |

|

|

|

292,990 |

|

| U.S. Cellular Corp., Senior Debt, 5.50%, due 6/1/70(a) |

|

|

|

10,815 |

|

|

|

189,911 |

|

| U.S. Cellular Corp., Senior Debt, 6.25%, due 9/1/69(a) |

|

|

|

23,860 |

|

|

|

464,077 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4,491,642 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| UTILITIES |

|

|

3.3% |

|

|

|

|

|

|

|

|

|

| Algonquin Power & Utilities Corp., 6.20% to 7/1/24,

due

7/1/79, Series 19-A (Canada)(a)(c) |

|

|

|

22,887 |

|

|

|

552,263 |

|

| Brookfield BRP Holdings Canada, Inc., 4.625% (Canada)(a)(b) |

|

|

|

25,091 |

|

|

|

392,674 |

|

| Brookfield BRP Holdings Canada, Inc., 4.875% (Canada)(a)(b) |

|

|

|

34,274 |

|

|

|

555,239 |

|

| Brookfield Infrastructure Finance ULC, 5.00%,

due 5/24/81 (Canada)(a) |

|

|

|

47,325 |

|

|

|

794,113 |

|

| Brookfield Infrastructure Partners LP, 5.125%, Series 13 (Canada)(a)(b) |

|

|

|

47,732 |

|

|

|

789,487 |

|

| CMS Energy Corp., 5.625%, due 3/15/78(a) |

|

|

|

39,996 |

|

|

|

981,902 |

|

| Duke Energy Corp., 5.625%, due 9/15/78(a) |

|

|

|

3,885 |

|

|

|

91,259 |

|

| SCE Trust VII, 7.50%, Series M(a)(b) |

|

|

|

111,200 |

|

|

|

2,900,096 |

|

| Sempra, 5.75%, due

7/1/79(a) |

|

|

|

15,666 |

|

|

|

391,337 |

|

| Southern Co., 4.95%, due 1/30/80, Series 2020(a) |

|

|

|

30,456 |

|

|

|

684,651 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8,133,021 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| TOTAL PREFERRED

SECURITIES—EXCHANGE-TRADED

(Identified cost—$68,223,093) |

|

|

|

|

|

|

|

67,082,143 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

Principal

Amount |

|

|

|

|

| PREFERRED SECURITIES—OVER-THE-COUNTER |

|

|

122.2% |

|

|

|

|

|

|

|

|

|

| BANKING |

|

|

78.7% |

|

|

|

|

|

|

|

|

|

| Abanca Corp. Bancaria SA, 6.00% to 1/20/26 (Spain)(b)(c)(e)(f) |

|

|

$ |

1,200,000 |

|

|

|

1,258,834 |

|

| Australia & New Zealand Banking Group Ltd.,

6.75% to 6/15/26

(Australia)(a)(b)(c)(e)(g) |

|

|

|

400,000 |

|

|

|

402,933 |

|

See accompanying notes to financial statements.

11

COHEN

& STEERS SELECT PREFERRED

AND INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2023

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

Principal

Amount |

|

|

Value |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Banco Bilbao Vizcaya Argentaria SA, 6.125% to 11/16/27 (Spain)(b)(c)(e) |

|

|

$

|

600,000 |

|

|

$

|

547,566 |

|

| Banco Bilbao Vizcaya Argentaria SA, 6.50% to 3/5/25,

Series 9 (Spain)(b)(c)(e) |

|

|

|

1,600,000 |

|

|

|

1,574,469 |

|

| Banco Bilbao Vizcaya Argentaria SA, 9.375% to 3/19/29 (Spain)(b)(c)(e) |

|

|

|

2,300,000 |

|

|

|

2,465,800 |

|

| Banco de Sabadell SA, 5.75% to 3/15/26 (Spain)(a)(b)(c)(e)(f) |

|

|

|

400,000 |

|

|

|

419,675 |

|

| Banco de Sabadell SA, 9.375% to 7/18/28 (Spain)(a)(b)(c)(e)(f) |

|

|

|

1,800,000 |

|

|

|

2,130,359 |

|

| Banco Mercantil del Norte SA, 6.625% to 1/24/32 (Mexico)(b)(c)(e)(g) |

|

|

|

200,000 |

|

|

|

170,400 |

|

| Banco Santander SA, 9.625% to 11/21/28 (Spain)(b)(c)(e) |

|

|

|

1,200,000 |

|

|

|

1,288,730 |

|

| Banco Santander SA, 9.625% to 5/21/33 (Spain)(b)(c)(e) |

|

|

|

3,200,000 |

|

|

|

3,504,000 |

|

| Bank of America Corp., 4.375% to 1/27/27,

Series RR(a)(b)(c) |

|

|

|

1,343,000 |

|

|

|

1,200,274 |

|

| Bank of America Corp., 5.875% to 3/15/28, Series FF(a)(b)(c) |

|

|

|

1,235,000 |

|

|

|

1,183,885 |

|

| Bank of America Corp., 6.10% to 3/17/25, Series AA(a)(b)(c) |

|

|

|

895,000 |

|

|

|

888,742 |

|

| Bank of America Corp., 6.125% to 4/27/27, Series TT(a)(b)(c) |

|

|

|

1,215,000 |

|

|

|

1,220,954 |

|

| Bank of America Corp., 6.25% to 9/5/24, Series X(a)(b)(c) |

|

|

|

305,000 |

|

|

|

302,953 |

|

| Bank of America Corp., 6.30% to 3/10/26, Series DD(a)(b)(c) |

|

|

|

662,000 |

|

|

|

666,966 |

|

| Bank of America Corp., 6.50% to 10/23/24, Series Z(a)(b)(c) |

|

|

|

305,000 |

|

|

|

304,284 |

|

| Bank of America Corp., 8.05%, due 6/15/27, Series B(a) |

|

|

|

1,815,000 |

|

|

|

1,953,697 |

|

| Bank of Ireland Group PLC, 7.50% to 5/19/25

(Ireland)(b)(c)(e)(f) |

|

|

|

1,010,000 |

|

|

|

1,131,771 |

|

| Bank of Nova Scotia, 4.90% to 6/4/25 (Canada)(a)(b)(c) |

|

|

|

1,020,000 |

|

|

|

976,805 |

|

| Bank of Nova Scotia, 8.625% to 10/27/27, due 10/27/82 (Canada)(a)(c) |

|

|

|

1,600,000 |

|

|

|

1,666,251 |

|

| Barclays Bank PLC, 6.278% to 12/15/34, Series 1

(United Kingdom)(b)(c) |

|

|

|

1,310,000 |

|

|

|

1,318,752 |

|

| Barclays PLC, 6.125% to 12/15/25 (United Kingdom)(b)(c)(e) |

|

|

|

1,400,000 |

|

|

|

1,340,793 |

|

| Barclays PLC, 7.125% to 6/15/25 (United Kingdom)(b)(c)(e) |

|

|

|

200,000 |

|

|

|

248,591 |

|

| Barclays PLC, 8.00% to 3/15/29 (United Kingdom)(b)(c)(e) |

|

|

|

1,800,000 |

|

|

|

1,771,042 |

|

| Barclays PLC, 8.875% to 9/15/27 (United Kingdom)(b)(c)(e)(f) |

|

|

|

200,000 |

|

|

|

254,930 |

|

| Barclays PLC, 9.625% to 12/15/29 (United Kingdom)(b)(c)(e) |

|

|

|

2,400,000 |

|

|

|

2,499,000 |

|

| BNP Paribas SA, 4.50% to 2/25/30 (France)(b)(c)(e)(g) |

|

|

|

1,600,000 |

|

|

|

1,277,642 |

|

| BNP Paribas SA, 4.625% to 1/12/27 (France)(b)(c)(e)(g) |

|

|

|

3,200,000 |

|

|

|

2,804,114 |

|

| BNP Paribas SA, 4.625% to 2/25/31 (France)(a)(b)(c)(e)(g) |

|

|

|

2,275,000 |

|

|

|

1,838,148 |

|

| BNP Paribas SA, 7.00% to 8/16/28 (France)(b)(c)(e)(g) |

|

|

|

1,165,000 |

|

|

|

1,146,565 |

|

| BNP Paribas SA, 7.375% to 8/19/25 (France)(b)(c)(e)(g) |

|

|

|

1,200,000 |

|

|

|

1,204,667 |

|

| BNP Paribas SA, 7.75% to 8/16/29 (France)(b)(c)(e)(g) |

|

|

|

2,600,000 |

|

|

|

2,660,502 |

|

| BNP Paribas SA, 8.50% to 8/14/28 (France)(b)(c)(e)(g) |

|

|

|

2,800,000 |

|

|

|

2,939,227 |

|

See accompanying notes to financial statements.

12

COHEN

& STEERS SELECT PREFERRED

AND INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2023

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

Principal

Amount |

|

|

Value |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| BNP Paribas SA, 9.25% to 11/17/27 (France)(a)(b)(c)(e)(g) |

|

|

$ |

1,800,000 |

|

|

$ |

1,929,357 |

|

| CaixaBank SA, 8.25% to 3/13/29 (Spain)(b)(c)(e)(f) |

|

|

|

1,400,000 |

|

|

|

1,641,366 |

|

| Charles Schwab Corp., 4.00% to 6/1/26, Series I(a)(b)(c) |

|

|

|

3,653,000 |

|

|

|

3,224,610 |

|

| Charles Schwab Corp., 4.00% to 12/1/30, Series H(b)(c) |

|

|

|

4,430,000 |

|

|

|

3,504,395 |

|

| Charles Schwab Corp., 5.00% to 6/1/27, Series K(a)(b)(c) |

|

|

|

652,000 |

|

|

|

590,234 |

|

| Charles Schwab Corp., 5.375% to 6/1/25, Series G(a)(b)(c) |

|

|

|

1,686,000 |

|

|

|

1,666,813 |

|

| Citigroup Capital III, 7.625%, due 12/1/36 (TruPS) |

|

|

|

4,115,000 |

|

|

|

4,235,818 |

|

| Citigroup, Inc., 3.875% to 2/18/26, Series X(b)(c) |

|

|

|

3,504,000 |

|

|

|

3,110,936 |

|

| Citigroup, Inc., 4.00% to 12/10/25, Series W(b)(c) |

|

|

|

420,000 |

|

|

|

387,623 |

|

| Citigroup, Inc., 5.00% to 9/12/24, Series U(b)(c) |

|

|

|

893,000 |

|

|

|

869,064 |

|

| Citigroup, Inc., 5.95% to 5/15/25, Series P(b)(c) |

|

|

|

2,461,000 |

|

|

|

2,411,922 |

|

| Citigroup, Inc., 6.25% to 8/15/26, Series T(b)(c) |

|

|

|

636,000 |

|

|

|

629,320 |

|

| Citigroup, Inc., 7.625% to 11/15/28(b)(c) |

|

|

|

2,429,000 |

|

|

|

2,486,324 |

|

| CoBank ACB, 6.25% to 10/1/26, Series I(a)(b)(c) |

|

|

|

2,534,000 |

|

|

|

2,445,230 |

|

| CoBank ACB, 6.45% to 10/1/27, Series K(a)(b)(c) |

|

|

|

1,370,000 |

|

|

|

1,332,325 |

|

| Commerzbank AG, 7.00% to 4/9/25 (Germany)(b)(c)(e)(f) |

|

|

|

1,200,000 |

|

|

|

1,158,210 |

|

| Credit Agricole SA, 4.00% to 12/23/27 (France)(a)(b)(c)(e)(f) |

|

|

|

400,000 |

|

|

|

412,190 |

|

| Credit Agricole SA, 4.75% to 3/23/29 (France)(a)(b)(c)(e)(g) |

|

|

|

2,400,000 |

|

|

|

2,041,917 |

|

| Credit Agricole SA, 7.25% to 9/23/28,

Series EMTN (France)(a)(b)(c)(e)(f) |

|

|

|

1,300,000 |

|

|

|

1,523,475 |

|

| Credit Agricole SA, 8.125% to 12/23/25 (France)(a)(b)(c)(e)(g) |

|

|

|

1,250,000 |

|

|

|

1,277,828 |

|

| Credit Suisse Group AG, 6.375%, Claim (Switzerland)(b)(d)(e)(g)(h) |

|

|

|

3,000,000 |

|

|

|

330,000 |

|

| Danske Bank AS, 7.00% to 6/26/25 (Denmark)(b)(c)(e)(f) |

|

|

|

600,000 |

|

|

|

592,527 |

|

| Deutsche Bank AG, 6.00% to 10/30/25,

Series 2020 (Germany)(b)(c)(e) |

|

|

|

800,000 |

|

|

|

727,990 |

|

| Deutsche Bank AG, 7.50% to 4/30/25 (Germany)(b)(c)(e) |

|

|

|

400,000 |

|

|

|

391,698 |

|

| Deutsche Bank AG, 10.00% to 12/1/27 (Germany)(b)(c)(e)(f) |

|

|

|

2,400,000 |

|

|

|

2,897,822 |

|

| DNB Bank ASA, 4.875% to 11/12/24 (Norway)(a)(b)(c)(e)(f) |

|

|

|

600,000 |

|

|

|

584,625 |

|

| Dresdner Funding Trust I, 8.151%, due 6/30/31 (TruPS)(g) |

|

|

|

757,869 |

|

|

|

840,287 |

|

| Farm Credit Bank of Texas, 5.70% to 9/15/25,

Series 4(b)(c)(g) |

|

|

|

1,850,000 |

|

|

|

1,776,000 |

|

| Farm Credit Bank of Texas, 9.656% (3 Month USD

Term SOFR + 4.01%)(b)(g)(i) |

|

|

|

9,779 |

† |

|

|

976,678 |

|

| First Horizon Bank, 6.518% (3 Month USD Term SOFR + 1.11%, Floor

3.75%)(a)(b)(g)(i) |

|

|

|

1,537 |

† |

|

|

954,861 |

|

| Goldman Sachs Capital I, 6.345%, due 2/15/34 (TruPS) |

|

|

|

1,007,000 |

|

|

|

1,060,231 |

|

| Goldman Sachs Group, Inc., 3.65% to 8/10/26,

Series U(b)(c) |

|

|

|

1,287,000 |

|

|

|

1,144,490 |

|

| Goldman Sachs Group, Inc., 7.50% to 2/10/29,

Series W(b)(c) |

|

|

|

1,514,000 |

|

|

|

1,585,755 |

|

See accompanying notes to financial statements.

13

COHEN

& STEERS SELECT PREFERRED

AND INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2023

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

Principal

Amount |

|

|

Value |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| HSBC Capital Funding Dollar 1 LP, 10.176% to 6/30/30,

Series 2 (United

Kingdom)(b)(c)(g) |

|

|

$ |

1,797,000 |

|

|

$ |

2,285,637 |

|

| HSBC Holdings PLC, 4.60% to 12/17/30

(United Kingdom)(a)(b)(c)(e) |

|

|

|

3,200,000 |

|

|

|

2,676,844 |

|

| HSBC Holdings PLC, 6.00% to 5/22/27

(United Kingdom)(a)(b)(c)(e) |

|

|

|

2,400,000 |

|

|

|

2,298,146 |

|

| HSBC Holdings PLC, 6.375% to 3/30/25

(United Kingdom)(a)(b)(c)(e) |

|

|

|

2,600,000 |

|

|

|

2,570,408 |

|

| HSBC Holdings PLC, 6.50% to 3/23/28

(United Kingdom)(a)(b)(c)(e) |

|

|

|

1,200,000 |

|

|

|

1,160,449 |

|

| HSBC Holdings PLC, 6.50%, due 9/15/37

(United Kingdom)(a) |

|

|

|

902,000 |

|

|

|

977,487 |

|

| HSBC Holdings PLC, 8.00% to 3/7/28

(United Kingdom)(a)(b)(c)(e) |

|

|

|

2,600,000 |

|

|

|

2,682,649 |

|

| Huntington Bancshares, Inc., 4.45% to 10/15/27,

Series G(b)(c) |

|

|

|

779,000 |

|

|

|

685,121 |

|

| Huntington Bancshares, Inc., 5.625% to 7/15/30,

Series F(b)(c) |

|

|

|

926,000 |

|

|

|

840,665 |

|

| ING Groep NV, 4.25% to 5/16/31, Series NC10 (Netherlands)(b)(c)(e) |

|

|

|

1,000,000 |

|

|

|

729,864 |

|

| ING Groep NV, 4.875% to 5/16/29 (Netherlands)(b)(c)(e)(f) |

|

|

|

2,400,000 |

|

|

|

1,992,480 |

|

| ING Groep NV, 5.75% to 11/16/26 (Netherlands)(b)(c)(e) |

|

|

|

2,800,000 |

|

|

|

2,616,232 |

|

| ING Groep NV, 6.50% to 4/16/25 (Netherlands)(b)(c)(e) |

|

|

|

2,000,000 |

|

|

|

1,951,404 |

|

| ING Groep NV, 7.50% to 5/16/28 (Netherlands)(b)(c)(e)(f) |

|

|

|

1,200,000 |

|

|

|

1,201,014 |

|

| Intesa Sanpaolo SpA, 7.70% to 9/17/25 (Italy)(b)(c)(e)(g) |

|

|

|

1,200,000 |

|

|

|

1,182,130 |

|

| Intesa Sanpaolo SpA, 9.125% to 9/7/29 (Italy)(b)(c)(e)(f) |

|

|

|

1,600,000 |

|

|

|

1,947,866 |

|

| JPMorgan Chase & Co., 3.65% to 6/1/26, Series KK(a)(b)(c) |

|

|

|

1,157,000 |

|

|

|

1,061,703 |

|

| JPMorgan Chase & Co., 6.10% to 10/1/24, Series X(a)(b)(c) |

|

|

|

303,000 |

|

|

|

301,527 |

|

| JPMorgan Chase & Co., 8.889%

(3 Month USD Term SOFR + 3.512%),

Series Q(a)(b)(i) |

|

|

|

1,306,000 |

|

|

|

1,315,247 |

|

| Lloyds Banking Group PLC, 6.75% to 6/27/26

(United Kingdom)(b)(c)(e) |

|

|

|

600,000 |

|

|

|

591,987 |

|

| Lloyds Banking Group PLC, 7.50% to 9/27/25

(United Kingdom)(b)(c)(e) |

|

|

|

2,200,000 |

|

|

|

2,159,939 |

|

| Lloyds Banking Group PLC, 8.00% to 9/27/29

(United Kingdom)(b)(c)(e) |

|

|

|

2,000,000 |

|

|

|

2,008,996 |

|

| M&T Bank Corp., 3.50% to 9/1/26, Series I(b)(c) |

|

|

|

178,000 |

|

|

|

131,073 |

|

| M&T Bank Corp., 5.125% to 11/1/26, Series F(b)(c) |

|

|

|

872,000 |

|

|

|

756,530 |

|

See accompanying notes to financial statements.

14

COHEN

& STEERS SELECT PREFERRED

AND INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2023

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

Principal

Amount |

|

|

Value |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Nationwide Building Society, 5.75% to 6/20/27

(United Kingdom)(b)(c)(e)(f) |

|

|

$ |

600,000 |

|

|

$ |

707,225 |

|

| NatWest Group PLC, 6.00% to 12/29/25

(United Kingdom)(b)(c)(e) |

|

|

|

2,000,000 |

|

|

|

1,938,617 |

|

| NatWest Group PLC, 8.00% to 8/10/25

(United Kingdom)(b)(c)(e) |

|

|

|

800,000 |

|

|

|

803,404 |

|

| Nordea Bank Abp, 6.625% to 3/26/26 (Finland)(a)(b)(c)(e)(g) |

|

|

|

1,800,000 |

|

|

|

1,788,721 |

|

| PNC Financial Services Group, Inc., 3.40% to 9/15/26,

Series T(a)(b)(c) |

|

|

|

|

|

|

1,581,000 |

|

|

|

1,268,633 |

|

| PNC Financial Services Group, Inc., 6.00% to 5/15/27,

Series U(a)(b)(c) |

|

|

|

|

|

|

1,381,000 |

|

|

|

1,311,277 |

|

| PNC Financial Services Group, Inc., 6.20% to 9/15/27,

Series V(a)(b)(c) |

|

|

|

|

|

|

1,976,000 |

|

|

|

1,926,082 |

|

| PNC Financial Services Group, Inc., 6.25% to 3/15/30,

Series W(a)(b)(c) |

|

|

|

|

|

|

1,832,000 |

|

|

|

1,712,311 |

|

| Regions Financial Corp., 5.75% to 6/15/25, Series D(b)(c) |

|

|

|

|

|

|

529,000 |

|

|

|

514,180 |

|

| Skandinaviska Enskilda Banken AB, 6.875% to 6/30/27 (Sweden)(a)(b)(c)(e)(f) |

|

|

|

|

|

|

200,000 |

|

|

|

196,998 |

|

| Societe Generale SA, 5.375% to 11/18/30 (France)(b)(c)(e)(g) |

|

|

|

|

|

|

1,400,000 |

|

|

|

1,148,886 |

|

| Societe Generale SA, 6.75% to 4/6/28 (France)(b)(c)(e)(g) |

|

|

|

|

|

|

1,160,000 |

|

|

|

1,038,882 |

|

| Societe Generale SA, 8.00% to 9/29/25 (France)(b)(c)(e)(g) |

|

|

|

|

|

|

600,000 |

|

|

|

599,929 |

|

| Societe Generale SA, 9.375% to 11/22/27 (France)(a)(b)(c)(e)(g) |

|

|

|

|

|

|

2,800,000 |

|

|

|

2,936,130 |

|

| Societe Generale SA, 10.00% to 11/14/28 (France)(b)(c)(e)(g) |

|

|

|

|

|

|

1,600,000 |

|

|

|

1,713,622 |

|

| Standard Chartered PLC, 4.30% to 8/19/28

(United Kingdom)(b)(c)(e)(g) |

|

|

|

|

|

|

2,400,000 |

|

|

|

1,957,246 |

|

| Standard Chartered PLC, 4.75% to 1/14/31

(United Kingdom)(b)(c)(e)(g) |

|

|

|

|

|

|

1,600,000 |

|

|

|

1,305,740 |

|

| Standard Chartered PLC, 7.75% to 8/15/27

(United Kingdom)(b)(c)(e)(g) |

|

|

|

|

|

|

1,600,000 |

|

|

|

1,637,906 |

|

| Swedbank AB, 7.625% to 3/17/28

(Sweden)(b)(c)(e)(f) |

|

|

|

|

|

|

200,000 |

|

|

|

195,040 |

|

| Toronto-Dominion Bank, 8.125% to 10/31/27, due 10/31/82 (Canada)(a)(c) |

|

|

|

|

|

|

3,400,000 |

|

|

|

3,547,183 |

|

| Truist Financial Corp., 4.95% to 9/1/25, Series P(a)(b)(c) |

|

|

|

|

|

|

694,000 |

|

|

|

665,815 |

|

| Truist Financial Corp., 5.10% to 3/1/30, Series Q(a)(b)(c) |

|

|

|

|

|

|

1,316,000 |

|

|

|

1,199,145 |

|

| Truist Financial Corp., 5.125% to 12/15/27, Series M(a)(b)(c) |

|

|

|

|

|

|

1,119,000 |

|

|

|

945,783 |

|

| UBS Group AG, 4.375% to 2/10/31 (Switzerland)(b)(c)(e)(g) |

|

|

|

|

|

|

2,600,000 |

|

|

|

2,059,925 |

|

| UBS Group AG, 4.875% to 2/12/27 (Switzerland)(b)(c)(e)(g) |

|

|

|

|

|

|

3,200,000 |

|

|

|

2,890,311 |

|

See accompanying notes to financial statements.

15

COHEN

& STEERS SELECT PREFERRED

AND INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2023

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

Principal

Amount |

|

|

Value |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| UBS Group AG, 5.125% to 7/29/26 (Switzerland)(b)(c)(e)(f) |

|

|

$ |

800,000 |

|

|

$ |

758,484 |

|

| UBS Group AG, 6.875% to 8/7/25 (Switzerland)(b)(c)(e)(f) |

|

|

|

2,400,000 |

|

|

|

2,365,872 |

|

| UBS Group AG, 7.00% to 2/19/25 (Switzerland)(b)(c)(e)(f) |

|

|

|

800,000 |

|

|

|

796,936 |

|

| UBS Group AG, 9.25% to 11/13/28 (Switzerland)(b)(c)(e)(g) |

|

|

|

2,800,000 |

|

|

|

3,027,576 |

|

| UBS Group AG, 9.25% to 11/13/33 (Switzerland)(b)(c)(e)(g) |

|

|

|

3,600,000 |

|

|

|

3,998,754 |

|

| U.S. Bancorp, 3.70% to 1/15/27, Series N(b)(c) |

|

|

|

488,000 |

|

|

|

384,312 |

|

| U.S. Bancorp, 5.30% to 4/15/27, Series J(a)(b)(c) |

|

|

|

1,000,000 |

|

|

|

899,530 |

|

| Wells Fargo & Co., 3.90% to 3/15/26, Series BB(b)(c) |

|

|

|

7,003,000 |

|

|

|

6,474,845 |

|

| Wells Fargo & Co., 5.875% to 6/15/25, Series U(b)(c) |

|

|

|

724,000 |

|

|

|

718,263 |

|

| Wells Fargo & Co., 5.95%, due 12/15/36 |

|

|

|

1,027,000 |

|

|

|

1,043,073 |

|

| Wells Fargo & Co., 7.625% to 9/15/28(b)(c) |

|

|

|

2,160,000 |

|

|

|

2,271,912 |

|

| Wells Fargo & Co., 7.95%, due 11/15/29, Series B |

|

|

|

249,000 |

|

|

|

278,165 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

192,457,353 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ENERGY |

|

|

2.7% |

|

|

|

|

|

|

|

|

|

| BP Capital Markets PLC, 4.375% to 6/22/25 (United Kingdom)(a)(b)(c) |

|

|

|

1,855,000 |

|

|

|

1,814,218 |

|

| BP Capital Markets PLC, 4.875% to 3/22/30 (United Kingdom)(a)(b)(c) |

|

|

|

5,112,000 |

|

|

|

4,871,340 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6,685,558 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| FINANCIAL SERVICES |

|

|

1.7% |

|

|

|

|

|

|

|

|

|

| Aircastle Ltd., 5.25% to 6/15/26, Series A(b)(c)(g) |

|

|

|

620,000 |

|

|

|

534,633 |

|

| American Express Co., 3.55% to 9/15/26, Series D(b)(c) |

|

|

|

1,833,000 |

|

|

|

1,576,013 |

|

| Apollo Management Holdings LP, 4.95% to 12/17/24,

due 1/14/50(a)(c)(g) |

|

|

|

878,000 |

|

|

|

831,475 |

|

| ARES Finance Co. III LLC, 4.125% to 6/30/26, due 6/30/51(a)(c)(g) |

|

|

|

1,075,000 |

|

|

|

916,393 |

|

| Discover Financial Services, 6.125% to 6/23/25,

Series D(b)(c) |

|

|

|

400,000 |

|

|

|

387,488 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4,246,002 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| INSURANCE |

|

|

14.8% |

|

|

|

|

|

|

|

|

|

| Aegon Ltd., 5.50% to 4/11/28, due 4/11/48 (Netherlands)(a)(c) |

|

|

|

600,000 |

|

|

|

571,201 |

|

| Aegon Ltd., 5.625% to 4/15/29 (Netherlands)(b)(c)(e)(f) |

|

|

|

1,200,000 |

|

|

|

1,235,141 |

|

| Allianz SE, 3.50% to 11/17/25 (Germany)(a)(b)(c)(e)(g) |

|

|

|

1,600,000 |

|

|

|

1,422,657 |

|

| Allianz SE, 6.35% to 3/6/33, due 9/6/53 (Germany)(a)(c)(g) |

|

|

|

1,000,000 |

|

|

|

1,039,340 |

|

| American International Group, Inc., 5.75% to 4/1/28,

due 4/1/48, Series

A-9(a)(c) |

|

|

|

200,000 |

|

|

|

197,347 |

|

| Assurant, Inc., 7.00% to 3/27/28, due 3/27/48(c) |

|

|

|

1,555,000 |

|

|

|

1,570,577 |

|

See accompanying notes to financial statements.

16

COHEN

& STEERS SELECT PREFERRED

AND INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2023

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

Principal

Amount |

|

|

Value |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| AXA SA, 8.60%, due 12/15/30 (France)(a) |

|

|

$

|

525,000 |

|

|

$

|

632,932 |

|

| AXIS Specialty Finance LLC, 4.90% to 1/15/30,

due 1/15/40(a)(c) |

|

|

|

545,000 |

|

|

|

454,571 |

|

| CNP Assurances SACA, 4.875% to 10/7/30 (France)(b)(c)(e)(f) |

|

|

|

600,000 |

|

|

|

472,132 |

|

| Corebridge Financial, Inc., 6.875% to 9/15/27, due 12/15/52(a)(c) |

|

|

|

1,790,000 |

|

|

|

1,786,346 |

|

| Enstar Finance LLC, 5.50% to 1/15/27, due 1/15/42(a)(c) |

|

|

|

1,390,000 |

|

|

|

1,179,923 |

|

| Enstar Finance LLC, 5.75% to 9/1/25, due 9/1/40(a)(c) |

|

|

|

1,770,000 |

|

|

|

1,660,403 |

|

| Equitable Holdings, Inc., 4.95% to 9/15/25, Series B(a)(b)(c) |

|

|

|

1,150,000 |

|

|

|

1,097,179 |

|

| Global Atlantic Fin Co., 4.70% to 7/15/26, due 10/15/51(c)(g) |

|

|

|

1,613,000 |

|

|

|

1,384,071 |

|

| Hartford Financial Services Group, Inc., 7.766%

(3 Month USD Term SOFR

+ 2.387%), due 2/12/47, Series ICON(a)(g)(i) |

|

|

|

1,400,000 |

|

|

|

1,202,946 |

|

| ILFC E-Capital Trust I, 7.186% (3

Month USD Term SOFR + 1.812%), due 12/21/65 (TruPS)(g)(i) |

|

|

|

693,000 |

|

|

|

515,855 |

|

| Lancashire Holdings Ltd., 5.625% to 3/18/31, due 9/18/41 (United Kingdom)(c)(f) |

|

|

|

1,000,000 |

|

|

|

858,750 |

|

| Liberty Mutual Group, Inc., 4.125% to 9/15/26, due 12/15/51(c)(g) |

|

|

|

1,150,000 |

|

|

|

965,833 |

|

| Lincoln National Corp., 9.25% to 12/1/27, Series C(b)(c) |

|

|

|

853,000 |

|

|

|

933,122 |

|

| Markel Group, Inc., 6.00% to 6/1/25(b)(c) |

|

|

|

690,000 |

|

|

|

683,064 |

|

| MetLife Capital Trust IV, 7.875%, due 12/15/37 (TruPS)(a)(g) |

|

|

|

2,278,000 |

|

|

|

2,452,443 |

|

| MetLife, Inc., 9.25%, due 4/8/38(a)(g) |

|

|

|

2,309,000 |

|

|

|

2,596,264 |

|

| Muenchener Rueckversicherungs-Gesellschaft AG in Muenchen, 5.875% to

11/23/31, due 5/23/42 (Germany)(a)(c)(g) |

|

|

|

600,000 |

|

|

|

603,000 |

|

| Nippon Life Insurance Co., 6.25% to 9/13/33, due 9/13/53 (Japan)(a)(c)(g) |

|

|

|

392,000 |

|

|

|

411,647 |

|

| Phoenix Group Holdings PLC, 5.625% to 1/29/25 (United Kingdom)(b)(c)(e)(f) |

|

|

|

600,000 |

|

|

|

573,000 |

|

| Prudential Financial, Inc., 5.125% to 11/28/31, due 3/1/52(a)(c) |

|

|

|

1,410,000 |

|

|

|

1,328,566 |

|

| Prudential Financial, Inc., 6.00% to 6/1/32, due 9/1/52(a)(c) |

|

|

|

1,985,000 |

|

|

|

1,980,406 |

|

| Prudential Financial, Inc., 6.75% to 12/1/32, due 3/1/53(a)(c) |

|

|

|

840,000 |

|

|

|

877,306 |

|

| QBE Insurance Group Ltd., 5.875% to 5/12/25 (Australia)(a)(b)(c)(g) |

|

|

|

1,800,000 |

|

|

|

1,758,224 |

|

| QBE Insurance Group Ltd., 5.875% to 6/17/26, due 6/17/46, Series EMTN

(Australia)(a)(c)(f) |

|

|

|

200,000 |

|

|

|

196,329 |

|

| Rothesay Life PLC, 4.875% to 4/13/27, Series NC6 (United Kingdom)(b)(c)(e)(f) |

|

|

|

400,000 |

|

|

|

322,700 |

|

| SBL Holdings, Inc., 6.50% to 11/13/26(b)(c)(g) |

|

|

|

1,730,000 |

|

|

|

1,068,275 |

|

| SBL Holdings, Inc., 7.00% to 5/13/25(b)(c)(g) |

|

|

|

1,466,000 |

|

|

|

976,125 |

|

| Swiss Re Finance Luxembourg SA, 5.00% to 4/2/29,

due 4/2/49

(Switzerland)(a)(c)(g) |

|

|

|

400,000 |

|

|

|

383,750 |

|

See accompanying notes to financial statements.

17

COHEN

& STEERS SELECT PREFERRED

AND INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2023

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

Principal

Amount |

|

|

Value |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Zurich Finance Ireland Designated Activity Co., 3.00% to 1/19/31, due

4/19/51, Series EMTN (Switzerland)(a)(c)(f) |

|

|

$

|

966,000 |

|

|

$

|

786,566 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

36,177,991 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| PIPELINES |

|

|

10.2% |

|

|

|

|

|

|

|

|

|

| Enbridge, Inc., 5.50% to 7/15/27, due 7/15/77,

Series 2017-A (Canada)(a)(c) |

|

|

|

275,000 |

|

|

|

251,846 |

|

| Enbridge, Inc., 5.75% to 4/15/30, due 7/15/80,

Series 20-A (Canada)(a)(c) |

|

|

|

1,600,000 |

|

|

|

1,478,920 |

|

| Enbridge, Inc., 6.00% to 1/15/27, due 1/15/77,

Series 16-A (Canada)(a)(c) |

|

|

|

1,724,000 |

|

|

|

1,639,575 |

|

| Enbridge, Inc., 6.25% to 3/1/28, due 3/1/78 (Canada)(a)(c) |

|

|

|

1,970,000 |

|

|

|

1,824,385 |

|

| Enbridge, Inc., 7.375% to 10/15/27, due 1/15/83 (Canada)(a)(c) |

|

|

|

698,000 |

|

|

|

688,125 |

|

| Enbridge, Inc., 7.625% to 10/15/32, due 1/15/83 (Canada)(a)(c) |

|

|

|

2,152,000 |

|

|

|

2,160,649 |

|

| Enbridge, Inc., 8.25% to 10/15/28, due 1/15/84,

Series NC5 (Canada)(a)(c) |

|

|

|

2,370,000 |

|

|

|

2,451,355 |

|

| Enbridge, Inc., 8.50% to 10/15/33, due 1/15/84 (Canada)(a)(c) |

|

|

|

2,815,000 |

|

|

|

3,001,201 |

|

| Energy Transfer LP, 6.50% to 11/15/26, Series H(b)(c) |

|

|

|

1,250,000 |

|

|

|

1,190,975 |

|

| Energy Transfer LP, 7.125% to 5/15/30, Series G(b)(c) |

|

|

|

1,623,000 |

|

|

|

1,499,617 |

|

| Enterprise Products Operating LLC, 8.638% (3 Month USD Term SOFR +

3.248%), due 8/16/77, Series D(a)(i) |

|

|

|

986,000 |

|

|

|

981,541 |

|

| Transcanada Trust, 5.50% to 9/15/29, due 9/15/79 (Canada)(c) |

|

|

|

3,007,000 |

|

|

|

2,576,189 |

|

| Transcanada Trust, 5.60% to 12/7/31, due 3/7/82 (Canada)(c) |

|

|

|

1,848,000 |

|

|

|

1,550,460 |

|

| Transcanada Trust, 5.875% to 8/15/26, due 8/15/76,

Series 16-A (Canada)(c) |

|

|

|

3,857,000 |

|

|

|

3,655,580 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

24,950,418 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| REAL ESTATE |

|

|

1.3% |

|

|

|