UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED

SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21467

LMP Capital and Income Fund Inc.

(Exact name of registrant as specified in charter)

620 Eighth

Avenue, 47th Floor, New York, NY 10018

(Address of principal executive offices) (Zip code)

George P. Hoyt

Franklin

Templeton

100 First Stamford Place

Stamford, CT 06902

(Name

and address of agent for service)

Registrant’s telephone number, including area code: 1-888-777-0102

Date of fiscal year end: November 30

Date of reporting period: November 30, 2023

| ITEM 1. |

REPORT TO STOCKHOLDERS. |

The Annual Report to Stockholders is filed herewith.

|

|

|

| Annual Report |

|

November 30, 2023 |

LMP

CAPITAL AND INCOME

FUND INC. (SCD)

|

| INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE |

Managed Distribution Policy: The Fund’s Board of Directors (the “Board”) has authorized a

managed distribution plan pursuant to which the Fund makes monthly distributions to shareholders at a fixed rate of $0.1130 per common share, which rate may be adjusted from time to time by the Fund’s Board (the “Plan”). The Plan is

intended to provide shareholders with a constant, but not guaranteed, fixed minimum rate of distribution each month. The Fund is managed with a goal of generating as much of the distribution as possible from net ordinary income and short-term

capital gains that is consistent with the Fund’s investment strategy and risk profile. To the extent that sufficient distributable income is not available on a monthly basis, the Fund will distribute long-term capital gains and/or return of

capital in order to maintain its managed distribution rate. A return of capital may occur, for example, when some or all of the money that was invested in the Fund is paid back to shareholders. A return of capital distribution does not necessarily

reflect the Fund’s investment performance and should not be confused with “yield” or “income”. Even though the Fund may realize current year capital gains, such gains may be offset, in whole or in part, by the Fund’s

capital loss carryovers from prior years.

The Board may amend the terms of the Plan or terminate the Plan at any time without prior notice to the Fund’s

shareholders, however, at this time there are no reasonably foreseeable circumstances that might cause the termination of the Plan. The amendment or termination of the Plan could have an adverse effect on the market price of the Fund’s common

shares. The Plan is subject to the periodic review by the Board to determine if an adjustment should be made.

Shareholders should not draw any conclusions about the

Fund’s investment performance from the amount of the current distribution or from the terms of the Fund’s Plan. The Fund will send a Form 1099-DIV to shareholders for the calendar year that will describe how to report the Fund’s

distributions for federal income tax purposes.

Fund objective

The Fund’s investment objective is total return with an emphasis on income.

The

Fund may invest in a broad range of equity and fixed income securities of both U.S. and foreign issuers. The Fund will vary its allocation between equity and fixed income securities depending on the investment manager’s view of economic, market

or political conditions, fiscal and monetary policy and security valuation.

|

|

|

| LMP Capital and Income Fund Inc. |

|

II |

Letter from the chairman

Dear Shareholder,

We are pleased to provide the annual report of LMP Capital and Income Fund Inc. for the twelve-month reporting period ended November 30, 2023. Please read on for a

detailed look at prevailing economic and market conditions during the Fund’s reporting period and to learn how those conditions have affected Fund performance.

As always, we remain committed to providing you with excellent service and a full spectrum of investment choices. We also remain committed to supplementing the support

you receive from your financial advisor. One way we accomplish this is through our website, www.franklintempleton.com. Here you can gain immediate access to market and investment information, including:

| • |

|

Fund prices and performance, |

| • |

|

Market insights and commentaries from our portfolio managers, and |

| • |

|

A host of educational resources. |

We look forward to helping you meet your financial goals.

Sincerely,

Jane Trust, CFA

Chairman, President and Chief Executive Officer

December 29, 2023

|

|

|

|

III |

|

LMP Capital and Income Fund Inc. |

Fund overview

Q. What is the Fund’s investment strategy?

A. The Fund’s investment objective is total return with an emphasis on income. Under normal market conditions, the Fund seeks to maximize total return by

investing at least 80% of its managed assets in a broad range of equity and fixed income securities of both U.S. and foreign issuers. The Fund may invest without limit in both energy and non-energy master limited partnerships (“MLPs”), so

long as no more than 25% of the Fund’s total assets are invested in MLPs that are treated as qualified publicly traded partnerships (“QPTPs”). The Fund will vary its allocation between equity and fixed income securities depending on

ClearBridge Investments, LLC’s (“ClearBridge”) view of economic, market or political conditions, fiscal and monetary policy and security valuation. Depending on ClearBridge’s view of these factors, which may vary from time to

time, ClearBridge, one of the Fund’s subadvisers, may allocate substantially all of the investments in the portfolio to equity securities or fixed income securities.

The Fund’s subadvisers apply a rigorous, “bottom-up” research process to identify companies with strong fundamentals, skilled and committed management

teams and a clear market advantage. Through patient management, the Fund seeks to capture earnings growth from companies offering new or innovative technologies, products and services.

Peter Vanderlee, CFA, of ClearBridge, oversees the Fund’s allocation between equity and fixed income securities, as well as the Fund’s equity investments in

general, with a focus on dividend-paying securities. The ClearBridge portfolio management team also includes Patrick McElroy, CFA, and Tatiana Eades, who are focused on their respective areas of expertise: Mr. McElroy on real estate investment

trusts (“REITs”) and Ms. Eades on utilities. These individuals manage the equity side of the Fund with a “bottom-up” approach focused on the risk and reward of each investment opportunity.

A portfolio management team at Western Asset Management Company, LLC (“Western Asset”) manages the fixed income portion of the Fund. The fixed income portfolio

management team includes portfolio managers S. Kenneth Leech, Christopher F. Kilpatrick, Mark Lindbloom, Michael C. Buchanan and Ryan Brist. Their focus is on portfolio structure, including sector allocation, duration weighting and term structure

decisions.

Q. What were the overall market conditions during the Fund’s reporting period?

A. Equities delivered positive returns during the twelve-month reporting period ended November 30, 2023, with the broad market S&P 500 Indexi advancing

13.84%. Resilient corporate earnings among mega cap growth stocks and investor enthusiasm about the potential for artificial intelligence (“AI”) led to outsized returns by the information technology (“IT”) (+41.27%) and

communication services (+37.01%) sectors. Continued interest rate hikes by the Federal Reserve Board (the “Fed”) to tame inflation drove 10-year U.S. Treasury yields up from 3.60% to 4.33% and weighed on income-oriented sectors such

as utilities (-9.31%) and consumer staples (-5.11%). The health care sector (-4.02%) was also out of favor as a rise in health care system utilization following the pandemic raised costs.

|

|

|

|

|

| LMP Capital and Income Fund Inc. 2023 Annual Report |

|

|

|

1 |

Fund overview (cont’d)

Initial signs of progress in the Fed’s efforts to tame generationally high inflation

supported equities in the fourth quarter of 2022 and the first quarter of 2023, with strong performance among defensive and cyclical1 stocks. In March, markets focused on the U.S. banking system

after significant market losses in Silicon Valley Bank’s securities portfolio spurred a run on the bank’s deposits and resulted in the second-largest bank failure in U.S. history. This sparked a crisis of confidence across small and

midsize regional banks, as consumers shifted their deposits to larger banks perceived to be more stable. Although contagion concerns had eased by the end of the month, the crisis intensified concern over the probability and severity of a recession

as banks are likely to tighten lending standards.

Stocks rose in the second quarter of 2023 as investors took cooling inflation to mean the Fed’s tightening

cycle was nearing its conclusion. Simultaneously, enthusiasm grew over the potential applications and benefits of AI. The result was positive overall market performance with gains particularly concentrated in a handful of mega cap companies in the

IT, consumer discretionary and communication services sectors.

Market leadership began to broaden by the beginning of the third quarter of 2023 as

better-than-expected corporate earnings and cooling inflation created a growing chorus for a soft landing for the economy (rather than a recession). This helped provide a bid to smaller and more economically sensitive stocks on the hopes that the

Fed would reach its rate hike zenith, or even reduce rates, before the end of the year. However, as the quarter wore on, stubborn inflationary data, continued economic resiliency and surging Treasury yields pushed out rate cut expectations further

into the future.

Q. How did we respond to these changing market conditions?

A. The Fund invests in equity securities that exhibit an attractive income stream, including dividend-paying stocks, energy MLPs and REITs. With weakness in the

REIT sector, largely a result of rising rates, we became more positive on its prospects. We increased the Fund’s exposure to the REIT sector as a result of weak stock prices which, in our assessment, were discounting an overly pessimistic view

on the prospects of the sector. In increasing exposure, we emphasized those REITs with strong balance sheets, ample cash flows, leadership positions in their sectors and attractive valuations. Among new positions were Digital Realty Trust, Extra

Space Storage, Apartment Income REIT and American Homes 4 Rent. Also among REITs, we adjusted the Fund’s exposure to communication towers, adding to American Tower on weakness while exiting Crown Castle and SBA Communications. One source of

Funds for these pivots was the IT sector, which had been a very strong performer, and where we have found that valuations were elevated, increasing risk. In the IT sector we exited Texas Instruments, TE Connectivity and Cisco Systems and reduced

positions in NXP Semiconductors and Broadcom.

| 1 |

Cyclical consists of the following industries: automotive, entertainment, gaming, home construction, lodging, retailers,

restaurants, textiles and other consumer services. |

|

|

|

|

|

|

2 |

|

|

|

LMP Capital and Income Fund Inc. 2023 Annual Report |

Performance review

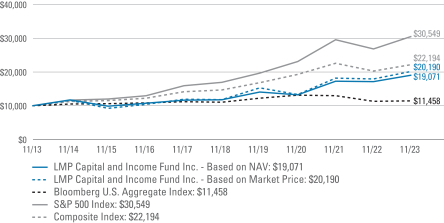

For the twelve months ended November 30, 2023, LMP Capital and Income Fund Inc. returned 11.18% based on its net asset value (“NAV”)ii and 12.51% based on its New York Stock Exchange (“NYSE”) market price per share. The Fund’s unmanaged benchmarks, the Bloomberg U.S. Aggregate Indexiii and the S&P 500 Index, returned 1.18% and 13.84%, respectively, for the same period. The Fund’s Composite Indexiv returned 9.39% over

the same time frame.

The Fund has adopted a managed distribution policy (the “Managed Distribution Policy”). Pursuant to this policy, the Fund intends to

make regular monthly distributions to common shareholders at a fixed rate per common share, which rate may be adjusted from time to time by the Fund’s Board of Directors. This policy has no impact on the Fund’s investment strategy and may

reduce the Fund’s NAV. The Fund’s manager believes the policy helps maintain the Fund’s competitiveness and may benefit the Fund’s market price and premium/ discount to the Fund’s NAV.

During the twelve-month period, the Fund made distributions to shareholders totaling $1.35 per share, of which $0.64 will be treated as a return of capital for tax

purposes.* The performance table shows the Fund’s twelve-month total return based on its NAV and market price as of November 30, 2023. Past performance is no guarantee of future results.

|

|

|

|

|

| Performance Snapshot as of November 30, 2023 |

|

| Price Per Share |

|

12-Month

Total Return** |

| $14.90 (NAV) |

|

|

11.18%† |

|

| $13.16 (Market Price) |

|

|

12.51%‡ |

|

All figures represent past performance and are not a guarantee of future results.

** Total returns are based on changes in NAV or market price, respectively. Returns reflect the deduction of all Fund expenses, including management fees, operating

expenses, and other Fund expenses. Returns do not reflect the deduction of brokerage commissions or taxes that investors may pay on distributions or the sale of shares.

† Total return assumes the reinvestment of all distributions, including returns of capital, at NAV.

‡ Total return assumes the reinvestment of all distributions, including returns of capital, in additional shares in accordance with the Fund’s Dividend

Reinvestment Plan.

Q. What were the leading contributors to performance?

A. On an absolute basis during the reporting period, the Fund’s greatest positive contributions to returns were found in the IT, energy and financials

sectors. Relative to the benchmark, overall stock selection contributed positively, in particular stock selection in the energy and financials sectors. Underweights to the health care and consumer staples sectors also contributed. In terms of

individual Fund holdings, leading contributors to

| * |

For the tax character of distributions paid during the fiscal year ended November 30, 2023, please refer to page 33

of this report. |

|

|

|

|

|

| LMP Capital and Income Fund Inc. 2023 Annual Report |

|

|

|

3 |

Fund overview (cont’d)

performance for the period included Broadcom, Microsoft, Magellan Midstream Partners, Energy

Transfer and Apple. In addition, the fixed income investments contributed to the overall return for the reporting period.

Q. What were the

leading detractors from performance?

A. On an absolute basis during the reporting period, the utilities and health care sectors were the primary

detractors from returns. Relative to the benchmark, overall sector allocation detracted from performance. Energy and utilities overweights and an underweight to the IT sector detracted. Stock selection in the health care, communication services,

industrials and utilities sectors also detracted. In terms of individual Fund holdings, leading detractors from performance for the period included Pfizer, NextEra Energy Partners LP, NextEra Energy, Bank of America and Alexandria Real Estate

Equities.

Q. Were there any significant changes to the Fund during the reporting period?

A. In addition to portfolio changes outlined above, during the period the Fund added positions in ONEOK in the energy sector, convertible preferred shares of

Apollo Global Management in the financials sector, 4.6% convertible preferred shares of NextEra Energy as well as PPL in the utilities sector, and Colgate-Palmolive in the consumer staples sector. The Fund exited 6% convertible preferred shares of

KKR in the financials sector, Danaher in the health care sector, RTX in the industrials sector, 6.219% corporate units of NextEra Energy in the utilities sector, and T-Mobile 5.25% convertible preferred shares, in the communication services sector.

Looking for additional information?

The

Fund is traded under the symbol “SCD” and its closing market price is available in most newspapers under the NYSE listings. The daily NAV is available online under the symbol “XSCDX” on most financial websites. Barron’s

and The Wall Street Journal’s Monday edition both carry closed-end fund tables that provide additional information.

In a continuing effort to

provide information concerning the Fund, shareholders may call 1-888-777-0102 (toll free), Monday through Friday from 8:00 a.m. to 5:30 p.m. Eastern Time, for the Fund’s current NAV, market price and other information.

Thank you for your investment in the LMP Capital and Income Fund Inc. As always, we appreciate that you have chosen us to manage your assets and we remain focused on

achieving the Fund’s investment goals.

Sincerely,

Peter Vanderlee, CFA

Portfolio Manager

ClearBridge

Investments, LLC

|

|

|

|

|

|

4 |

|

|

|

LMP Capital and Income Fund Inc. 2023 Annual Report |

Tatiana Eades

Portfolio Manager

ClearBridge Investments, LLC

Patrick McElroy, CFA

Portfolio Manager

ClearBridge

Investments, LLC

Western Asset Management Company, LLC

(Fixed Income Portion)

December 19, 2023

RISKS: The Fund is a non-diversified, closed-end management investment company designed primarily as a

long-term investment and not as a trading vehicle. The Fund is not intended to be a complete investment program and, due to the uncertainty inherent in all investments, there can be no assurance that the Fund will achieve its investment objective.

The Fund’s common stock is traded on the New York Stock Exchange. Similar to stocks, the Fund’s share price will fluctuate with market conditions and, at the time of sale, may be worth more or less than the original investment. Shares of

closed-end funds often trade at a discount to their net asset value. Because the Fund is non-diversified, it may be more susceptible to economic, political or regulatory events than a diversified fund. The Fund’s investments are subject to a

number of risks such as stock market and equity securities risk, MLP risk, fixed income securities risk, foreign investments risk, market events risk and portfolio management risk. Investments in MLP securities are subject to unique risks. The

Fund’s concentration of investments in energy related MLPs subjects it to the risks of MLPs and the energy sector, including the risks of declines in energy and commodity prices, decreases in energy demand, adverse weather conditions, natural

or other disasters, changes in government regulation, and changes in tax laws. MLP distributions are not guaranteed and there is no assurance that all such distributions will be tax deferred. Stock and bond prices are subject to fluctuation. As

interest rates rise, bond prices fall, reducing the value of the fixed income securities held by the Fund. Investing in foreign securities is subject to certain risks not associated with domestic investing, such as currency fluctuations and changes

in political, social, and economic conditions. These risks are magnified in emerging or developing markets. Emerging market countries tend to have economic, political, and legal systems that are less developed and are less stable than those of more

developed countries. The

|

|

|

|

|

| LMP Capital and Income Fund Inc. 2023 Annual Report |

|

|

|

5 |

Fund overview (cont’d)

Fund may invest in lower rated higher yielding bonds or “junk bonds”, which are

subject to greater liquidity and credit risk (risk of default) than higher rated obligations. The repositioning of the Fund’s portfolio may increase a shareholder’s risk of loss associated with an investment in the Fund’s shares.

Funds that invest in securities related to the real estate industry are subject to the risks of real estate markets, including fluctuating property values, changes in interest rates and other mortgage-related risks. The Fund may use derivatives,

such as options and futures, which can be illiquid, may disproportionately increase losses, and have a potentially large impact on Fund performance. Leverage may result in greater volatility of NAV and the market price of common shares and increases

a shareholder’s risk of loss. Dividends are not guaranteed, and a company may reduce or eliminate its dividend at any time. Distributions are not guaranteed and are subject to change. The Fund may also invest in money market funds, including

funds affiliated with the Fund’s manager and subadvisers. The market values of securities or other assets will fluctuate, sometimes sharply and unpredictably, due to changes in general market conditions, overall economic trends or events,

governmental actions or intervention, actions taken by the U.S. Federal Reserve or foreign central banks, market disruptions caused by trade disputes or other factors, political developments, armed conflicts, economic sanctions and countermeasures

in response to sanctions, major cybersecurity events, investor sentiment, the global and domestic effects of a pandemic, and other factors that may or may not be related to the issuer of the security or other asset. For more information on Fund

risk, see Summary of information regarding the Fund – Principal Risk Factors in this report.

Portfolio holdings and breakdowns are as of November 30,

2023 and are subject to change and may not be representative of the portfolio managers’ current or future investments. The Fund’s top ten holdings (as a percentage of net assets) as of November 30, 2023 were: Microsoft Corp. (7.0%),

Energy Transfer LP (5.9%), Enterprise Products Partners LP (5.0%), Apple Inc. (4.9%), Blackstone Inc. (4.8%), Sunoco LP (3.5%), Broadcom Inc.(3.4%), ONEOK Inc. (3.2%), Apollo Global Management Inc. (3.1%) and Plains GP Holdings LP (2.9%).

Please refer to pages 11 through 17 for a list and percentage breakdown of the Fund’s holdings.

The mention of sector breakdowns is for informational purposes

only and should not be construed as a recommendation to purchase or sell any securities. The information provided regarding such sectors is not a sufficient basis upon which to make an investment decision. Investors seeking financial advice

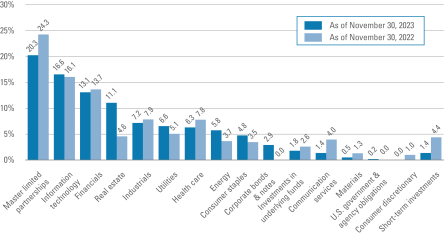

regarding the appropriateness of investing in any securities or investment strategies discussed should consult their financial professional. The Fund’s top five sector holdings (as a percentage of net assets) as of November 30, 2023 were:

master limited partnerships (25.2%), information technology (20.7%), financials (17.5%), real estate (13.8%) and industrials (9.2%). The Fund’s portfolio composition is subject to change at any time.

All investments are subject to risk including the possible loss of principal. Past performance is no guarantee of future results. All index performance reflects no

deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

The information provided is not intended to be a forecast of

future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

|

|

|

|

|

|

6 |

|

|

|

LMP Capital and Income Fund Inc. 2023 Annual Report |

| i |

The S&P 500 Index is an unmanaged index of the stocks of 500 leading companies, and is generally representative of the

performance of larger companies in the U.S. |

| ii |

Net asset value (“NAV”) is calculated by subtracting total liabilities, including liabilities associated with

financial leverage (if any), from the closing value of all securities held by the Fund (plus all other assets) and dividing the result (total net assets) by the total number of the common shares outstanding. The NAV fluctuates with changes in the

market prices of securities in which the Fund has invested. However, the price at which an investor may buy or sell shares of the Fund is the Fund’s market price as determined by supply of and demand for the Fund’s shares.

|

| iii |

The Bloomberg U.S. Aggregate Index is a broad-based bond index comprised of government, corporate, mortgage-and

asset-backed issues, rated investment grade or higher, and having at least one year to maturity. |

| iv |

The Composite Index reflects the blended rate of return of the following underlying indices: 65% S&P 500 Index and 35%

Bloomberg U.S. Aggregate Index. |

|

|

|

|

|

| LMP Capital and Income Fund Inc. 2023 Annual Report |

|

|

|

7 |

Fund at a glance† (unaudited)

Investment breakdown (%) as a percent of total

investments

| † |

The bar graph above represents the composition of the Fund’s investments as of November 30, 2023 and

November 30, 2022. The Fund is actively managed. As a result, the composition of the Fund’s investments is subject to change at any time. |

|

|

|

|

|

|

8 |

|

|

|

LMP Capital and Income Fund Inc. 2023 Annual Report |

Fund performance (unaudited)

|

|

|

|

|

| Net Asset Value |

|

|

|

| Average annual total returns1 |

|

|

|

| Twelve Months Ended 11/30/23 |

|

|

11.18 |

% |

| Five Years Ended 11/30/23 |

|

|

10.11 |

|

| Ten Years Ended 11/30/23 |

|

|

6.67 |

|

|

|

| Cumulative total returns1 |

|

|

|

| 11/30/13 through 11/30/23 |

|

|

90.71 |

% |

|

|

|

|

|

| Market Price |

|

|

|

| Average annual total returns2 |

|

|

|

| Twelve Months Ended 11/30/23 |

|

|

12.51 |

% |

| Five Years Ended 11/30/23 |

|

|

11.31 |

|

| Ten Years Ended 11/30/23 |

|

|

7.28 |

|

|

|

| Cumulative total returns2 |

|

|

|

| 11/30/13 through 11/30/23 |

|

|

101.90 |

% |

All figures represent past performance and are not a guarantee of future results. Returns reflect the deduction of all Fund expenses,

including management fees, operating expenses, and other Fund expenses. Returns do not reflect the deduction of brokerage commissions or taxes that investors may pay on distributions or the sale of shares.

| 1 |

Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value.

|

| 2 |

Assumes the reinvestment of all distributions, including returns of capital, if any, in additional shares in accordance

with the Fund’s Dividend Reinvestment Plan. |

|

|

|

|

|

| LMP Capital and Income Fund Inc. 2023 Annual Report |

|

|

|

9 |

Fund performance

(unaudited) (cont’d)

Historical performance

Value of $10,000 invested in

LMP Capital and Income Fund Inc. vs. Benchmark Indices† — November 2013 - November 2023

All figures represent past performance and are not a guarantee of future results. Returns reflect the deduction of all Fund

expenses, including management fees, operating expenses, and other Fund expenses. Returns do not reflect the deduction of brokerage commissions or taxes that investors may pay on distributions or the sale of shares.

| † |

Hypothetical illustration of $10,000 invested in LMP Capital and Income Fund Inc. on November 30, 2013, assuming the

reinvestment of all distributions, including returns of capital, if any, at net asset value and also assuming the reinvestment of all distributions, including returns of capital, if any, in additional shares in accordance with the Fund’s

Dividend Reinvestment Plan through November 30, 2023. The hypothetical illustration also assumes a $10,000 investment in the Bloomberg U.S. Aggregate Index, S&P 500 Index and the Composite Index (together, the “Indices”). The

Bloomberg U.S. Aggregate Index is a broad-based bond index comprised of government, corporate, mortgage- and asset-backed issues, rated investment grade or higher, and having at least one year to maturity. The S&P 500 Index is an unmanaged index

of the stocks of 500 leading companies and is generally representative of the performance of larger companies in the U.S. The Composite Index reflects the blended rate of return of the following underlying indices: 65% S&P 500 Index and 35%

Bloomberg U.S. Aggregate Index. The Indices are unmanaged and are not subject to the same management and trading expenses as a mutual fund. Please note that an investor cannot invest directly in an index. |

|

|

|

|

|

|

10 |

|

|

|

LMP Capital and Income Fund Inc. 2023 Annual Report |

Schedule of investments

November 30, 2023

LMP Capital and Income Fund Inc.

(Percentages shown based on Fund net assets)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Security |

|

|

|

|

|

|

|

Shares |

|

|

Value |

|

| Common Stocks — 85.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Communication Services — 1.3% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Wireless Telecommunication Services —

1.3% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| T-Mobile US Inc. |

|

|

|

|

|

|

|

|

|

|

21,400 |

|

|

$ |

3,219,630 |

|

| Consumer Staples — 5.9% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Beverages — 2.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Coca-Cola Co. |

|

|

|

|

|

|

|

|

|

|

99,210 |

|

|

|

5,797,833 |

(a)

|

| Food Products —

1.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| McCormick & Co. Inc., Non Voting Shares |

|

|

|

|

|

|

|

|

|

|

47,600 |

|

|

|

3,085,908 |

|

| Household Products —

2.5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Colgate-Palmolive Co. |

|

|

|

|

|

|

|

|

|

|

41,400 |

|

|

|

3,261,078 |

|

| Procter & Gamble Co. |

|

|

|

|

|

|

|

|

|

|

19,860 |

|

|

|

3,048,907 |

(a) |

| Total Household Products |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6,309,985 |

|

| Total Consumer Staples |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15,193,726 |

|

| Energy — 7.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Oil, Gas & Consumable Fuels —

7.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ConocoPhillips |

|

|

|

|

|

|

|

|

|

|

23,300 |

|

|

|

2,692,781 |

|

| DT Midstream Inc. |

|

|

|

|

|

|

|

|

|

|

43,000 |

|

|

|

2,463,470 |

|

| Enbridge Inc. |

|

|

|

|

|

|

|

|

|

|

41,960 |

|

|

|

1,463,145 |

|

| ONEOK Inc. |

|

|

|

|

|

|

|

|

|

|

119,779 |

|

|

|

8,246,784 |

(a) |

| Williams Cos. Inc. |

|

|

|

|

|

|

|

|

|

|

96,740 |

|

|

|

3,559,065 |

(a) |

| Total Energy |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18,425,245 |

|

| Financials — 13.3% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Banks — 2.4% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| JPMorgan Chase & Co. |

|

|

|

|

|

|

|

|

|

|

39,480 |

|

|

|

6,162,038 |

(a) |

| Capital Markets —

8.9% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Blackstone Inc. |

|

|

|

|

|

|

|

|

|

|

109,710 |

|

|

|

12,328,113 |

(a) |

| Blue Owl Capital Inc. |

|

|

|

|

|

|

|

|

|

|

394,200 |

|

|

|

5,313,816 |

|

| CME Group Inc. |

|

|

|

|

|

|

|

|

|

|

6,680 |

|

|

|

1,458,645 |

|

| Goldman Sachs Group Inc. |

|

|

|

|

|

|

|

|

|

|

4,700 |

|

|

|

1,605,238 |

|

| Intercontinental Exchange Inc. |

|

|

|

|

|

|

|

|

|

|

9,930 |

|

|

|

1,130,431 |

|

| Trinity Capital Inc. |

|

|

|

|

|

|

|

|

|

|

59,691 |

|

|

|

881,039 |

|

| Total Capital Markets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

22,717,282 |

|

| Insurance — 1.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Chubb Ltd. |

|

|

|

|

|

|

|

|

|

|

13,590 |

|

|

|

3,117,954 |

|

| Mortgage Real Estate Investment Trusts

(REITs) — 0.8% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| AGNC Investment Corp. |

|

|

|

|

|

|

|

|

|

|

231,900 |

|

|

|

2,045,358 |

|

| Total Financials |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

34,042,632 |

|

See Notes to Financial

Statements.

|

|

|

|

|

| LMP Capital and Income Fund Inc. 2023 Annual Report |

|

|

|

11 |

Schedule of investments (cont’d)

November 30, 2023

LMP Capital and Income Fund Inc.

(Percentages shown based on Fund net assets)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Security |

|

|

|

|

|

|

|

Shares |

|

|

Value |

|

| Health Care — 7.9% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Biotechnology —

1.7% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| AbbVie Inc. |

|

|

|

|

|

|

|

|

|

|

19,900 |

|

|

$ |

2,833,561 |

|

| Amgen Inc. |

|

|

|

|

|

|

|

|

|

|

5,190 |

|

|

|

1,399,431 |

|

| Total Biotechnology |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4,232,992 |

|

| Health Care Equipment & Supplies

— 0.9% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Abbott Laboratories |

|

|

|

|

|

|

|

|

|

|

22,700 |

|

|

|

2,367,383 |

|

| Pharmaceuticals —

5.3% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Eli Lilly & Co. |

|

|

|

|

|

|

|

|

|

|

3,700 |

|

|

|

2,186,848 |

|

| Johnson & Johnson |

|

|

|

|

|

|

|

|

|

|

17,156 |

|

|

|

2,653,347 |

(a) |

| Merck & Co. Inc. |

|

|

|

|

|

|

|

|

|

|

64,600 |

|

|

|

6,620,208 |

(a) |

| Pfizer Inc. |

|

|

|

|

|

|

|

|

|

|

71,008 |

|

|

|

2,163,614 |

|

| Total Pharmaceuticals |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13,624,017 |

|

| Total Health Care |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

20,224,392 |

|

| Industrials — 8.9% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Aerospace & Defense —

2.8% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| L3Harris Technologies Inc. |

|

|

|

|

|

|

|

|

|

|

14,700 |

|

|

|

2,804,907 |

(a) |

| Lockheed Martin Corp. |

|

|

|

|

|

|

|

|

|

|

9,878 |

|

|

|

4,423,072 |

(a) |

| Total Aerospace &

Defense |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7,227,979 |

|

| Air Freight & Logistics —

0.5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| United Parcel Service Inc., Class B Shares |

|

|

|

|

|

|

|

|

|

|

8,760 |

|

|

|

1,328,103 |

(a) |

| Electrical Equipment —

0.9% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Emerson Electric Co. |

|

|

|

|

|

|

|

|

|

|

25,720 |

|

|

|

2,286,508 |

(a) |

| Ground Transportation —

2.6% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Union Pacific Corp. |

|

|

|

|

|

|

|

|

|

|

29,200 |

|

|

|

6,577,884 |

(a) |

| Machinery — 1.8% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Otis Worldwide Corp. |

|

|

|

|

|

|

|

|

|

|

54,510 |

|

|

|

4,676,413 |

(a) |

| Professional Services —

0.3% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Paychex Inc. |

|

|

|

|

|

|

|

|

|

|

5,170 |

|

|

|

630,585 |

(a) |

| Total Industrials |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

22,727,472 |

|

| Information Technology — 20.7% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Electronic Equipment, Instruments &

Components — 1.0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Amphenol Corp., Class A Shares |

|

|

|

|

|

|

|

|

|

|

27,500 |

|

|

|

2,502,225 |

|

| Semiconductors & Semiconductor

Equipment — 6.1% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Broadcom Inc. |

|

|

|

|

|

|

|

|

|

|

9,267 |

|

|

|

8,578,740 |

(a) |

| NXP Semiconductors NV |

|

|

|

|

|

|

|

|

|

|

4,240 |

|

|

|

865,299 |

|

| QUALCOMM Inc. |

|

|

|

|

|

|

|

|

|

|

46,940 |

|

|

|

6,057,607 |

(a) |

| Total Semiconductors &

Semiconductor Equipment |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15,501,646 |

|

See Notes to Financial

Statements.

|

|

|

|

|

|

12 |

|

|

|

LMP Capital and Income Fund Inc. 2023 Annual Report |

LMP Capital and Income Fund Inc.

(Percentages shown based on Fund net assets)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Security |

|

|

|

|

|

|

|

Shares |

|

|

Value |

|

| Software — 8.7% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Microsoft Corp. |

|

|

|

|

|

|

|

|

|

|

47,330 |

|

|

$ |

17,933,810 |

(a) |

| Oracle Corp. |

|

|

|

|

|

|

|

|

|

|

37,690 |

|

|

|

4,379,955 |

(a) |

| Total Software |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

22,313,765 |

|

| Technology Hardware, Storage &

Peripherals — 4.9% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Apple Inc. |

|

|

|

|

|

|

|

|

|

|

65,530 |

|

|

|

12,447,423 |

(a) |

| Total Information Technology |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

52,765,059 |

|

| Materials — 0.6% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Chemicals — 0.6% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Huntsman Corp. |

|

|

|

|

|

|

|

|

|

|

60,050 |

|

|

|

1,477,230 |

(a) |

| Real Estate — 13.8% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Health Care REITs —

0.3% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Global Medical REIT Inc. |

|

|

|

|

|

|

|

|

|

|

72,500 |

|

|

|

727,175 |

|

| Industrial REITs —

2.1% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Prologis Inc. |

|

|

|

|

|

|

|

|

|

|

47,700 |

|

|

|

5,482,161 |

(a) |

| Residential REITs —

2.5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| American Homes 4 Rent, Class A Shares |

|

|

|

|

|

|

|

|

|

|

63,800 |

|

|

|

2,314,026 |

|

| Apartment Income REIT Corp. |

|

|

|

|

|

|

|

|

|

|

74,200 |

|

|

|

2,309,104 |

|

| Equity LifeStyle Properties Inc. |

|

|

|

|

|

|

|

|

|

|

24,330 |

|

|

|

1,729,863 |

|

| Total Residential REITs |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6,352,993 |

|

| Specialized REITs —

8.9% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| American Tower Corp. |

|

|

|

|

|

|

|

|

|

|

26,490 |

|

|

|

5,530,582 |

(a) |

| Digital Realty Trust Inc. |

|

|

|

|

|

|

|

|

|

|

38,800 |

|

|

|

5,384,664 |

|

| Equinix Inc. |

|

|

|

|

|

|

|

|

|

|

5,410 |

|

|

|

4,409,204 |

(a) |

| Extra Space Storage Inc. |

|

|

|

|

|

|

|

|

|

|

29,900 |

|

|

|

3,892,083 |

|

| Gaming and Leisure Properties Inc. |

|

|

|

|

|

|

|

|

|

|

74,677 |

|

|

|

3,489,657 |

(a) |

| Total Specialized REITs |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

22,706,190 |

|

| Total Real Estate |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

35,268,519 |

|

| Utilities — 5.6% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Electric Utilities —

1.7% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| PPL Corp. |

|

|

|

|

|

|

|

|

|

|

169,600 |

|

|

|

4,429,952 |

|

| Multi-Utilities —

3.9% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| DTE Energy Co. |

|

|

|

|

|

|

|

|

|

|

43,825 |

|

|

|

4,562,621 |

|

| Sempra |

|

|

|

|

|

|

|

|

|

|

72,360 |

|

|

|

5,272,873 |

(a) |

| Total Multi-Utilities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9,835,494 |

|

| Total Utilities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14,265,446 |

|

| Total Common Stocks (Cost —

$146,653,265) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

217,609,351 |

|

See Notes to Financial

Statements.

|

|

|

|

|

| LMP Capital and Income Fund Inc. 2023 Annual Report |

|

|

|

13 |

Schedule of investments (cont’d)

November 30, 2023

LMP Capital and Income Fund Inc.

(Percentages shown based on Fund net assets)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Security |

|

|

|

|

|

|

|

Shares/Units |

|

|

Value |

|

| Master Limited Partnerships — 25.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Diversified Energy Infrastructure —

13.8% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Energy Transfer LP |

|

|

|

|

|

|

|

|

|

|

1,087,280 |

|

|

$ |

15,102,319 |

(a) |

| Enterprise Products Partners LP |

|

|

|

|

|

|

|

|

|

|

472,780 |

|

|

|

12,661,049 |

(a) |

| Plains GP Holdings LP, Class A Shares |

|

|

|

|

|

|

|

|

|

|

463,340 |

|

|

|

7,487,574 |

* |

| Total Diversified Energy

Infrastructure |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

35,250,942 |

|

| Oil/Refined Products —

7.6% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| CrossAmerica Partners LP |

|

|

|

|

|

|

|

|

|

|

151,970 |

|

|

|

3,606,248 |

(a) |

| MPLX LP |

|

|

|

|

|

|

|

|

|

|

188,500 |

|

|

|

6,872,710 |

(a) |

| Sunoco LP |

|

|

|

|

|

|

|

|

|

|

165,300 |

|

|

|

9,035,298 |

(a) |

| Total Oil/Refined

Products |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

19,514,256 |

|

| Petrochemicals —

2.1% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Westlake Chemical Partners LP |

|

|

|

|

|

|

|

|

|

|

239,536 |

|

|

|

5,425,490 |

(a) |

| Power Generation —

0.4% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| NextEra Energy Partners LP |

|

|

|

|

|

|

|

|

|

|

37,500 |

|

|

|

882,750 |

|

| Propane — 1.3% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Suburban Propane Partners LP |

|

|

|

|

|

|

|

|

|

|

200,000 |

|

|

|

3,430,000 |

(a) |

| Total Master Limited Partnerships (Cost —

$25,243,990) |

|

|

|

64,503,438 |

|

|

|

|

|

|

| |

|

Rate |

|

|

|

|

|

Shares |

|

|

|

|

| Convertible Preferred Stocks — 6.3% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Communication Services — 0.5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Media — 0.5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Paramount Global, Non Voting Shares |

|

|

5.750 |

% |

|

|

|

|

|

|

67,964 |

|

|

|

1,344,328 |

|

| Financials — 3.1% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Financial Services —

3.1% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Apollo Global Management Inc. |

|

|

6.750 |

% |

|

|

|

|

|

|

142,451 |

|

|

|

7,904,606 |

|

| Utilities — 2.7% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Electric Utilities —

2.3% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| NextEra Energy Inc. |

|

|

6.926 |

% |

|

|

|

|

|

|

154,200 |

|

|

|

5,711,568 |

|

| Gas Utilities —

0.4% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Spire Inc. |

|

|

7.500 |

% |

|

|

|

|

|

|

23,100 |

|

|

|

1,079,347 |

|

| Total Utilities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6,790,915 |

|

| Total Convertible Preferred Stocks (Cost —

$20,167,228) |

|

|

|

|

|

|

|

16,039,849 |

|

See Notes to Financial

Statements.

|

|

|

|

|

|

14 |

|

|

|

LMP Capital and Income Fund Inc. 2023 Annual Report |

LMP Capital and Income Fund Inc.

(Percentages shown based on Fund net assets)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Security |

|

Rate |

|

|

Maturity

Date |

|

|

Face

Amount |

|

|

Value |

|

| Corporate Bonds & Notes — 3.7% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Communication Services — 0.7% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Entertainment —

0.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Netflix Inc., Senior Notes |

|

|

5.375 |

% |

|

|

11/15/29 |

|

|

$ |

400,000 |

|

|

$ |

402,890 |

(b) |

| Walt Disney Co., Senior Notes |

|

|

2.000 |

% |

|

|

9/1/29 |

|

|

|

300,000 |

|

|

|

259,180 |

|

| Total Entertainment |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

662,070 |

|

| Interactive Media & Services —

0.1% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Match Group Holdings II LLC, Senior Notes |

|

|

3.625 |

% |

|

|

10/1/31 |

|

|

|

250,000 |

|

|

|

204,534 |

(b) |

| Media — 0.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Charter Communications Operating LLC/Charter Communications Operating Capital Corp.,

Senior Secured Notes |

|

|

6.384 |

% |

|

|

10/23/35 |

|

|

|

200,000 |

|

|

|

196,465 |

|

| Comcast Corp., Senior Notes |

|

|

4.250 |

% |

|

|

10/15/30 |

|

|

|

400,000 |

|

|

|

381,426 |

|

| Total Media |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

577,891 |

|

| Wireless Telecommunication Services —

0.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| T-Mobile USA Inc., Senior Notes |

|

|

3.875 |

% |

|

|

4/15/30 |

|

|

|

500,000 |

|

|

|

459,384 |

|

| Total Communication

Services |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1,903,879 |

|

| Consumer Discretionary — 0.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Automobiles — 0.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Ford Motor Co., Senior Notes |

|

|

3.250 |

% |

|

|

2/12/32 |

|

|

|

550,000 |

|

|

|

438,878 |

|

| Consumer Staples — 0.3% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Food Products —

0.1% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Lamb Weston Holdings Inc., Senior Notes |

|

|

4.375 |

% |

|

|

1/31/32 |

|

|

|

400,000 |

|

|

|

349,047 |

(b)

|

| Personal Care Products —

0.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Kenvue Inc., Senior Notes |

|

|

4.900 |

% |

|

|

3/22/33 |

|

|

|

400,000 |

|

|

|

396,719 |

|

| Total Consumer Staples |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

745,766 |

|

| Financials — 1.1% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Banks — 0.9% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Bank of America Corp., Senior Notes (5.015% to 7/22/32 then SOFR + 2.160%) |

|

|

5.015 |

% |

|

|

7/22/33 |

|

|

|

400,000 |

|

|

|

380,200 |

(c) |

| Citigroup Inc., Subordinated Notes (6.174% to 5/25/33 then SOFR + 2.661%) |

|

|

6.174 |

% |

|

|

5/25/34 |

|

|

|

700,000 |

|

|

|

694,885 |

(c) |

| JPMorgan Chase & Co., Subordinated Notes (5.717% to 9/14/32 then SOFR +

2.580%) |

|

|

5.717 |

% |

|

|

9/14/33 |

|

|

|

700,000 |

|

|

|

697,847 |

(c) |

| Wells Fargo & Co., Senior Notes (4.897% to 7/25/32 then SOFR + 2.100%) |

|

|

4.897 |

% |

|

|

7/25/33 |

|

|

|

500,000 |

|

|

|

467,852 |

(c) |

| Total Banks |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2,240,784 |

|

See Notes to Financial

Statements.

|

|

|

|

|

| LMP Capital and Income Fund Inc. 2023 Annual Report |

|

|

|

15 |

Schedule of investments (cont’d)

November 30, 2023

LMP Capital and Income Fund Inc.

(Percentages shown based on Fund net assets)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Security |

|

Rate |

|

|

Maturity

Date |

|

|

Face

Amount |

|

|

Value |

|

| Consumer Finance —

0.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| American Express Co., Senior Notes (5.043% to 5/1/33 then SOFR + 1.835%) |

|

|

5.043 |

% |

|

|

5/1/34 |

|

|

$ |

500,000 |

|

|

$ |

482,345 |

(c) |

| Total Financials |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2,723,129 |

|

| Health Care — 0.8% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Biotechnology —

0.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Amgen Inc., Senior Notes |

|

|

5.250 |

% |

|

|

3/2/33 |

|

|

|

400,000 |

|

|

|

396,113 |

|

| Health Care Providers & Services

— 0.5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Centene Corp., Senior Notes |

|

|

3.000 |

% |

|

|

10/15/30 |

|

|

|

600,000 |

|

|

|

501,147 |

|

| CVS Health Corp., Senior Notes |

|

|

3.750 |

% |

|

|

4/1/30 |

|

|

|

600,000 |

|

|

|

549,134 |

|

| UnitedHealth Group Inc., Senior Notes |

|

|

5.000 |

% |

|

|

10/15/24 |

|

|

|

250,000 |

|

|

|

249,125 |

|

| Total Health Care Providers &

Services |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1,299,406 |

|

| Pharmaceuticals —

0.1% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Pfizer Investment Enterprises Pte Ltd., Senior Notes |

|

|

4.750 |

% |

|

|

5/19/33 |

|

|

|

400,000 |

|

|

|

389,287 |

|

| Total Health Care |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2,084,806 |

|

| Industrials — 0.3% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Aerospace & Defense —

0.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Northrop Grumman Corp., Senior Notes |

|

|

4.750 |

% |

|

|

6/1/43 |

|

|

|

500,000 |

|

|

|

450,743 |

|

| Trading Companies & Distributors

— 0.1% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| United Rentals North America Inc., Senior Notes |

|

|

3.750 |

% |

|

|

1/15/32 |

|

|

|

350,000 |

|

|

|

296,711 |

|

| Total Industrials |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

747,454 |

|

| Materials — 0.3% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Containers & Packaging —

0.1% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Ball Corp., Senior Notes |

|

|

3.125 |

% |

|

|

9/15/31 |

|

|

|

400,000 |

|

|

|

330,655 |

|

| Metals & Mining —

0.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Freeport-McMoRan Inc., Senior Notes |

|

|

5.450 |

% |

|

|

3/15/43 |

|

|

|

500,000 |

|

|

|

448,962 |

|

| Total Materials |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

779,617 |

|

| Total Corporate Bonds &

Notes (Cost —$9,570,990) |

|

|

|

|

|

|

|

|

|

|

|

9,423,529 |

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

Shares |

|

|

|

|

| Investments in Underlying Funds — 2.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Ares Capital Corp. (Cost — $5,260,817) |

|

|

|

|

|

|

|

|

|

|

286,890 |

|

|

|

5,686,160 |

(a)(d)

|

| U.S. government & agency obligations — 0.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| U.S. Treasury Notes (Cost — $490,319) |

|

|

1.500 |

% |

|

|

2/29/24 |

|

|

|

495,000 |

|

|

|

490,269 |

|

| Total Investments before

Short-Term Investments (Cost — $207,386,609) |

|

|

|

313,752,596 |

|

See Notes to Financial

Statements.

|

|

|

|

|

|

16 |

|

|

|

LMP Capital and Income Fund Inc. 2023 Annual Report |

LMP Capital and Income Fund Inc.

(Percentages shown based on Fund net assets)

|

|

|

|

|

|

|

|

|

|

|

|

|

| Security |

|

Rate |

|

|

Shares |

|

|

Value |

|

| Short-Term Investments — 1.7% |

|

|

|

|

|

|

|

|

|

|

|

|

| Dreyfus Government Cash Management, Institutional Shares |

|

|

5.241 |

% |

|

|

30,608 |

|

|

$ |

30,608 |

(e) |

| JPMorgan 100% U.S. Treasury Securities Money Market Fund, Institutional Class |

|

|

5.231 |

% |

|

|

4,306,543 |

|

|

|

4,306,543 |

(e) |

| Total Short-Term Investments (Cost —

$4,337,151) |

|

|

|

|

|

|

|

|

|

|

4,337,151 |

|

| Total Investments — 124.5% (Cost —

$211,723,760) |

|

|

|

|

|

|

|

|

|

|

318,089,747 |

|

| Liabilities in Excess of Other Assets —

(24.5)% |

|

|

|

|

|

|

|

|

|

|

(62,660,476 |

) |

| Total Net Assets —

100.0% |

|

|

|

|

|

|

|

|

|

$ |

255,429,271 |

|

| * |

Non-income producing security. |

| (a) |

All or a portion of this security is pledged as collateral pursuant to the loan agreement (Note 5). |

| (b) |

Security is exempt from registration under Rule 144A of the Securities Act of 1933. This security may be resold in

transactions that are exempt from registration, normally to qualified institutional buyers. This security has been deemed liquid pursuant to guidelines approved by the Board of Directors. |

| (c) |

Variable rate security. Interest rate disclosed is as of the most recent information available. Certain variable rate

securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions. These securities do not indicate a reference rate and spread in their description above.

|

| (d) |

Security is a business development company (Note 1). |

| (e) |

Rate shown is one-day yield as of the end of the reporting period. |

|

|

|

| Abbreviation(s) used in this

schedule: |

|

|

| REIT |

|

— Real Estate Investment Trust |

|

|

| SOFR |

|

— Secured Overnight Financing Rate |

See Notes to Financial

Statements.

|

|

|

|

|

| LMP Capital and Income Fund Inc. 2023 Annual Report |

|

|

|

17 |

Statement of assets and liabilities

November 30, 2023

|

|

|

|

|

|

|

| Assets: |

|

|

|

|

| Investments, at value (Cost — $211,723,760) |

|

$ |

318,089,747 |

|

| Dividends and interest receivable |

|

|

655,592 |

|

| Prepaid expenses |

|

|

2,685 |

|

| Total Assets |

|

|

318,748,024 |

|

|

|

| Liabilities: |

|

|

|

|

| Loan payable (Note 5) |

|

|

61,000,000 |

|

| Distributions payable |

|

|

1,936,571 |

|

| Investment management fee payable |

|

|

215,306 |

|

| Directors’ fees payable |

|

|

11,142 |

|

| Interest expense payable |

|

|

10,353 |

|

| Accrued expenses |

|

|

145,381 |

|

| Total Liabilities |

|

|

63,318,753 |

|

| Total Net Assets |

|

$ |

255,429,271 |

|

|

|

| Net Assets: |

|

|

|

|

| Par value ($0.001 par value; 17,137,794 shares issued and outstanding; 100,000,000 shares

authorized) |

|

$ |

17,138 |

|

| Paid-in capital in excess of par value |

|

|

155,724,872 |

|

| Total distributable earnings (loss) |

|

|

99,687,261 |

|

| Total Net Assets |

|

$ |

255,429,271 |

|

|

|

| Shares Outstanding |

|

|

17,137,794 |

|

|

|

| Net Asset Value |

|

|

$14.90 |

|

See Notes to Financial

Statements.

|

|

|

|

|

|

18 |

|

|

|

LMP Capital and Income Fund Inc. 2023 Annual Report |